Southeast Asia Data Center Market Size 2026-2030

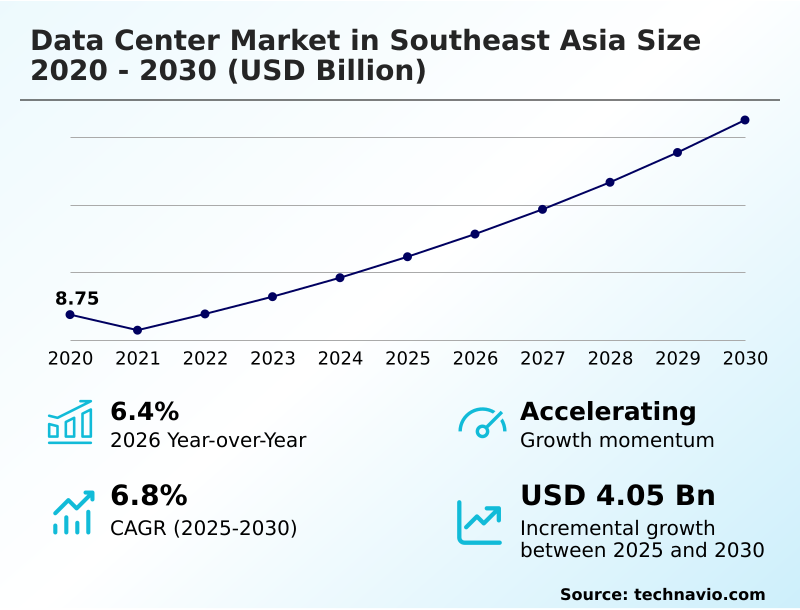

The southeast asia data center market size is valued to increase by USD 4.05 billion, at a CAGR of 6.8% from 2025 to 2030. Escalation of cross border digital integration and regional connectivity hubs will drive the southeast asia data center market.

Major Market Trends & Insights

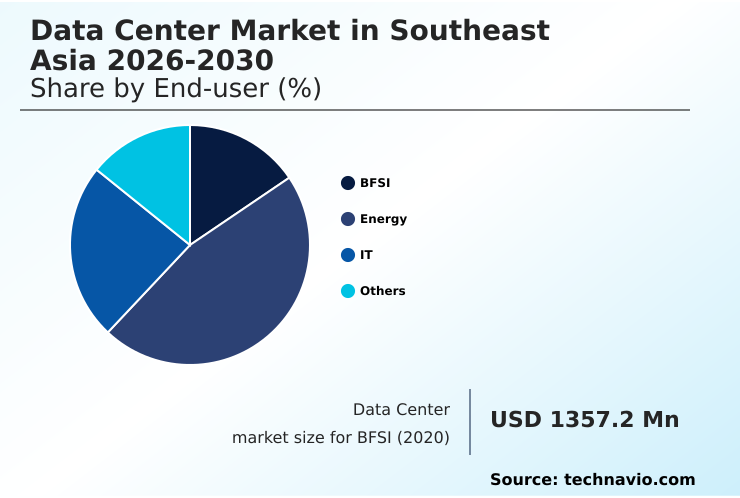

- By End-user - BFSI segment was valued at USD 1.51 billion in 2024

- By Component - IT infrastructure segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 5.76 billion

- Market Future Opportunities: USD 4.05 billion

- CAGR from 2025 to 2030 : 6.8%

Market Summary

- The data center market in Southeast Asia is undergoing a rapid industrialization, driven by the critical need to support the region's burgeoning digital economies. This expansion is fueled by the institutionalization of artificial intelligence workloads and stringent data sovereignty laws, compelling a shift towards high-density computing environments.

- A key trend is the transition to advanced infrastructure capable of supporting significant power and cooling requirements, including the widespread adoption of liquid cooling technologies. However, this growth is met with challenges such as power grid limitations and a shortage of skilled engineering talent.

- As a real-world scenario, a multinational manufacturing firm might establish edge data centers to run its digital twin and industrial IoT platforms. This requires localized, low-latency processing to reduce disruptions on the factory floor, where a mere 5% improvement in predictive maintenance accuracy can prevent millions in losses from unscheduled downtime.

- The market's evolution is defined by this balance between deploying cutting-edge technology and overcoming fundamental resource constraints to build a resilient digital backbone.

What will be the Size of the Southeast Asia Data Center Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Southeast Asia Data Center Market Segmented?

