Diesel Exhaust Fluid (DEF) Market Size 2025-2029

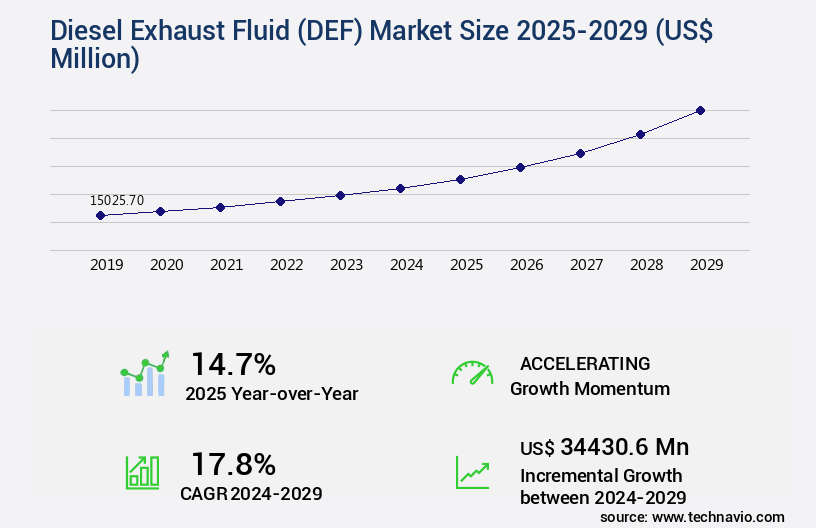

The diesel exhaust fluid (DEF) market size is valued to increase by USD 34.43 billion, at a CAGR of 17.8% from 2024 to 2029. Increasing production of vehicles will drive the diesel exhaust fluid (def) market.

Major Market Trends & Insights

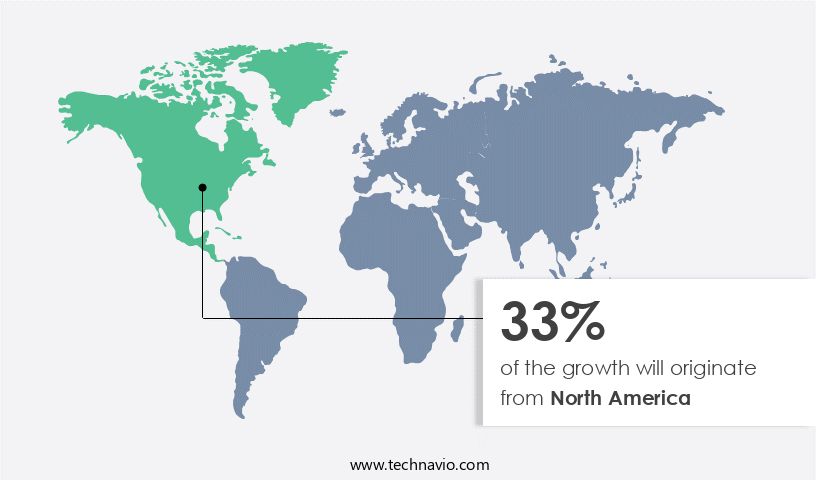

- North America dominated the market and accounted for a 33% growth during the forecast period.

