Clinical Laboratory Services Market Size 2024-2028

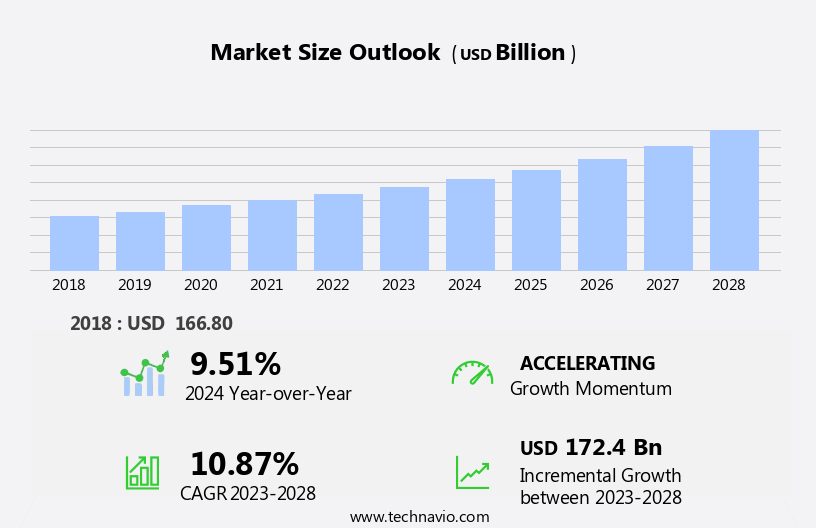

The clinical laboratory services market size is forecast to increase by USD 172.4 billion, at a CAGR of 10.87% between 2023 and 2028.

- The market is experiencing significant growth due to the increasing geriatric population and the rising adoption of preventive healthcare. The aging demographic trend is driving a surge in demand for diagnostic and screening tests, as older adults require more frequent health monitoring. Preventive healthcare, on the other hand, is gaining traction as people become more health-conscious and proactive about managing their health. This shift is leading to an increase in the number of laboratory tests being ordered, particularly for early disease detection. However, the market also faces challenges that could hinder its growth. One such challenge is the lack of skilled professionals, which can impact the quality of services provided and lead to delays in test results.

- This shortage is due to the complex nature of laboratory work and the high level of expertise required to perform various tests accurately. Additionally, the increasing use of automation and technology in laboratories may alleviate some of the pressure on the workforce but also necessitates significant investment in infrastructure and training. Companies seeking to capitalize on market opportunities and navigate challenges effectively should focus on addressing these issues by investing in workforce development and leveraging technology to enhance efficiency and accuracy.

What will be the Size of the Clinical Laboratory Services Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by advancements in technology and the increasing demand for personalized healthcare solutions. Digital pathology, a key area of growth, leverages artificial intelligence (AI) and automated microscopy to enhance diagnostic accuracy and improve workflow efficiency. Clinical trials rely on test validation and data integration to ensure the reliability and consistency of results. Health outcomes are optimized through the use of reference ranges, analytical specificity, and biomarker analysis. Laboratory automation, including robotics and lab automation software, streamlines processes and reduces errors. Remote monitoring enables real-time data access and analysis, while continuing education and staff training ensure a skilled workforce.

Precision medicine and genomic sequencing are revolutionizing disease management, with applications in immunoassay analyzers, blood gas analysis, therapeutic monitoring, and liquid biopsy. Data analytics, including big data analytics and machine learning, provide valuable insights for research and development, test reporting, and regulatory compliance. Emerging technologies, such as next-generation sequencing (NGS) and microfluidic devices, offer new possibilities for diagnostic testing and biomarker discovery. The market's continuous dynamism is further reflected in the ongoing development of molecular diagnostics, point-of-care testing (POCT), and laboratory data management systems. Biohazard management, waste management, and laboratory safety remain critical considerations, with a focus on regulatory compliance and quality control.

The integration of these various components creates a complex and interconnected ecosystem, shaping the future of clinical laboratory services.

How is this Clinical Laboratory Services Industry segmented?

The clinical laboratory services industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Hospital-based laboratories

- Stand-alone laboratories

- Clinic-based laboratories

- Application

- Bioanalytical and lab chemistry

- Toxicology testing

- Cell and gene therapy

- Preclinical and clinical trial

- Others

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Rest of World (ROW).