The southeast asia data center industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

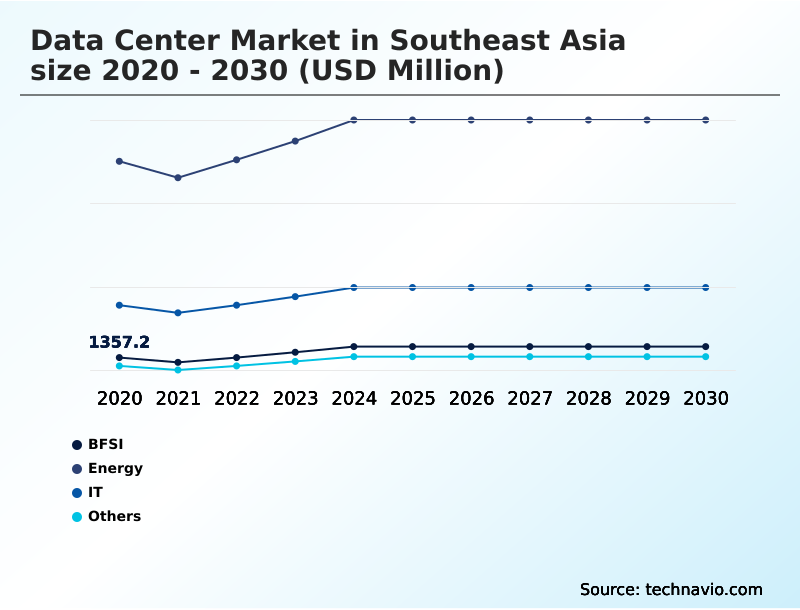

- BFSI

- Energy

- IT

- Others

- Component

- IT infrastructure

- Electrical construction

- Mechanical construction

- General construction

- Security solutions

- Type

- Traditional

- Modular

- Containerized

- Geography

- Southeast Asia

By End-user Insights

The bfsi segment is estimated to witness significant growth during the forecast period.

The banking, financial services, and insurance (BFSI) segment is a primary consumer of data center capacity, driven by the sector's rapid shift to digital-first financial ecosystems.

Financial institutions are migrating core systems to decentralized cloud architectures and specialized colocation services to enhance resilience and meet demand for real-time transactional capabilities.

Stringent data localization mandates necessitate the use of localized IT infrastructure to ensure financial data remains within national borders, demanding robust security solutions and data governance.

This has led to the adoption of zero-trust security frameworks and biometric access controls to protect sensitive information.

Integrating artificial intelligence for fraud detection has boosted computational requirements, with successful implementations reducing fraudulent transaction processing by over 15%, underscoring the need for high-performance, secure digital environments.

The BFSI segment was valued at USD 1.51 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic deployment of digital infrastructure is evolving, driven by the convergence of high-performance computing and sustainability mandates. Decisions around financial modeling for data center investment are now intrinsically linked to long-term power usage effectiveness in tropical climates and the ability to navigate complex cross-border data flow regulations.

- As enterprises adopt ai-ready data center design principles, the focus shifts to deploying liquid cooling for high-density servers and ensuring robust data center infrastructure management tools are in place. This pivot is not just about technology but also about compliance and risk, with data sovereignty and cloud infrastructure becoming a board-level concern.

- The integration of sustainable power sources for data centers is now a critical component of corporate strategy, often verified through a data center environmental impact assessment. Effective data center risk management and compliance, supported by multi-tier data center security protocols and rigorous site selection criteria, are paramount.

- Facilities designed with modern power efficiency strategies can achieve up to a 20% greater efficiency, significantly reducing operational costs. Furthermore, talent development for data center operations is crucial for managing this sophisticated ecosystem, from initial building information modeling for data centers to eventual data center decommissioning and recycling.

What are the key market drivers leading to the rise in the adoption of Southeast Asia Data Center Industry?

