Software As A Service (saas) Market Size 2026-2030

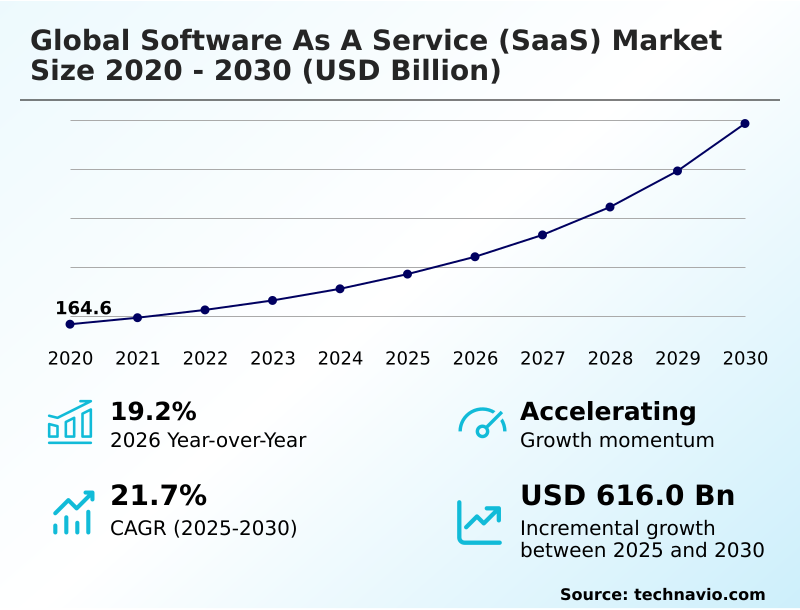

The software as a service (saas) market size is valued to increase by USD 616 billion, at a CAGR of 21.7% from 2025 to 2030. Integration of generative AI associated with SaaS will drive the software as a service (saas) market.

Major Market Trends & Insights

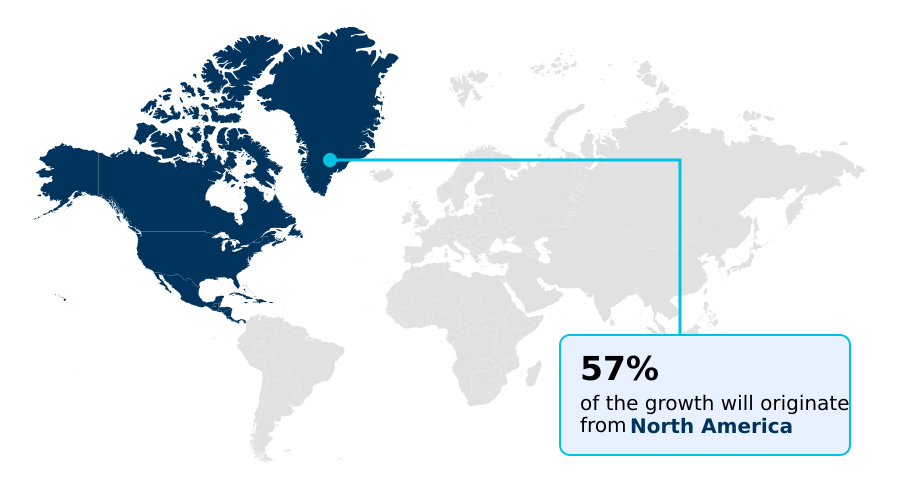

- North America dominated the market and accounted for a 56.9% growth during the forecast period.

