Cider Market Size 2025-2029

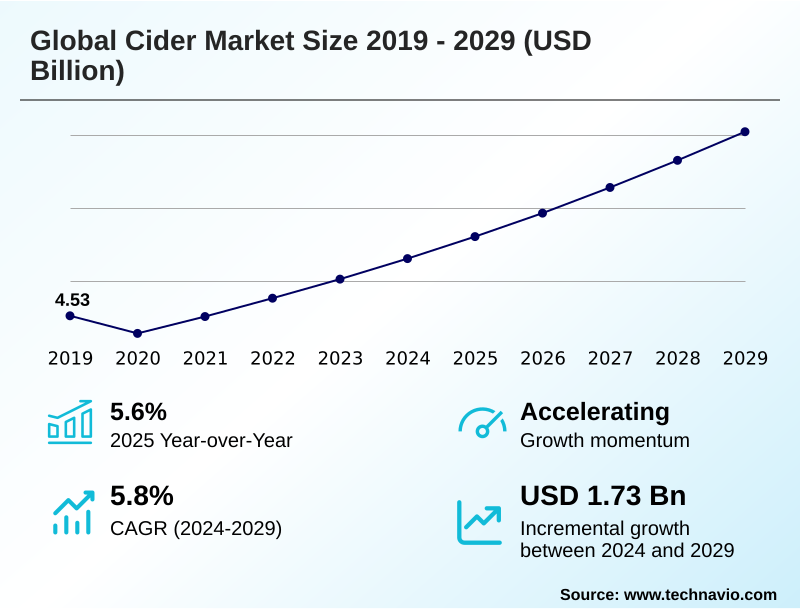

The cider market size is valued to increase by USD 1.73 billion, at a CAGR of 5.8% from 2024 to 2029. Increasing demand for gluten-free and perceived healthier alternatives will drive the cider market.

Major Market Trends & Insights

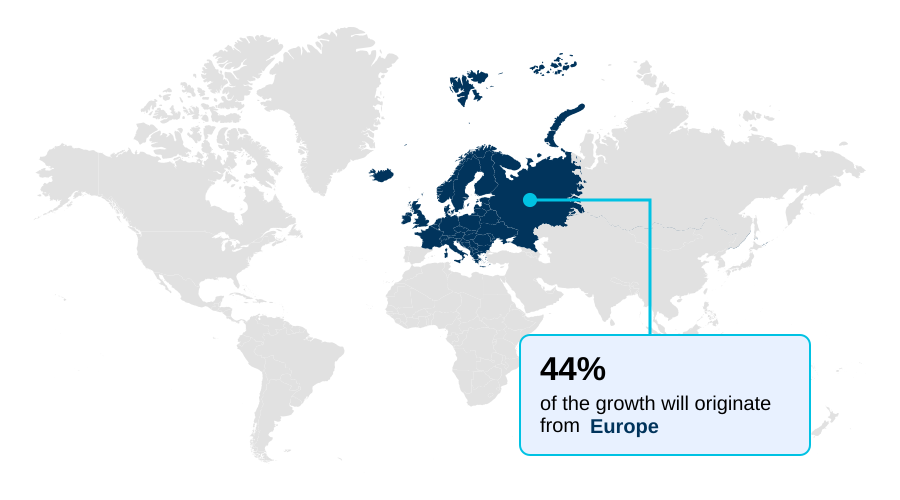

- Europe dominated the market and accounted for a 43.9% growth during the forecast period.