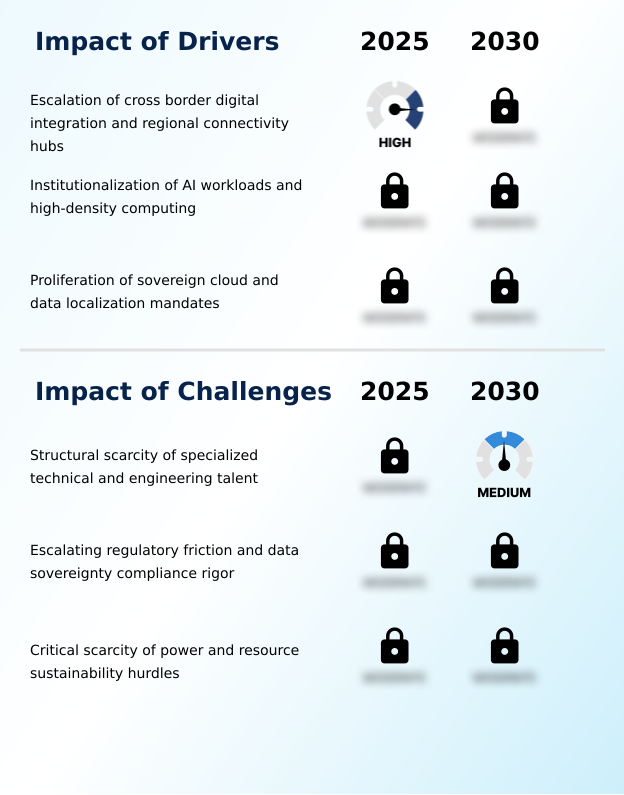

- The escalation of cross-border digital integration and the development of regional connectivity hubs are key drivers for the market.

- The institutionalization of artificial intelligence is the primary driver reshaping infrastructure requirements, mandating a move toward AI-ready infrastructure. The proliferation of graphics processing units (GPUs) for high-performance computing clusters has created unprecedented demand for high-density computing environments.

- Consequently, facilities are being re-engineered to support high-density power configurations, with rack power needs jumping from 12 kilowatts to over 30 kilowatts. This shift necessitates advanced electrical construction and mechanical construction to implement direct-to-chip technologies for cooling.

- The demand for specialized technical talent to manage these complex systems has surged, as organizations recognize that achieving digital transformation goals is directly tied to their ability to deploy and maintain this next-generation hardware.

- This trend is causing a strategic pivot where investment is now prioritized for projects that enhance national AI capabilities.

What are the market trends shaping the Southeast Asia Data Center Industry?

- Advancements in sustainable and sovereign energy integration are an upcoming market trend. This involves a strategic shift toward green power sources and enhanced data residency.

- A primary trend shaping the market is the dual focus on sustainable energy integration and digital sovereignty. To align with aggressive net-zero commitments, operators are increasingly adopting renewable energy certificates and exploring green hydrogen as a power source, which directly influences operational expenditure.

- This push for sustainability is reflected in facility design, where achieving a low power usage effectiveness (PUE) is a key performance metric, with some advanced facilities improving PUE by 15% through innovative cooling. Concurrently, sovereign cloud initiatives are gaining momentum, driven by government mandates for data residency.

- This requires infrastructure that ensures digital sovereignty, compelling operators to navigate complex power purchase agreements and regulations governing environmental performance, thereby creating a new competitive benchmark for green and sovereign-ready data centers.

What challenges does the Southeast Asia Data Center Industry face during its growth?

- A structural scarcity of specialized technical and engineering talent presents a key challenge to industry growth.

- A critical challenge is the structural scarcity of power and the associated resource sustainability hurdles, creating significant bottlenecks for new projects. The time required to secure grid connectivity can now exceed four years in prime locations, severely impacting data center commissioning timelines.

- This is compounded by the operational strain of ensuring business continuity with increasingly unreliable power grids, elevating the importance of robust uninterruptible power supply systems and backup power and ups systems. The high ambient heat necessitates energy-intensive thermal management solutions, which strains both power and water resources.

- Furthermore, ensuring fault-tolerant architectures that can withstand both physical and cyber threats, such as supply chain attacks, adds another layer of complexity. These infrastructure-level challenges mean that even with advanced technologies like hyper-converged infrastructure, the physical limitations of general construction and resource availability can impede growth.

Exclusive Technavio Analysis on Customer Landscape

The southeast asia data center market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the southeast asia data center market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Southeast Asia Data Center Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, southeast asia data center market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - Providers deliver scalable colocation, hyperscale infrastructure, and interconnection services, focusing on power and cooling efficiency for high-density computing environments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Bridge Data Centres

- Caterpillar Inc.

- Cisco Systems Inc.

- Dell Technologies Inc.

- Delta Electronics Inc.

- Digital Realty Trust Inc.

- EdgeConneX Inc.

- Equinix Inc.

- GDS Holdings Ltd.

- Global Switch Ltd.