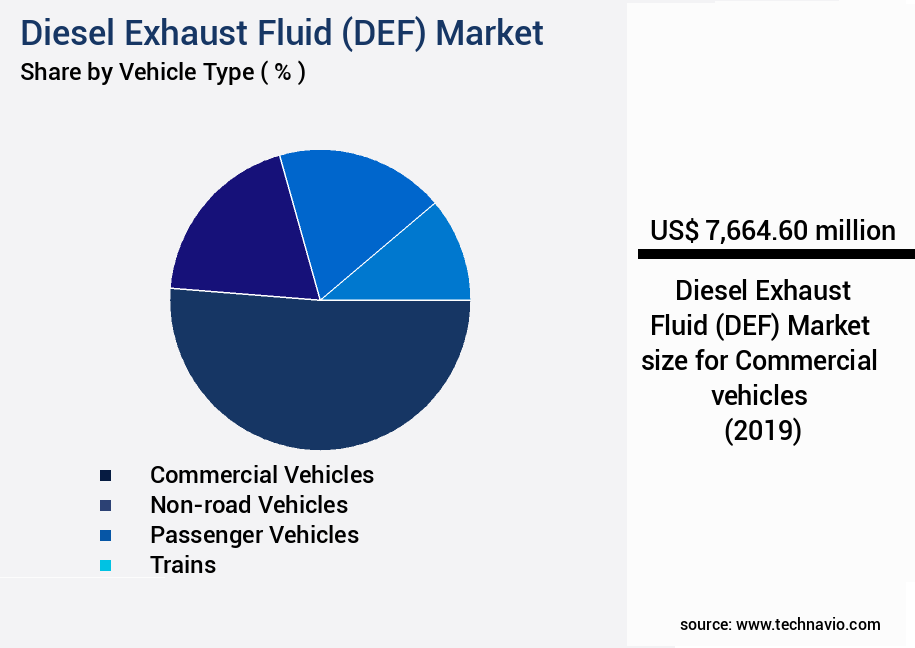

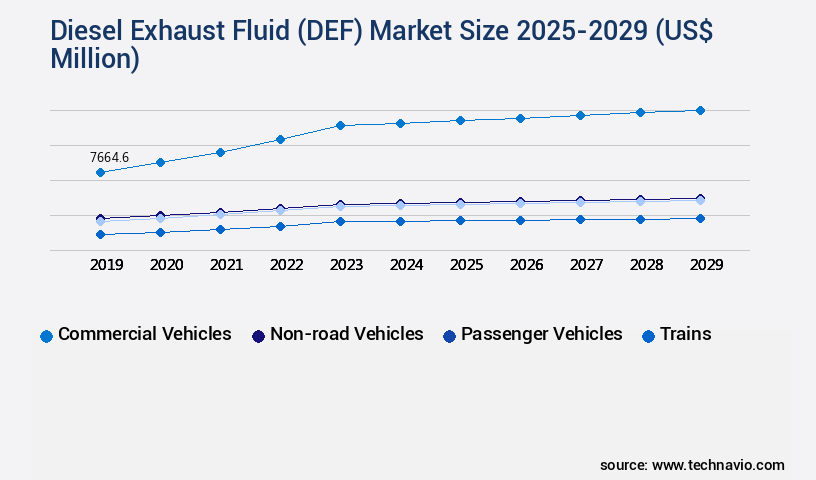

- By Vehicle Type - Commercial vehicles segment was valued at USD 7.66 billion in 2023

- By Packaging - Bulk segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 309.80 million

- Market Future Opportunities: USD 34430.60 million

- CAGR : 17.8%

- North America: Largest market in 2023

Market Summary

- The market is a dynamic and evolving industry, driven by the continuous production of vehicles and the introduction of new technologies for the reduction of NOx emissions. According to recent reports, the global DEF market is expected to experience significant growth due to the increasing adoption of Selective Catalytic Reduction (SCR) technology in diesel engines. This technology relies on DEF to neutralize harmful emissions, making it a crucial component in the automotive industry. Core technologies, such as SCR and AdBlue systems, are at the forefront of this market, enabling diesel engines to meet stringent emissions regulations. The application of DEF in various industries, including transportation, construction, and power generation, is expanding, further fueling market growth.

- However, the market faces challenges, including the decrease in demand for diesel engine vehicles due to increasing competition from electric and hybrid vehicles. Regulations, such as the European Union's Euro 6 and the US Environmental Protection Agency's Tier 4 emissions standards, continue to shape the market landscape. A recent study reveals that the DEF market is projected to account for over 30% of the total automotive aftermarket by 2025. This growth is attributed to the increasing demand for cleaner transportation solutions and the continuous development of advanced technologies to meet emissions regulations. In conclusion, the market is an essential and evolving industry, shaped by technological advancements, regulatory requirements, and market trends.

- The market's future growth is driven by the increasing adoption of SCR technology and the need for cleaner transportation solutions.

What will be the Size of the Diesel Exhaust Fluid (DEF) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Diesel Exhaust Fluid (DEF) Market Segmented and what are the key trends of market segmentation?

The diesel exhaust fluid (def) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Vehicle Type

- Commercial vehicles

- Non-road vehicles

- Passenger vehicles

- Trains

- Packaging

- Bulk

- Cans and bottles

- IBCs and drums

- Component

- Selective catalytic reduction (SCR) catalyst

- Diesel exhaust fluid (DEF) tank

- Diesel exhaust fluid (DEF) injector

- Diesel exhaust fluid (DEF) supply module

- Diesel exhaust fluid (DEF) sensor

- End-user

- OEM

- Aftermarket

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Vehicle Type Insights

The commercial vehicles segment is estimated to witness significant growth during the forecast period.

