Cattle Healthcare Market Size 2024-2028

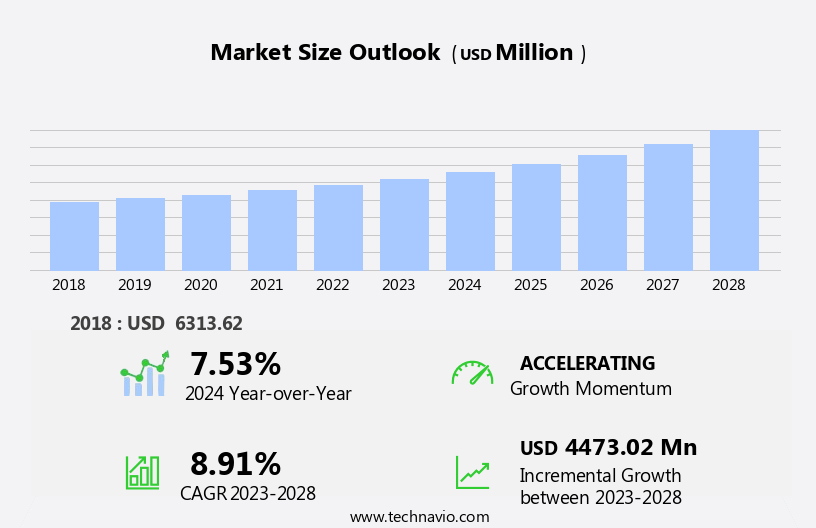

The cattle healthcare market size is forecast to increase by USD 4.47 billion at a CAGR of 8.91% between 2023 and 2028.

What will be the Size of the Cattle Healthcare Market During the Forecast Period?

How is this Cattle Healthcare Industry segmented and which is the largest segment?

The cattle healthcare industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Beef cattle

- Dairy cattle

- Product

- Pharmaceuticals

- Feed additives

- Vaccines

- Others

- Geography

- North America

- US

- Europe

- Germany

- France

- Asia

- China

- India

- Rest of World (ROW)

- North America

By Type Insights

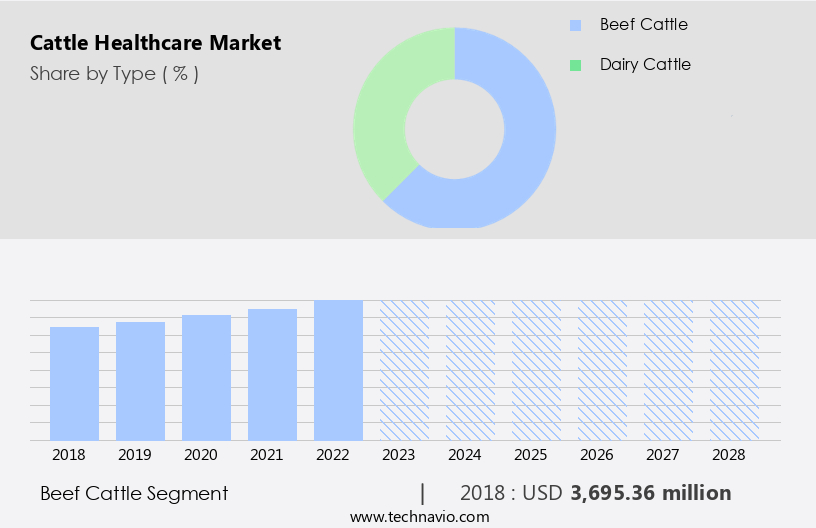

- The beef cattle segment is estimated to witness significant growth during the forecast period.

Beef cattle healthcare is a critical component of animal farming, focusing on the prevention, diagnosis, and treatment of diseases, as well as the promotion of productivity and animal welfare. Disease prevention is achieved through vaccination programs targeting illnesses like bovine tuberculosis, milk fever, and chronic diseases, ensuring herd health and reducing drug consumption. Proper nutrition plays a significant role in maintaining cattle health and productivity, with balanced diets tailored to various life stages. Regular health monitoring, including parasite control and hoof care, is essential to address potential health issues. Medical devices, such as diagnostic imaging tools like CT scans and magnetic resonance imaging, are used to diagnose and treat conditions affecting the mammary gland, such as clinical mastitis and inflammation.

