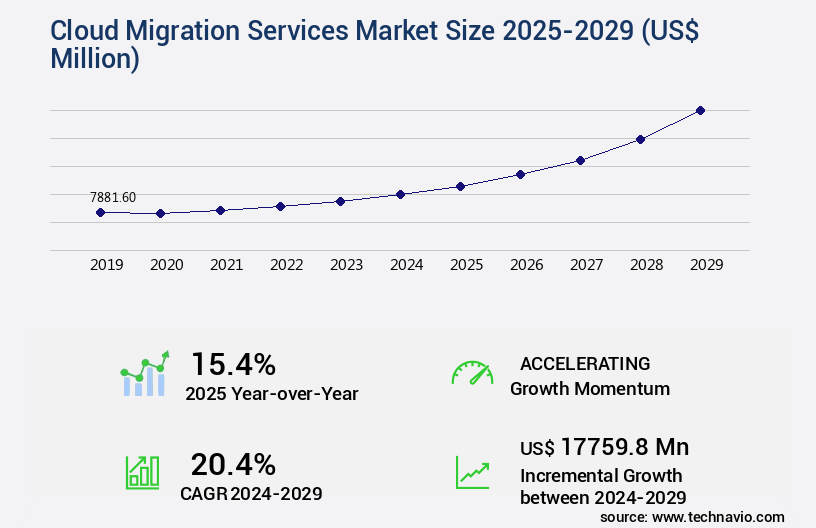

Cloud Migration Services Market Size 2025-2029

The cloud migration services market size is valued to increase by USD 17.76 billion, at a CAGR of 20.4% from 2024 to 2029. Rising demand for digital transformation will drive the cloud migration services market.

Major Market Trends & Insights

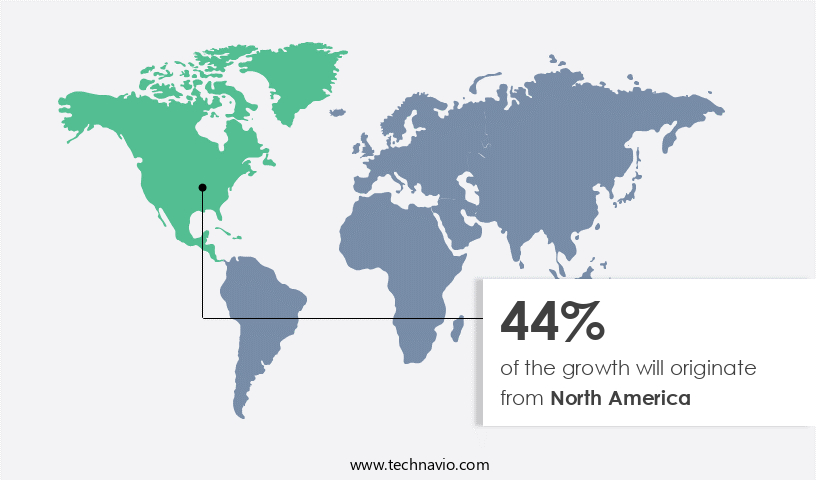

- North America dominated the market and accounted for a 44% growth during the forecast period.

