Breakfast Food Market Size 2026-2030

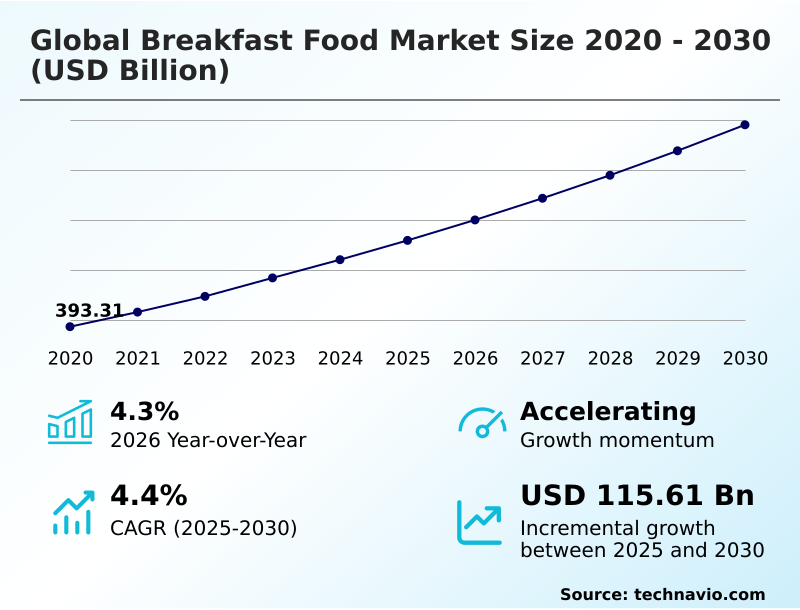

The breakfast food market size is valued to increase by USD 115.61 billion, at a CAGR of 4.4% from 2025 to 2030. Mainstreaming of functional convenience and industrialization of on-the-go nutritive solutions will drive the breakfast food market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 33.4% growth during the forecast period.

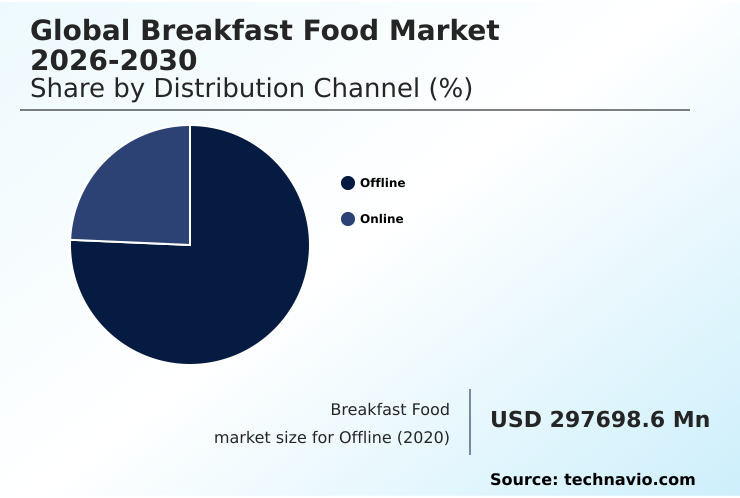

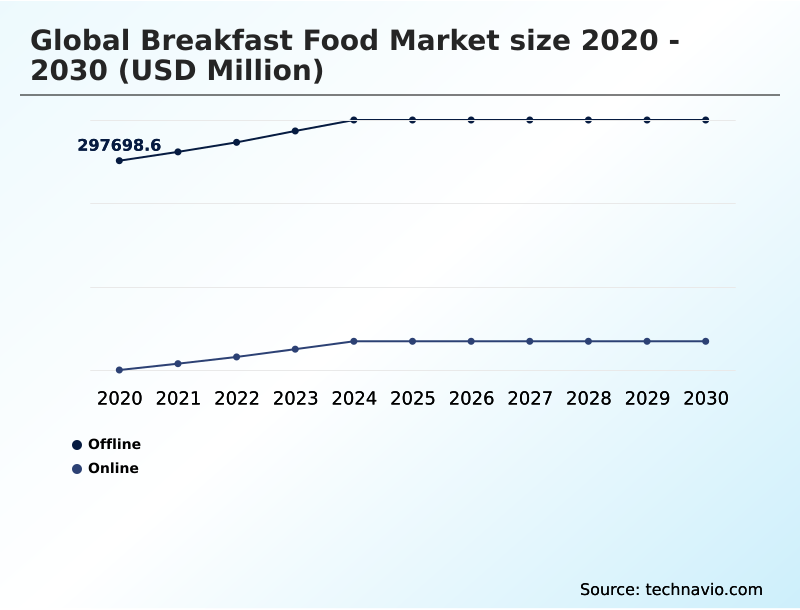

- By Distribution Channel - Offline segment was valued at USD 336.99 billion in 2024

