Care Management Solution Market Size 2024-2028

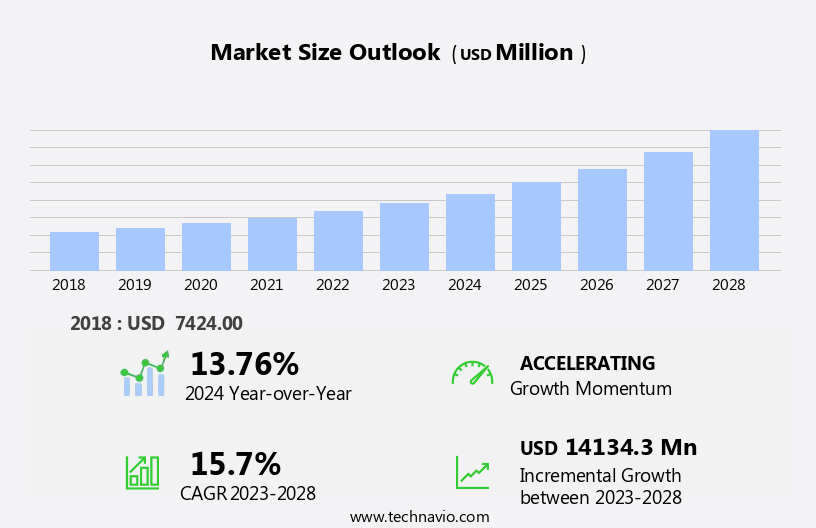

The care management solution market size is forecast to increase by USD 14.13 billion, at a CAGR of 15.7% between 2023 and 2028.

- The market is experiencing significant growth, driven by the increasing adoption of Electronic Health Records (EHRs) and advanced technologies in healthcare. EHRs enable efficient data management, streamlined workflows, and improved patient care, making them a crucial investment for healthcare providers. In parallel, advanced technologies like artificial intelligence, machine learning, and IoT are revolutionizing care management by enabling predictive analytics, remote monitoring, and personalized care plans. However, this market landscape is not without challenges. The growing reliance on digital solutions raises concerns about the security of patient data and the threat of cyberattacks. Ensuring robust data security measures is essential to maintain patient trust and protect sensitive information.

- As healthcare organizations navigate these challenges, they must prioritize data privacy, invest in cybersecurity solutions, and establish clear policies and procedures for data access and management. By addressing these challenges, market players can capitalize on the opportunities presented by the evolving care management landscape and deliver innovative, effective solutions to meet the needs of healthcare providers and patients alike.

What will be the Size of the Care Management Solution Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by the increasing demand for efficient and effective patient care. Seamlessly integrated patient engagement strategies, risk stratification models, clinical decision support, personalized care plans, virtual care platforms, real-time health updates, care transition management, wearable device integration, and other advanced technologies are transforming the healthcare landscape. These solutions enable healthcare providers to identify care gaps, assess fall risks, and deliver personalized health recommendations. Clinical workflow automation tools and quality improvement initiatives are streamlining processes, reducing errors, and improving patient outcomes. Chronic disease management, population health management, and preventive care programs are gaining traction, as healthcare organizations strive to optimize care delivery and improve patient experiences.

Virtual care platforms, telehealth integration, and remote patient monitoring are becoming essential components of care delivery, enabling providers to offer real-time health updates and personalized care plans. Care coordination platforms, home health monitoring, and community resource integration are also critical, ensuring seamless communication and collaboration among care teams. Data security protocols and interoperability standards are essential, as healthcare organizations navigate the complexities of health data exchange and provider communication. Predictive analytics models and outcome measurement metrics are providing valuable insights, enabling providers to proactively address patient needs and improve overall population health. The ongoing unfolding of market activities and evolving patterns in the market reflect the dynamic nature of healthcare delivery, as providers continue to seek innovative solutions to meet the complex needs of patients and populations.

How is this Care Management Solution Industry segmented?