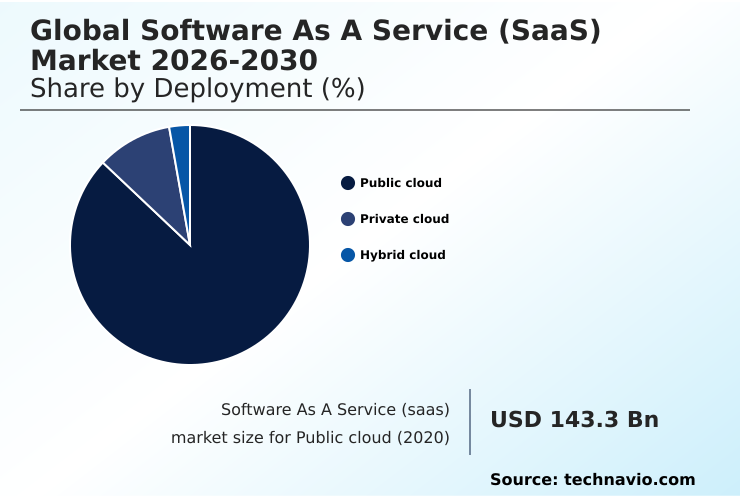

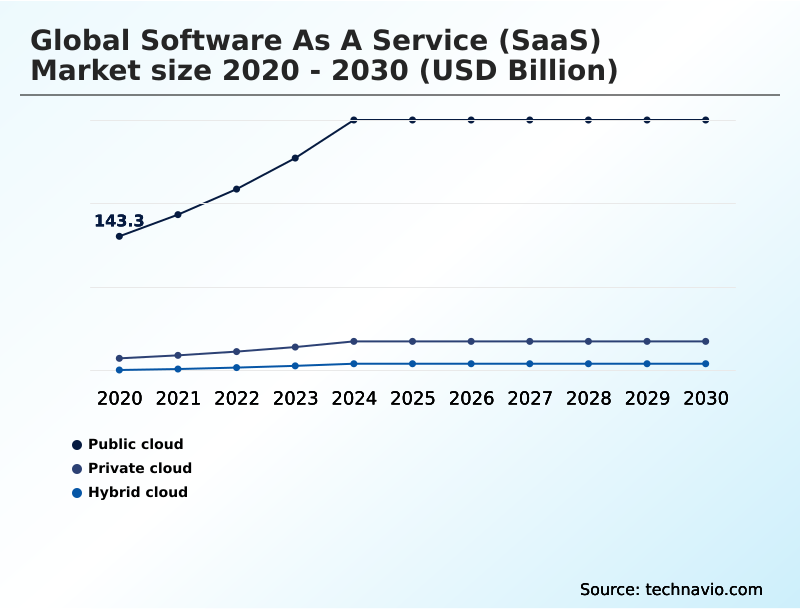

- By Deployment - Public cloud segment was valued at USD 264 billion in 2024

- By End-user - Large enterprises segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 821 billion

- Market Future Opportunities: USD 616 billion

- CAGR from 2025 to 2030 : 21.7%

Market Summary

- The software as a service (SaaS) market is undergoing a significant transformation, driven by the need for digital agility and operational efficiency. Organizations are increasingly shifting from on-premises systems to cloud-based solutions to achieve greater scalability, remote accessibility, and cost-effectiveness.

- This evolution is particularly evident in how businesses manage core functions, with a strong demand for tools that provide actionable insights rather than just data storage. For instance, in supply chain management, companies are leveraging SaaS platforms to gain real-time visibility into logistics, which improves inventory turnover by up to 20% and reduces shipment delays.

- The market is also characterized by a move toward vertical-specific solutions tailored to the unique regulatory and operational needs of industries like finance and healthcare. The integration of advanced technologies such as artificial intelligence and machine learning is central to this shift, enabling automated workflows and predictive analytics.

- As businesses continue to prioritize data-driven decision-making, the ability of SaaS to provide sophisticated yet accessible tools will remain a critical factor in its sustained adoption and impact on enterprise operations.

What will be the Size of the Software As A Service (saas) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Software As A Service (saas) Market Segmented?

The software as a service (saas) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Deployment

- Public cloud

- Private cloud

- Hybrid cloud

- End-user

- Large enterprises

- SMEs

- Component

- Software

- Services

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- India

- Japan

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Deployment Insights

The public cloud segment is estimated to witness significant growth during the forecast period.

The public cloud segment facilitates unparalleled scalability and operational efficiency, allowing organizations to deploy applications without significant upfront capital investment in information technology infrastructure.

This model leverages multi-tenant architecture to deliver software, with providers managing all underlying hardware and maintenance, ensuring users always have access to the latest features.

The adoption of public cloud solutions, including business process management tools, improves application development agility by over 30%. This deployment strategy is central to modernizing enterprise-grade workflows and supporting real-time interoperability.

The use of cloud-native applications and intelligent agents within these environments enables advanced data and content management. Organizations utilize enterprise applications and financial applications on these platforms, benefiting from robust disaster recovery strategies and comprehensive data protection measures.

The focus remains on enhancing user experience through highly available and resilient services.

