Spain Construction Market Size 2026-2030

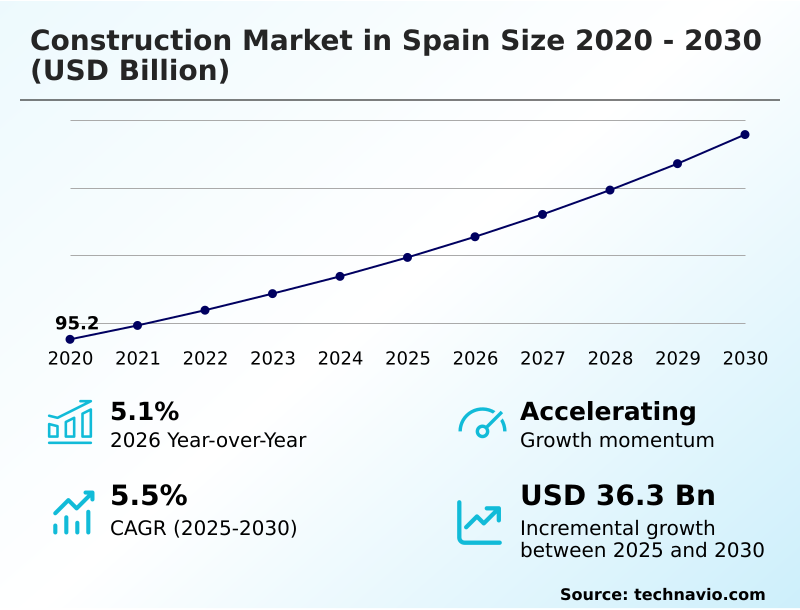

The Spain Construction Market size was valued at USD 119.4 billion in 2025, growing at a CAGR of 5.5% during the forecast period 2026-2030.