- North America

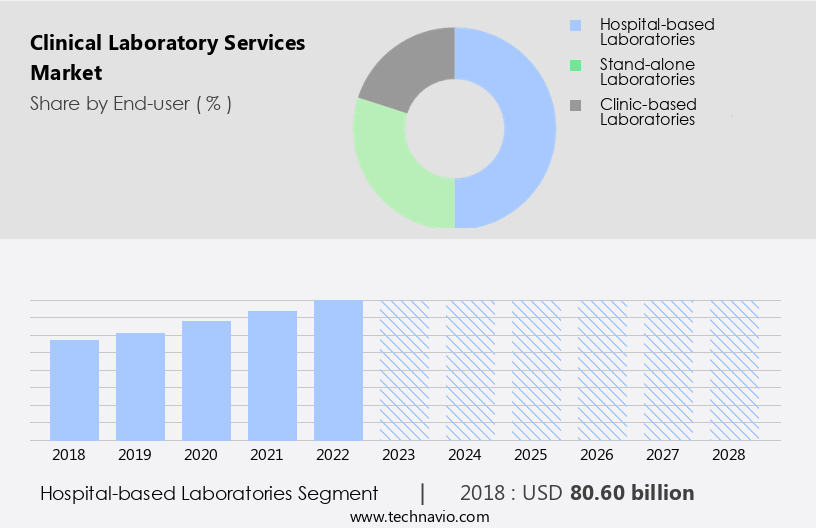

By End-user Insights

The hospital-based laboratories segment is estimated to witness significant growth during the forecast period.

In the dynamic the market, hospitals and clinical laboratories collaborate to enhance operational efficiency and reduce turnaround time. Hospital-based laboratories dominated the market in 2023, with many hospitals referring tests to clinical laboratories to manage high volumes and save on costs. Technologically advanced, rapid diagnostics, such as real-time polymerase chain reaction (PCR) and peptide nucleic acid fluorescent in situ hybridization (PNA-FISH), offer quick results but require expensive equipment. To mitigate these costs, hospitals outsource these tests. Digital pathology and artificial intelligence (AI) are transforming laboratory services, enabling remote monitoring, automated microscopy, and machine learning for improved diagnostic accuracy.

Precision medicine and personalized treatment plans require extensive research and development, including immunology testing, blood gas analysis, and therapeutic monitoring. Next-generation sequencing (NGS) and genomic sequencing are essential for disease management and prognostic value. Laboratory accreditation, regulatory compliance, and quality control ensure diagnostic accuracy and safety. Workflow management, data integration, and data analytics streamline processes and improve overall efficiency. Automated microscopy, liquid biopsy, and serology testing offer new possibilities for disease detection and monitoring. Biopsy analysis, analytical specificity, and biohazard management are crucial for maintaining diagnostic accuracy and laboratory safety. Point-of-care testing (POCT) and lab automation software enable real-time results and streamlined workflows.

Microfluidic devices, cloud computing, and sample handling optimize laboratory operations. Clinical trials and test validation are integral to the development and implementation of new technologies, including molecular diagnostics and emerging technologies. Continuing education and staff training ensure that laboratory personnel remain up-to-date on the latest techniques and technologies. The market is characterized by a focus on advanced technologies, collaboration between hospitals and clinical laboratories, and a commitment to diagnostic accuracy, safety, and efficiency. From digital pathology and AI to NGS and POCT, the market is continually evolving to meet the needs of healthcare providers and patients alike.

The Hospital-based laboratories segment was valued at USD 80.60 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

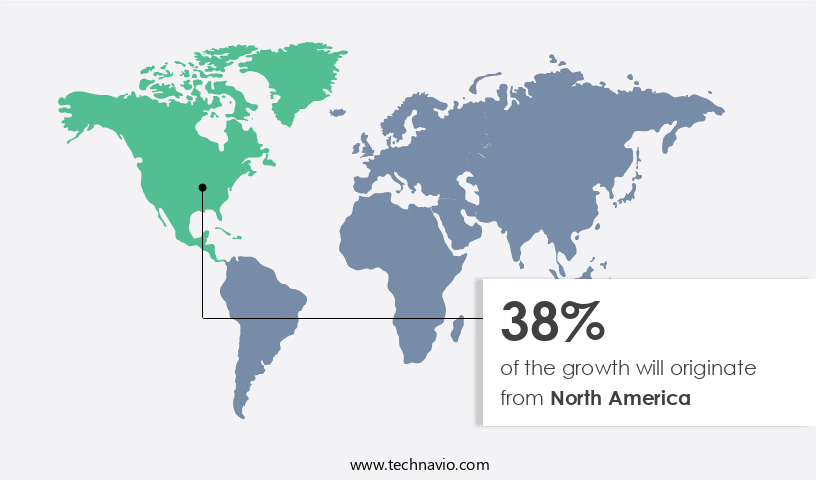

North America is estimated to contribute 38% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in North America is experiencing significant growth, driven by the rising prevalence of chronic conditions such as cardiovascular diseases and diabetes. The United States leads this market due to increased disease awareness, the development of rapid diagnostics, and a large patient population. companies are prioritizing the launch of cost-effective and time-saving diagnostic procedures, particularly in vitro tests, which are gaining popularity due to the increasing incidence of lifestyle and chronic diseases. In the US, numerous clinical laboratories operate, with the adoption of advanced technologies such as laboratory automation, digital pathology, and artificial intelligence (AI) fueling market expansion.

