Commercial Aircraft Emergency Generators Market Size 2024-2028

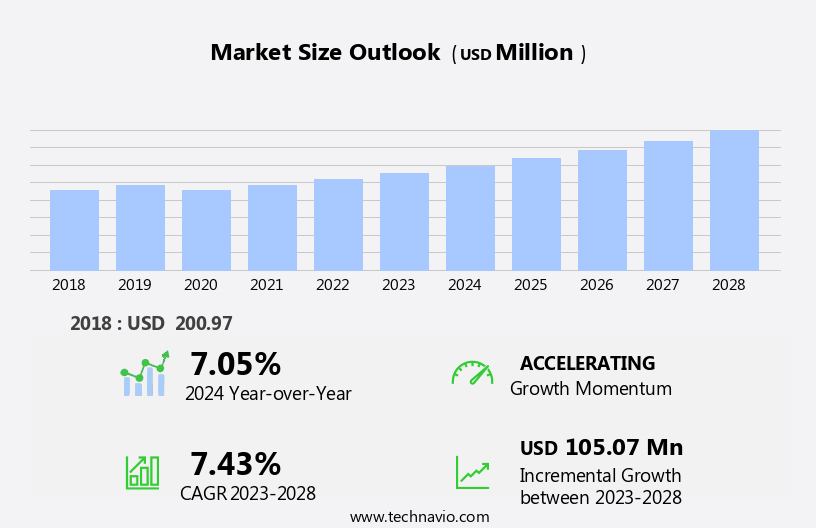

The commercial aircraft emergency generators market size is forecast to increase by USD 105.07 million at a CAGR of 7.43% between 2023 and 2028.

What will be the Size of the Commercial Aircraft Emergency Generators Market During the Forecast Period?

How is this Commercial Aircraft Emergency Generators Industry segmented and which is the largest segment?

The commercial aircraft emergency generators industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Narrow-body aircraft

- Wide-body aircraft

- Regional aircraft

- Channel

- OEM

- Aftermarket

- Geography

- North America

- Canada

- US

- Europe

- Germany

- France

- APAC

- China

- South America

- Middle East and Africa

- North America

By Application Insights

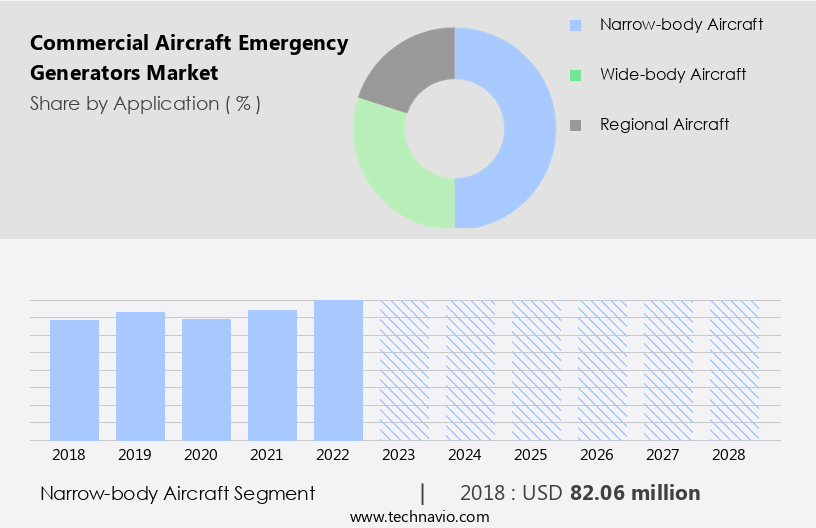

The narrow-body aircraft segment is estimated to witness significant growth during the forecast period. Narrow-body aircraft, characterized by single-aisle cabins enabling up to 6-abreast seating and twin-engine setup at the wings, are driving growth In the commercial aviation sector. Efficiency-focused airline operations in both emerging and developed economies, influenced by average load factors and seasonality, are fueling demand. Aircraft Original Equipment Manufacturers (OEMs) are responding by delivering upgraded versions and investing in new narrow-body aircraft, while low-cost carriers (LCCs) modernize their fleets to maintain competitiveness. Aircraft power systems, including reliable and efficient generators, are a critical focus area for OEMs, addressing challenges in power consumption, distribution, and management. Innovations in generator design, performance, and functionality, along with advancements in aircraft electrical systems and battery technology, are shaping the future of aircraft power.

Aviation safety regulations continue to emphasize the importance of stable power supplies for navigation systems, avionics power supply, and aircraft maintenance. The aviation industry is witnessing trends towards energy efficiency, electric propulsion, and aviation technology, including green aviation, sustainable aviation, and renewable energy aviation. Aircraft certification, aircraft production, and aircraft engine technology are also undergoing significant changes. Aviation investment In these areas is expected to continue, driven by the need for improved aircraft performance and components, as well as aviation safety and regulations. Aerospace engineering and aircraft electrification are key areas of focus for OEMs and investors alike.