The care management solution industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Chronic care management

- Disease management

- Utilization management

- Deployment

- Cloud-based

- On-premises

- Geography

- North America

- US

- Canada

- Europe

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

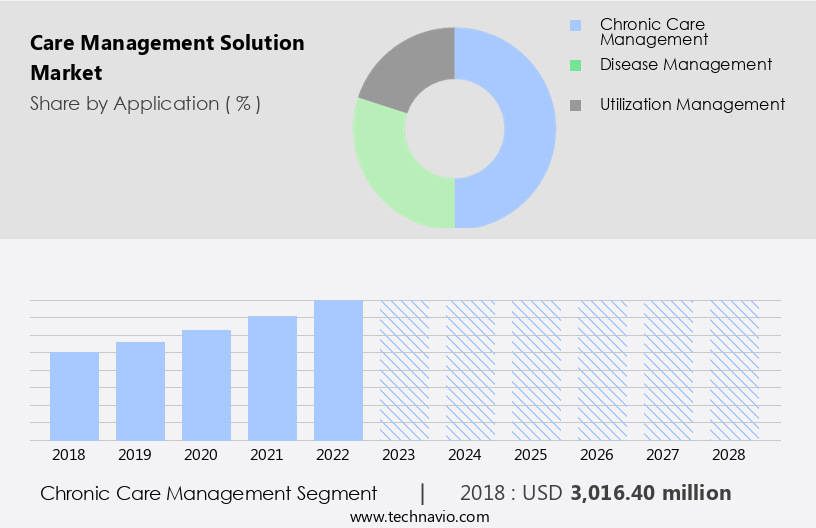

By Application Insights

The chronic care management segment is estimated to witness significant growth during the forecast period.

In today's healthcare landscape, the need for effective care management solutions has become increasingly important due to the rising prevalence of chronic diseases and an aging population. Electronic health records and workflow automation tools facilitate efficient data management and streamlined processes, enhancing the overall quality of care. Adherence improvement programs and personalized health recommendations, driven by data analytics and predictive analytics models, help patients manage chronic conditions more effectively. Quality improvement initiatives and risk stratification models enable proactive care by identifying care gaps, fall risks, and other potential health issues. Clinical decision support systems and personalized care plans, integrated with virtual care platforms and real-time health updates, empower providers to deliver timely, data-driven interventions.

Telehealth integration, wearable device integration, and remote patient monitoring expand access to care and enable continuous monitoring, especially for patients with complex needs. Behavioral health integration and preventive care programs address the whole person, improving patient engagement and overall health outcomes. Care transition management, care coordination platforms, and home health monitoring ensure seamless transitions between care settings and promote effective communication between providers. Data security protocols and interoperability standards ensure the secure exchange of health data, enhancing collaboration and coordination among healthcare teams. Community resource integration further strengthens the care management ecosystem, connecting patients to essential resources and support networks, ultimately improving population health management and patient satisfaction.

The Chronic care management segment was valued at USD 3.02 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