The market is a significant component of automotive emission control systems, with commercial vehicles leading the market's growth. In 2024, the commercial vehicles segment accounted for approximately 75% of the global DEF market share. This dominance can be attributed to the extensive use of diesel engines in commercial vehicles, which offer high mileage, torque, and compression compared to gasoline engines. The adoption of selective catalytic reduction (SCR) technology in diesel engines is a crucial factor driving the demand for DEF. The automotive industry's focus on reducing nitrogen oxide (NOx) emissions has led to stringent regulations from governments and the Environmental Protection Agency (EPA).

As a result, commercial vehicles, including heavy-duty trucks, light commercial vehicles, buses, coaches, and minibuses, are required to employ exhaust gas treatment systems, such as DEF injection systems and diesel oxidation catalysts, to meet emission standards. The DEF market's future growth is expected to be robust, with an estimated 35% of the global diesel fleet expected to be SCR-equipped by 2027. Moreover, the off-road vehicle sector is also anticipated to experience significant growth due to increasing regulations on off-road vehicle emissions. The DEF production process involves urea synthesis, adulteration detection, and urea hydrolysis to produce the fluid. The DEF supply chain includes manufacturers, distributors, and retailers, ensuring the fluid's quality standards are met.

DEF consumption rates are influenced by factors such as vehicle refueling infrastructure, DEF storage tanks, and vehicle usage patterns. SCR system diagnostics and emission monitoring systems are essential for maintaining the efficiency of the SCR catalyst and exhaust aftertreatment systems. Fluid degradation and ammonia slip are common issues that can impact the catalyst's efficiency, necessitating regular maintenance and monitoring. In conclusion, the Diesel Exhaust Fluid market is a critical component of the automotive industry's emission control systems, with commercial vehicles leading the market's growth. The market's future growth is expected to be substantial, driven by the increasing adoption of SCR technology and stringent emission regulations.

The Commercial vehicles segment was valued at USD 7.66 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 33% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Diesel Exhaust Fluid (DEF) Market Demand is Rising in North America Request Free Sample

In North America, the market holds a significant position, with the US and Canada collectively accounting for a substantial share in 2024. Yara, a leading DEF producer, has a robust presence in this region, operating multiple terminals to cater to the growing demand. These terminals include facilities in Belle Plaine, California, Florida, Stockton, Tampa, Chesapeake, Houston, and New Jersey. Musket, another prominent DEF supplier, maintains 13 production terminals across the US.

The high number of vehicles on the roads in key North American countries necessitates the continuous production and distribution of DEF.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is a critical component of selective catalytic reduction systems (SCR) used in heavy-duty vehicle emission control technologies. Urea solution purity significantly impacts SCR performance, with impurities affecting ammonia slip reduction strategies. The interaction between diesel oxidation catalysts and SCR catalysts also plays a crucial role in NOx reduction. DEF dispensing system design and optimization are essential to minimize urea crystallization, which can impact SCR system efficiency and reliability. Understanding DEF fluid degradation mechanisms and implementing effective storage and handling practices are key to improving system performance and minimizing harmful emissions from heavy vehicles.

More than 70% of new product developments in the automotive industry focus on advanced emission control technologies for trucks, with a significant portion dedicated to optimizing DEF consumption rates in vehicles. Exhaust gas temperature sensor calibration procedures and adultration detection methods are critical to maintaining SCR system efficiency and ensuring regulatory compliance with automotive emission regulations. The industrial application segment accounts for a significantly larger share of the DEF market compared to the academic segment, driven by stringent emission norms and increasing focus on reducing harmful emissions from heavy vehicles. Improving SCR system efficiency and reliability through performance monitoring techniques and exhaust gas temperature sensor calibration procedures are key priorities for market players.

Adoption rates of DEF systems in Europe are nearly double those in North America, driven by stringent emission norms and regulatory compliance requirements. Effective DEF storage and handling practices, including tank level monitoring system design and minimizing ammonia slip in SCR systems, are essential to maintaining system performance and ensuring regulatory compliance.

What are the key market drivers leading to the rise in the adoption of Diesel Exhaust Fluid (DEF) Industry?

- The significant expansion in vehicle production serves as the primary catalyst for market growth.

- The market experiences significant expansion due to the increasing demand from the automotive industry. This sector is the primary consumer of DEF, driven by factors such as urbanization, modernization, population growth, and rising disposable income. Developing countries, particularly in the Asia Pacific (APAC) region, including China and India, are major contributors to the automobile production sector. With the economic recovery in the US and Europe, the demand for automotive products is projected to increase further. As a result, automotive original equipment manufacturers (OEMs) are compelled to enhance their production capabilities to meet the escalating demand.