Additionally, the shift towards remote monitoring, data integration, and machine learning is transforming the industry. The FDA's approval of innovative diagnostics, including human genetic tests and microbial tests, further accelerates market growth. Precision medicine, clinical chemistry analyzers, and hematology analyzers are some of the key technologies shaping the market. The integration of next-generation sequencing (NGS), genomic sequencing, and cloud computing is revolutionizing laboratory data management and research & development. Furthermore, regulatory compliance, quality control, and diagnostic accuracy are essential aspects of the market, ensuring the delivery of reliable and accurate test results.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Clinical Laboratory Services Industry?

- The geriatric population's growth serves as the primary catalyst for market expansion.

- The market is experiencing significant growth due to demographic changes and advancements in healthcare technology. The aging population, driven by increased life expectancy and a shift from acute to chronic diseases, is fueling the demand for laboratory services. This trend is expected to continue, with the OECD projecting that the global aging population will increase from 17% in 2015 to 28% by 2050. Advancements in laboratory technology are also contributing to market growth. Specimen processing and sample handling have been improved through automation and emerging technologies such as Lab Automation Software and Point-of-Care Testing (POCT). Microbiology testing and Molecular Diagnostics have benefited from Genomic Sequencing and Cloud Computing, enabling faster and more accurate results.

- Regulatory compliance is a critical factor in the market. Stringent regulations ensure the quality and safety of laboratory services, which is essential for patient safety and trust. Compliance with regulations such as the Clinical Laboratory Improvement Amendments (CLIA) and the College of American Pathologists (CAP) is mandatory for laboratory operations. Emerging technologies, such as Artificial Intelligence (AI) and Machine Learning (ML), are transforming laboratory services. These technologies enable faster turnaround times (TAT), improved accuracy, and enhanced patient care. For instance, AI and ML algorithms can analyze large datasets to identify patterns and trends, enabling early detection and diagnosis of diseases.

- The market is experiencing significant growth due to demographic changes and technological advancements. The aging population, driven by increased life expectancy and a shift from acute to chronic diseases, is fueling the demand for laboratory services. Advancements in laboratory technology, including automation, POCT, Genomic Sequencing, and Cloud Computing, are improving laboratory processes and enabling faster and more accurate results. Regulatory compliance remains a critical factor in the market, ensuring the quality and safety of laboratory services. Emerging technologies, such as AI and ML, are transforming laboratory services and enabling early detection and diagnosis of diseases.

What are the market trends shaping the Clinical Laboratory Services Industry?

- The prevailing market trend underscores the growing importance of preventive healthcare. More professionals and individuals are embracing this approach to maintain optimal health.

- In response to the rising prevalence of chronic diseases and the increasing emphasis on preventive healthcare, the demand for clinical laboratory services is experiencing significant growth. These services play a crucial role in disease prevention by providing accurate and timely diagnostic information. Doctors recommend routine healthcare tests based on a patient's age and gender to prevent illnesses and their progression. For instance, women between the ages of 38 and 42 are at a higher risk for breast cancer, making regular mammogram screenings essential. Moreover, the advancements in technology are revolutionizing the market. Digital pathology, artificial intelligence (AI), and automated microscopy are transforming the way laboratory tests are conducted.

- Clinical trials and test validation are also becoming increasingly important to ensure the accuracy and reliability of test results. Laboratory automation, data integration, workflow management, and remote monitoring are other key trends driving the market's growth. Continuing education and staff training are essential to keep up with the latest technologies and techniques.The market is witnessing significant growth due to the increasing demand for preventive healthcare and the technological advancements in diagnostics.

What challenges does the Clinical Laboratory Services Industry face during its growth?

- The insufficient supply of skilled professionals poses a significant challenge to the expansion and growth of the industry.

- Clinical laboratory services play a pivotal role in disease management through various diagnostic techniques, including Immunoassay Analyzers, Blood Gas Analysis, Therapeutic Monitoring, Liquid Biopsy, Serology Testing, and Biopsy Analysis. These tests offer analytical specificity and prognostic value, enabling early detection and effective treatment of diseases. Advanced technologies, such as Microfluidic Devices and Next-Generation Sequencing (NGS), enhance analytical sensitivity, providing more accurate results. Data analytics is a significant trend in clinical laboratory services, enabling the interpretation of complex data and improving patient outcomes. Biopsy analysis and disease monitoring require stringent biohazard management to ensure safety and accuracy.