Get a glance at the market report of various segments Request Free Sample

The Narrow-body aircraft segment was valued at USD 82.06 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

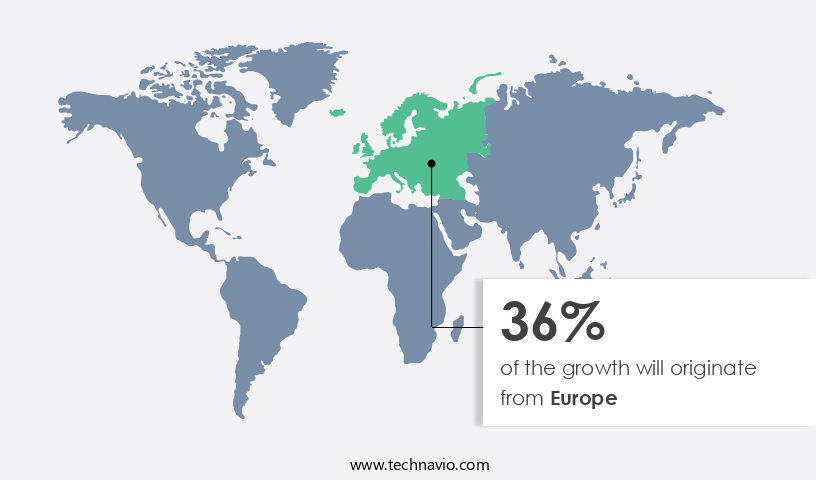

Europe is estimated to contribute 36% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The commercial aircraft industry in North America, driven primarily by the United States, is a mature market with a strong focus on aircraft power systems. Aircraft power solutions, including efficient and reliable generators, are essential for ensuring stable power supplies to aircraft electrical systems, avionics, navigation systems, and aircraft batteries. The increasing demand for aircraft production, driven by the resurging US economy and growing air travel, necessitates the development of innovative and lightweight generator technologies. These advancements aim to enhance aircraft performance, reduce power consumption, and improve overall aircraft efficiency. The aviation industry is also exploring renewable energy avenues for sustainable aviation, which is expected to influence future aircraft design and certification.

Aircraft power management and generator reliability are critical aspects of aviation safety regulations. Tier-1 and Tier-2 suppliers In the region are investing in research and development to meet the evolving demands of major commercial aircraft manufacturers, such as Boeing Co. And Bombardier Inc., and stay competitive In the global market. The future of aircraft power systems lies in advanced generator design, aviation innovation, and energy efficiency, including electric propulsion and aircraft battery technology.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Commercial Aircraft Emergency Generators Industry?

- Growing demand for new generation aircraft is the key driver of the market.The global commercial aviation sector is experiencing substantial expansion, driven by rising air traffic, both domestically and internationally. Emerging economies In the Asia Pacific region, including India, China, and Indonesia, are spearheading this growth. The increasing demand for air travel In these countries is leading to an escalating need for narrow-body aircraft, thereby fueling the growth of the market. These generators play a crucial role in ensuring aircraft power safety and reliability during emergencies. Aircraft power innovation and efficiency are key trends In the market, with a focus on lightweight generators and advanced aircraft power management systems. The aviation industry is also investing in sustainable aviation solutions, such as renewable energy aviation and aircraft electrification, to address the challenges of aircraft power consumption and distribution.

Aviation safety regulations continue to emphasize the importance of stable power supplies for navigation systems, avionics power supply, and aircraft maintenance. Aircraft generator maintenance and generator functionality are critical aspects of aircraft electrical systems, and generator reliability is a top priority for aircraft manufacturers and operators. The future of aircraft power systems lies in advanced generator technology, aircraft battery systems, and electric propulsion, which will enable greater energy efficiency and performance. The aviation market is expected to continue its growth trajectory, with the supply chain focusing on aircraft components, aviation technology, and aerospace engineering to meet the evolving demands of the industry.

What are the market trends shaping the Commercial Aircraft Emergency Generators market?

- Rising focus on increasing efficiency and performance of aircraft electrical systems is the upcoming market trend.The global aerospace industry is focusing on enhancing aircraft power safety and efficiency by investing in reliable aircraft power solutions. Innovations in aircraft power technology include lightweight generators and improved generator performance, aiming to address the challenges of aircraft power consumption and distribution. Aviation power systems are evolving to meet the demands of aviation safety regulations and the increasing use of navigation systems, avionics, and aircraft maintenance. The aviation industry trends indicate a shift towards electric propulsion, aircraft battery technology, and aircraft electrification, which require stable power supplies and generator reliability. The aviation market is witnessing significant investment in aircraft production, aircraft engine technology, and aerospace engineering to meet the demands for energy efficiency and sustainable aviation through renewable energy aviation.

