Cognitive Media Solutions Market Size 2024-2028

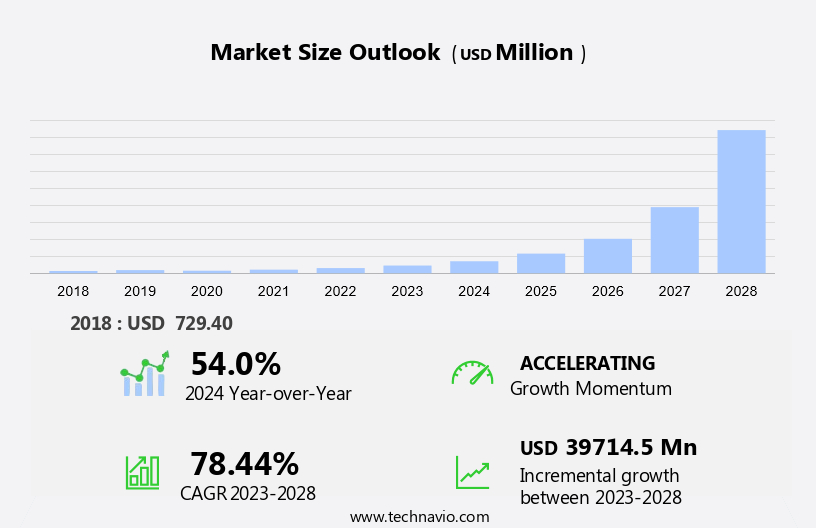

The cognitive media solutions market size is forecast to increase by USD 39.71 billion at a CAGR of 78.44% between 2023 and 2028.

- The market is experiencing significant growth due to the increasing adoption of advanced digital devices, such as smartphones and tablets, which enable the consumption of digital content in various formats. Artificial intelligence (AI) and analytics are key technologies driving this market, with applications ranging from visual analytics in the publishing and music industries to deep learning in education and autonomous vehicles. Cloud computing is facilitating the delivery and accessibility of cognitive media solutions, allowing for real-time data integration and automation. However, challenges remain, including system integration and interoperability issues, as well as the need for natural language processing and CRM software to effectively analyze and understand unstructured data. Overall, the market is poised for continued expansion as AI and analytics continue to transform the way we create, consume, and interact with digital content.

What will be the Size of the Cognitive Media Solutions Market During the Forecast Period?

- The market in the media industry is experiencing significant growth as media companies embrace automated workflows to enhance content creation and publishing processes. This market encompasses cognitive computing solutions that leverage artificial intelligence (AI) technologies such as deep learning, machine learning, and natural language processing to analyze and make decisions based on vast amounts of data. These advanced technologies enable media companies to triangulate data from multiple sources, including publishing platforms and subscriber bases, to deliver user-centric streaming content on demand. Cognitive media solutions are increasingly being deployed in the cloud and optimized for mobile devices, including smartphones, tablets, and internet browser-connected devices.

- The video-streaming sector, in particular, is witnessing a rise in demand for cognitive media solutions due to the growing consumer's screen time and the need for personalized content recommendations. Content owners are leveraging these solutions to improve operational efficiency, enhance user experience, and monetize their assets more effectively. Overall, the market is poised for continued growth as media companies seek to leverage AI technologies to gain a competitive edge and meet evolving consumer demands.

How is this Cognitive Media Solutions Industry segmented and which is the largest segment?

The industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- SME

- Large enterprises

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Middle East and Africa

- South America

- North America

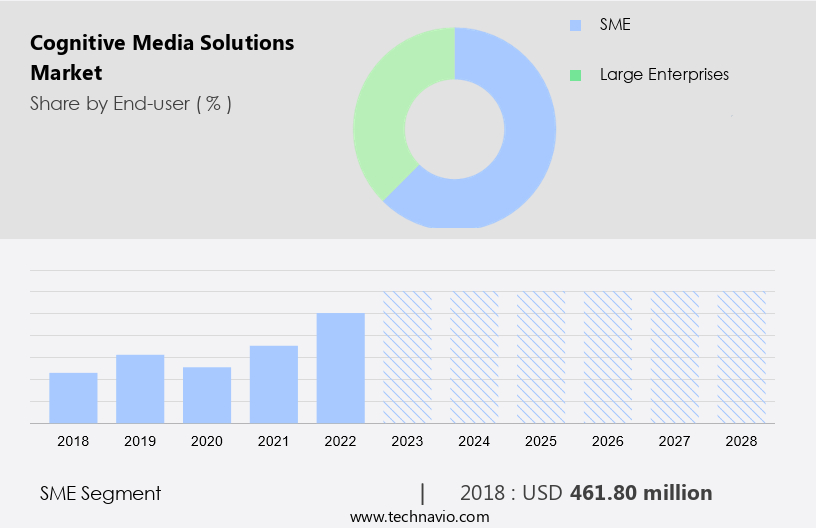

By End-user Insights

- The SME segment is estimated to witness significant growth during the forecast period.