- By Type - Bakery products segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 201.91 billion

- Market Future Opportunities: USD 115.61 billion

- CAGR from 2025 to 2030 : 4.4%

Market Summary

- The breakfast food market is undergoing a significant transformation, driven by a consumer shift towards health and wellness. This evolution is compelling manufacturers to move beyond traditional formulations and embrace nutrient-dense formats and clean-label ingredients. The demand for functional convenience has spurred innovation in ready-to-eat cereals and on-the-go nutritive solutions, designed for busy lifestyles.

- Technologies such as high-pressure processing (HPP) and advanced extrusion for cereal texture are crucial in preserving the organoleptic properties and nutritional value of products. A key business scenario involves the strategic recipe reformulation of a legacy product line to comply with new front-of-package labeling requirements.

- This requires balancing the reduction of high glycemic indices with maintaining taste and shelf-life, often through the integration of high-potency sweeteners and plant-based proteins. Success in this landscape depends on aligning product development with ethical sourcing standards and the growing consumer preference for foods that support metabolic stability and overall well-being.

- This shift is not just about ingredients but also about processing and packaging innovations that ensure product integrity and consumer appeal.

What will be the Size of the Breakfast Food Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Breakfast Food Market Segmented?

The breakfast food industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Distribution channel

- Offline

- Online

- Type

- Bakery products

- Ready meals

- Cereals

- Snack bars

- Others

- Product

- RTE

- RTC

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- India

- Japan

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

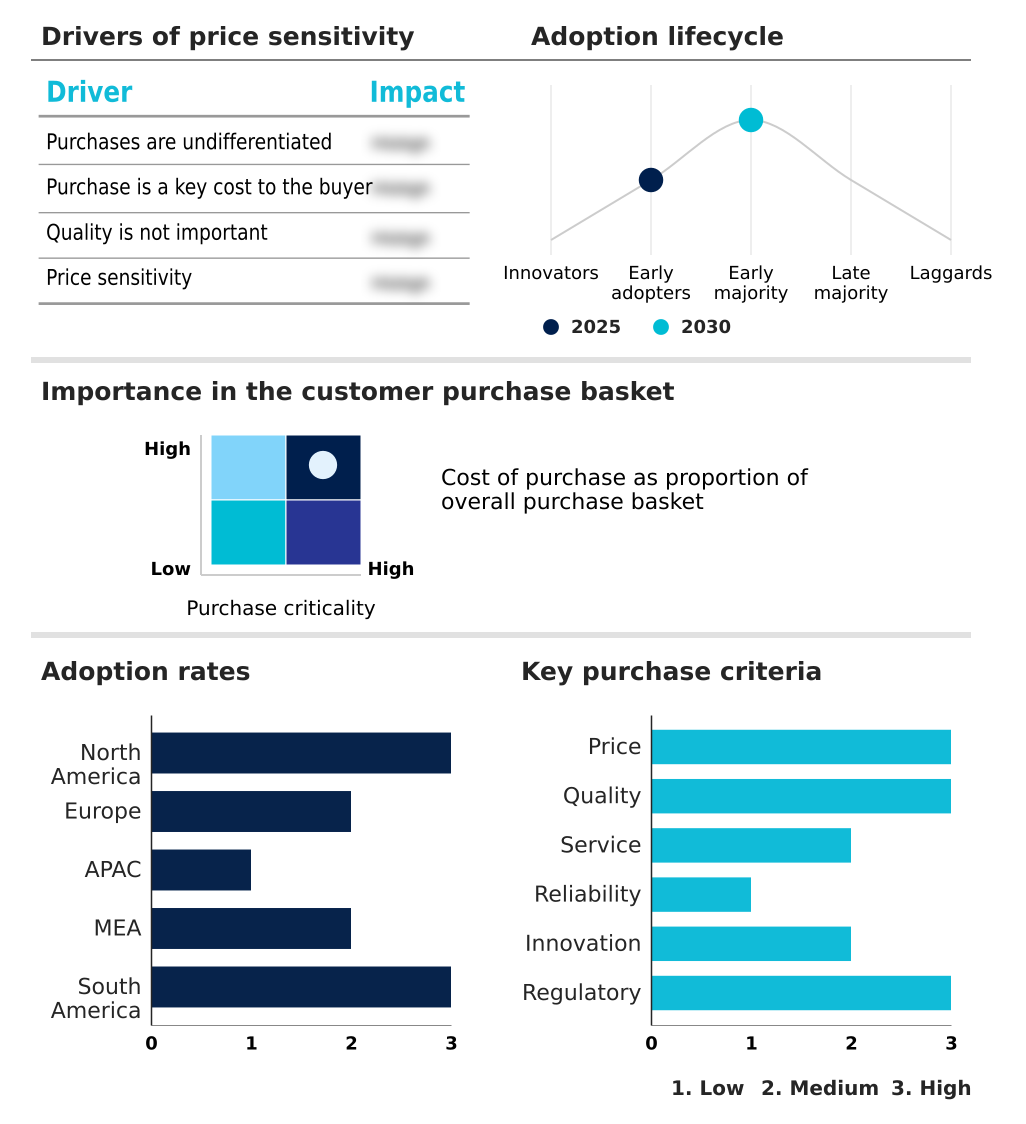

By Distribution Channel Insights

The offline segment is estimated to witness significant growth during the forecast period.

The offline segment remains the foundational pillar of the breakfast food market, driven by the immediate availability of perishable staples and a high degree of consumer trust in physical product inspection.