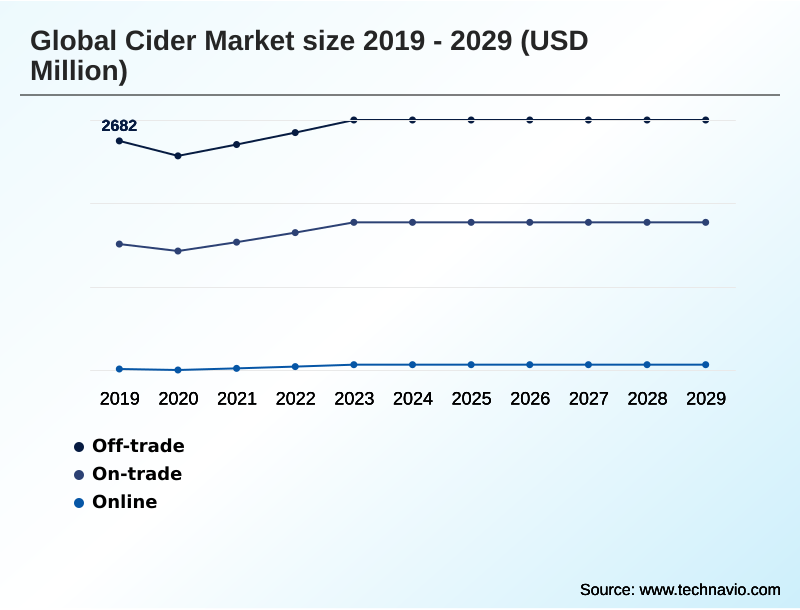

- By Distribution Channel - Off-trade segment was valued at USD 2.90 billion in 2023

- By Product Type - Apple cider segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 2.51 billion

- Market Future Opportunities: USD 1.73 billion

- CAGR from 2024 to 2029 : 5.8%

Market Summary

- The Cider Market is undergoing a significant transformation, evolving from a traditional beverage to a sophisticated and diverse category. This renaissance is propelled by the artisanal cider movement, which champions craft cider production using heirloom apple varietals to create beverages with complex tannin structure and distinct cider terroir.

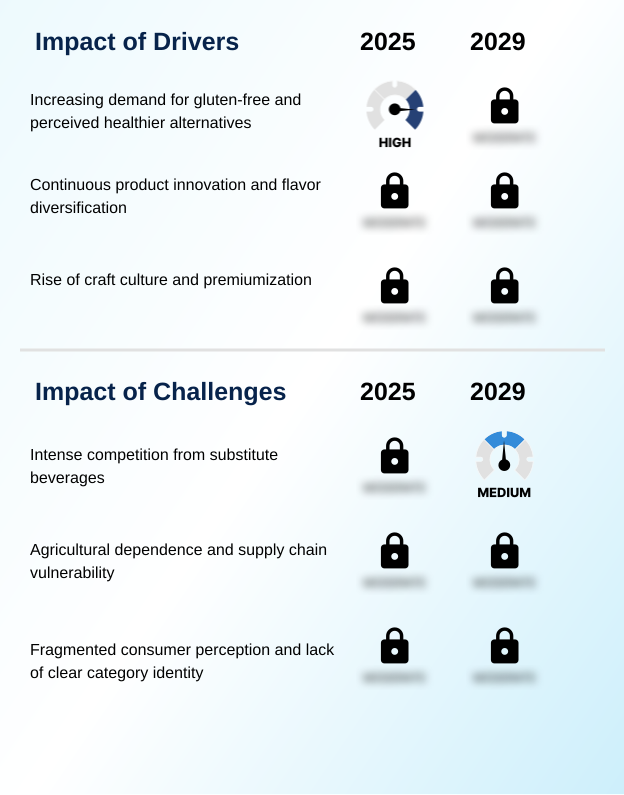

- Key market drivers include the growing consumer shift toward healthier, gluten-free alcoholic beverage options and a willingness to explore premium cider brands.

- A critical operational scenario for producers involves managing the supply chain for specific bittersweet apples and bittersharp apples, as inconsistent availability can disrupt production schedules and impact the final product's flavor profile, which is defined by its cider sweetness scale and acidity levels.

- While continuous fruit-flavored cider innovation attracts new consumers, the industry faces challenges from intense competition and the need for greater consumer education to differentiate between mass-market products and high-quality single varietal ciders. The heritage cider revival is a key trend, bringing renewed focus to traditional methods and authentic flavors.

What will be the Size of the Cider Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Cider Market Segmented?

The cider industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Distribution channel

- Off-trade

- On-trade

- Online

- Product type

- Apple cider

- Fruit flavored cider

- Craft or specialty cider

- Traditional cider

- Pear cider

- Packaging

- Glass

- Can

- Kegs

- Others

- Geography

- Europe

- UK

- France

- Spain

- North America

- US

- Canada

- Mexico

- APAC

- Australia

- China

- Japan

- South America

- Brazil

- Argentina

- Middle East and Africa

- South Africa

- UAE

- Saudi Arabia

- Rest of World (ROW)

- Europe

By Distribution Channel Insights

The off-trade segment is estimated to witness significant growth during the forecast period.

Market segmentation reveals distinct channel dynamics. The on-trade channel distribution relies heavily on draught cider systems to deliver fresh products, while off-trade success is increasingly tied to canned cider convenience and the appeal of premium cider brands.

