Computer Servers Market Size 2024-2028

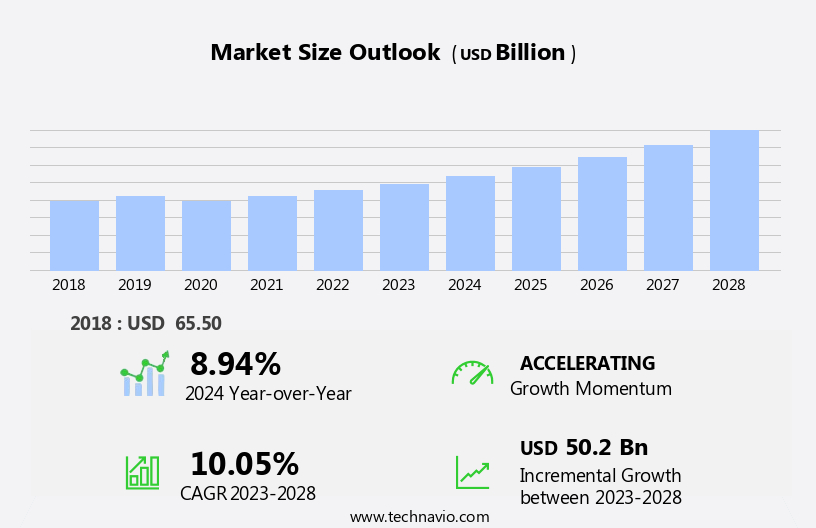

The computer servers market size is forecast to increase by USD 50.2 billion, at a CAGR of 10.05% between 2023 and 2028.

- The market is experiencing significant growth, driven by escalating investments in the construction of hyperscale data centers. These data centers demand an increasing number of servers to accommodate the surging digital transformation and cloud computing adoption. Moreover, technological advancements in the market, such as the integration of artificial intelligence and machine learning capabilities, are fueling the demand for high-performance servers. However, this market landscape is not without challenges. Security concerns, particularly the threat of cyberattacks and data breaches, pose a significant obstacle. As businesses increasingly rely on servers to store sensitive information, ensuring robust security measures becomes crucial.

- Companies must prioritize implementing advanced security features and protocols to mitigate these risks and maintain customer trust. In summary, the market presents lucrative opportunities for growth, fueled by the digital transformation and technological advancements. However, companies must navigate the challenges, particularly the security concerns, to capitalize on these opportunities and maintain a competitive edge.

What will be the Size of the Computer Servers Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by the ever-increasing demand for advanced technology solutions across various sectors. AI workloads and network connectivity are key factors fueling this growth, with an emphasis on CPU cores and operating systems that can efficiently handle complex data processing tasks. Big data analytics and edge computing require significant power consumption, leading to innovations in thermal management and server procurement. Database servers and server management software play a crucial role in ensuring system performance and data security. Virtual machines and server virtualization enable businesses to optimize their data center infrastructure and reduce costs.

Disaster recovery and server decommissioning are essential components of server lifecycle management, ensuring business continuity and reducing IT expenses. The ongoing evolution of server technology includes the adoption of ARM architecture and high availability features, as well as software-defined networking and high performance computing. Web servers and cloud computing have transformed the way businesses operate, while gaming servers cater to the growing demand for immersive entertainment experiences. Network attached storage and storage area networks provide the necessary capacity for managing and storing large volumes of data. Server uptime is a critical metric for businesses, and machine learning applications are being integrated into server systems to improve performance and efficiency.

In the dynamic and ever-changing landscape of the market, these trends and patterns continue to unfold, shaping the future of technology solutions.

How is this Computer Servers Industry segmented?