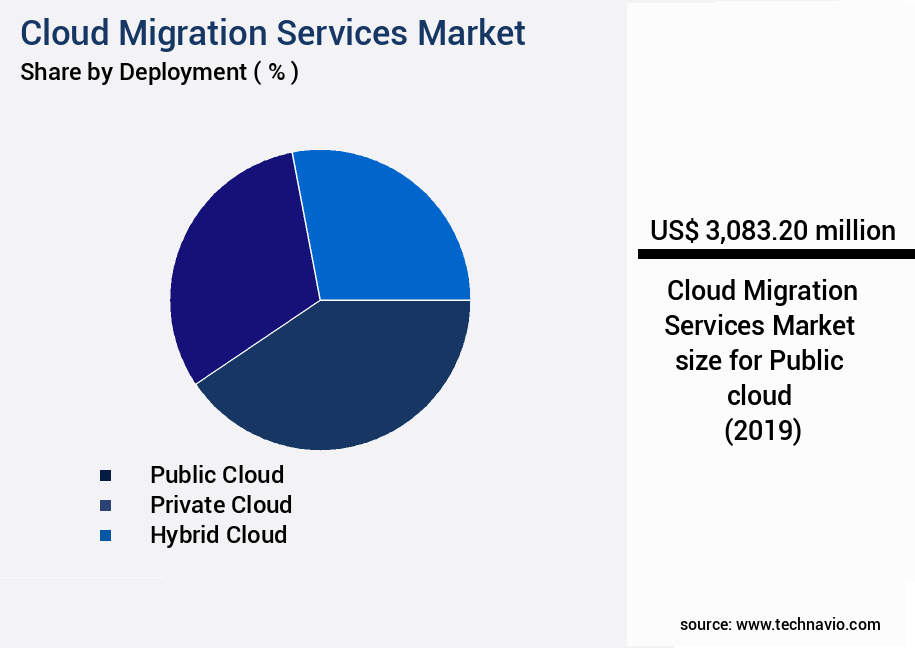

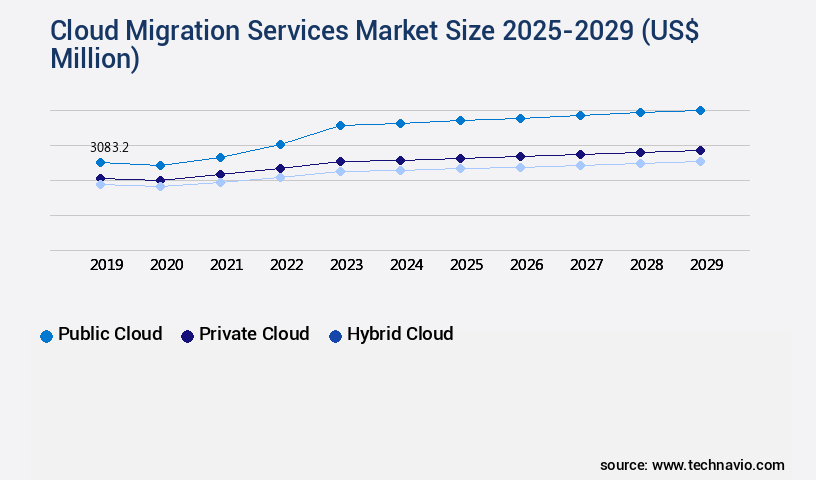

- By Deployment - Public cloud segment was valued at USD 3.08 billion in 2023

- By Service Type - Infrastructure migration segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 273.10 million

- Market Future Opportunities: USD 17759.80 million

- CAGR from 2024 to 2029 : 20.4%

Market Summary

- The market is experiencing significant growth due to the increasing demand for digital transformation among businesses worldwide. Companies are recognizing the benefits of moving their operations to the cloud, including increased operational efficiency, cost savings, and enhanced scalability. According to recent studies, businesses that have migrated to the cloud have seen error rates reduced by up to 25%, leading to improved productivity and customer satisfaction. However, the adoption of cloud migration services is not without challenges. Data Security and privacy concerns continue to be a major concern for organizations, particularly those in regulated industries. In a supply chain optimization scenario, a retailer migrating to the cloud may experience a 20% increase in processing speed, enabling faster order fulfillment and delivery.

- Yet, ensuring the security of sensitive customer data during the migration process is crucial to maintaining trust and avoiding potential regulatory penalties.

What will be the Size of the Cloud Migration Services Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Cloud Migration Services Market Segmented ?

The cloud migration services industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Deployment

- Public cloud

- Private cloud

- Hybrid cloud

- Service Type

- Infrastructure migration

- Platform migration

- Application migration

- Data migration

- Security and compliance services

- End-user

- Large enterprises

- SMEs

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- Australia

- China

- India

- Japan

- South America

- Brazil

- Rest of World (ROW)

- North America

By Deployment Insights

The public cloud segment is estimated to witness significant growth during the forecast period.