This segment allows for diverse specialty cider styles, where production methods like bottle conditioning and malolactic fermentation can be marketed directly. Producers manage carbonation levels and sorbitol content to meet consumer preferences.

For instance, brands that have won cider competition awards see a sales lift of over 10% in this channel. Innovations in aseptic packaging extend shelf life, while cider club subscriptions create a direct-to-consumer flywheel, building loyalty beyond the retail shelf.

The Off-trade segment was valued at USD 2.90 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

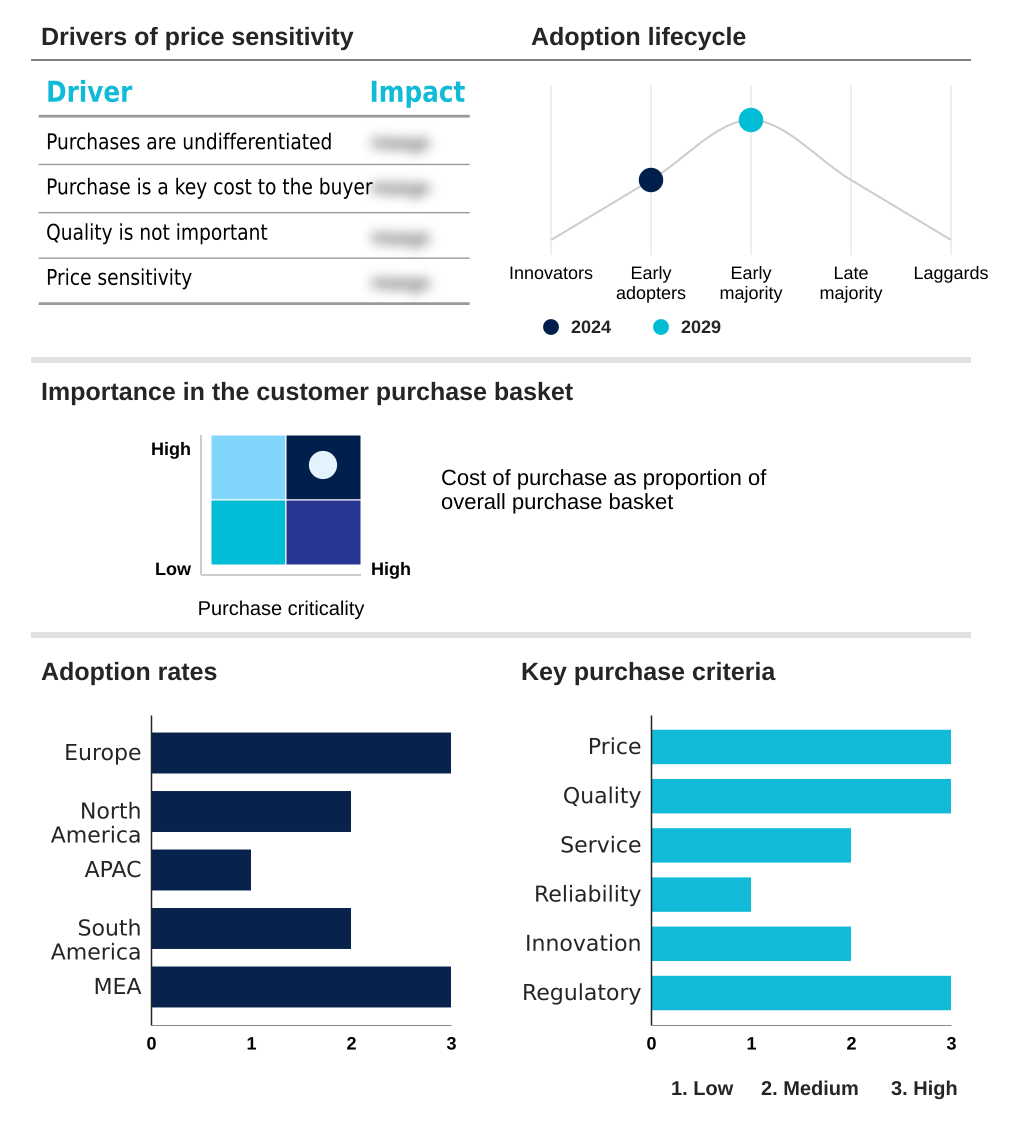

Europe is estimated to contribute 43.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Cider Market Demand is Rising in Europe Get Free Sample

The market's geography is defined by pronounced regional cider differences. Europe remains the core, accounting for nearly 44% of growth, with traditions like apfelwein production in Germany and sidra natural in Spain, where specific cider house rules dictate consumption.

