Central Nervous System (CNS) Stimulant Drugs Market Size 2026-2030

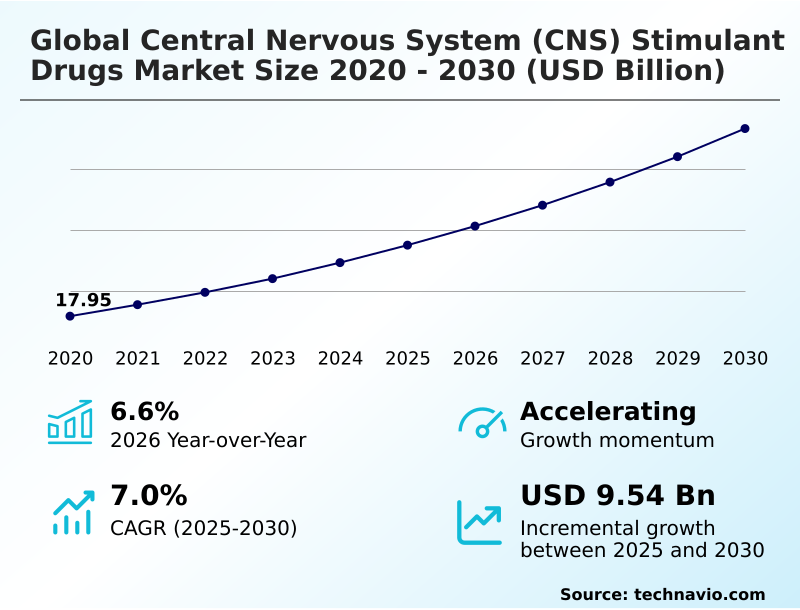

The central nervous system (cns) stimulant drugs market size is valued to increase by USD 9.54 billion, at a CAGR of 7% from 2025 to 2030. Integration of pediatric and adolescent diagnostic precision and evolution of early-intervention therapeutic protocols will drive the central nervous system (cns) stimulant drugs market.

Major Market Trends & Insights

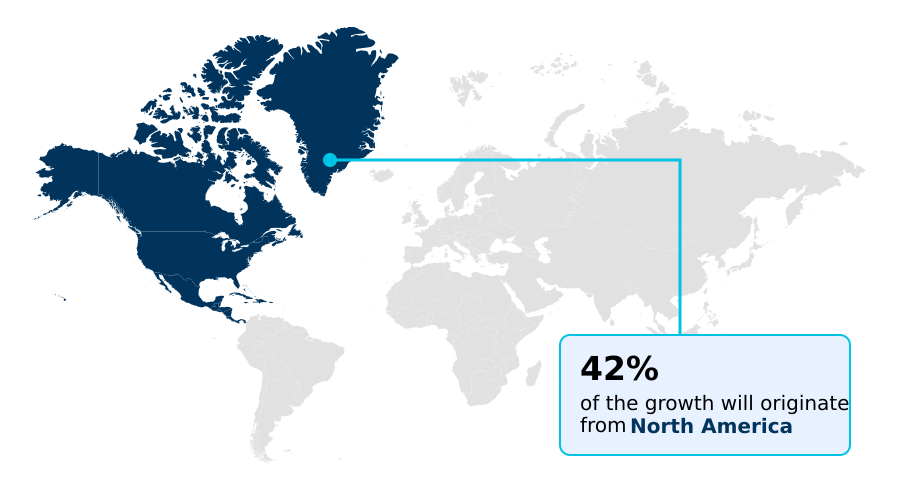

- North America dominated the market and accounted for a 41.5% growth during the forecast period.