The Public cloud segment was valued at USD 264 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 56.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Software As A Service (saas) Market Demand is Rising in North America Get Free Sample

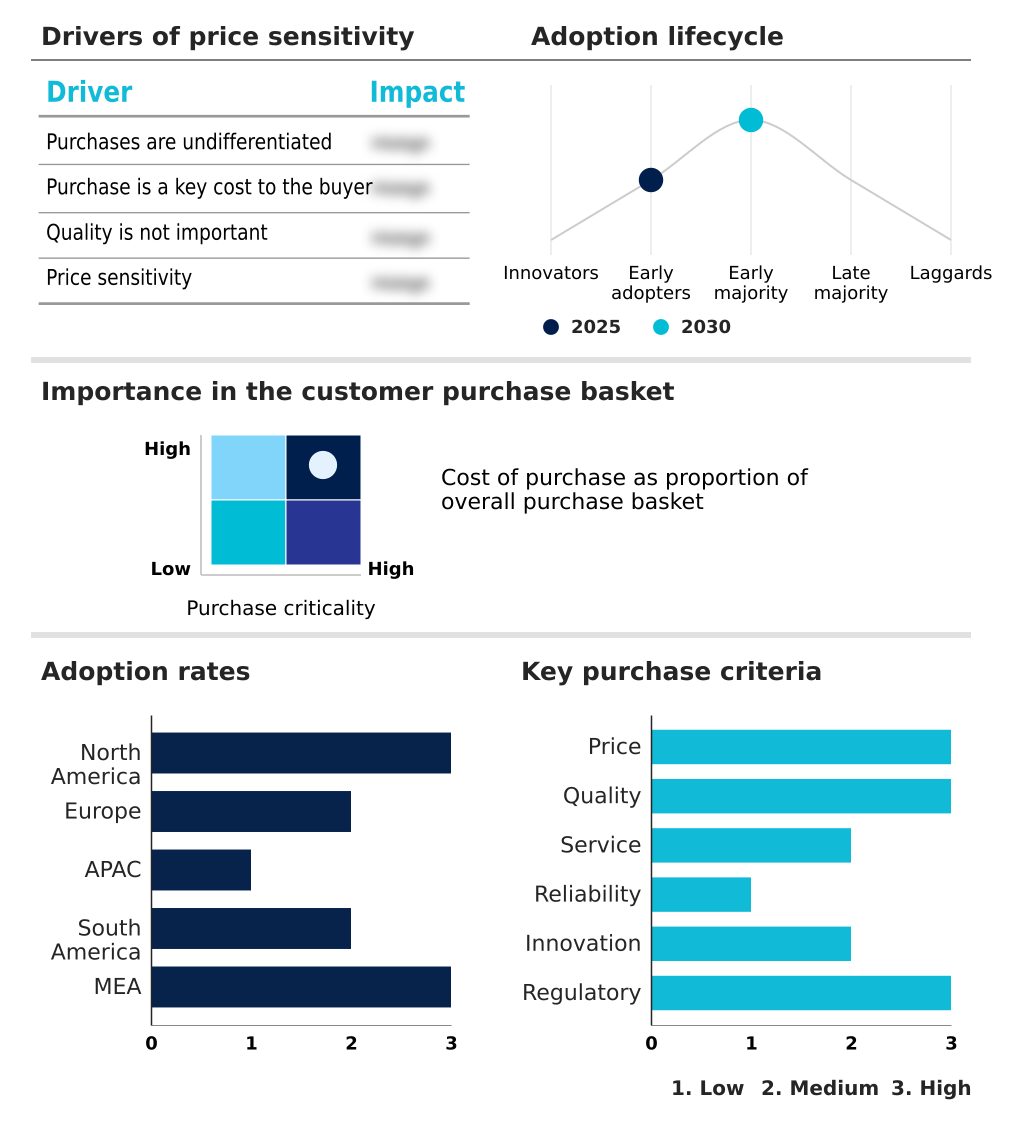

The geographic landscape of the software as a service (SaaS) market is characterized by varied adoption rates and strategic priorities across regions.

North America leads in market maturity, with a high concentration of enterprises leveraging big data platforms for advanced analytics. This region shows a 40% higher adoption rate of AI-driven observability solutions compared to others.

In contrast, the APAC region is the fastest-growing market, driven by mobile-first strategies and the digitalization of SMEs. Europe focuses on data sovereignty and compliance, with a strong demand for private cloud deployment to meet regulatory requirements.

The use of robotic process automation and unified communications platforms is expanding globally.