The computer servers industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Large enterprises

- Small and medium enterprises

- Geography

- North America

- US

- Canada

- Europe

- Germany

- UK

- APAC

- China

- Rest of World (ROW)

- North America

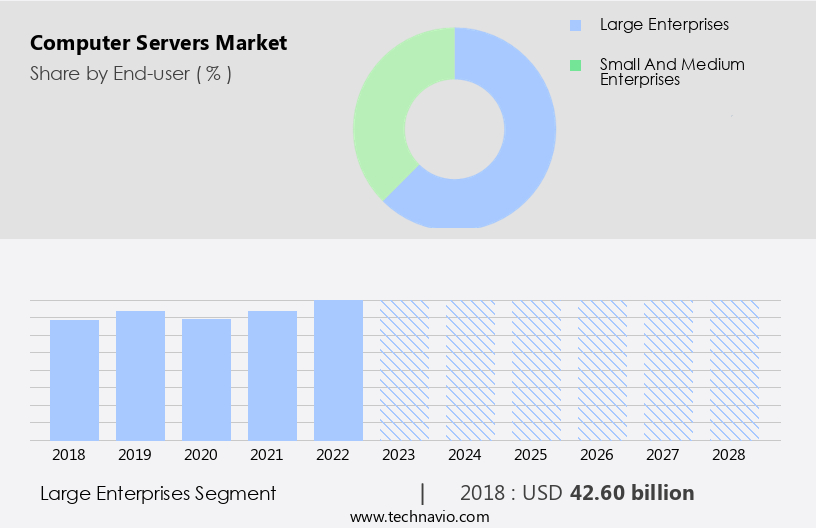

By End-user Insights

The large enterprises segment is estimated to witness significant growth during the forecast period.

The market is witnessing significant growth, driven by the increasing demand for advanced IT infrastructure from large enterprises. These businesses, particularly in sectors such as IT, telecom, healthcare, banking, financial services, and insurance (BFSI), and defense, are investing heavily to manage escalating enterprise data volumes. Upgrading IT infrastructure offers numerous benefits, including enhanced storage capacity, improved security, and faster processing speeds for high-volume data. Network connectivity and server virtualization are crucial factors fueling this trend. The adoption of big data analytics, machine learning applications, and edge computing is driving the need for more powerful and efficient servers.

Operating systems, such as Linux and Windows, continue to dominate the market, while database servers and application servers are essential components of modern IT infrastructure. Power consumption and thermal management are critical concerns for data center infrastructure, leading to the increasing popularity of x86 architecture, blade servers, and rackmount servers. High availability and disaster recovery solutions ensure uninterrupted server uptime, while server management software and virtual machines facilitate efficient server utilization. Cloud computing and web servers are transforming the market landscape, with many businesses opting for server procurement from cloud service providers. Data security is a top priority, leading to the adoption of server lifecycle management and server maintenance best practices.

Storage capacity, gaming servers, and server decommissioning are other areas of focus for the market. In conclusion, the market is evolving rapidly, with large enterprises leading the charge due to their significant IT infrastructure investments. The market is driven by factors such as network connectivity, cpu cores, operating systems, big data analytics, edge computing, power consumption, database servers, server management software, virtual machines, data security, application servers, disaster recovery, server decommissioning, system performance, storage area network, ram capacity, server virtualization, data center infrastructure, x86 architecture, blade servers, high availability, software defined networking, high performance computing, web servers, cloud computing, tower servers, rackmount servers, server lifecycle management, server maintenance, storage capacity, gaming servers, thermal management, arm architecture, and server uptime.

The Large enterprises segment was valued at USD 42.60 billion in 2018 and showed a gradual increase during the forecast period.