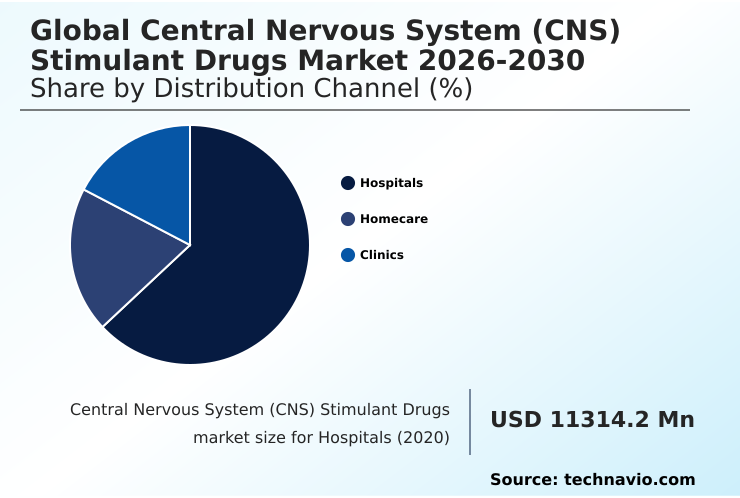

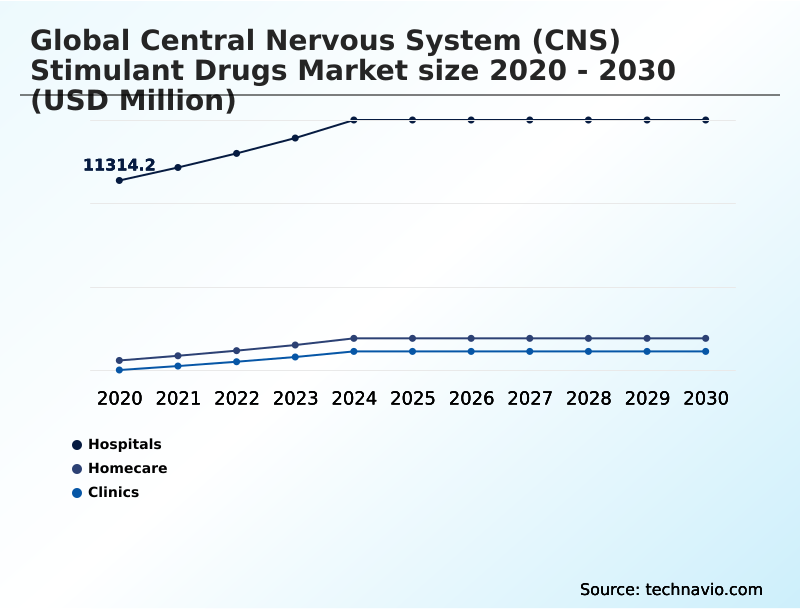

- By Distribution Channel - Hospitals segment was valued at USD 13.93 billion in 2024

- By Application - Attention-deficit hyperactivity disorder segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 15.35 billion

- Market Future Opportunities: USD 9.54 billion

- CAGR from 2025 to 2030 : 7%

Market Summary

- The central nervous system (CNS) stimulant drugs market is undergoing significant evolution, driven by rising diagnostic precision for conditions like attention deficit hyperactivity disorder and increasing neuro-performance demands in adult populations. Key market trends include the development of abuse-deterrent formulations and the shift towards orexin-first therapies that offer novel monoaminergic mechanisms.

- These innovations aim to enhance therapeutic outcomes while addressing critical challenges such as supply chain volatility and a stringent regulatory compliance landscape. For example, a mid-sized pharmaceutical company is leveraging pharmacogenomic testing data to optimize its clinical trial design for a new multi-modal stimulant.

- By stratifying patient groups based on predicted metabolic pathways, the firm improves the trial's efficiency, reduces clinical trial attrition rates by an estimated 15%, and accelerates its path to market.

- This data-driven approach, combined with advances in transdermal drug delivery and digital therapeutics, is reshaping the competitive landscape, pushing the industry towards more personalized and secure treatment paradigms for managing sleep-wake dysregulation and other complex neurological conditions. The focus on early-intervention therapeutic protocols further supports this preventative and proactive healthcare model.

What will be the Size of the Central Nervous System (CNS) Stimulant Drugs Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Central Nervous System (CNS) Stimulant Drugs Market Segmented?

The central nervous system (cns) stimulant drugs industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Distribution channel

- Hospitals

- Homecare

- Clinics

- Application

- Attention-deficit hyperactivity disorder

- Narcolepsy

- Others

- Route of administration

- Oral tablets and capsules

- Injectables

- Transdermal patches

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By Distribution Channel Insights

The hospitals segment is estimated to witness significant growth during the forecast period.

The hospitals segment is a critical channel for the global central nervous system (CNS) stimulant drugs market, managing high-potency therapies for acute neurological conditions.