The development of high-performance engineering software as a service is gaining traction in industrial economies, while emerging markets prioritize cost-effective communication and collaboration applications and cloud accounting platforms to fuel business growth.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of the software as a service (SaaS) market is increasingly defined by its ability to address complex, specific enterprise needs. Successfully executing SaaS integration with legacy systems remains a critical hurdle, often determining the overall ROI of SaaS adoption. Organizations now prioritize security in multi-tenant SaaS applications, recognizing that a single breach can have cascading effects.

- The shift toward vertical SaaS for the manufacturing sector highlights the demand for industry-specific functionalities that generic platforms cannot offer. Concurrently, the rise of low-code development for business users is democratizing innovation, allowing non-technical staff to create automated workflows in SaaS platforms.

- The integration of generative AI in CRM software is transforming customer engagement, while the use of a SaaS platform for digital twins is revolutionizing product design. This has led to a 15% reduction in prototyping costs for early adopters.

- Strategic decisions now revolve around SaaS pricing models for enterprises and the development of API strategies for SaaS ecosystems to foster interoperability. Furthermore, managing data sovereignty in SaaS is a non-negotiable aspect of modern IT governance, alongside ensuring SaaS compliance with data regulations. Firms are also exploring hybrid cloud for SaaS deployment and optimizing SaaS for mobile-first experiences.

- The focus on credential management in SaaS environments and achieving SaaS for supply chain visibility addresses critical operational risks. Ultimately, success depends on a combination of robust technology—such as SaaS solutions for high-performance engineering and SaaS for enterprise IoT management—and a strong focus on user experience design in SaaS, supported by effective SaaS implementation and migration services.

What are the key market drivers leading to the rise in the adoption of Software As A Service (saas) Industry?

- The integration of generative AI within SaaS platforms is a primary market driver, transforming application functionality and enhancing user productivity through intelligent automation.

- The primary driver propelling the software as a service (SaaS) market is the integration of generative artificial intelligence, which automates complex tasks and enhances productivity. Companies leveraging AI-powered tools report a 30% increase in workflow efficiency.

- This technological shift is complemented by the surge in vertical software as a service adoption, providing industry-specific functionalities that generic platforms lack.

- The expansion of low-code platforms is also crucial, empowering non-technical users to build and deploy applications, thereby accelerating digital transformation initiatives by up to 40%. The citizen developer model is becoming mainstream, supported by virtual teammates and composable enterprise architectures.

- These drivers collectively enable organizations to innovate faster, improve customer service performance, and respond more effectively to market changes, utilizing tools such as enterprise IoT platforms.

What are the market trends shaping the Software As A Service (saas) Industry?

- The adoption of hybrid monetization models that combine recurring subscription fees with usage-based components represents a key market trend, aligning software costs with business value.

- Key trends in the software as a service (SaaS) market are reshaping how organizations approach technology investment and monetization. The adoption of hybrid monetization models is accelerating, allowing businesses to align software costs with actual usage, which can reduce shelf-ware by up to 25%. This trend is driven by the rise of resource-intensive generative artificial intelligence features.

- Another significant trend is the convergence of operational tools with analytical platforms through a unified data lakehouse architecture, which improves real-time data access and eliminates information silos. The expansion of vertical software as a service for industries like manufacturing and finance delivers tailored, compliant solutions.

- The use of financial management software and tax preparation software from the cloud is now standard. This evolution towards flexible, integrated, and specialized platforms, including e-commerce merchant solutions, enables greater business agility.

What challenges does the Software As A Service (saas) Industry face during its growth?

- Growing exposure to credential-based cyberattacks presents a significant market challenge, increasing security risks for enterprises that rely heavily on SaaS environments for critical operations.

- The software as a service (SaaS) market faces significant challenges, primarily centered on security and operational resilience. The growing exposure to credential-based cyberattacks remains a top concern, with incidents of unauthorized access rising by over 20% in the last year. This necessitates stronger identity management and the adoption of zero-trust frameworks.

- Another challenge is the risk of systemic failure due to dependency on a few major cloud providers, as a single outage can disrupt global operations. The fragility of the digital supply chain was highlighted by recent events that impacted millions of endpoints.

- Furthermore, economic uncertainty is forcing organizations to scrutinize software spending, leading to portfolio consolidation and pressure on vendors to demonstrate immediate value. The rapid evolution of artificial intelligence platforms also creates technological disruption, challenging incumbents to adapt or risk obsolescence.

