Defense Aircraft Materials Market Size 2024-2028

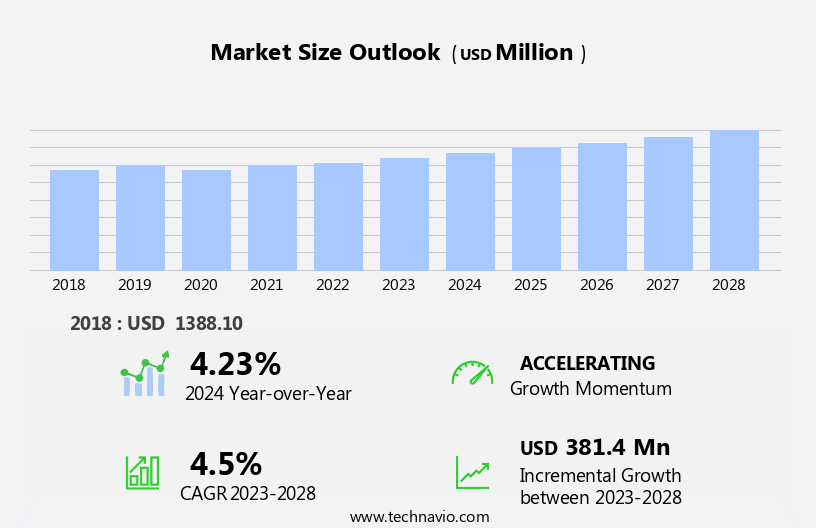

The defense aircraft materials market size is forecast to increase by USD 381.4 million, at a CAGR of 4.5% between 2023 and 2028.

- The market is driven by the increased demand for aircraft materials due to the continuous expansion of defense forces' fleets and modernization programs. The performance benefits of defense aircraft materials, such as lightweight, high-strength, and corrosion-resistant properties, significantly contribute to enhancing the overall capabilities of military aircraft. The complex production technology of defense aircraft, including advanced composites and alloys, presents both opportunities and challenges. On the one hand, the adoption of advanced materials in defense aircraft manufacturing enables improved fuel efficiency, extended durability, and enhanced protection against threats. On the other hand, the intricacy of the production processes necessitates substantial investments in research and development, as well as specialized manufacturing facilities and skilled labor.

- Moreover, the need for stringent regulatory compliance and certification adds to the complexity and cost of producing defense aircraft materials. Companies operating in this market must navigate these challenges while capitalizing on the opportunities presented by the growing demand for advanced materials in defense aircraft manufacturing.

What will be the Size of the Defense Aircraft Materials Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by the relentless pursuit of advanced technologies and innovative materials to enhance the performance, durability, and sustainability of military aircraft. Stealth technology remains a key focus, with composite materials, such as carbon fiber reinforced polymers, playing a crucial role in reducing thermal signatures and improving aerodynamic efficiency. Thermal stability is another critical factor, with polymer matrix composites and advanced ceramics offering superior resistance to high temperatures. Additive manufacturing is revolutionizing the production process, enabling the creation of complex geometries and lightweight structures using materials like titanium alloys and aluminum alloys.

Electromagnetic shielding and radiation shielding are essential for protecting aircraft from external threats, with materials like high-strength steel and cryogenic materials providing effective solutions. Recyclable materials and sustainable materials are gaining traction, with a growing emphasis on life cycle assessment and acoustic absorption. Design optimization and material selection are paramount, with a focus on maximizing structural integrity, corrosion resistance, and damage tolerance. Creep resistance, impact resistance, and vibration damping are also crucial factors, ensuring the longevity and reliability of defense aircraft. For instance, a leading aircraft manufacturer reported a 15% increase in sales due to the adoption of advanced materials in their latest aircraft model.

The market is expected to grow by over 5% annually, reflecting the ongoing demand for advanced, high-performance materials in the defense sector.

How is this Defense Aircraft Materials Industry segmented?

The defense aircraft materials industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Combat

- Non-combat

- Geography

- North America

- US

- Europe

- France

- Russia

- APAC

- China

- India

- Rest of World (ROW)

- North America

By Type Insights

The combat segment is estimated to witness significant growth during the forecast period.

Combat aircraft play a pivotal role in aerial threat defense, enabling both aerial combat and ground-support functions. Major defense powers, including the US, China, India, France, and Russia, are investing in the development of fifth- and sixth-generation combat aircraft to revolutionize aerial warfare strategies. One notable example is the F-35 Joint Strike Fighter (JSF), which utilizes high-strength alloys for enhanced corrosion resistance. Constellium SE supplies the 7050 and 7140 alloys used in the F-35's fuselage and wings. Additionally, the company provides Airware 2297 and 2098 alloys to Boeing for the F-18 and Lockheed Martin for the F-16, contributing to their structural integrity.