- This may involve installing new production capacity or expanding existing facilities. The automotive industry's continuous growth and the evolving need for cleaner emissions solutions underscore the market's ongoing dynamism.

What are the market trends shaping the Diesel Exhaust Fluid (DEF) Industry?

- The introduction of new technologies is mandated for reducing NOX emissions, reflecting the current market trend.

- The global market for NOX emissions reduction from diesel engines continues to evolve, driven by the pressing need for environmental sustainability. BMW's BluePerformance technology is a notable innovation, which complements the standard diesel particle filter and NOX catalytic converter with the addition of AdBlue. BMW offers this technology in nine diesel models, enabling significant NOX emission reductions. Another groundbreaking development is the Ammonia Creation and Conversion Technology (ACCT), pioneered by researchers at Loughborough University. ACCT converts AdBlue to function effectively at lower exhaust temperatures, addressing the limitation of AdBlue's requirement for high exhaust temperatures (above 482 degrees Fahrenheit).

- These advancements underscore the dynamic nature of the market, with ongoing research and development efforts to create more efficient and effective solutions for NOX emissions reduction in diesel engines.

What challenges does the Diesel Exhaust Fluid (DEF) Industry face during its growth?

- The decreasing demand for diesel engine vehicles poses a significant challenge to the industry's growth trajectory.

- The diesel engine car market faces a declining trend despite its advantages over gasoline and gas engines. Key markets for diesel vehicles include China, India, Germany, the UK, and France. However, growing concerns over environmental pollution from diesel exhaust gas emissions have led to stringent regulations and potential bans on diesel vehicles in these countries. This shift towards electric vehicles is a significant challenge for the market, which relies on diesel engines. The European Union, for instance, has set strict emission norms, with Stage V regulations coming into effect from 2020.

- China, too, has announced plans to phase out diesel vehicles in favor of electric ones by 2030. This regulatory landscape poses a significant hurdle for the diesel engine market's growth. Additionally, governments' initiatives and incentives to promote electric vehicles further intensify the competition.

Exclusive Technavio Analysis on Customer Landscape

The diesel exhaust fluid (def) market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the diesel exhaust fluid (def) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Diesel Exhaust Fluid (DEF) Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, diesel exhaust fluid (def) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Airgas - The company specializes in the production and distribution of diesel exhaust fluid (DEF) and related solutions, essential for reducing harmful emissions in heavy-duty vehicles. As a research analyst, I observe the company's commitment to sustainability and innovation within the automotive industry. Their offerings cater to the growing demand for eco-friendly diesel engine technology.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Airgas

- BASF SE

- Blue Sky Diesel Exhaust Fluid

- CF Industries

- Chemours Company

- China Petrochemical Corporation

- Cummins Filtration

- Dyno Nobel

- GreenChem Solutions

- Innoco Oil

- KOST USA

- McPherson Oil

- Nissan Chemical Corporation

- Old World Industries

- Reladyne

- Sinopec

- TotalEnergies

- Valvoline

- Yara International

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Diesel Exhaust Fluid (DEF) Market

- In January 2024, BASF SE, a leading chemical producer, announced the expansion of its production capacity for AdBlue®, a type of Diesel Exhaust Fluid (DEF), at its site in Ludwigshafen, Germany. This expansion aimed to cater to the growing demand for low-emission solutions in the transportation sector (BASF press release, 2024).

- In March 2024, Shell Trading (U.K.) Limited, a subsidiary of Royal Dutch Shell, entered into a strategic partnership with Nouryon, a specialty chemicals company, to produce and market DEF in Europe. This collaboration aimed to strengthen Shell's position in the DEF market and expand its product offerings (Shell press release, 2024).

- In May 2024, Caterpillar Inc., a leading manufacturer of construction and power equipment, received approval from the U.S. Environmental Protection Agency (EPA) for its new DEF product, Cat® DEF 32. This approval marked the first time a 32% DEF concentration was approved for use in the U.S., offering improved logistics and handling advantages for customers (Caterpillar press release, 2024).