Supermarkets and hypermarkets utilize sophisticated shelf-management strategies and in-store promotions, which influence a significant portion of impulse purchasing decisions for new product lines. This channel is evolving through the integration of click-and-collect models, blending digital convenience with local inventory.

The demand for artisanal breakfast products is supported by the tactile and sensory shopping environment of high-end grocers.

As retailers invest in automation, the offline channel provides the essential infrastructure for both daily household replenishment and the distribution of specialized items like savory porridges and probiotic-rich yogurts, addressing consumer demand for both convenience and high-potency sweeteners in their choices.

The Offline segment was valued at USD 336.99 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 33.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Breakfast Food Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the breakfast food market is shifting, with APAC emerging as the primary growth engine, projected to contribute 33.4% of incremental growth.

The region's expansion, with a 5.5% CAGR, significantly outpaces mature markets like North America, which is growing at 3.9%.

This growth is fueled by rising disposable incomes and the rapid adoption of Western breakfast habits, including a demand for high-protein functionalism and nutrient-dense formats.

In contrast, North America and Europe are focused on the premiumization of existing categories, with an emphasis on performance-oriented formats and hyper-convenient hybrid meal kits.

Manufacturers are tailoring products to regional tastes, introducing savory porridges in Asia while focusing on fortified vitamins and minerals in Western markets to meet diverse consumer health objectives and preferences.

Market Dynamics

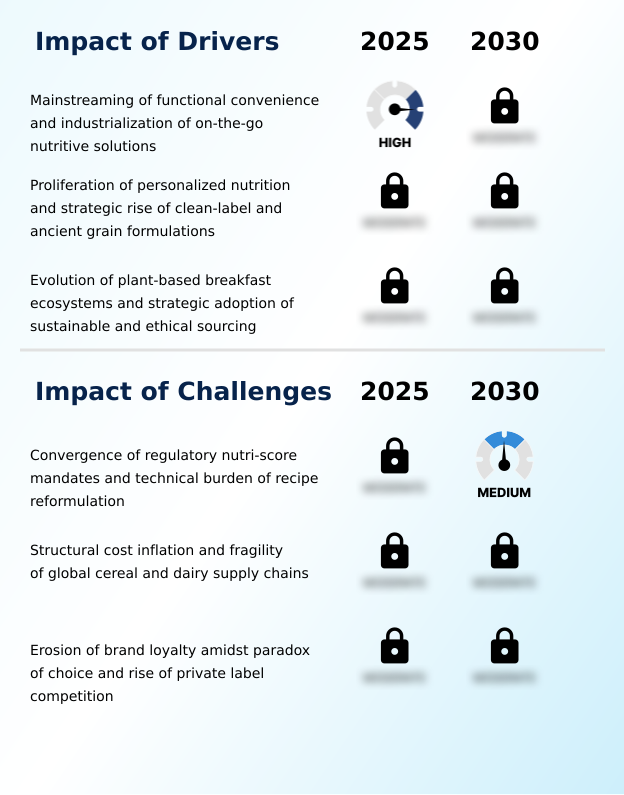

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global breakfast food market 2026-2030 is increasingly defined by consumer demand for products that align with specific health goals, such as breakfast food for metabolic stability and managing blood sugar with breakfast. This has accelerated the trend of high-protein functionalism in ready meals and the development of clean-label ancient grain formulations.