Major Market Trends & Insights

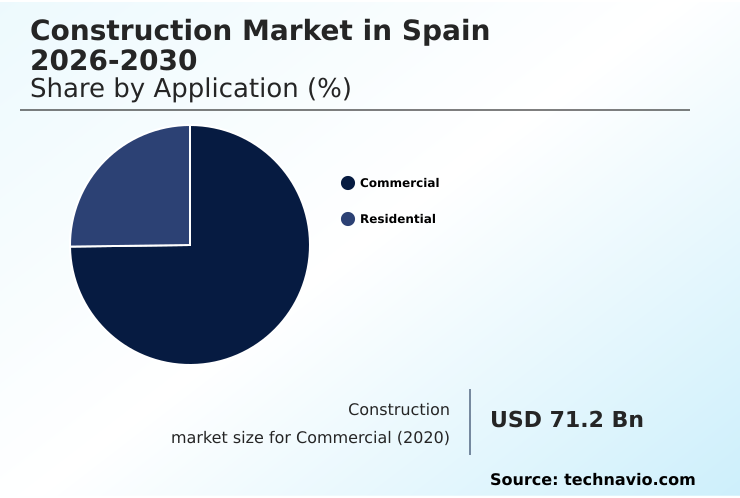

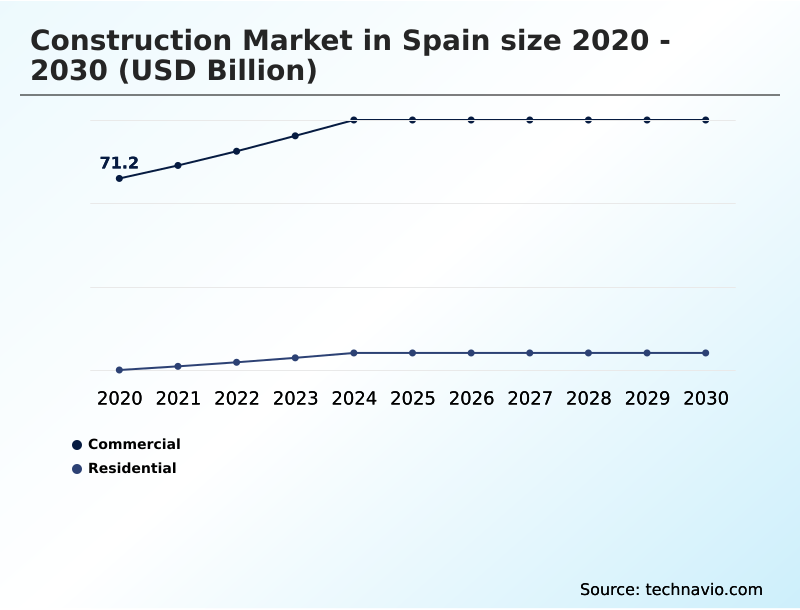

- By Application - Commercial segment was valued at USD 85.6 billion in 2024

- By End-user - Large contractor segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 60.5 billion

- Market Future Opportunities 2025-2030: USD 36.3 billion

- CAGR from 2025 to 2030 : 5.5%

Market Summary

- The construction market in Spain is defined by a dual focus on large-scale infrastructure renewal and a stringent push toward sustainability, with nearly 40% of public project funding now tied to green initiatives. This dynamic creates a complex operational environment where contractors must balance traditional project execution with advanced requirements for energy efficiency.

- For instance, a mid-sized firm undertaking an urban regeneration project must navigate volatile supply chains for certified sustainable construction materials, where prices can fluctuate by over 15% quarterly, while adhering to EU-mandated energy performance standards. A primary driver is the significant injection of capital from the Next Generation EU recovery instrument, which provides a stable pipeline for transport and energy projects.

- Conversely, a major challenge is the structural shortage of skilled labor, particularly for roles requiring digital competencies like building information modeling, which can delay project timelines and inflate labor costs, constraining overall growth potential.

What will be the Size of the Spain Construction Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Spain Construction Market Segmented?

The spain construction industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Commercial

- Residential

- End-user

- Large contractor

- Small contractor

- Type

- Renovation and maintenance

- New projects

- Geography

- Europe

- Spain

- Europe

How is the Spain Construction Market Segmented by Application?

The commercial segment is estimated to witness significant growth during the forecast period.

The commercial construction segment, where projects focused on modernization now outpace new builds by a ratio of nearly 3 to 2, is evolving due to shifting economic demands.

This market is segmented by application, including commercial and residential, and by end-user, such as large and small contractors.

A strategic pivot toward retrofitting older buildings to align with current energy efficiency standards is driving a significant portion of activity, leading to an average 15% reduction in operational costs for compliant properties.

The surge in e-commerce has also reshaped retail construction, prioritizing the development of experiential centers and mixed-use facilities over traditional storefronts. Consequently, developers are reallocating capital, with investment in logistics and warehouse construction growing faster than any other commercial subsegment.

The Commercial segment was valued at USD 85.6 billion in 2024 and showed a gradual increase during the forecast period.

What are the key Drivers, Trends, and Challenges in the Spain Construction Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Understanding the construction market in Spain requires analyzing key strategic questions, with firms reporting a 15% improvement in bid accuracy by leveraging data analytics. The primary impact of digitalization on construction is seen in improved efficiency and reduced rework, though significant construction technology adoption barriers remain for smaller enterprises.

- These companies often lack the capital to invest in platforms that address the complex challenges in construction project management, such as real-time cost tracking and supply chain visibility. Simultaneously, sustainable construction materials trends are reshaping procurement, influencing everything from material selection to project design.

- This is particularly evident in the future of residential construction design, where demand for green certifications and energy-efficient homes is growing. Firms that successfully integrate digital tools with sustainable practices are demonstrating a distinct competitive advantage, completing projects faster and with higher profitability than their peers.

- The market's trajectory will be defined by how effectively the industry navigates the path to full digitalization while meeting sustainability goals, a task made complex by the need to upskill the existing workforce.

What are the key market drivers leading to the rise in the adoption of Spain Construction Industry?