Exclusive Technavio Analysis on Customer Landscape

The software as a service (saas) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the software as a service (saas) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Software As A Service (saas) Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, software as a service (saas) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accenture Plc - Delivers software as a service (SaaS) solutions that support digital transformation by enabling the deployment of cloud native business applications for enhanced enterprise integration.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture Plc

- Adobe Inc.

- Amazon.com Inc.

- BetterCloud Inc.

- Box Inc.

- Cisco Systems Inc.

- Convedo Ltd.

- Fujitsu Ltd.

- Google LLC

- Hewlett Packard Entp Co.

- IBM Corp.

- Infosys Ltd.

- Intuit Inc.

- Microsoft Corp.

- Oracle Corp.

- Salesforce Inc.

- SAP SE

- ServiceNow Inc.

- Shopify Inc.

- Zendesk Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Software as a service (saas) market

- In September 2024, Salesforce entered into a definitive agreement to acquire Own Company, a leading provider of data protection and management solutions to bolster its platform with robust backup and recovery capabilities.

- In October 2024, Siemens entered into an agreement to acquire Altair Engineering to strengthen its position in industrial software and accelerate the integration of simulation and data analytics within its digital business platform.

- In November 2024, Guidewire Software introduced Claims Intel, a predictive intelligence solution designed to streamline claims management and improve risk selection for property and casualty insurers.

- In May 2025, HubSpot unveiled significant updates to Breeze, an integrated AI engine that facilitates lead enrichment and content creation across the entire customer journey.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Software As A Service (saas) Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 302 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 21.7% |

| Market growth 2026-2030 | USD 616.0 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 19.2% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Australia, Singapore, Brazil, Argentina, Chile, Saudi Arabia, UAE, Egypt, South Africa and Qatar |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The software as a service (SaaS) market is advancing beyond basic cloud delivery toward a more integrated and intelligent ecosystem. A key strategic shift involves the convergence of operational tools and data analytics, enabled by the adoption of a unified data lakehouse architecture.

- This approach, which improves data processing efficiency by over 35%, is critical for powering generative artificial intelligence and other intelligent agents within core business applications. Enterprises are increasingly adopting a hybrid cloud architecture and private cloud deployment models to balance security, cost, and performance, addressing concerns around data sovereignty.

- The market is also seeing a rise in hybrid monetization models, where pricing is tied to consumption, reflecting the variable costs of AI-driven features. Boardroom decisions are now heavily influenced by the need to secure the digital supply chain against credential-based cyberattacks and to implement robust disaster recovery strategies.

- The emphasis on user experience and real-time interoperability through open data standards is compelling organizations to rethink their IT infrastructure and embrace more flexible, cloud-native capabilities.

What are the Key Data Covered in this Software As A Service (saas) Market Research and Growth Report?

-

What is the expected growth of the Software As A Service (saas) Market between 2026 and 2030?

-

USD 616 billion, at a CAGR of 21.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Public cloud, Private cloud, and Hybrid cloud), End-user (Large enterprises, and SMEs), Component (Software, and Services) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Integration of generative AI associated with SaaS, Growing exposure to credential-based cyberattacks

-

-

Who are the major players in the Software As A Service (saas) Market?

-

Accenture Plc, Adobe Inc., Amazon.com Inc., BetterCloud Inc., Box Inc., Cisco Systems Inc., Convedo Ltd., Fujitsu Ltd., Google LLC, Hewlett Packard Entp Co., IBM Corp., Infosys Ltd., Intuit Inc., Microsoft Corp., Oracle Corp., Salesforce Inc., SAP SE, ServiceNow Inc., Shopify Inc. and Zendesk Inc.

-

Market Research Insights

- The software as a service (SaaS) market is shaped by dynamic forces that prioritize digital agility and cost optimization. The integration of artificial intelligence platforms into enterprise resource planning applications is a key factor, with some businesses reporting a 25% improvement in forecast accuracy. This shift toward intelligent automation allows organizations to streamline operations and reallocate resources to strategic initiatives.

- The adoption of specialized talent orchestration solutions improves internal mobility by over 30%, addressing skill gaps more efficiently. Meanwhile, the use of predictive intelligence solutions in niche sectors enhances risk assessment and operational decision-making.

- As the market evolves, the focus on unified digital adoption capabilities and robust infrastructure automation offerings becomes critical for maintaining a competitive edge and ensuring seamless integration across diverse software ecosystems.

We can help! Our analysts can customize this software as a service (saas) market research report to meet your requirements.

RIA -

RIA -