The market is undergoing continuous evolution, with public cloud deployment representing a significant segment. Enterprises are transitioning workloads to third-party managed infrastructure like Amazon Web Services, Microsoft Azure, and Google Cloud, favoring the operational flexibility and accessibility of this model. Key drivers include cost efficiency, enabled by pay-as-you-go pricing, and improved budget predictability. Devops methodologies, migration project management, and risk mitigation strategies are essential components of this transition. Performance monitoring, system integration testing, disaster recovery planning, and high availability design are crucial elements of a successful migration. Network optimization strategies, data center consolidation, ITIL framework, cloud infrastructure assessment, and scalability testing are also integral.

Hybrid cloud migration, CI/CD pipeline, backup and recovery, application modernization, cloud security architecture, multi-cloud strategy, containerization technologies, cloud company selection, business continuity plan, database migration tools, legacy system migration, risk assessment methodology, server virtualization techniques, data loss prevention, automated deployment, cloud cost optimization, data migration strategies, Data Governance framework, capacity planning, change management processes, IT infrastructure audit, application compatibility testing, and microservices architecture are all integral parts of the migration process. According to a recent study, over 90% of enterprises have adopted or plan to adopt cloud services, underscoring the market's growing importance.

The Public cloud segment was valued at USD 3.08 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 44% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Cloud Migration Services Market Demand is Rising in North America Request Free Sample

The North American the market is witnessing significant growth, fueled by the increasing adoption of digital transformation initiatives, artificial intelligence (AI) integration, and the implementation of hybrid cloud strategies. With the U.S. And Canada leading the way as the most mature cloud markets globally, enterprises across various sectors are modernizing legacy systems to enhance scalability, operational agility, and cost savings. The post-pandemic era has accelerated this trend, with the number of remote workers in the U.S. More than doubling from 9 million in 2019 to over 22 million in 2023. This shift towards cloud-native environments enables organizations to support remote work, improve business resilience, and foster innovation.

By adopting cloud migration services, companies can achieve operational efficiency gains of up to 30% and reduce IT infrastructure costs by up to 50%. These compelling benefits have made cloud migration a priority for businesses seeking to remain competitive in today's digital landscape.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth as enterprises seek to modernize their IT infrastructure and take advantage of the numerous benefits offered by cloud computing. Cloud migration for enterprise applications has become a critical priority for businesses looking to increase agility, reduce costs, and enhance security. Assessing application readiness for cloud is a crucial initial step in the migration process. This involves evaluating the suitability of existing applications for cloud deployment and identifying any necessary modifications or upgrades. Implementing robust data security measures is another essential consideration, as businesses must ensure their data is protected during and after migration. Optimizing cloud infrastructure costs is a key driver for cloud migration, and designing a high availability cloud architecture is essential for ensuring business continuity during and after the migration process. Developing a comprehensive migration plan is necessary to minimize disruption and ensure a smooth transition. Managing cloud migration risks is a significant challenge, and businesses must take steps to mitigate potential issues. This includes planning for capacity scaling in the cloud, achieving compliance with industry standards, and integrating cloud services with existing IT infrastructure. Leveraging automation tools for efficient migration can help streamline the process and reduce the risk of errors. Migrating legacy systems to a modern cloud platform requires careful planning and execution. Implementing DevOps practices for cloud migration can help streamline the process and improve collaboration between development and operations teams. Monitoring and managing cloud resources is essential for ensuring optimal performance and maintaining security. In summary, the market is a dynamic and growing field, driven by the need for businesses to modernize their IT infrastructure, reduce costs, and enhance security. Cloud migration for enterprise applications involves assessing application readiness, implementing robust security measures, optimizing infrastructure costs, designing high availability architectures, managing risks, ensuring business continuity, leveraging automation tools, achieving compliance, and integrating cloud services with existing IT infrastructure.

What are the key market drivers leading to the rise in the adoption of Cloud Migration Services Industry?

