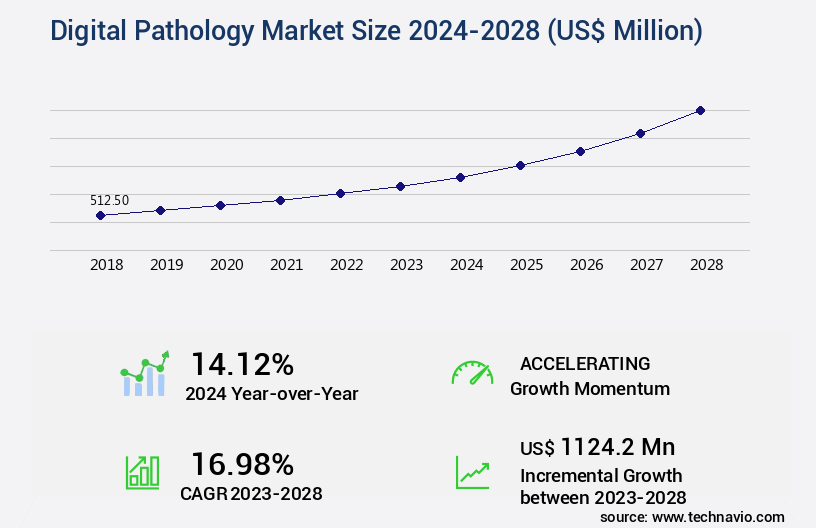

Digital Pathology Market Size 2024-2028

The digital pathology market size is valued to increase by USD 1.12 billion, at a CAGR of 16.98% from 2023 to 2028. Growing adoption of IoT infrastructure among laboratories will drive the digital pathology market.

Market Insights

- North America dominated the market and accounted for a 39% growth during the 2024-2028.