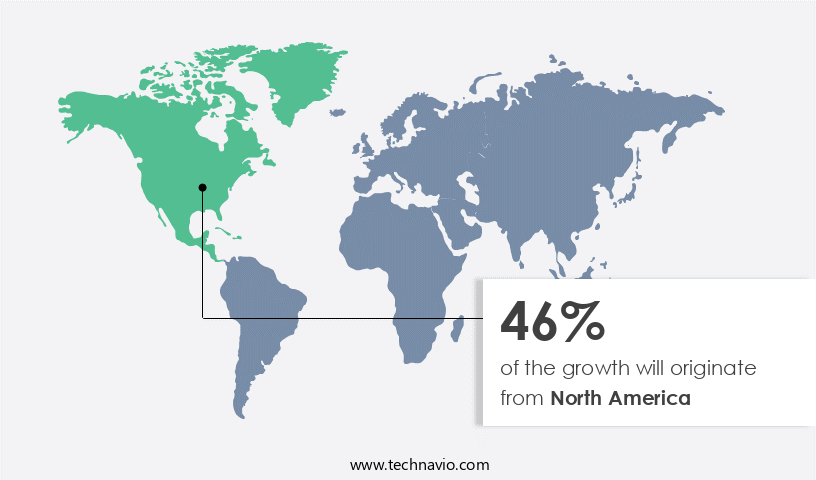

Regional Analysis

North America is estimated to contribute 46% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market is witnessing significant growth, driven by the increasing adoption of artificial intelligence workloads, edge computing, and high performance computing. Network connectivity and power consumption are crucial factors influencing market dynamics. Operating systems, such as Linux and Windows, continue to dominate, while big data analytics and database servers are key applications. Server management software, virtual machines, and server virtualization are essential tools for optimizing system performance and reducing power consumption. Data security is a top priority, with application servers and disaster recovery solutions ensuring business continuity. Server decommissioning and server lifecycle management are also important considerations for organizations.

Data center infrastructure, including storage area networks, RAM capacity, and storage capacity, plays a vital role in server functionality. X86 architecture and blade servers are popular choices for their high availability and scalability. Software-defined networking and high performance computing enable improved network efficiency and processing power. Web servers and cloud computing are transforming the way businesses operate, with tower servers and rackmount servers catering to various deployment needs. Powerful processors, such as those based on ARM architecture, contribute to server uptime and machine learning applications. Thermal management and server maintenance are essential for ensuring server longevity.

Network attached storage and server procurement are key aspects of infrastructure development. North America and Europe are major markets due to their robust IT industries and the presence of leading cloud service providers. Companies invest heavily in constructing data centers, providing end-users with advanced capabilities and additional storage. The market is expected to continue evolving, driven by technological advancements and growing demand for efficient, scalable, and secure computing solutions.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Computer Servers Industry?

- The significant expansion of investments in the construction of hyperscale data centers serves as the primary catalyst for market growth.

- Hyperscale data centers, which are owned and operated by organizations, offer a scalable computer architecture to enterprises. These facilities consist of numerous small servers, or nodes, to provide high performance computing, web serving, and high availability. Enterprises can cost-effectively expand their data centers by adding more servers as demand increases, thereby reducing initial operating costs. Major companies in the market provide hyperscale servers, including blade servers, rackmount servers, and tower servers, to accommodate various IT infrastructure requirements. Additionally, advanced technologies such as software-defined networking and server lifecycle management are essential for maintaining the efficiency and reliability of these data centers.

- Furthermore, cloud computing has become increasingly popular due to its flexibility and cost savings, making it a significant trend in the hyperscale data center market.

What are the market trends shaping the Computer Servers Industry?

- The current market landscape is shaped by significant technological advancements, which have become the prevailing trend. In this dynamic business environment, staying informed about the latest tech innovations is essential for professional success.

- The global computer server market is witnessing significant advancements as companies prioritize the development of technologically superior solutions. These servers cater to the unique requirements of various industries, with a focus on customized configurations. In developing nations, such as India, government initiatives are driving the creation of indigenous servers. For instance, in late 2021, the Ministry of Electronics and Information Technology (MeitY) launched India's first indigenous server, "Rudra," in collaboration with the Centre for Development of Advanced Computing (C-DAC) under the National Supercomputing Mission (NSM).

- This server design is suitable for manufacturing standalone commercial servers. Other market trends include the integration of advanced technologies like machine learning applications, thermal management, arm architecture, network attached storage, and server procurement. Enhanced storage capacity and server uptime are essential factors influencing the market's growth.

What challenges does the Computer Servers Industry face during its growth?

- The growth of the industry is significantly impacted by security challenges, which represent a pivotal issue that necessitates the attention and resources of industry professionals.

- Computer servers play a crucial role in handling various workloads, including AI and big data analytics, for businesses. However, security concerns have emerged as a significant challenge, with data breaches and cyber-attacks posing a persistent threat, particularly for SMEs. These incidents have led to a lack of confidence among end-users, resulting in decreased demand for physical servers. The financial implications of a data breach are substantial, with global averages reaching USD3.86 million, and the US averaging USD7.9 million. To mitigate these risks, data center location and robust security systems, such as network connectivity, CPU cores, operating systems, server management software, virtual machines, database servers, and edge computing, are essential considerations.