French producers utilize the keeving technique to create naturally sweet cidre bouché. These regions champion natural cider, often using wild yeast fermentation. In contrast, APAC’s growth of over 23% is driven by modern styles.

North American producers leverage direct-to-consumer cider sales to showcase still cider and sparkling cider made from perry pear varieties and apples with unique tannin structure, highlighting the category's global diversity.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global cider market is being reshaped by powerful premiumization trends, shifting it away from a monolithic category into one defined by quality and diversity. Central to this evolution is a deeper consumer and producer focus on understanding tannins in heritage apple ciders, which distinguishes artisanal products from their mass-market counterparts.

- This appreciation for complexity has paved the way for significant innovation in cider and wine hybrid beverages, a key growth area that blurs traditional category lines and appeals to adventurous palates. At the same time, sustainability practices in modern cider making are becoming a crucial point of differentiation and a core component of brand identity.

- These practices resonate strongly with environmentally conscious consumers and often lead to operational efficiencies. This intersects with the evolving consumer perception of canned craft cider, which has moved from being seen as a lower-quality option to a preferred format for its convenience, portability, and superior preservation of flavor.

- For instance, producers that have successfully marketed the quality of their canned offerings have seen adoption rates increase by more than 30% among urban consumers compared to those sticking exclusively to glass.

What are the key market drivers leading to the rise in the adoption of Cider Industry?

- Increasing consumer demand for gluten-free and perceived healthier alternatives is a key driver for the market's growth.

- The market is primarily driven by its positioning as a gluten-free alcoholic beverage and the rise of the artisanal cider movement. This has fueled demand for premium cider brands that emphasize craft cider production using heirloom apple varietals.

- These single varietal ciders allow producers to highlight specific characteristics on the cider sweetness scale. Evolving cider consumption trends show a preference for authenticity, boosting organic cider production and sustainable cidery practices.

- Fruit-flavored cider innovation continues to attract new demographics, while the emergence of imperial ciders and other high-abv ciders caters to demand for more robust experiences. Brands effectively marketing these attributes see consumer acquisition rates improve by over 20%.

What are the market trends shaping the Cider Industry?

- The emergence of low- and no-alcohol ciders represents a significant market trend, driven by a growing consumer focus on health, wellness, and mindful drinking.

- Key trends reflect a heritage cider revival and a push towards sophistication in modern cider making. The barrel aging process and techniques like dry hopping and co-fermentation are creating complex specialty cider styles, including popular rosé ciders, that command premium pricing, with some achieving margins 40% higher than standard offerings. This complexity enhances cider and food pairing opportunities.

- Concurrently, the growth of low-alcohol cider options and the broader non-alcoholic cider market are expanding consumption occasions, with some brands reporting a 15% increase in daytime sales for sessionable ciders. Consumers are exploring cider terroir through detailed cider tasting notes and utilizing versatile products in cider cocktail recipes, indicating a deepening engagement with the category.

What challenges does the Cider Industry face during its growth?

- Intense competition from a wide range of substitute beverages presents a key challenge affecting the industry's growth.

- Significant challenges stem from agricultural dependencies and intense competition. Securing consistent supplies of bittersweet apples and bittersharp apples from cider apple orchards is a primary concern, with climate-related events causing raw material cost fluctuations of up to 20% for some producers.

- The high cost of specialized cider production equipment for processes like juice pressing and advanced cider filtration methods also presents a barrier. Intense competition requires sophisticated cider marketing strategies and innovative cider packaging solutions to secure placement in both off-trade channel sales and on-trade channel distribution.

- Furthermore, complex cider industry regulations and a short cider shelf life for unpasteurized products add operational complexity, intensifying the cider vs hard cider debate for consumer mindshare.

Exclusive Technavio Analysis on Customer Landscape

The cider market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the cider market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Cider Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, cider market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

2 Towns Ciderhouse - An analyst's view highlights the firm's focus on 100% fresh-pressed apples for its craft ciders, eschewing concentrates to maintain product integrity and authenticity.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 2 Towns Ciderhouse

- Ace Cider i, LLC

- Anheuser Busch InBev SA NV

- C and C Group PLC

- Carlsberg Breweries AS

- Cornish Orchards

- Dunkertons Cider

- Gwynt y Ddraig

- Heineken NV

- Kopparberg

- Molson Coors Beverage Co.