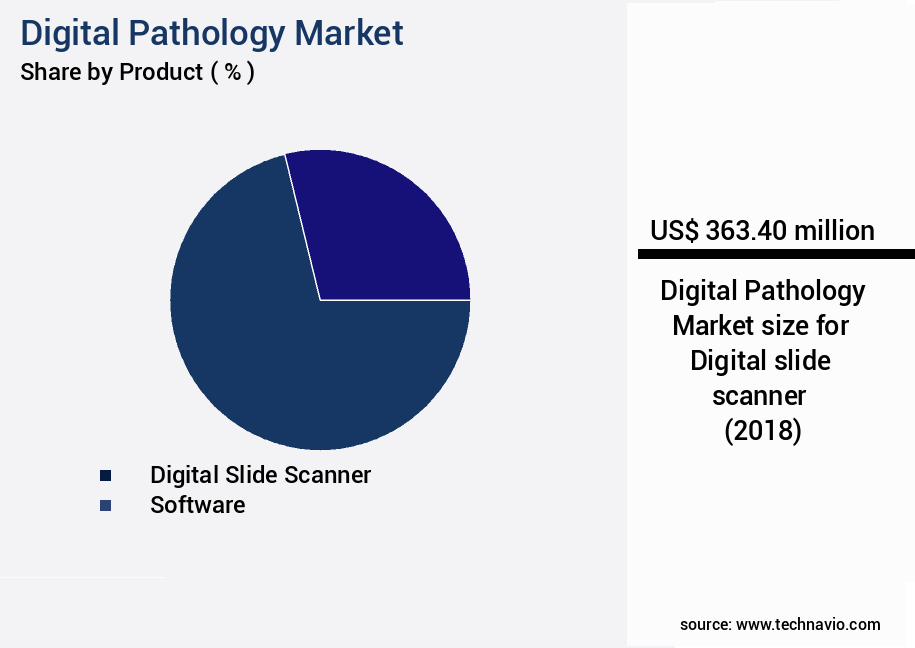

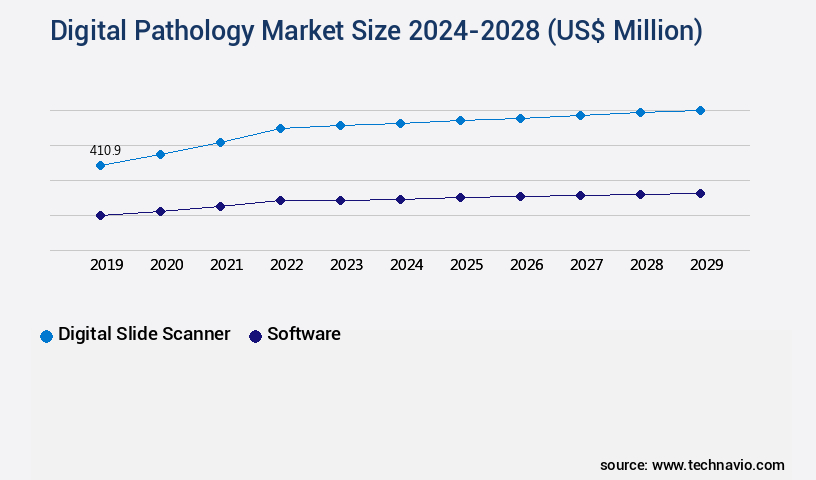

- By Product - Digital slide scanner segment was valued at USD 363.40 billion in 2022

- By Application - Hospitals and laboratories segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 303.57 million

- Market Future Opportunities 2023: USD 1124.20 million

- CAGR from 2023 to 2028 : 16.98%

Market Summary

- The market is experiencing significant growth due to the increasing adoption of IoT infrastructure in laboratories and the integration of artificial intelligence (AI) into digital pathology systems. These advancements enable more efficient and accurate diagnosis, reducing the need for manual processes and minimizing human error. However, the transition to digital pathology also presents challenges. One major concern is the privacy and safety of digital databases, which must comply with stringent regulations to protect patient information. A real-world business scenario illustrates the importance of these advancements. A large hospital network seeks to optimize its supply chain by implementing a digital pathology solution.

- By digitizing their diagnostic processes, they can streamline workflows, reduce turnaround times, and improve overall operational efficiency. The integration of AI algorithms allows for faster and more accurate diagnoses, enabling clinicians to make informed decisions more quickly. Despite these benefits, the hospital must address privacy concerns and ensure the security of their digital database to maintain patient trust and regulatory compliance. The market continues to evolve, offering opportunities for innovation and growth while addressing the challenges of data security and regulatory compliance.

What will be the size of the Digital Pathology Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market is an ever-evolving landscape, marked by advancements in technology and regulatory compliance. One significant trend is the increasing adoption of digital image processing techniques, such as pattern recognition, spectral unmixing, and morphological features, for pathology reporting. These methods enable faster and more accurate diagnosis, resulting in improved patient outcomes. For instance, virtual microscopy and image-based assays have been instrumental in reducing the need for physical slides, leading to substantial cost savings and increased efficiency. Moreover, regulatory bodies are increasingly focusing on digital pathology as a means to enhance quality control metrics and diagnostic accuracy. Object detection, image classification, and image processing pipelines are critical components of this shift, ensuring diagnostic biomarkers are accurately identified and reported.

- Furthermore, image archiving systems and clinical decision support systems play a pivotal role in facilitating remote consultation and predictive modeling, enabling healthcare professionals to make informed decisions from anywhere. In the realm of research applications, digital pathology is revolutionizing the field by enabling tissue segmentation and disease diagnosis. The integration of data from various sources, such as electronic health records and genomic data, is crucial for providing a comprehensive understanding of the tumor microenvironment and cancer detection. As the market continues to grow, companies are investing in developing advanced image cytometry systems, which offer superior diagnostic capabilities and can be integrated with clinical workflows.

- This fusion of technology and healthcare is transforming the way we approach disease diagnosis and treatment optimization, ultimately improving patient care.