These institutions are central to initiating treatment for severe narcolepsy treatment and stabilizing patients requiring immediate neuro-modulation therapies.

The segment’s importance is highlighted by regulatory actions, with production quotas for controlled research compounds increasing by 67% to support hospital-based trials and specialized protocols. This environment demands rigorous prescription drug monitoring and advanced systems for medication diversion control.

Hospitals are increasingly adopting sophisticated histaminergic modulators and catecholamine release stimulation agents, driving demand for therapies with superior cardiovascular safety profiles to manage conditions like excessive daytime sleepiness within an inpatient setting, ensuring both efficacy and compliance.

The Hospitals segment was valued at USD 13.93 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 41.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Central Nervous System (CNS) Stimulant Drugs Market Demand is Rising in North America Get Free Sample

The geographic landscape is shifting, with Asia emerging as the fastest-growing region, expanding at a rate of 9.4%, significantly outpacing North America's 6.3% growth.

This surge is fueled by a 38% increase in the identification of CNS-related conditions due to improved diagnostic access and a growing focus on pediatric neurodevelopment.

In mature markets, the focus is on precision neuro-modulation and implementing pro-drug stimulant technology to manage executive dysfunction support. In contrast, emerging economies are focused on building infrastructure for narcolepsy treatment and cataplexy management.

This global expansion relies on harmonizing standards for controlled-release harmonization and secure supply chain logistics to ensure therapies from selective norepinephrine reuptake inhibitors to sympathomimetic stimulants are available worldwide, addressing the global sleep-wake dysregulation burden.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the market is increasingly shaped by the development of abuse-deterrent cns stimulant formulations and the global harmonization of abuse-deterrent standards to address regulatory pressures. The integration of digital therapeutics for adhd management, often delivered via telepsychiatry for stimulant prescription monitoring, is becoming a standard of care.

- In therapeutics, a significant shift is occurring toward orexin agonists for narcolepsy treatment, moving away from traditional approaches. Precision medicine is being realized through pharmacogenomic testing for stimulant selection, which helps in mitigating cardiovascular risks of stimulant use.

- The industry is also exploring advanced delivery systems like long-acting injectables for cns disorders and transdermal patch technology for adhd to improve patient compliance and therapeutic outcomes. However, firms face significant challenges, including extended-release methylphenidate supply chain issues and the scientific hurdle of blood-brain barrier penetration enhancement techniques.

- The intense regulatory oversight for schedule ii stimulants and ongoing challenges in developing novel cns therapeutics are major constraints. Discussions around the impact of pro-drug technology on misuse and the role of triple reuptake inhibitors are shaping R&D priorities.

- Furthermore, managing the supply of controlled substances requires strategies for both supply chain resilience for controlled substances and addressing strategies for cns drug supply shortages.

- Clinical practice is evolving with a focus on pediatric cns stimulant dosing strategies, managing adult adhd with lisdexamfetamine, optimizing cognitive performance with modafinil, and exploring non-stimulant alternatives for cns conditions and neuro-modulation as a stimulant alternative.

What are the key market drivers leading to the rise in the adoption of Central Nervous System (CNS) Stimulant Drugs Industry?

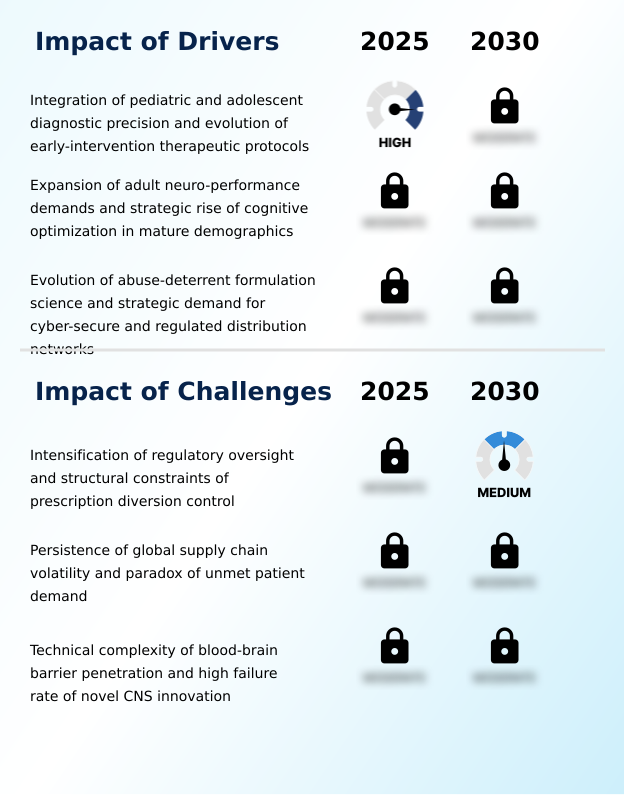

- A key market driver is the integration of pediatric and adolescent diagnostic precision, which is consequently leading to the evolution of early-intervention therapeutic protocols.