Small and medium enterprises (SMEs) are increasingly adopting cognitive media solutions to enhance customer engagement and improve business insights. The media industry's shift towards technology-driven, omnichannel processes is leading SMEs to implement AI-powered platforms for marketing, sales, and customer relationship management. Cognitive media solutions offer intelligent, personalized experiences by analyzing customer data from various operations. These insights help SMEs to understand customer preferences, optimize content, and improve customer service. AI technologies, such as deep learning, machine learning, and natural language processing, enable cognitive media solutions to provide pre-purchase and post-purchase engagement experiences. Additionally, cognitive media solutions offer features like tagging content, content metadata management, network optimization, recommendation and personalization, security management, and support and maintenance.

These solutions assist in gaining customer feedback through surveys, managing billing and payments, providing technical support, and promoting campaigns. The adoption of cognitive media solutions is crucial for SMEs In the media industry to stay competitive and meet evolving consumer demands across various devices, including smartphone apps, tablets, and internet browser-connected devices.

Get a glance at the market report of share of various segments Request Free Sample

The SME segment was valued at USD 461.80 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

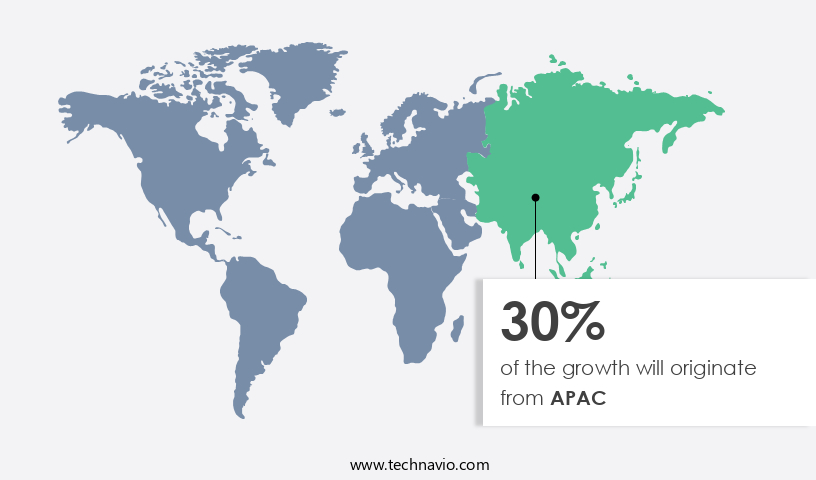

- APAC is estimated to contribute 30% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The market in the US and Canada is experiencing significant growth due to the adoption of these technologies by various end-user industries, including media and entertainment, automotive, retail, healthcare, hospitality, and BFSI. Cognitive computing solutions, such as deep learning, machine learning, and natural language processing, are being integrated into content management systems, network optimization, recommendation and personalization, security management, and content supply chain to enhance user experience and improve operational efficiency. Individual users are also adopting cognitive media solutions in their homes, fueled by the increasing availability of smart devices and advanced technologies like 5G and the production of autonomous vehicles.

The media industry is leveraging cognitive technologies to automate workflows, tag content, and create AI-based solutions for content strategy and metadata management. Cognitive media solutions play a critical role in the media industry by enabling content owners to analyze consumer behavior, predict customer churn, and optimize the content supply chain. These solutions are also used for content creation, programmatic marketing, and adblocking mitigation. The evolution of technology and the availability of skilled AI professionals are driving the adoption of cognitive media solutions in the region. Cognitive media solutions are available as software tools and platforms, with options for cloud and on-premises deployment.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Cognitive Media Solutions Industry?

Increasing adoption of technologically advanced mobile devices is the key driver of the market.

- The media industry is experiencing significant transformation due to the integration of cognitive computing technology into various applications. This technology, which includes Machine Learning, Deep Learning, Natural Language Processing, and AI predictive modeling, is revolutionizing content creation, management, and delivery. Automated workflows are streamlining internal functioning, enabling media companies to optimize network infrastructure, improve security management, and enhance user-centric streaming content. In the publishing sources sector, cognitive computing solutions are facilitating data triangulation, allowing for more accurate tagging of content and better organization of content metadata. Content professionals are utilizing AI-based solutions to improve content strategy and create more personalized and engaging experiences for consumers.

- The evolution of technology and the increasing use of cloud infrastructures have made cognitive media solutions accessible to a wider audience. These solutions offer support and maintenance, training and consulting, and can be deployed on both cloud and on-premises. The media industry's subscriber base is increasingly relying on smartphone apps, tablets, and Internet browser-connected devices for their viewing experience. Cognitive media solutions are also playing a critical role in areas such as programmatic marketing, recommendation and personalization, and content supply chain management. The use of AI technology is helping media companies to minimize customer churn, improve content metadata, and enhance the overall viewing experience.

What are the market trends shaping the Cognitive Media Solutions Industry?

High utilization of social media is the upcoming market trend.