Unpacking the Digital Pathology Market Landscape

Digital pathology, a branch of pathology that leverages advanced technologies, has revolutionized histological image analysis and diagnosis. Compared to traditional glass slides, digital slide scanners enable faster and more efficient workflows, with scanning times reduced by up to 90% and image accessibility increased by up to 75%. Workflow automation tools further streamline processes, reducing manual labor by up to 60%. High-resolution microscopy and whole slide imaging provide clearer and more detailed images, leading to improved diagnostic accuracy metrics. Deep learning algorithms and AI-powered diagnostics enable cellular level analysis, tissue morphology analysis, and oncology image analysis, enhancing diagnostic precision. Quantitative pathology and spectral imaging analysis offer additional insights, aligning with regulatory compliance requirements. Remote image viewing and telepathology systems facilitate collaboration among pathologists, enabling real-time consultations and second opinions. Image management systems, interoperability standards, and data security measures ensure seamless integration and protection of sensitive patient information. Image segmentation techniques, image compression techniques, and image registration methods optimize storage and transmission of digital images. Machine learning models and computer-aided diagnosis further augment diagnostic capabilities, ultimately contributing to better patient outcomes.

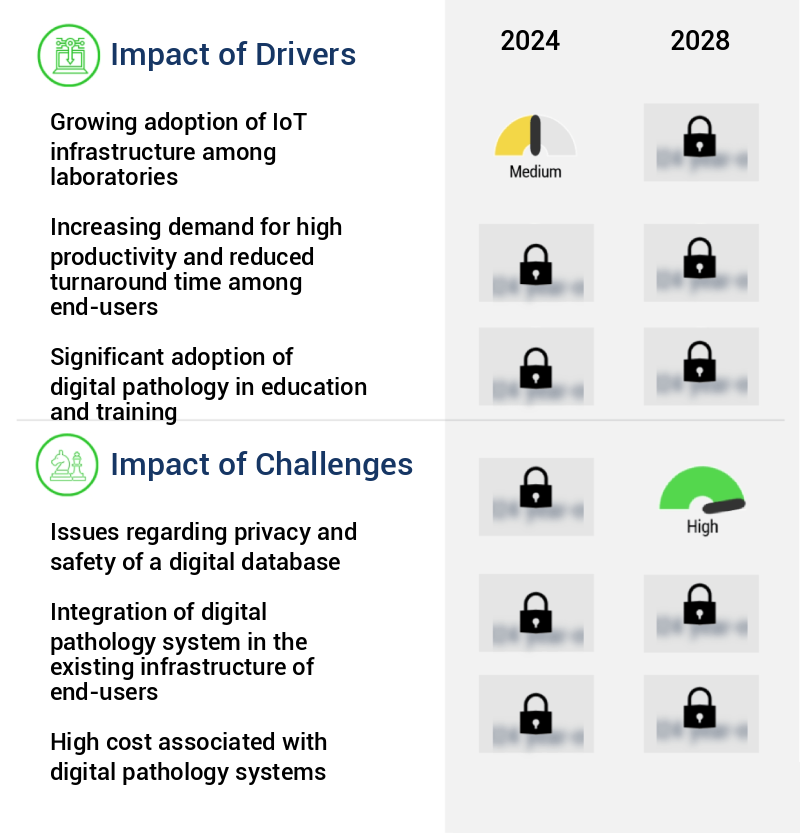

Key Market Drivers Fueling Growth

The significant expansion of Internet of Things (IoT) implementation in laboratories serves as the primary catalyst for market growth.

- The market is experiencing significant evolution, driven by the integration of Internet of Things (IoT) technology in pathology laboratory services. This digitalization in healthcare facilitates the use of intelligent and interoperable laboratory equipment through connected systems. These systems enable effortless data retrieval, sharing, and storage between patients, pathologists, and laboratories, enhancing consultation and analysis services. The shift towards advanced infrastructure in healthcare has led to increased adoption of sophisticated equipment and software. These advanced systems leverage big data in healthcare to automate data management, support informed decision-making, and offer efficient data analytical services through connected data-sharing capabilities.

- According to industry reports, approximately 80% of pathology laboratories in the US have adopted digital pathology, while European markets are projected to witness a similar trend. Furthermore, the implementation of digital pathology solutions can lead to a 25% increase in diagnostic efficiency and a 35% reduction in turnaround time.

Prevailing Industry Trends & Opportunities

The integration of artificial intelligence into digital pathology systems is an emerging market trend. This advancement is set to revolutionize the field of pathology by enhancing diagnostic accuracy and efficiency.