- A primary market driver is the surge in neuro-performance demands, particularly with the rise in adult ADHD diagnosis.

- This has led to a record percentage increase in dispensing rates for adults over 25, creating a lifespan-management model for cognitive optimization pharmacology.

- To meet this demand responsibly, the industry is advancing abuse-deterrent formulation science and pushing for secure regulated distribution networks. The recent regulatory approval of a generic amphetamine with specific exclusivity periods highlights the competitive pressure to balance access with safety.

- This focus on pediatric diagnostic precision and early-intervention therapeutic protocols for conditions like attention deficit hyperactivity disorder ensures that pharmacokinetic profiles are optimized from an early stage, setting a foundation for long-term treatment success.

What are the market trends shaping the Central Nervous System (CNS) Stimulant Drugs Industry?

- The market is witnessing a significant trend toward the institutionalization of specialized orexin agonists. This marks a strategic shift away from traditional monoaminergic mechanisms for promoting wakefulness.

- The market is evolving beyond traditional pills, with transdermal drug delivery systems now accounting for 24% of new treatment modalities for certain CNS disorders. This shift is driven by the need to ensure therapeutic window stability and improve patient adherence monitoring.

- The institutionalization of digital therapeutics and telepsychiatry-integrated monitoring systems is accelerating, underscored by a recent 9% single-quarter surge in CNS stimulant prescriptions in one major European health system. This reflects a broader trend toward a holistic management of neurodevelopmental disorders, where pharmacological intervention governance is enhanced by real-time data.

- As non-monoaminergic wakefulness agents and orexin-first therapies gain traction, the focus remains on minimizing diversion risks and addressing unmet patient demand sustainably.

What challenges does the Central Nervous System (CNS) Stimulant Drugs Industry face during its growth?

- A primary challenge affecting industry growth is the intensification of regulatory oversight coupled with the structural constraints of controlling prescription diversion.

- A significant market challenge is the technical complexity of drug development, as blood-brain barrier penetration remains a formidable obstacle, blocking nearly 98% of potential therapeutic candidates. This results in high clinical trial attrition rates, with CNS drug candidates showing a markedly lower success rate compared to other therapy areas.

- The industry grapples with supply chain volatility, which exacerbates unmet patient demand and complicates the management of medication diversion control. Furthermore, intensified regulatory oversight and the need for advanced compliance software create significant operational hurdles.

- Addressing the psychiatric comorbidity management in patients requires more sophisticated multi-modal stimulants, yet the high cost of research and development investment and the difficulty in clinical endpoint demonstration restrain innovation, especially for treatment-resistant depression.