- Manufacturers are focused on creating on-the-go nutritive solutions that do not compromise on nutritional value. Central to this is the advancement of plant-based breakfast ecosystem development, which addresses both health and ethical sourcing in breakfast food. However, the industry faces significant hurdles, including the operational impact of nutri-score on cereals and the overarching challenge of supply chain fragility breakfast foods.

- In this competitive environment, the rise of private label competition breakfast bars forces established brands to innovate continuously. Technological advancements are key, with extrusion technology for cereal texture and high-pressure processing for breakfast meals enabling the creation of superior products. Innovations in packaging, like resealable pouches for breakfast snacks, enhance consumer convenience and extend shelf life.

- Companies that effectively manage the organoleptic properties of frozen breakfast products while ensuring their offerings are rich in fortified vitamins in ready-to-eat cereals are better positioned for success. Firms leveraging advanced analytics for supply chain planning have reported a 25% reduction in waste compared to those using traditional methods, highlighting the importance of operational efficiency.

What are the key market drivers leading to the rise in the adoption of Breakfast Food Industry?

- The market's primary growth driver is the mainstreaming of functional convenience, underscored by the industrialization of on-the-go nutritive solutions for time-constrained consumers.

- Market growth is primarily propelled by the mainstreaming of functional convenience and the industrialization of on-the-go nutritive solutions.

- The convenience factor is now a primary purchase driver for over 60% of consumers in metropolitan areas, fueling demand for products like ready-to-eat cereals and breakfast bars.

- This is supported by the expansion of direct-to-consumer digital channels, through which firms report a 20% increase in customer lifetime value.

- The strategic adoption of sustainable and ethical sourcing is also becoming a significant driver, appealing to a growing base of conscious consumers.

- As the focus on metabolic stability and long-term satiety intensifies, manufacturers are innovating with high-protein and fiber-rich formulations, creating high-value growth opportunities and increasing household penetration.

What are the market trends shaping the Breakfast Food Industry?

- The institutionalization of high-protein functionalism and the proliferation of performance-oriented formats are defining market evolution. This shift prioritizes nutrient density to meet consumer demands for foods that support metabolic stability and long-term satiety.

- Key trends are reshaping the breakfast food market, with a strong emphasis on functional and sustainable options. The integration of ancient grain formulations is becoming mainstream as consumers seek nutrient-dense alternatives to traditional grains. This shift is complemented by the development of climate-resilient cereal ecosystems, which has enabled some producers to reduce water usage by up to 15%.

- There is also a notable proliferation of hyper-convenient hybrid meal kits, which have seen a 25% year-over-year growth in adoption among urban demographics. This trend reflects a broader move toward performance-oriented formats that align with busy, health-conscious lifestyles.

- The focus on personalized nutrition is also gaining traction, as consumers look for products tailored to their specific dietary needs, driving innovation across all product segments.

What challenges does the Breakfast Food Industry face during its growth?

- A key market challenge arises from the convergence of stringent regulatory mandates, such as the nutri-score system, and the significant technical burden of recipe reformulation.

- The market faces considerable challenges, led by the technical burden of recipe reformulation to meet evolving regulatory standards like the nutri-score system. Structural cost inflation across global cereal and dairy supply chains has compressed margins by up to 8% for manufacturers unable to pass on increased costs.

- This pressure is compounded by intense private label competition, which has captured an additional 5% market share in the last two years, leading to brand loyalty erosion. The paradox of choice in a crowded marketplace further complicates consumer purchasing decisions.

- Successfully navigating these challenges requires significant investment in R&D to develop cost-effective, compliant, and appealing products while reinforcing brand value against lower-priced alternatives.

Exclusive Technavio Analysis on Customer Landscape

The breakfast food market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the breakfast food market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Breakfast Food Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, breakfast food market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alimento Agro Foods Pvt ltd - Offers a strategic portfolio of breakfast foods, including cereals and baked goods, designed for diverse global retail channels and consumer segments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alimento Agro Foods Pvt ltd

- Associated British Foods Plc

- Aussee Oats Milling Pvt Ltd

- B and G Foods Inc.

- Bobs Red Mill Natural Foods

- Conagra Brands Inc.