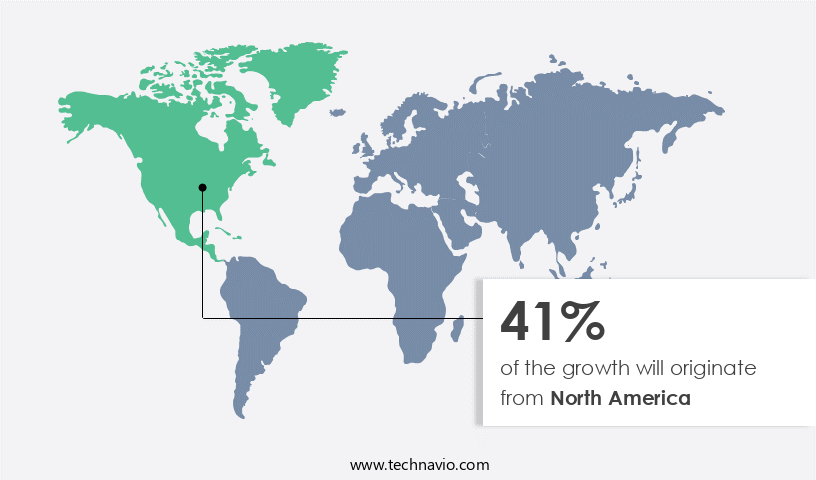

North America is estimated to contribute 41% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in North America is experiencing significant growth due to escalating healthcare expenditures. In 2021, US healthcare spending rose by 9.6% compared to the previous year, primarily driven by substantial investments in major federal healthcare programs like Medicare, Medicaid, and the Children's Health Insurance Program (CHIP), as well as Affordable Care Act health insurance exchange subsidies. This increasing spending on healthcare, coupled with government policies, is fueling the adoption of digital health technologies. Electronic health records, workflow automation tools, adherence improvement programs, quality improvement initiatives, chronic disease management, personalized health recommendations, care gap identification, fall risk assessment, patient engagement strategies, risk stratification models, clinical decision support, personalized care plans, virtual care platforms, real-time health updates, care transition management, wearable device integration, outcome measurement metrics, medication adherence tracking, telehealth integration, preventive care programs, behavioral health integration, remote patient monitoring, patient portal integration, data security protocols, care coordination platforms, home health monitoring, predictive analytics models, population health management, interoperability standards, health data exchange, provider communication tools, and community resource integration are all playing pivotal roles in this digital transformation.

These advanced technologies enable seamless data exchange, real-time monitoring, and personalized care plans, improving patient outcomes and overall population health. Furthermore, they streamline workflows, enhance care coordination, and reduce healthcare costs by addressing care gaps, improving medication adherence, and preventing readmissions. The integration of telehealth, wearable devices, and behavioral health services also ensures comprehensive care, addressing the unique needs of diverse patient populations. Overall, the market in North America is poised for continued growth as digital health technologies increasingly become an integral part of the healthcare ecosystem.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Care Management Solution Industry?

- The significant rise in the implementation of Electronic Health Records (EHRs) serves as the primary catalyst for market growth.

- Electronic Health Records (EHRs) have become an essential component of modern healthcare systems, enabling the digital collection and storage of patient medical information. EHRs and Electronic Medical Records (EMRs) streamline hospital workflows through automated access to information and network connectivity, allowing physicians and doctors to access comprehensive patient histories, diagnoses, medications, treatment plans, immunization dates, allergies, radiology images, and test results. This information sharing enhances care coordination, reduces medical errors, and improves the accuracy and clarity of medical records. Hospitals are increasingly adopting EHRs to minimize data replication and ensure database auto-update.

- Moreover, EHRs support workflow automation tools, adherence improvement programs, quality improvement initiatives, chronic disease management, personalized health recommendations, care gap identification, and fall risk assessment. These features contribute to enhanced patient care and better health outcomes.

What are the market trends shaping the Care Management Solution Industry?

- Advanced technologies are increasingly being adopted in the healthcare industry, marking a significant market trend. This shift towards technological innovation aims to enhance patient care and improve overall healthcare delivery.

- Healthcare providers are increasingly adopting advanced technologies to enhance patient engagement, streamline care delivery, and reduce costs. One such area of investment is Care Management Solutions, which incorporate patient engagement strategies, risk stratification models, clinical decision support, personalized care plans, virtual care platforms, real-time health updates, care transition management, and wearable device integration. These solutions enable healthcare professionals to gain valuable insights from patient data, facilitating proactive interventions and personalized care plans. Risk stratification models help identify high-risk patients, allowing for targeted interventions and improved outcomes. Clinical decision support systems provide real-time guidance to healthcare providers, ensuring evidence-based care and reducing medical errors.

- Virtual care platforms offer remote monitoring and real-time health updates, enabling continuous patient engagement and timely intervention. Care transition management ensures seamless coordination between care settings, reducing readmissions and improving patient satisfaction. Wearable device integration provides valuable data on patient activity levels, vital signs, and other health metrics, enabling early intervention and proactive care. The integration of these technologies into care management solutions is revolutionizing the healthcare industry, offering improved patient outcomes, enhanced efficiency, and reduced costs.

What challenges does the Care Management Solution Industry face during its growth?

- The growth of the healthcare industry is significantly impacted by concerns surrounding the security of patient data and the increasing threat of cyberattacks. It is essential to implement robust security measures to protect sensitive information and mitigate potential risks, ensuring both patient privacy and industry progression.

- In the rapidly evolving healthcare landscape, ensuring data security is paramount. The market addresses this concern by implementing robust data security protocols. Outcome measurement metrics, medication adherence tracking, telehealth integration, preventive care programs, behavioral health integration, remote patient monitoring, and patient portal integration are integral components of these solutions. However, with the increased digitization of healthcare data, cybersecurity remains a significant challenge. Threats such as data theft, unauthorized access, improper data disposal, data loss, and hacking pose risks to sensitive patient information.