Aircraft design and certification processes are prioritizing flight efficiency and aircraft performance, making generator functionality and aircraft power management crucial components of the aviation industry.

What challenges does the Commercial Aircraft Emergency Generators Industry face during its growth?

- Replacement of RAT with fuel cell technology is a key challenge affecting the industry growth.The market plays a crucial role in ensuring aircraft power safety and reliability. Innovations in aircraft power technology focus on efficiency and performance to reduce consumption and improve generator functionality. However, the aviation industry faces challenges in aircraft power distribution and maintenance, necessitating the need for stable power supplies and reliable aircraft power solutions. Aviation power systems are subject to stringent safety regulations, including those related to navigation systems, aircraft maintenance, and avionics power supply. Aircraft battery systems and generator maintenance are essential components of aircraft power management. The future of aircraft power systems lies in advanced generator design, renewable energy aviation, and aircraft electrification.

Airbus SE is at the forefront of aviation power trends, having conducted extensive research on fuel cell technology as a potential replacement for traditional auxiliary power units and RATs. The integration of fuel cells as a multifunctional emergency power source could significantly impact the market dynamics. The aviation industry's investment in aircraft production, aircraft engine technology, and aerospace engineering continues to drive the need for efficient and reliable aircraft power systems. The focus on energy efficiency, electric propulsion, and aircraft battery technology is shaping the future of the aviation market and the aircraft supply chain.

Exclusive Customer Landscape

The commercial aircraft emergency generators market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the commercial aircraft emergency generators market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, commercial aircraft emergency generators market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

ATGI - Advanced Technologies Group Inc. Provides commercial aircraft emergency generators, including the High Powered Ram Air Turbine (HP-RAT), which generates over 60kw of power at an airspeed of 250 knots. This innovative technology, developed by Advanced Technologies Group Inc., ensures uninterrupted power supply during aircraft emergencies. The HP-RAT is designed to meet the stringent requirements of the aviation industry, offering reliable and efficient power solutions for commercial aircraft.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ATGI

- General Electric Co.

- Honeywell International Inc.

- RTX Corp.

- Safran SA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Commercial aircraft operate in an environment where a stable and reliable power supply is essential for ensuring the safety and efficiency of operations. The demand for innovative and efficient aircraft power solutions continues to grow, driven by the increasing complexity of avionics systems and the need for reduced fuel consumption. Aircraft power systems have evolved significantly over the years, with a focus on improving performance, reliability, and efficiency. Lightweight generators have gained popularity due to their ability to reduce overall aircraft weight and improve fuel economy. These generators are designed to provide stable power to electrical systems, ensuring the proper functioning of navigation systems, avionics, and other critical components.

The aviation industry is constantly seeking ways to address the challenges associated with aircraft power distribution and management. Aviation safety regulations require that aircraft electrical systems be designed to ensure a reliable power supply at all times. Generator functionality and reliability are critical factors in meeting these requirements. Aircraft battery systems have also gained attention as a potential solution for reducing aircraft power consumption and improving efficiency. Battery technology has advanced significantly in recent years, with a focus on increasing energy density and improving charging efficiency. However, challenges remain in terms of weight, cost, and the need for efficient charging systems.

The aviation industry is also exploring the potential of renewable energy sources for powering aircraft. Green aviation and sustainable aviation are becoming increasingly important areas of focus, with research and development efforts focused on developing electric propulsion systems and other renewable energy technologies. Aircraft certification is a critical aspect of the aviation industry, and power systems must meet strict safety and performance standards. Aviation regulations require that all aircraft components, including power systems, undergo rigorous testing and certification processes to ensure they meet these standards. The aviation market is a dynamic and complex industry, with ongoing trends and challenges shaping the future of aircraft power systems.

Aviation investment and manufacturing continue to be significant drivers of innovation and growth in this sector. Aerospace engineering and aircraft design are also critical areas of focus, with a focus on developing more efficient and sustainable aircraft power systems. In conclusion, the market is a critical area of focus for the aviation industry, with a need for innovative and efficient power solutions that meet strict safety and performance standards. The market is driven by ongoing trends and challenges, including the need for reduced fuel consumption, improved reliability, and the exploration of renewable energy sources. The future of aircraft power systems is likely to be shaped by continued innovation and investment in advanced technologies and sustainable solutions.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

150 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.43% |

|

Market growth 2024-2028 |

USD 105.07 million |

|

Market structure |

Concentrated |

|

YoY growth 2023-2024(%) |

7.05 |

|

Key countries |

US, Canada, China, Germany, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Commercial Aircraft Emergency Generators Market Research and Growth Report?

- CAGR of the Commercial Aircraft Emergency Generators industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the commercial aircraft emergency generators market growth of industry companies

We can help! Our analysts can customize this commercial aircraft emergency generators market research report to meet your requirements.

RIA -

RIA -