- The surge in demand for digital transformation serves as the primary catalyst for market growth.

- The market is experiencing robust growth as businesses worldwide embrace digital transformation to stay competitive and agile. According to recent research, approximately 45% of European enterprises adopted cloud services in 2023, marking a 4% increase from 2021. This trend is not limited to Europe; the global adoption rate continues to rise, driven by the need for faster decision-making, automation, and scalable infrastructure. Cloud computing, artificial intelligence, Data Analytics, and the Internet of Things are central to digital transformation strategies, enabling organizations to streamline processes, reduce downtime, and improve forecast accuracy by up to 18%.

What are the market trends shaping the Cloud Migration Services Industry?

- Focusing on new product launches is currently a significant market trend. This trend prioritizes the introduction of innovative and improved offerings to cater to consumer demands.

- The market is experiencing a strategic evolution, with a focus on new offerings that expedite enterprise cloud adoption, ensure regulatory compliance, and streamline complex migration processes. This shift underscores the growing demand for customized, high-assurance solutions addressing both technical and jurisdictional requirements. For instance, Capgemini and Orange's joint venture, Bleu, launched on January 15, 2024, caters to French public sector and critical infrastructure organizations. The platform, developed in collaboration with Microsoft, offers a cloud de confiance solution, ensuring alignment with national data sovereignty and regulatory mandates. Bleu supports secure migration to Microsoft 365 and Azure services and is anticipated to achieve the SecNumCloud 3 certification.

- These initiatives underline the market's commitment to providing robust, reliable, and compliant cloud migration services.

What challenges does the Cloud Migration Services Industry face during its growth?

- Data security and privacy concerns represent significant challenges that can impede industry growth. Companies must prioritize safeguarding sensitive information to maintain consumer trust and comply with regulations.

- The market is witnessing significant growth as more organizations adopt cloud solutions to enhance business agility, reduce costs, and improve efficiency. However, the shift to cloud environments presents new challenges, particularly in ensuring data security and privacy. According to recent studies, the average cost of a data breach is a substantial USD4 million for organizations worldwide. As sensitive workloads and confidential data are moved from on-premises to public or hybrid cloud platforms, the risk of cyberattacks, unauthorized access, and data loss increases.

- To mitigate these risks, robust encryption, secure APIs, identity and access management, and compliance with data protection regulations such as GDPR, HIPAA, and CCPA are essential throughout the migration lifecycle. By implementing these measures, businesses can optimize their cloud migration strategies, ensuring a secure and compliant transition to cloud environments.

Exclusive Technavio Analysis on Customer Landscape

The cloud migration services market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the cloud migration services market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Cloud Migration Services Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, cloud migration services market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accenture PLC - This company specializes in cloud migration services, utilizing proprietary tools for discovery and analysis, customized strategy and planning, automated execution, and support for sovereign cloud solutions across IaaS, PaaS, and SaaS models. Their approach ensures seamless transition and optimization for businesses.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture PLC

- Amazon Web Services Inc.

- Capgemini Service SAS

- Cognizant Technology Solutions Corp.

- Deloitte Touche Tohmatsu Ltd.

- DXC Technology Co.

- Google LLC

- HCL Technologies Ltd.

- Infosys Ltd.

- International Business Machines Corp.

- LTIMindtree Ltd.

- Microsoft Corp.

- Mphasis Ltd.

- NTT DATA Corp.

- Oracle Corp.

- Persistent Systems Ltd.

- Tata Consultancy Services Ltd.

- Veritis Group Inc.

- VMware Inc.

- Wipro Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Cloud Migration Services Market

- In August 2024, IBM announced the acquisition of Cloud Modernization Services provider, Lighthouse, to strengthen its hybrid cloud offerings. The deal, valued at approximately USD2.1 billion, aimed to accelerate IBM's cloud migration services for enterprise clients (IBM Press Release, 2024).

- In November 2024, Amazon Web Services (AWS) launched AWS Migration Hub, a centralized dashboard for managing and tracking migration projects across multiple AWS services. This tool aimed to simplify the migration process for businesses moving to AWS (AWS Press Release, 2024).