Veterinary services and medications, including vaccines and medicines naturally derived, are crucial in maintaining the well-being of the cattle population. Livestock production, including milk production, poultry production, and dairy industry, relies on effective cattle healthcare practices, with emerging economies investing in initiatives to improve infrastructure, funding, and awareness. Disease control and monitoring are essential for sustainable livestock production, addressing zoonotic diseases like Salmonellosis and ensuring animal welfare.

Get a glance at the Cattle Healthcare Industry report of share of various segments Request Free Sample

The Beef cattle segment was valued at USD 3.7 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

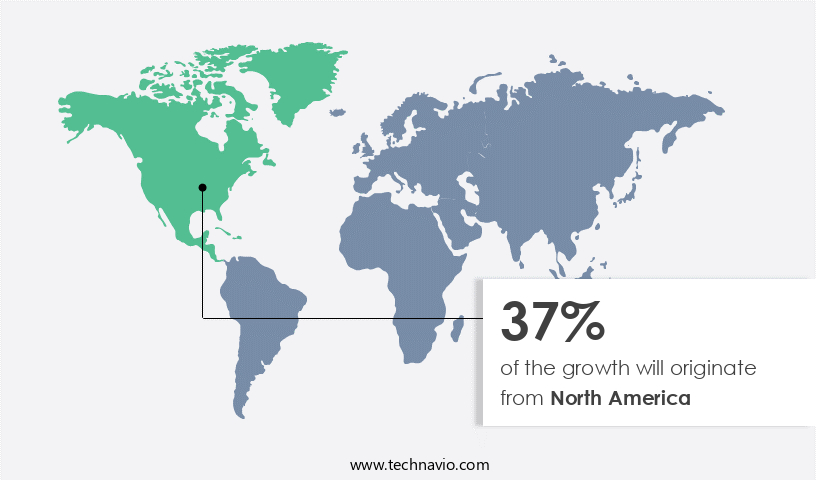

- North America is estimated to contribute 37% to the growth of the global market during the forecast period.

Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The North American the market is experiencing significant growth due to several factors. The region's increasing cattle population and heightened focus on animal welfare have fueled the demand for advanced cattle healthcare solutions. Approximately 60% to 65% of US households own cattle, with around 85 million to 87 million homes housing them. To enhance cattle health, veterinary clinics and hospitals are adopting innovative healthcare products and services. Chronic diseases in aging cattle contribute to market expansion. For instance, the North American Veterinary Community (NAVC) regularly highlights the latest advancements in pain treatment, driving industry growth through knowledge sharing. Cattle health encompasses various aspects, including immunity, mastitis, inflammation, and disease prevention.

Effective management practices, veterinary care, medications, vaccination programs, parasite control, nutritional management, disease surveillance, and animal welfare are essential components of the market. Additionally, initiatives from public and private organizations, diagnostic imaging technologies like CT scans and magnetic resonance imaging, and veterinary services are crucial in maintaining the physical and mental well-being of cattle. Disease prevention, nutrition, environment, and disease control are integral to sustainable livestock production, which is a critical sector for animal protein supply and population growth. Zoonotic diseases, such as bovine tuberculosis, milk fever, lumpy skin disease, and Salmonellosis, pose significant challenges to the market. Awareness and regulations regarding ethical use, veterinary drugs, vaccines, and medicines naturally align with the dairy industry's needs in emerging economies.

Environmental concerns and sustainable production practices are essential considerations for the livestock industry's future. Vaccination campaigns and regulations are crucial in ensuring herd health and animal welfare.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Cattle Healthcare Industry?

Rising burden of cattle diseases is the key driver of the market.

What are the market trends shaping the Cattle Healthcare Industry?

Rising shift towards animal farming is the upcoming market trend.