- To mitigate these risks, care management solutions prioritize data security, employing encryption techniques, access control mechanisms, and regular vulnerability assessments. These measures ensure the harmonious balance between advancing technology and safeguarding patient privacy.

Exclusive Customer Landscape

The care management solution market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the care management solution market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, care management solution market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AssureCare LLC - This company specializes in care management, delivering advanced solutions through predictive modeling, workflow automation, comprehensive social determinants of health content, customizable assessments, and extensive care plan library. These tools optimize healthcare delivery and patient outcomes.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AssureCare LLC

- athenahealth Inc.

- Cognizant Technology Solutions Corp.

- Constellation Software Inc.

- Epic Systems Corp.

- ExlService Holdings Inc.

- HealthEdge Software Inc.

- HealthSmart Holdings Inc.

- i2i Systems Inc.

- InfoMC Inc.

- International Business Machines Corp.

- InterSystems Corp.

- Koninklijke Philips N.V.

- Medecision Inc.

- Oracle Corp.

- OSP

- Pegasystems Inc.

- Veradigm LLC

- ZeOmega Inc.

- Zyter Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Care Management Solution Market

- In January 2024, Cerner Corporation, a leading health care technology company, announced the launch of its Care Management Platform, an advanced solution designed to help manage patient populations and coordinate care across multiple settings (Cerner Corporation Press Release, 2024). This new offering aims to streamline care coordination and improve patient outcomes.

- In March 2024, IBM Watson Health and Amazon Web Services (AWS) entered into a strategic partnership to accelerate the development and deployment of AI-powered care management solutions (IBM Watson Health Press Release, 2024). The collaboration combines IBM Watson Health's expertise in AI and healthcare with AWS's scalable cloud infrastructure, aiming to enhance the efficiency and effectiveness of care management solutions.

- In May 2024, UnitedHealth Group, the largest US health insurer, completed the acquisition of MedSynergies, a leading provider of revenue cycle management and care coordination services (UnitedHealth Group Press Release, 2024). The acquisition strengthened UnitedHealth's position in the care management market, enabling it to offer more comprehensive services to its clients.

- In April 2025, the US Centers for Medicare & Medicaid Services (CMS) announced the expansion of its Care Coordination Innovation Model, which incentivizes healthcare providers to collaborate and coordinate care for Medicare beneficiaries (CMS Press Release, 2025). The initiative aims to improve care quality and reduce costs by promoting care coordination and population health management.

Research Analyst Overview

- In the dynamic the market, provider collaboration tools facilitate seamless communication and coordination among healthcare providers. Health data analytics enable population health strategies by identifying trends and risks, while patient self-management tools empower individuals to take charge of their health. Clinical communication tools ensure effective communication between care teams, and care transition protocols streamline handoffs between providers. Electronic prescribing systems, home health technology, and wearable health sensors enhance care delivery, particularly in remote settings. Care management software, data visualization dashboards, and appointment scheduling systems optimize workflows and improve operational efficiency. Health equity initiatives, clinical guideline implementation, and risk assessment algorithms address disparities and improve patient outcomes.

- Interoperability solutions, data privacy regulations, and cybersecurity measures ensure secure data exchange and protection. Patient engagement technology, predictive modeling techniques, and care coordination workflow improve patient satisfaction and adherence to care plans. Medication management systems, quality reporting systems, and personalized medicine initiatives promote better medication management and patient-centered care. Value-based care models, disease management programs, and patient satisfaction surveys drive accountability and continuous improvement in care delivery. Remote monitoring devices, patient education materials, and care coordination workflow enable proactive care and timely interventions. Overall, the market continues to evolve, addressing the complex needs of healthcare providers and patients alike.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Care Management Solution Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

158 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 15.7% |

|

Market growth 2024-2028 |

USD 14134.3 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

13.76 |

|

Key countries |

US, China, UK, Canada, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Care Management Solution Market Research and Growth Report?

- CAGR of the Care Management Solution industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the care management solution market growth of industry companies

We can help! Our analysts can customize this care management solution market research report to meet your requirements.

RIA -

RIA -