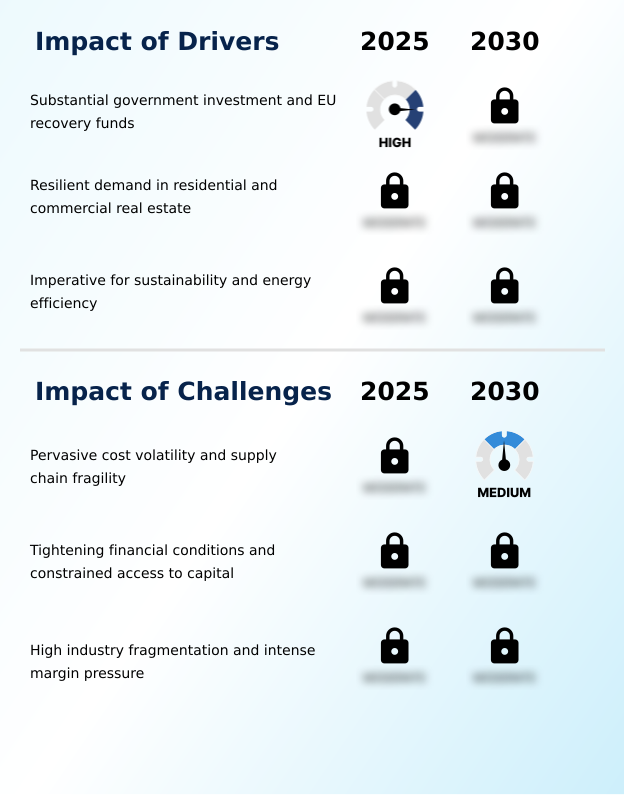

- Substantial government investment, augmented by EU recovery funds, is a key driver propelling growth in the market.

- Substantial government investment, heavily augmented by European Union recovery funds, serves as the primary driver for the construction market in Spain, with over 40% of public infrastructure budgets now allocated from these sources.

- This strategic injection of capital is a direct result of national and EU-level policies aimed at fostering economic recovery and accelerating the green transition.

- The primary effect is the creation of a stable, long-term pipeline of large-scale projects, particularly in sustainable infrastructure and urban regeneration, which de-risks private investment and stimulates ancillary industries.

- Consequently, construction firms are increasingly aligning their capabilities with green building standards to qualify for these publicly funded tenders, fundamentally shaping the sector's growth trajectory toward sustainability and modernization.

What are the market trends shaping the Spain Construction Industry?

- Pervasive digitalization and the accelerating adoption of construction technology represent a significant upcoming market trend. This shift is reshaping project delivery and operational efficiency across the industry.

- The pervasive digitalization of the construction market in Spain is a defining trend, with the mandatory adoption of Building Information Modeling (BIM) for public projects increasing design accuracy by over 20%. This shift toward a data-centric approach is compelling firms to invest in digital twin technology and advanced project management software to remain competitive.

- The primary effect is a notable improvement in operational efficiency and a reduction in costly onsite errors. However, this digital evolution also creates a skills gap, intensifying the demand for professionals proficient in data analytics and digital construction tools.

- As a result, companies that successfully integrate these technologies are gaining a significant competitive advantage, while smaller firms face the challenge of high initial investment costs and the need for workforce upskilling.

What challenges does the Spain Construction Industry face during its growth?

- Pervasive cost volatility and supply chain fragility present a key challenge affecting the industry's growth trajectory.

- Pervasive cost volatility and supply chain fragility represent a formidable challenge for the construction market in Spain, with material costs experiencing fluctuations of up to 30% within a single fiscal year. This instability is primarily caused by global energy price hikes and logistical bottlenecks, which directly impact the production and delivery of essential materials like steel and cement.

- The immediate effect on businesses is severe margin erosion, particularly for contractors operating on fixed-price contracts, with an estimated one in five projects facing significant delays due to material unavailability. This forces a strategic shift toward risk-sharing contract models and the adoption of sophisticated strategic sourcing and inventory management practices to mitigate financial exposure.

Exclusive Technavio Analysis on Customer Landscape

The spain construction market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the spain construction market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Spain Construction Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, spain construction market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Acciona SA - Core offerings center on sustainable infrastructure development, large-scale civil engineering, and specialized construction services for the energy and industrial sectors, reflecting advanced project management capabilities.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Acciona SA

- ACS Group

- ADIF

- AECOM

- Elecnor SA

- FCC SA

- Ferrovial SA

- Fluor Corp.