What challenges does the Cattle Healthcare Industry face during its growth?

Problem in disease management of cattle is a key challenge affecting the industry growth.

Exclusive Customer Landscape

The cattle healthcare market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the cattle healthcare market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, cattle healthcare market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

Biozyme Inc. - The company specializes in providing a range of healthcare solutions for the cattle industry. Among its offerings are AO Biotics Amaferm, AO Biotics EQE, and VitaFerm products. These solutions are designed to enhance cattle health and productivity through nutritional supplementation and microbial balancing. AO Biotics Amaferm is a prebiotic that promotes a healthy digestive system, while AO Biotics EQE is an ionophore that improves feed efficiency and growth. VitaFerm, on the other hand, is a mineral supplement that provides essential nutrients for optimal health and performance. By offering these innovative solutions, the company aims to help cattle producers improve herd health and profitability.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Biozyme Inc.

- Boehringer Ingelheim International GmbH

- Ceva Sante Animale

- Elanco Animal Health Inc.

- IDEXX Laboratories Inc.

- ImmuCell Corp.

- Indian Immunologicals Ltd.

- Innovative Diagnostics

- International Health Care Ltd.

- Kyoritsuseiyaku Corp.

- Merck and Co. Inc.

- Norbrook Laboratories Ltd.

- Phibro Animal Health Corp.

- Thermo Fisher Scientific Inc.

- Vamso Biotec Pvt. Ltd.

- Vetoquinol SA

- Virbac Group

- Zenex Animal Health India Private Ltd.

- Zoetis Inc.

- Zovix Pharmaceuticals

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Cattle healthcare is a crucial aspect of animal husbandry and livestock production, focusing on maintaining the physical and mental well-being of bovine animals. The importance of cattle health lies in enhancing productivity, ensuring the quality of animal products, and promoting sustainable livestock industry practices. Chronic diseases, such as bovine tuberculosis and mastitis, pose significant challenges to the industry. These conditions can lead to substantial drug consumption and veterinary care expenses, impacting the profitability of livestock farms. In addition, diseases like milk fever and inflammation of the mammary gland can negatively affect milk production, further reducing the overall efficiency of the operation.

To address these challenges, various initiatives have been undertaken to improve cattle health through vaccine development, infrastructure development, and funding for research and development. Veterinary services play a vital role in diagnosing and treating clinical mastitis and other diseases, while diagnostic imaging technologies like CT scans and magnetic resonance imaging help in identifying and monitoring health issues. Preventive measures, such as disease surveillance, parasite control, and nutritional management, are essential for maintaining herd health. Proper management practices, including monitoring and evaluation, are crucial in ensuring the well-being of cattle. Public and private organizations have taken various initiatives to promote disease prevention and control In the livestock industry.

These initiatives include vaccination programs, regulations, and ethical use of veterinary drugs and vaccines. Awareness campaigns have also been launched to educate farmers about the importance of animal welfare and sustainable production practices. The dairy industry, in particular, has been a significant focus of these efforts due to its high production volume and the potential for zoonotic diseases, such as salmonellosis, to spread from cattle to humans. Emerging economies are also investing in improving their livestock production systems to meet the growing demand for animal protein and address population growth. Environmental concerns have become increasingly important In the livestock industry, with a focus on sustainable production practices.

This includes reducing the use of antibiotics and promoting disease prevention through better infrastructure, nutrition, and management practices. In conclusion, the market is a dynamic and evolving industry focused on maintaining the health and well-being of bovine animals. Through various initiatives, including vaccine development, veterinary services, and preventive measures, the industry is working to improve productivity, ensure the quality of animal products, and promote sustainable livestock production practices.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

169 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.91% |

|

Market growth 2024-2028 |

USD 4473.02 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

7.53 |

|

Key countries |

US, France, Germany, India, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Cattle Healthcare Market Research and Growth Report?

- CAGR of the Cattle Healthcare industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the cattle healthcare market growth of industry companies

We can help! Our analysts can customize this cattle healthcare market research report to meet your requirements.

RIA -

RIA -