- In March 2025, Microsoft and Google Cloud entered a strategic partnership to offer joint solutions for cloud migration and digital transformation. The collaboration enabled seamless migration of workloads from Microsoft Azure to Google Cloud Platform (Microsoft Blog, 2025).

- In May 2025, Oracle Corporation announced the acquisition of NetSuite, a leading provider of cloud business software. This acquisition was expected to expand Oracle's cloud offerings and enhance its position in the market (Oracle Press Release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Cloud Migration Services Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

246 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 20.4% |

|

Market growth 2025-2029 |

USD 17759.8 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

15.4 |

|

Key countries |

US, UK, China, Germany, India, Japan, Australia, Brazil, France, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market continues to evolve, driven by the increasing adoption of cloud technologies across various sectors. DevOps methodologies have become essential in managing migration projects, ensuring seamless transitions and faster time-to-market. Migration risk mitigation strategies, such as performance monitoring, system integration testing, and disaster recovery planning, are crucial in minimizing potential disruptions. High availability design, network optimization strategies, and data center consolidation are key components of cloud infrastructure assessment, enabling businesses to optimize their cloud environments for optimal performance and cost savings. ITIL framework integration facilitates efficient cloud management and service delivery. Scalability testing, hybrid cloud migration, CI/CD pipeline, and backup and recovery are essential elements of application modernization.

- Cloud security architecture, multi-cloud strategy, containerization technologies, and cloud company selection are critical components of a robust cloud security posture. A recent study indicates that the cloud services market is expected to grow by over 20% annually. For instance, a leading retailer successfully migrated 80% of its workloads to the cloud, resulting in a 30% increase in sales. Data migration strategies, data governance frameworks, capacity planning, change management processes, IT infrastructure audits, application compatibility testing, microservices architecture, server virtualization techniques, data loss prevention, automated deployment, cloud cost optimization, and business continuity plans are all integral parts of a comprehensive cloud migration strategy.

What are the Key Data Covered in this Cloud Migration Services Market Research and Growth Report?

-

What is the expected growth of the Cloud Migration Services Market between 2025 and 2029?

-

USD 17.76 billion, at a CAGR of 20.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Public cloud, Private cloud, and Hybrid cloud), Service Type (Infrastructure migration, Platform migration, Application migration, Data migration, and Security and compliance services), End-user (Large enterprises and SMEs), and Geography (North America, Europe, APAC, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rising demand for digital transformation, Data security and privacy concerns

-

-

Who are the major players in the Cloud Migration Services Market?

-

Accenture PLC, Amazon Web Services Inc., Capgemini Service SAS, Cognizant Technology Solutions Corp., Deloitte Touche Tohmatsu Ltd., DXC Technology Co., Google LLC, HCL Technologies Ltd., Infosys Ltd., International Business Machines Corp., LTIMindtree Ltd., Microsoft Corp., Mphasis Ltd., NTT DATA Corp., Oracle Corp., Persistent Systems Ltd., Tata Consultancy Services Ltd., Veritis Group Inc., VMware Inc., and Wipro Ltd.

-

Market Research Insights

- The market is a continuously evolving landscape, with organizations increasingly recognizing the benefits of moving their IT infrastructure to the cloud. According to recent industry reports, over 70% of enterprises have already initiated cloud migrations, with this figure projected to reach 90% by 2025. One notable example of the market's impact is a mid-sized financial services company that saw a 35% increase in sales following their migration to a cloud platform. This shift enables businesses to optimize costs through cost allocation, automate processes using serverless computing and automation tools, and enhance security through techniques like data masking and encryption.

- Additionally, cloud services enable organizations to manage DNS, problem and incident management, API gateways, and monitoring dashboards more effectively. Industry growth expectations remain strong, with the market projected to expand at a steady rate in the coming years.

We can help! Our analysts can customize this cloud migration services market research report to meet your requirements.

RIA -

RIA -