Exclusive Technavio Analysis on Customer Landscape

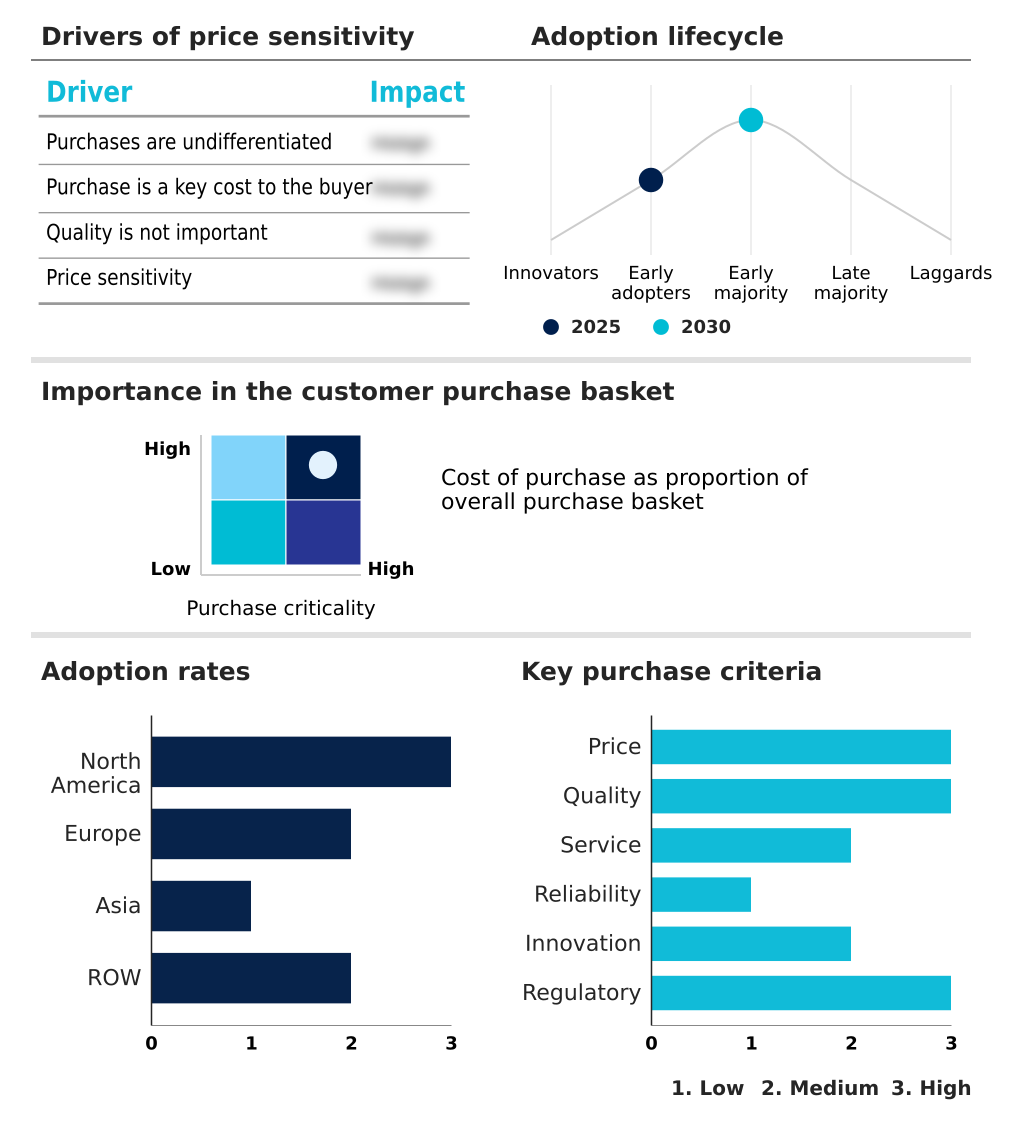

The central nervous system (cns) stimulant drugs market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the central nervous system (cns) stimulant drugs market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Central Nervous System (CNS) Stimulant Drugs Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, central nervous system (cns) stimulant drugs market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AbbVie Inc. - Offers central nervous system (CNS) stimulant drugs such as ABV-1505 and Vraylar for treating complex neurological conditions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AbbVie Inc.

- Amneal Pharmaceuticals Inc.

- Assertio Holdings Inc

- Aytu BioPharma Inc.

- Azurity Pharmaceuticals Inc.

- Cosette Pharmaceuticals Inc.

- Jazz Pharmaceuticals Plc

- Lannett Co Inc.

- Mallinckrodt Plc

- Novartis AG

- Noven Pharmaceuticals Inc.

- Otsuka Holdings Co. Ltd.

- Pfizer Inc.

- Purdue Pharma LP

- Rhodes Pharmaceuticals L.P.

- Supernus Pharmaceuticals Inc.

- Takeda Pharmaceutical Ltd.

- Teva Pharmaceutical Ltd.

- Zealand Pharma

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Central nervous system (cns) stimulant drugs market

- In April 2025, Jazz Pharmaceuticals Plc reported that its sleep franchise exceeded $2 billion in annual revenue for 2024, supported by the continued growth of its leading treatments for narcolepsy.

- In February 2025, Supernus Pharmaceuticals Inc. reported record total revenues for its 2024 fiscal year, driven by the sustained commercial momentum of its integrated ADHD portfolio.