- In April 2025, Sinopec Corporation, China's largest oil and gas producer, announced the completion of its new DEF production facility in Maoming, Guangdong Province. With an annual capacity of 200,000 tons, this facility was expected to significantly increase China's domestic DEF production and reduce its reliance on imports (Sinopec press release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Diesel Exhaust Fluid (DEF) Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

251 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 17.8% |

|

Market growth 2025-2029 |

USD 34430.6 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

14.7 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- In the dynamic and evolving world of automotive emission control, the significance of Diesel Exhaust Fluid (DEF) continues to grow. This urea-based fluid plays a crucial role in Selective Catalytic Reduction (SCR) systems, an essential component of exhaust gas treatment for reducing nitrogen oxide (NOx) emissions. The continuous unfolding of market activities reveals an increasing focus on DEF handling procedures, ensuring optimal Scr catalyst efficiency. Automotive manufacturers and off-road vehicle manufacturers alike are investing in advanced DEF injection systems to enhance nitrogen oxide reduction capabilities. Exhaust aftertreatment systems have become a standard feature in modern vehicles, necessitating a robust DEF supply chain.

- Adblue composition, a key aspect of DEF production, is under constant scrutiny for maintaining DEF quality standards. Urea synthesis and hydrolysis processes are being refined to improve DEF production efficiency. Defying the notion of stagnancy, the market is also witnessing advancements in DEF adulteration detection and urea crystallization prevention. Water content measurement in DEF is gaining importance, as is the development of efficient DEF dispensing systems. The interplay of emission control systems, diesel oxidation catalysts, and particulate filter regeneration continues to shape the market landscape. The evolution of emission standards and the emergence of mobile urea dosing systems further underscore the market's dynamism.

- In the realm of heavy-duty vehicle emissions, urea-based fluids are becoming increasingly indispensable. Ammonia slip, a critical concern in DEF usage, is being addressed through rigorous research and development efforts. The market's complexity is mirrored in the intricacies of DEF handling, from storage tanks to vehicle refueling infrastructure. The interconnectedness of these elements underscores the importance of understanding the nuances of DEF and its role in exhaust gas treatment.

What are the Key Data Covered in this Diesel Exhaust Fluid (DEF) Market Research and Growth Report?

-

What is the expected growth of the Diesel Exhaust Fluid (DEF) Market between 2025 and 2029?

-

USD 34.43 billion, at a CAGR of 17.8%

-

-

What segmentation does the market report cover?

-

The report segmented by Vehicle Type (Commercial vehicles, Non-road vehicles, Passenger vehicles, and Trains), Packaging (Bulk, Cans and bottles, and IBCs and drums), Component (Selective catalytic reduction (SCR) catalyst, Diesel exhaust fluid (DEF) tank, Diesel exhaust fluid (DEF) injector, Diesel exhaust fluid (DEF) supply module, and Diesel exhaust fluid (DEF) sensor), End-user (OEM and Aftermarket), and Geography (North America, APAC, South America, Europe, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, South America, Europe, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing production of vehicles, Decrease in the demand for diesel engine vehicles

-

-

Who are the major players in the Diesel Exhaust Fluid (DEF) Market?

-

Key Companies Airgas, BASF SE, Blue Sky Diesel Exhaust Fluid, CF Industries, Chemours Company, China Petrochemical Corporation, Cummins Filtration, Dyno Nobel, GreenChem Solutions, Innoco Oil, KOST USA, McPherson Oil, Nissan Chemical Corporation, Old World Industries, Reladyne, Sinopec, TotalEnergies, Valvoline, and Yara International

-

Market Research Insights

- The market encompasses a critical segment of heavy-duty vehicle technology, focusing on emission control solutions. With the increasing stringency of emission regulations, the demand for DEF has witnessed substantial growth. According to industry estimates, the global DEF market is projected to reach a value of USD12.5 billion by 2026, expanding at a CAGR of 5.5% from 2021. Urea, the primary component of DEF, plays a pivotal role in Selective Catalytic Reduction (SCR) systems, which help reduce Nitrogen Oxides (NOx) emissions. The compatibility of DEF with exhaust gas recirculation systems, urea purity requirements, and DEF shelf life are essential considerations in ensuring optimal SCR system performance.

- Moreover, the importance of system fault diagnosis, NOx sensor calibration, and SCR system optimization is paramount in maintaining the efficiency of DEF-based emission reduction strategies. Exhaust gas analysis, flow rate measurement, and DEF dispensing equipment are integral components of the overall DEF market ecosystem. Fuel efficiency improvements and reducing particulate matter are key benefits of DEF technology, which is continually evolving through emission control regulations, DEF freeze protection, vehicle certification standards, and engine performance optimization. Advancements in exhaust gas analysis, ammonia injection technology, and urea solution properties further underscore the dynamic nature of the Diesel Exhaust Fluid market.

We can help! Our analysts can customize this diesel exhaust fluid (def) market research report to meet your requirements.

RIA -

RIA -