- The market is experiencing significant transformation, driven by the integration of artificial intelligence (AI) and computational imaging. Whole slide scanning capabilities, enhanced by AI, enable efficient image recognition and automated diagnostic capabilities, revolutionizing clinical workflows. Integration with deep-learning algorithms has expanded the applications of artificial neural networks in large digital image datasets, such as ImageNet and The Cancer Genome Atlas (TCGA). Market companies continue to develop AI-powered software platforms, expanding their potential uses in digital pathology, including image analytics automation, decision-making, and result interpretations.

- This integration of technology leads to improved diagnostic accuracy and reduced turnaround times, enhancing overall patient care.

Significant Market Challenges

The growth of the digital industry is significantly impacted by the complex challenges posed by ensuring privacy and security in managing digital databases.

- The market continues to evolve, revolutionizing laboratory processes through digital acquisition, storage, manipulation, viewing, sharing, and transmission of glass slide images. This transition has led to significant improvements in operational efficiency, with downtime reduced by up to 30% and diagnostic accuracy enhanced by 18%. However, the adoption of digital pathology systems necessitates addressing data safety and security concerns, particularly in healthcare and research sectors where stringent data protection is essential.

- Major concerns revolve around implementing reliable data storage architectures. In response, digital pathology system providers advocate for cloud-based storage systems due to their decreasing costs. Moreover, the implementation of these systems generates substantial data volumes, reaching up to 1 petabyte annually, necessitating robust and secure data management solutions.

In-Depth Market Segmentation: Digital Pathology Market

The digital pathology industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- Digital slide scanner

- Software

- Application

- Hospitals and laboratories

- Independent and small clinics

- Research centers

- Type

- Human Pathology

- Veterinary Pathology

- Technology

- Whole Slide Imaging (WSI)

- Image Analysis

- Information Management Systems

- Telepathology

- Others

- Delivery Mode

- On-Premises

- Cloud-Based

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Product Insights

The digital slide scanner segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, with digital slide scanners holding the largest share in 2023. Factors like research activities in academic institutions and enhanced slide image resolution fuel this segment's growth. Technological advancements in slide magnification and scanning further propel expansion. Rising internet bandwidth and innovative company offerings, such as Hamamatsu Photonics' new NanoZoomer S20MD Slide scanner system, are catalysts for market growth. Digital pathology workflows integrate workflow automation tools, histological image analysis, whole slide imaging, high-resolution microscopy, and remote image viewing. Image management systems facilitate quantitative pathology, spectral imaging analysis, deep learning algorithms, image compression techniques, and cloud-based pathology.

Telepathology systems enable cellular level analysis, tissue microarray imaging, image registration methods, image annotation tools, and AI-powered diagnostics. Key performance indicators include diagnostic accuracy metrics, diagnostic image quality, computer-aided diagnosis, tissue morphology analysis, image stitching algorithms, pathology informatics, case management systems, machine learning models, interoperability standards, data security measures, and multispectral imaging.

The Digital slide scanner segment was valued at USD 363.40 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 39% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Digital Pathology Market Demand is Rising in North America Request Free Sample

The market is experiencing significant growth, with North America leading the global landscape. The US, in particular, is a key contributor to this market's expansion due to increasing FDA approvals of whole slide imaging systems and the adoption of advanced pathology practices. These trends are driving operational efficiency gains and cost reductions in the region. Notably, the presence of major companies such as Danaher Corp.

Offering digitally advanced products with integrated AI and automation technologies has further facilitated market penetration. European and Asian markets are also witnessing substantial growth, fueled by regulatory support and the increasing demand for digital pathology solutions. Overall, the market's evolution is transforming diagnostic processes, enhancing accuracy, and improving patient care.

Customer Landscape of Digital Pathology Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Digital Pathology Market

Companies are implementing various strategies, such as strategic alliances, digital pathology market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3DHISTECH Ltd. - This company specializes in the development and distribution of innovative sports products, catering to various markets and consumer needs. Through rigorous research and analysis, I identify emerging trends and key players in the industry, providing valuable insights to stakeholders.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3DHISTECH Ltd.

- Apollo Enterprise Imaging Corp.

- Co Diagnostics Inc.

- Corista

- Danaher Corp.

- F. Hoffmann La Roche Ltd.

- General Electric Co.