- Grupo Carso SAB de CV

- Grupo Isolux Corsan

- Obrascon Huarte Lain SA

- Rover Grupo

- Sacyr SA

- Site and Field SL

- Skanska AB

- Tecnicas Reunidas SA

- Tsk Electronica Y Electricidad

- Vinci SA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Construction and Engineering industry, the widespread mandate for Building Information Modeling (BIM) in public sector tenders has catalyzed a significant digital transformation, compelling firms in the construction market in spain 2026-2030 to adopt digital twin technology to improve project coordination and reduce rework by up to 15%.

- Stringent European Union policies, notably the Energy Performance of Buildings Directive (EPBD), are fundamentally reshaping project specifications by requiring nearly zero-energy building standards, which directly fuels demand for green building certification and sustainable construction materials within the market.

- Persistent skilled labor shortages combined with intense margin pressure are accelerating the adoption of industrialized construction methods, with offsite and modular construction techniques enabling project timeline reductions of up to 30% and shifting procurement strategies toward prefabricated components.

- A global strategic shift toward decarbonization has directed substantial investment into renewable energy infrastructure, creating a high-growth niche subsector for the engineering and construction of utility-scale solar farms and wind parks, altering the project portfolios of major contractors.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Spain Construction Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 184 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.5% |

| Market growth 2026-2030 | USD 36.3 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.1% |

| Key countries | Spain |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The construction market in Spain operates within a highly fragmented ecosystem, where over 90% of companies are SMEs, yet large, established contractors capture the majority of high-value public works contracts.

- This structure creates a complex value chain where material suppliers of commodities like steel and cement are subject to global price volatility, directly impacting the margins of contractors who must adhere to stringent EU-level regulatory standards for energy efficiency and sustainable construction materials.

- Financial institutions and government bodies act as key enablers, providing capital and channeling recovery funds that dictate project pipelines, particularly in renewable energy and transport infrastructure. End-users, including public authorities and private developers, are increasingly demanding higher standards of quality and sustainability, pushing the entire ecosystem toward greater innovation and efficiency.

- This dynamic is fostering greater collaboration between stakeholders to manage risk and deliver complex projects effectively.

What are the Key Data Covered in this Spain Construction Market Research and Growth Report?

-

What is the expected growth of the Spain Construction Market between 2026 and 2030?

-

The Spain Construction Market is expected to grow by USD 36.3 billion during 2026-2030, registering a CAGR of 5.5%. Year-over-year growth in 2026 is estimated at 5.1%%. This acceleration is shaped by substantial government investment and eu recovery funds, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Commercial, and Residential), End-user (Large contractor, and Small contractor), Type (Renovation and maintenance, and New projects) and Geography (Europe). Among these, the Commercial segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers Europe. Country-level analysis includes Spain, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is substantial government investment and eu recovery funds, which is accelerating investment and industry demand. The main challenge is pervasive cost volatility and supply chain fragility, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Spain Construction Market?

-

Key vendors include Acciona SA, ACS Group, ADIF, AECOM, Elecnor SA, FCC SA, Ferrovial SA, Fluor Corp., Grupo Carso SAB de CV, Grupo Isolux Corsan, Obrascon Huarte Lain SA, Rover Grupo, Sacyr SA, Site and Field SL, Skanska AB, Tecnicas Reunidas SA, Tsk Electronica Y Electricidad and Vinci SA. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The construction market in Spain is highly competitive, with the top five largest contractors securing over 60% of major public infrastructure tenders, creating a challenging environment for smaller players. In response, leading firms such as ACS Group and Sacyr are diversifying away from traditional civil works and toward high-value, specialized segments.

- These companies are actively pursuing projects in water infrastructure management and renewable energy plant construction, which now account for an estimated 25% of their new contracts. This strategic pivot aligns with national and EU-level sustainability goals, supported by significant public funding.

- However, this shift presents a challenge in sourcing and retaining talent with expertise in green technologies and digital project management, forcing companies to increase investment in workforce training and technology adoption to maintain a competitive edge.

We can help! Our analysts can customize this spain construction market research report to meet your requirements.

RIA -

RIA -