- Del Monte Foods Inc.

- Dr. August Oetker KG

- General Mills Inc.

- Happy Egg Co. USA.

- Hormel Foods Corp.

- ITC Ltd.

- Kellanova

- Mars Inc.

- Nestle SA

- PepsiCo Inc.

- pladis Foods Ltd.

- The Campbell Co

- The Hain Celestial Group

- The Kraft Heinz Co.

- Unilever PLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Breakfast food market

- In February, 2025, the United States Food and Drug Administration issued an updated final rule regarding the 'healthy' claim on food packaging, establishing stricter thresholds for added sugars, sodium, and saturated fats, impacting a majority of the ready-to-eat cereal and bakery segments.

- In October, 2024, a leading multinational food corporation announced its acquisition of a high-growth startup specializing in plant-based, ready-to-eat breakfast bowls for an estimated $250 million, signaling a strategic push into the vegan market segment.

- In January, 2025, a major CPG company partnered with a food-tech firm to integrate blockchain technology into its supply chain, aiming to provide consumers with transparent sourcing information for its organic and ancient grain cereal lines.

- In April, 2025, a European food giant launched a new line of hyper-convenient hybrid meal kits across the UK and Germany, featuring par-baked goods and portioned ingredients designed for quick, high-quality home breakfast preparation.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Breakfast Food Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 299 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.4% |

| Market growth 2026-2030 | USD 115608.7 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.3% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Turkey, Israel, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The breakfast food market's evolution is fundamentally a technical one, driven by the convergence of food science, consumer health demands, and regulatory pressures. The industry is moving decisively toward high-protein functionalism, necessitating sophisticated recipe reformulation to incorporate nutrient-dense formats without compromising taste or texture.

- Key technologies enabling this shift include advanced extrusion for cereal texture, which creates appealing product structures, and high-pressure processing (HPP) to preserve the integrity of clean-label ingredients. The challenge of reducing high glycemic indices in products like shelf-stable pastries is being met with innovations in high-potency sweeteners.

- Firms are also investing in rapid-freezing techniques, which have demonstrated a 40% improvement in maintaining the organoleptic properties of products over extended periods. This focus on technical excellence extends to packaging, with resealable pouches and single-serve trays becoming standard for on-the-go nutritive solutions.

- The market's direction is clear: success hinges on the ability to deliver functional convenience through scientifically advanced, ethically sourced, and appealingly packaged products, from ready-to-eat cereals to probiotic-rich yogurts and soy-based yogurt alternatives.

What are the Key Data Covered in this Breakfast Food Market Research and Growth Report?

-

What is the expected growth of the Breakfast Food Market between 2026 and 2030?

-

USD 115.61 billion, at a CAGR of 4.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Distribution Channel (Offline, and Online), Type (Bakery products, Ready meals, Cereals, Snack bars, and Others), Product (RTE, and RTC) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Mainstreaming of functional convenience and industrialization of on-the-go nutritive solutions, Convergence of regulatory nutri-score mandates and technical burden of recipe reformulation

-

-

Who are the major players in the Breakfast Food Market?

-

Alimento Agro Foods Pvt ltd, Associated British Foods Plc, Aussee Oats Milling Pvt Ltd, B and G Foods Inc., Bobs Red Mill Natural Foods, Conagra Brands Inc., Del Monte Foods Inc., Dr. August Oetker KG, General Mills Inc., Happy Egg Co. USA., Hormel Foods Corp., ITC Ltd., Kellanova, Mars Inc., Nestle SA, PepsiCo Inc., pladis Foods Ltd., The Campbell Co, The Hain Celestial Group, The Kraft Heinz Co. and Unilever PLC

-

Market Research Insights

- Market dynamics are increasingly shaped by the erosion of brand loyalty amidst a paradox of choice, compelling incumbents to innovate beyond legacy products. The rise of private label competition, which now accounts for over 20% of shelf space in key categories, has intensified price pressures and forced a greater emphasis on differentiation through personalized nutrition.

- Brands that successfully leverage direct-to-consumer digital channels see a 15% higher customer retention rate compared to those relying solely on traditional retail. The convenience factor remains paramount, but it is now coupled with demands for sustainable supply chains and functional benefits.

- This complex environment requires a strategic approach to managing global cereal and dairy supply chains while navigating structural cost inflation and evolving consumer preferences for performance-oriented formats.

We can help! Our analysts can customize this breakfast food market research report to meet your requirements.

RIA -

RIA -