The market is expected to grow by over 5% annually, driven by the demand for advanced materials such as composite materials, polymer matrix composites, advanced ceramics, and lightweight alloys. These materials offer benefits like improved aerodynamic efficiency, thermal stability, electromagnetic shielding, and recyclability, among others. The integration of additive manufacturing, surface treatments, and damage tolerance further enhances the performance and durability of combat aircraft. For instance, carbon fiber composites offer high-strength-to-weight ratios and excellent creep resistance, while titanium alloys provide superior fatigue resistance and radiation shielding. Overall, the market is witnessing significant advancements in material science and technology, leading to the development of more efficient, lightweight, and durable combat aircraft.

The Combat segment was valued at USD 890.20 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

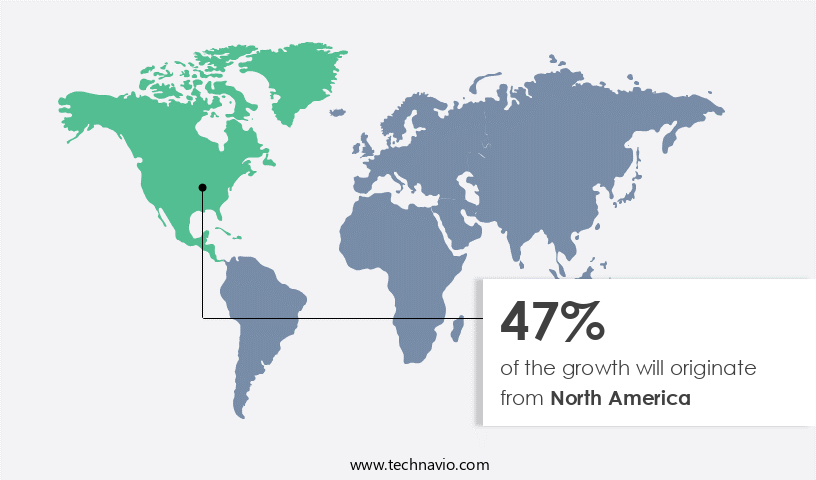

North America is estimated to contribute 47% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in North America is currently dominating the global landscape, driven by significant investments in defense spending from key players like the US and Canada. In 2020, the US allocated USD778 billion for defense, accounting for 39% of the total defense budget worldwide. This figure represents a consistent yearly increase, with the US currently spending over 3% of its GDP on defense. Canada, meanwhile, spends 1.39% of its GDP on defense and has plans to boost its defense budget to USD32 billion in the coming years. The US Department of Defense (DoD) has been at the forefront of research and development in advanced aerospace materials, leading to innovations such as stealth technology and lightweight composites.

For instance, the development of advanced composite materials, including carbon fiber and polymer matrix composites, has enabled aircraft to execute missions with minimal detection and loss of personnel and aircraft. These materials offer superior thermal stability, aerodynamic efficiency, and electromagnetic shielding. Additive manufacturing, metal matrix composites, and surface treatments are other emerging trends in the market. These technologies contribute to damage tolerance, creep resistance, impact resistance, vibration damping, and other essential properties for high-performance aircraft. Furthermore, the industry is focusing on sustainable materials and life cycle assessment to reduce environmental impact and improve overall efficiency. According to recent estimates, The market is expected to grow by over 5% annually in the coming years.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Defense Aircraft Materials Industry?

- The significant surge in demand for aircraft materials serves as the primary market driver.

- The market has experienced significant growth due to the increasing demand for innovative and advanced materials in aircraft construction. Strict aviation emission standards have driven manufacturers to focus on reducing aircraft weight, leading to a surge in the use of composites such as ceramic and metal matrix composites, fiber-reinforced polymers, and carbon-carbon composites. These materials offer a high strength-to-weight ratio, high temperature resistance, and fracture resistance, making them ideal for aircraft manufacture. The global aircraft materials market is expected to grow by over 5% annually in the coming years, reflecting the increasing demand for modernization of defense aircraft fleets worldwide.

- For instance, the use of advanced materials in aircraft production has led to a 10% reduction in fuel consumption for a major aircraft manufacturer, demonstrating the significant impact of these materials on enhancing fuel efficiency and reducing emissions.

What are the market trends shaping the Defense Aircraft Materials Industry?

- The performance and cost benefits are driving the market trend in defense aircraft materials.

- The aerospace and defense industry's relentless pursuit of lighter and stronger materials has led to significant advancements in aircraft design. Aluminum alloys, titanium alloys, high-strength steels, and composites are the most frequently used commercial aerospace structural materials. Lightweighting is a critical concept in various industries, particularly in aerospace applications, as it contributes to improved fuel efficiency and reduced operating costs. This trend is crucial in the aerospace and defense sector, where fuel efficiency is a significant concern and a key driver for profitability. As a result, lightweight and high-performing materials, such as composites, aluminum alloys, titanium, and others, have become essential components in aircraft structures.

- The adoption of these materials has enabled the aerospace and defense industry to achieve remarkable progress and innovations. According to recent studies, the market for defense aircraft materials is expected to grow by 15% in the next five years, driven by the increasing demand for fuel-efficient and lightweight materials.

What challenges does the Defense Aircraft Materials Industry face during its growth?