- In January 2025, Takeda Pharmaceutical Ltd. announced a revision to its full-year 2024 financial forecasts, noting an acceleration toward its next-generation late-stage programs in neuroscience.

- In September 2024, Alkermes plc received Breakthrough Therapy designation from the US Food and Drug Administration for alixorexton, an investigational oral OX2R agonist for the treatment of narcolepsy.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Central Nervous System (CNS) Stimulant Drugs Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 289 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7% |

| Market growth 2026-2030 | USD 9541.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.6% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Spain, The Netherlands, Italy, China, Japan, India, South Korea, Indonesia, Thailand, Brazil, Saudi Arabia, Turkey, UAE, South Africa, Israel, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is defined by a push for cognitive optimization pharmacology, driven by escalating neuro-performance demands. A key boardroom focus is aligning R&D with abuse-deterrent formulation science, as the clinical success rate for CNS therapies remains significantly lower than other areas. Innovation is centered on orexin-first therapies and non-monoaminergic wakefulness agents, moving beyond traditional monoaminergic mechanisms and serotonin reuptake inhibition.

- Development of abuse-deterrent formulations using prodrug technologies and microsphere matrices is critical for secure regulated distribution. Firms are exploring long-acting injectable formulations, pro-drug stimulant technology, and transdermal drug delivery to improve pharmacokinetic profiles. The pipeline includes precision neuro-modulation via orexin receptor agonists, selective norepinephrine reuptake inhibitors, alpha-2 adrenergic agonists, and histaminergic modulators.

- Managing psychiatric comorbidity management requires advanced multi-modal stimulants and pharmacogenomic testing to overcome challenges in blood-brain barrier penetration and avoid interactions with synthetic cathinones. This requires detailed early-intervention therapeutic protocols based on pediatric diagnostic precision and supported by telepsychiatry-integrated monitoring.

- The goal is controlled-release harmonization of agents that influence catecholamine release stimulation and neurotransmitter regulation through extended-release matrices and triple reuptake inhibitor technology.

What are the Key Data Covered in this Central Nervous System (CNS) Stimulant Drugs Market Research and Growth Report?

-

What is the expected growth of the Central Nervous System (CNS) Stimulant Drugs Market between 2026 and 2030?

-

USD 9.54 billion, at a CAGR of 7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Distribution Channel (Hospitals, Homecare, and Clinics), Application (Attention-deficit hyperactivity disorder, Narcolepsy, and Others), Route of Administration (Oral tablets and capsules, Injectables, and Transdermal patches) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Integration of pediatric and adolescent diagnostic precision and evolution of early-intervention therapeutic protocols, Intensification of regulatory oversight and structural constraints of prescription diversion control

-

-

Who are the major players in the Central Nervous System (CNS) Stimulant Drugs Market?

-

AbbVie Inc., Amneal Pharmaceuticals Inc., Assertio Holdings Inc, Aytu BioPharma Inc., Azurity Pharmaceuticals Inc., Cosette Pharmaceuticals Inc., Jazz Pharmaceuticals Plc, Lannett Co Inc., Mallinckrodt Plc, Novartis AG, Noven Pharmaceuticals Inc., Otsuka Holdings Co. Ltd., Pfizer Inc., Purdue Pharma LP, Rhodes Pharmaceuticals L.P., Supernus Pharmaceuticals Inc., Takeda Pharmaceutical Ltd., Teva Pharmaceutical Ltd. and Zealand Pharma

-

Market Research Insights

- The market dynamics are shaped by the need to manage adult ADHD diagnosis and executive dysfunction support amid a strict regulatory compliance landscape. The adoption of advanced compliance software has been shown to reduce reporting errors by over 40%, a critical factor given the scrutiny on medication diversion control.

- As lifespan-management model approaches become standard for attention deficit hyperactivity disorder, the industry is focusing on diversion risk mitigation through innovative delivery systems. This has improved patient adherence monitoring, with some digital platforms showing a 25% increase in medication consistency.

- The dual pressures of unmet patient demand and supply chain volatility are pushing firms toward more resilient secure supply chain logistics, making post-market surveillance and proactive risk management central to operational strategy.

We can help! Our analysts can customize this central nervous system (cns) stimulant drugs market research report to meet your requirements.

RIA -

RIA -