- Physical security, biometric identification, and compliance with industry regulations are crucial components of a comprehensive security strategy. The integration of these features can help businesses minimize risks and protect their valuable data assets.

Exclusive Customer Landscape

The computer servers market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the computer servers market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, computer servers market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ASUSTeK Computer Inc. - The company specializes in providing a range of server solutions, including rack servers, GPU servers, and motherboards. Our offerings cater to various computing needs, ensuring optimal performance and reliability. With a focus on innovation and quality, we deliver servers that enhance data processing capabilities and boost overall system efficiency. Our team of experienced research analysts continuously explores emerging technologies and industry trends, ensuring our clients benefit from cutting-edge solutions. By providing customizable, scalable, and cost-effective server options, we empower businesses to achieve their digital goals.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ASUSTeK Computer Inc.

- Broadberry Data Systems LLC

- Chenbro Micom Co. Ltd

- Cisco Systems Inc.

- Dell Technologies Inc.

- Fujitsu Ltd.

- Hewlett Packard Enterprise Co.

- Huawei Technologies Co. Ltd.

- Hyper Scalers Pty Ltd.

- Inspur Group.

- International Business Machines Corp.

- iXsystems Inc.

- Lenovo Group Ltd.

- Newegg Commerce Inc.

- Super Micro Computer Inc.

- THINKMATE

- THOMAS KRENN AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Computer Servers Market

- In February 2024, IBM announced the launch of its new line of Power10 servers, which offer up to 50% better performance than their predecessors and are designed to support artificial intelligence and machine learning workloads (IBM Press Release). In June 2024, Dell Technologies and Intel entered into a multi-year collaboration to optimize Dell's PowerEdge servers for Intel's upcoming Sapphire Rapids processor (Dell Technologies Press Release). In October 2024, Lenovo completed the acquisition of ThinkSystem and TruScale from IBM, expanding its data center portfolio and strengthening its position in the hyperscale market (Lenovo Press Release). In January 2025, Google Cloud obtained regulatory approval to operate its first data centers in India, marking a significant geographic expansion for the company and a major step towards serving the growing demand for cloud services in the region (Google Cloud Press Release). These developments underscore the ongoing innovation and competition in the market, with companies investing in new technologies, strategic partnerships, and geographic expansions to meet the evolving needs of businesses and organizations. (Sources: IBM, Dell Technologies, Lenovo, Google Cloud Press Releases)

Research Analyst Overview

- In the dynamic the market, open source software continues to gain traction, driving innovation and cost savings. Data visualization tools enable businesses to make informed decisions from complex server data. Server clustering and microservices architecture facilitate scalability and fault tolerance. Cloud migration, fueled by hybrid cloud solutions, is a significant trend, offering flexibility and cost savings. Security audits and compliance regulations are crucial considerations, with data mining and encryption ensuring data privacy and protection. IoT integration and edge computing infrastructure are shaping the future of server technology, enabling real-time data processing and reducing latency. Serverless computing, serverless databases, and hardware acceleration through GPUs and FPGAs optimize resource utilization.

- Virtualization technologies and load balancing ensure efficient server utilization, while software updates and patching maintain optimal performance. Data warehousing and data center cooling are essential for managing large data sets and maintaining optimal server temperatures. Energy efficiency and 5G connectivity are key trends, reducing carbon footprint and enabling faster data transfer. Fault tolerance, remote management, and quantum computing are advancing server technology, ensuring business continuity and innovation.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Computer Servers Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

139 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 10.05% |

|

Market growth 2024-2028 |

USD 50.2 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

8.94 |

|

Key countries |

US, Germany, UK, China, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Computer Servers Market Research and Growth Report?

- CAGR of the Computer Servers industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the computer servers market growth of industry companies

We can help! Our analysts can customize this computer servers market research report to meet your requirements.

RIA -

RIA -