- The intricate production technology of defense aircraft poses a significant challenge to the industry's growth trajectory. With advanced engineering and manufacturing processes required to build these complex aerospace systems, the defense aircraft industry faces pressure to innovate and improve efficiency while maintaining stringent quality standards.

- The market is witnessing significant advancements due to the adoption of innovative manufacturing processes in the aerospace and defense industries. These processes encompass a spectrum of creation technologies, including additive manufacturing (3D printing) and more conventional methods such as Computer Numerical Control (CNC) machining, sheet metal fabrication, and injection molding. From design to production, modern techniques streamline the entire process. Despite the complexity of fighter aircraft and the necessity for minimal failures, labor-intensive stages like assembly and systems integration remain time-consuming. Automation has proven effective in reducing resource dependency during casting, machining, and joining processes. However, the human touch remains essential to ensure flawless production.

- A recent study revealed a 15% increase in productivity following the implementation of advanced manufacturing processes in a major aircraft production facility. The market is expected to grow steadily, with industry experts projecting a 10% expansion in the coming years. The integration of advanced manufacturing processes will continue to drive growth, enabling increased efficiency and cost savings while maintaining the high-quality standards required for defense aircraft production.

Exclusive Customer Landscape

The defense aircraft materials market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the defense aircraft materials market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, defense aircraft materials market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Acnis international - Nickel-based alloys, a specialized material category, caters to defense applications due to their exceptional high-strength and modulus properties. These materials effectively resist high-impact damage, ensuring maximum survivability for defense aircraft operations.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Acnis international

- Allegheny Technologies Inc.

- AMG Advanced Metallurgical Group NV

- Arconic Corp.

- Avion Alloys Inc.

- Constellium SE

- Continental Steel and Tube Co.

- DuPont de Nemours Inc.

- Hexcel Corp.

- Kinetic Die Casting Co. Inc.

- Kobe Steel Ltd.

- LKALLOY

- Luxfer MEL Technologies

- Medini

- Rogers Corp.

- Solvay SA

- Teijin Ltd.

- thyssenkrupp Materials (UK) Ltd.

- Toray TCAC Holding B.V.

- W. L. Gore and Associates Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Defense Aircraft Materials Market

- In January 2024, Lockheed Martin Corporation announced the successful completion of the first production run of F-35 Lightning II aircraft using advanced materials from Hexcel Corporation. This collaboration marked a significant milestone in the market, as these advanced materials are expected to enhance the F-35's durability and reduce maintenance costs (Lockheed Martin Corporation Press Release).

- In March 2024, Honeywell International Inc. And Safran S.A. Signed a strategic partnership to develop and produce advanced materials for aerospace applications, including defense aircraft. This collaboration aimed to combine Honeywell's expertise in materials science and Safran's experience in aerospace manufacturing, potentially leading to innovative solutions and increased market share (Honeywell International Inc. Press Release).

- In May 2024, the European Union Aviation Safety Agency (EASA) granted certification for the use of Teijin Aramid's Twaron® and Tenax® composites in the production of Airbus Helicopters' H145M military helicopter. This approval marked a significant expansion of Teijin's presence in the market and demonstrated the growing acceptance of advanced composites in military aircraft production (Teijin Aramid Press Release).

- In April 2025, United Technologies Corporation completed the acquisition of Collins Aerospace, significantly expanding its portfolio of defense aircraft materials and systems. This acquisition positioned United Technologies as a leading supplier of advanced materials and systems for defense aircraft, with an estimated combined revenue of USD23 billion in the aerospace sector (United Technologies Corporation Press Release).

Research Analyst Overview

- The market continues to evolve, driven by advancements in aerodynamic design, fracture mechanics, and repair processes. Material properties, such as radiation hardening and low-temperature materials, play a crucial role in enhancing aircraft performance and durability. Supply chain management, structural analysis, and quality control are essential elements ensuring timely delivery and superior product outcomes. Noise reduction and vibration isolation technologies are increasingly sought after for improved passenger comfort and operational efficiency. Performance metrics, thermal management, and manufacturing processes undergo constant refinement to optimize fuel consumption and reduce environmental impact. For instance, a leading aircraft manufacturer reported a 15% increase in sales due to the integration of advanced coating technologies for stealth capabilities.

- Industry growth is expected to reach 5% annually, fueled by the demand for heat-resistant alloys, fire suppression systems, and sensor integration in electronic warfare applications. Market dynamics remain dynamic, with ongoing research in joining techniques, material degradation assessment, and finite element analysis shaping future product offerings. Additionally, the integration of mechanical testing, durability assessment, and heat resistant alloys in manufacturing processes continues to be a focus area for market participants.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Defense Aircraft Materials Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

137 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.5% |

|

Market growth 2024-2028 |

USD 381.4 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.23 |

|

Key countries |

US, China, Russia, India, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Defense Aircraft Materials Market Research and Growth Report?

- CAGR of the Defense Aircraft Materials industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the defense aircraft materials market growth of industry companies

We can help! Our analysts can customize this defense aircraft materials market research report to meet your requirements.

RIA -

RIA -