- Iron Mountain Inc.

- NTT DATA Corp.

- Princeton Digital Group

- Schneider Electric SE

- Singapore Telecom Ltd.

- SpaceDC

- STT GDC Pte Ltd.

- True Internet Data Center Co.

- Vantage Data Centers Management

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Southeast asia data center market

- In May, 2025, Equinix Inc. integrated advanced sustainability features, including high-efficiency power arrays, into its JK1 facility in Jakarta to align with regional green energy mandates.

- In April, 2025, Mobile-health Network Solutions, in partnership with specialized infrastructure investors, initiated the development of a sixty-megawatt artificial intelligence data center campus in Sarawak, Malaysia, designed to host hyperscale workloads.

- In March, 2025, Vantage Data Centers Management partnered with the Malaysia Forest Fund to advance sustainability initiatives and pursue carbon-neutral goals within its hyperscale data center campuses in the region.

- In January, 2025, Digital Realty Trust Inc. expanded its presence by executing an agreement to acquire CSF Advisers, which includes a data center in Cyberjaya, Malaysia, capable of supporting an additional fourteen megawatts of IT load.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Southeast Asia Data Center Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 227 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.8% |

| Market growth 2026-2030 | USD 4049.0 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.4% |

| Key countries | Singapore, Indonesia, Malaysia, Thailand and Rest of Southeast Asia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The data center market in southeast asia is defined by a strategic industrialization toward supporting high-density computing and artificial intelligence workloads. This transition requires significant capital investment in not just physical space but specialized technologies, making it a key boardroom-level decision. The market is shifting from traditional colocation services to integrated platforms offering hyper-converged infrastructure, software-defined networking, and carrier-neutral connectivity.

- This evolution is driven by the need to support graphics processing units and high-performance computing clusters, which in turn necessitates advanced thermal management solutions like direct-to-chip technologies. Modern facilities are now being engineered for rack densities exceeding 30 kilowatts, a nearly threefold increase from legacy standards, compelling the use of liquid cooling technologies.

- This entire ecosystem is underpinned by robust subsea cable systems, terrestrial fiber networks, and stringent data localization mandates, which drive the adoption of sovereign cloud initiatives and advanced data governance. As a result, the focus is on creating resilient, high-performance environments that can guarantee business continuity.

What are the Key Data Covered in this Southeast Asia Data Center Market Research and Growth Report?

-

What is the expected growth of the Southeast Asia Data Center Market between 2026 and 2030?

-

USD 4.05 billion, at a CAGR of 6.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (BFSI, Energy, IT, and Others), Component (IT infrastructure, Electrical construction, Mechanical construction, General construction, and Security solutions), Type (Traditional, Modular, and Containerized) and Geography (Southeast Asia)

-

-

Which regions are analyzed in the report?

-

Southeast Asia

-

-

What are the key growth drivers and market challenges?

-

Escalation of cross border digital integration and regional connectivity hubs, Structural scarcity of specialized technical and engineering talent

-

-

Who are the major players in the Southeast Asia Data Center Market?

-

ABB Ltd., Bridge Data Centres, Caterpillar Inc., Cisco Systems Inc., Dell Technologies Inc., Delta Electronics Inc., Digital Realty Trust Inc., EdgeConneX Inc., Equinix Inc., GDS Holdings Ltd., Global Switch Ltd., Iron Mountain Inc., NTT DATA Corp., Princeton Digital Group, Schneider Electric SE, Singapore Telecom Ltd., SpaceDC, STT GDC Pte Ltd., True Internet Data Center Co. and Vantage Data Centers Management

-

Market Research Insights

- The market's dynamics are shaped by a strategic pivot toward AI-ready infrastructure, compelling new standards in facility design and engineering. As enterprises pursue digital transformation goals, demand has intensified for high-density power configurations to support advanced workloads, with some facilities seeing a threefold increase in rack power requirements.

- This shift necessitates robust backup power and UPS systems to ensure mission-critical operations remain uninterrupted. Concurrently, multi-market expansion strategies are being adopted to navigate resource constraints and improve regional connectivity hubs. This sophisticated environment requires specialized technical talent to manage complex systems, where optimized power purchase agreements can reduce operational expenditure by more than 10%.

- Ultimately, success hinges on balancing capital expenditure with scalable, resilient, and compliant infrastructure.

We can help! Our analysts can customize this southeast asia data center market research report to meet your requirements.

RIA -

RIA -