- Samuel Smith Old Brewery

- Seattle Cider Co.

- Sheppys Cider Ltd

- Thatchers Cider

- The Boston Beer Co. Inc.

- Westons Cider

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Cider market

- In September 2024, Heineken NV expands its Strongbow portfolio with the global launch of Strongbow 0.0% Dark Fruit, responding to growing consumer demand for premium non-alcoholic beverage options.

- In November 2024, 2 Towns Ciderhouse secures a significant growth equity investment from a private equity firm to expand its production capacity and national distribution network for its craft ciders.

- In January 2025, The Boston Beer Co. Inc. introduces 'Angry Orchard Vine and Press,' a new line of cider-wine hybrids co-fermented with wine grapes, targeting consumers seeking sophisticated, cross-category beverage experiences.

- In April 2025, C and C Group PLC announces a strategic partnership with a leading beverage distributor in Brazil to launch its Magners Irish Cider brand, capitalizing on the growing interest in international premium beverages in South America.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Cider Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 301 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.8% |

| Market growth 2025-2029 | USD 1733.0 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 5.6% |

| Key countries | UK, Ireland, France, Spain, Germany, The Netherlands, US, Canada, Mexico, Australia, China, Japan, India, South Korea, Indonesia, Brazil, Argentina, Chile, South Africa, UAE, Egypt, Morocco and Saudi Arabia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Cider Market's evolution is rooted in the transformation of fermented apple juice into a diverse beverage spectrum. The heritage cider revival is driving interest in cider terroir, with craft cider production leveraging specific cider apple orchards.

- Producers utilize heirloom apple varietals, including bittersweet apples and bittersharp apples, to craft single varietal ciders with unique tannin structure and defined cider acidity levels. Advanced techniques such as the keeving technique, wild yeast fermentation, malolactic fermentation, and bottle conditioning are becoming more prevalent. Boardroom strategy is now focused on portfolio expansion into rosé ciders, imperial ciders, and ice cider.

- The entire production chain, from juice pressing and pulp maceration to the judicious use of sulfite addition and modern cider filtration methods, is being optimized. Firms refining these processes have noted a 15% increase in production efficiency.

- The market offers everything from still cider to sparkling cider with managed carbonation levels, distributed via on-trade channel distribution using draught cider systems and off-trade channel sales leveraging aseptic packaging. This diverse offering solidifies cider's position as a leading gluten-free alcoholic beverage.

What are the Key Data Covered in this Cider Market Research and Growth Report?

-

What is the expected growth of the Cider Market between 2025 and 2029?

-

USD 1.73 billion, at a CAGR of 5.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Distribution Channel (Off-trade, On-trade, and Online), Product Type (Apple cider, Fruit flavored cider, Craft or specialty cider, Traditional cider, and Pear cider), Packaging (Glass, Can, Kegs, and Others) and Geography (Europe, North America, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

Europe, North America, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for gluten-free and perceived healthier alternatives, Intense competition from substitute beverages

-

-

Who are the major players in the Cider Market?

-

2 Towns Ciderhouse, Ace Cider i, LLC, Anheuser Busch InBev SA NV, C and C Group PLC, Carlsberg Breweries AS, Cornish Orchards, Dunkertons Cider, Gwynt y Ddraig, Heineken NV, Kopparberg, Molson Coors Beverage Co., Samuel Smith Old Brewery, Seattle Cider Co., Sheppys Cider Ltd, Thatchers Cider, The Boston Beer Co. Inc. and Westons Cider

-

Market Research Insights

- The Cider Market is shaped by the artisanal cider movement, which has elevated consumer expectations and driven demand for premium cider brands. This shift encourages sophisticated consumption, with a growing interest in cider and food pairing and the use of cider in cider cocktail recipes.

- In response, producers are adopting sustainable cidery practices, with some achieving a 10% reduction in operational waste. Furthermore, brands leveraging direct-to-consumer sales models are reporting customer loyalty rates 25% higher than those relying on traditional retail.

- This focus on quality and authenticity is also fueling interest in organic cider production, as consumers seek products with transparent sourcing and cleaner labels, creating new avenues for market differentiation and value creation.

We can help! Our analysts can customize this cider market research report to meet your requirements.

RIA -

RIA -