- The market is driven by the increasing prevalence of chronic diseases, the need for personalized medicine, and the growing emphasis on preventive healthcare. Improving expertise and training in handling technologically advanced diagnostic devices is crucial to mitigate the risk of incorrect diagnoses. The market for clinical laboratory services is expected to grow due to the increasing demand for accurate and timely diagnostic services, the development of advanced technologies, and the rising focus on cost-effective healthcare solutions.

Exclusive Customer Landscape

The clinical laboratory services market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the clinical laboratory services market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, clinical laboratory services market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abbott Laboratories - This company specializes in delivering accurate and dependable clinical laboratory results for healthcare professionals. Our services cater to the data requirements of medical practitioners, ensuring informed decision-making in patient care. By employing advanced technologies and rigorous quality control measures, we provide precise and actionable insights to enhance patient outcomes. Our commitment to excellence and innovation sets US apart, fostering trust and confidence among our clients.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- AP Moller Holding AS

- ARUP Laboratories

- Bio Rad Laboratories Inc.

- Cerba HealthCare

- Charles River Laboratories International Inc.

- Enzo Clinical Labs Inc.

- Eurofins Scientific SE

- Fresenius Medical Care AG and Co. KGaA

- Genova Diagnostics Inc.

- HU Group Holdings Inc.

- Illumina Inc.

- Laboratory Corp. of America Holdings

- NeoGenomics Laboratories Inc.

- OPKO Health Inc.

- QIAGEN NV

- Quest Diagnostics Inc.

- Siemens AG

- Sonic Healthcare Ltd.

- SYNLAB International GmbH

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Clinical Laboratory Services Market

- In February 2023, Roche Diagnostics, a leading provider of in vitro diagnostic solutions, launched the Cobas sARS-CoV-2 Variant Select Test, which can detect key SARS-CoV-2 variants, including Omicron, in a single test run (Roche Diagnostics Press Release). This technological advancement addresses the need for rapid and accurate identification of virus variants to inform public health responses.

- In March 2024, LabCorp and Quest Diagnostics, two major clinical laboratory service providers in the US, announced a strategic collaboration to offer combined COVID-19 testing services, allowing for expanded testing capacity and improved access to testing for patients (LabCorp Press Release). This partnership represents a significant shift in the competitive landscape of the market.

- In May 2024, Illumina, a global leader in genomic sequencing and array-based solutions, raised USD1.2 billion in a secondary offering to fund research and development efforts, including the expansion of its clinical and diagnostic offerings (Illumina Press Release). This substantial investment demonstrates the growing importance of genomic testing and sequencing in clinical laboratory services.

- In October 2025, the European Union's In Vitro Diagnostic Medical Devices Regulation (IVDR) came into effect, replacing the older In Vitro Diagnostic Medical Devices Directive (IVDD). This regulatory change aims to enhance safety and quality standards for in vitro diagnostic medical devices, including clinical laboratory services (European Commission Press Release). This initiative will likely lead to increased costs and regulatory compliance challenges for market players.

Research Analyst Overview

- The market is experiencing significant transformation, driven by advancements in technology and shifting healthcare priorities. Predictive analytics and lab operations optimization are key trends, enabling early disease detection and improving quality and efficiency. Serological assays, companion diagnostics, and precision diagnostics are gaining traction, enhancing patient care and outcomes. Patient engagement is a priority, with automated tissue processors and image analysis tools facilitating remote consultation and real-time results. Mass spectrometry and flow cytometry are essential for complex diagnostic testing, while lean management and six sigma methodologies ensure process automation and quality improvement. Population health management is a growing concern, with data visualization and healthcare cost containment strategies essential for effective health surveillance.

- Direct-to-consumer testing and home healthcare services are expanding, offering convenience and accessibility to patients. Real-time PCR technology is revolutionizing infectious disease diagnosis, ensuring swift and accurate results. Innovations in technology, such as automation and data analysis, are shaping the clinical laboratory services landscape, enabling more effective and efficient diagnostic processes. The market is expected to continue evolving, with a focus on improving patient care, reducing costs, and enhancing overall healthcare outcomes.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Clinical Laboratory Services Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

188 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 10.87% |

|

Market growth 2024-2028 |

USD 172.4 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

9.51 |

|

Key countries |

US, UK, China, Germany, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Clinical Laboratory Services Market Research and Growth Report?

- CAGR of the Clinical Laboratory Services industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the clinical laboratory services market growth of industry companies

We can help! Our analysts can customize this clinical laboratory services market research report to meet your requirements.

RIA -

RIA -