- Cognitive computing technology is revolutionizing the media industry by automating workflows and enhancing content creation through advanced technologies such as Deep Learning, Machine Learning, and Natural Language Processing. Media companies are leveraging cognitive solutions to optimize their content management systems, improve network optimization, and deliver personalized recommendations to their subscriber base. These AI-based solutions enable media organizations to tag content effectively, analyze customer churn, and develop content strategies based on consumer behavior and preferences. Moreover, cognitive media solutions are critical for media companies to manage their content supply chain, including music, films, and video-streaming services, across various devices such as smartphone apps, tablets, and Internet browser-connected devices.

- AI predictive modeling and programmatic marketing help media companies to engage customers effectively and mitigate adblocking. Content professionals can benefit from these cognitive solutions by streamlining their workflows and focusing on creative tasks. Cloud deployment and on-premises infrastructures are key considerations for media companies when adopting cognitive media solutions. Skilled AI professionals are in high demand to support and maintain these complex systems, ensuring the viewing experience remains optimal for consumers. As technological developments continue to evolve, media companies must adapt to stay competitive and meet the changing demands of their audience.

What challenges does the Cognitive Media Solutions Industry face during its growth?

System integration and interoperability issues is a key challenge affecting the industry growth.

- Cognitive computing technology plays a critical role in the media industry by automating workflows and enhancing content creation through AI-based solutions. Content owners leverage deep learning and machine learning technologies for data triangulation and tagging content for efficient content management. Automation of workflows, including network optimization, recommendation and personalization, security management, and content strategy, improves internal functioning and customer engagement. However, integrating cognitive computing solutions with existing IT infrastructures can pose technical challenges. Differences in software versions and hardware requirements may lead to interoperability issues and potential disruptions. Migrating data from on-premises to cloud-based analytics software can also create complications due to varying protocols.

- Despite these challenges, the evolution of technology and the increasing importance of AI technology in the content supply chain have driven media companies to invest in cognitive computing solutions. Content professionals rely on these AI-driven tools for content metadata management, AI predictive modeling, and programmatic marketing. Consumers' increasing screen time on smartphone apps, tablets, and Internet browser-connected devices demands a user-centric streaming content experience. Cloud deployment and machine learning enable media companies to manage their subscriber base more effectively, while security management and software tools ensure the protection of valuable content. Skilled AI professionals are in high demand to address the complexities of implementing and maintaining these cognitive computing solutions.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Acrolinx GmbH

- Adobe Inc.

- Albert Technologies

- Alphabet Inc.

- Amazon.com Inc.

- Axle Ai Inc

- Baidu Inc.

- ByteDance Ltd.

- Cision US Inc.

- Clarifai Inc.

- International Business Machines Corp.

- Microsoft Corp.

- MiQ Digital Ltd

- NVIDIA Corp.

- Phrasee Ltd

- Salesforce Inc.

- SAP SE

- Skai

- SoundHound AI Inc.

- Valossa Labs Ltd

- Veritone Inc

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market continues to gain momentum in the media industry as automated workflows become increasingly essential for content creation and publishing sources. This technology, which leverages deep learning, machine learning, and natural language processing, is revolutionizing content management and network optimization. Cognitive computing solutions are transforming the way media companies handle their content supply chain. By implementing AI-based solutions, media organizations can streamline their operations, reduce customer churn, and improve user experience. These technologies enable tagging content with metadata, making it easier for content professionals to manage and distribute content across various platforms. The evolution of technology has led to the emergence of cloud infrastructures and on-premises solutions for cognitive computing.

Moreover, these platforms offer support and maintenance, training, and consulting services to help media companies optimize their IT infrastructures. Data triangulation is a critical role played by cognitive computing technology in the media industry. It involves the use of multiple data sources to provide accurate and reliable insights. Machine learning algorithms analyze vast amounts of data to identify patterns and trends, which can then be used to inform content strategy and personalized recommendations. The media industry's technological developments have also led to the automation of workflows, allowing content writers and editors to focus on more creative tasks. AI predictive modeling is used to anticipate consumer behavior and preferences, enabling programmatic marketing and targeted advertising.

However, the rise of adblocking and the increasing use of mobile devices, smartphone apps, tablets, and internet browser-connected devices have created new challenges for media companies. Cognitive computing solutions are helping to address these challenges by optimizing the viewing experience across various platforms and devices. Security management is another area where cognitive computing technology is making a significant impact. AI-based solutions are being used to analyze user behavior and detect potential security threats, ensuring the protection of valuable media assets.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

153 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 78.44% |

|

Market growth 2024-2028 |

USD 39.71 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

54.0 |

|

Key countries |

US, China, UK, Germany, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Cognitive Media Solutions Market Research and Growth Report?

- CAGR of the Cognitive Media Solutions industry during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the cognitive media solutions market growth of industry companies

We can help! Our analysts can customize this cognitive media solutions market research report to meet your requirements.

RIA -

RIA -