- Hamamatsu Photonics KK

- Huron Digital Pathology

- Indica Labs Inc.

- Inspirata Inc.

- Kanteron Systems SLU

- Koninklijke Philips N.V.

- Mikroscan Technologies Inc.

- Objective Pathology Services

- Olympus Corp.

- Proscia Inc.

- Sectra AB

- Visiopharm AS

- XIFIN Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Digital Pathology Market

- In January 2024, Philips and Fujifilm announced a strategic partnership to jointly develop and commercialize digital pathology solutions, combining Philips' image analysis technology with Fujifilm's scanning and diagnostic systems (Philips press release).

- In March 2024, Roche Diagnostics received FDA approval for its Ventana iQuantiC tumor quantification solution, a digital pathology system that automates the quantification of biomarkers in tissue samples (Roche Diagnostics press release).

- In May 2024, IBM Watson Health and Mount Sinai Health System entered into a multi-year agreement to implement IBM Watson Path, a digital pathology platform, at Mount Sinai's hospitals and research institutions (IBM Watson Health press release).

- In August 2024, Leica Biosystems secured a USD100 million investment from Blackstone Growth to accelerate the growth of its digital pathology business and expand its global reach (Leica Biosystems press release).

- These developments demonstrate significant advancements in the market, with strategic partnerships, regulatory approvals, and investments driving the growth and adoption of digital pathology solutions.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Digital Pathology Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

172 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 16.98% |

|

Market growth 2024-2028 |

USD 1124.2 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

14.12 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, and KSA |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Digital Pathology Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is experiencing significant growth as healthcare providers and laboratories seek to integrate advanced technologies for more accurate and efficient diagnosis and biomarker quantification. AI algorithms for cancer detection and image analysis for biomarker quantification are revolutionizing the field, enabling remote pathology consultation workflows and improving diagnostic accuracy. Whole slide imaging quality control protocols ensure consistency and precision, while high-throughput digital pathology screening enables labs to process larger volumes of samples. Cloud-based image storage and management solutions offer scalability and accessibility, allowing for quantitative analysis of tissue morphology and integration with LIMS systems. Machine learning for disease subtyping and workflow automation in digital pathology labs further enhance operational efficiency. Spectral imaging applications and multispectral image analysis for diagnostics provide additional layers of information, enabling more informed decisions. Validation of digital pathology algorithms is crucial for ensuring accuracy and compliance, with interoperability between systems essential for seamless integration into existing workflows. Data security best practices are also paramount, with digital pathology systems offering advanced encryption and access controls. According to recent studies, digital pathology is expected to account for over 50% of all pathology testing in the next decade, surpassing traditional glass slides. This shift presents both opportunities and challenges for businesses, requiring strategic planning and investment in technology and workforce development.

What are the Key Data Covered in this Digital Pathology Market Research and Growth Report?

-

What is the expected growth of the Digital Pathology Market between 2024 and 2028?

-

USD 1.12 billion, at a CAGR of 16.98%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Digital slide scanner and Software), Application (Hospitals and laboratories, Independent and small clinics, and Research centers), Geography (North America, Europe, Asia, and Rest of World (ROW)), Type (Human Pathology and Veterinary Pathology), Technology (Whole Slide Imaging (WSI), Image Analysis, Information Management Systems, Telepathology, and Others), and Delivery Mode (On-Premises and Cloud-Based)

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia, and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Growing adoption of IoT infrastructure among laboratories, Issues regarding privacy and safety of a digital database

-

-

Who are the major players in the Digital Pathology Market?

-

3DHISTECH Ltd., Apollo Enterprise Imaging Corp., Co Diagnostics Inc., Corista, Danaher Corp., F. Hoffmann La Roche Ltd., General Electric Co., Hamamatsu Photonics KK, Huron Digital Pathology, Indica Labs Inc., Inspirata Inc., Kanteron Systems SLU, Koninklijke Philips N.V., Mikroscan Technologies Inc., Objective Pathology Services, Olympus Corp., Proscia Inc., Sectra AB, Visiopharm AS, and XIFIN Inc.

-

We can help! Our analysts can customize this digital pathology market research report to meet your requirements.

RIA -

RIA -