Digital IC Market Size 2025-2029

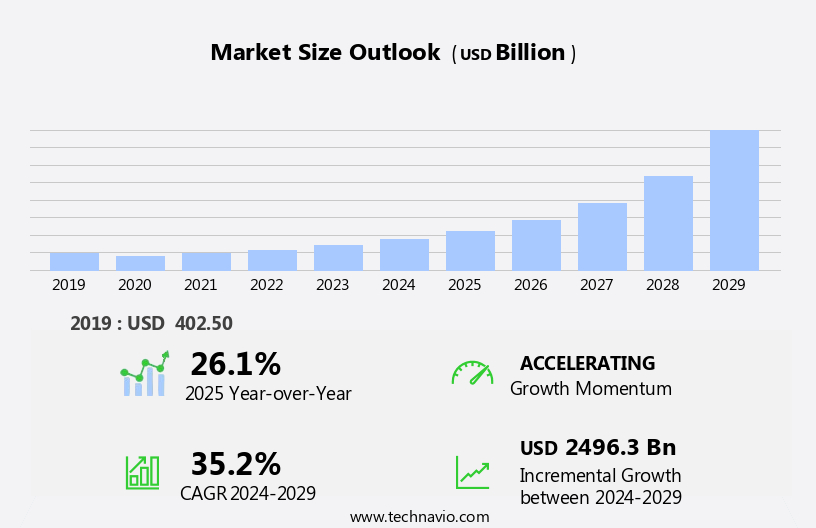

The digital IC market size is forecast to increase by USD 2,496.3 billion, at a CAGR of 35.2% between 2024 and 2029.

- The market is experiencing significant growth, driven by the widespread adoption of smartphones and tablets worldwide. This trend is fueled by the increasing demand for advanced features and functionalities in mobile devices. Another key driver is the growing adoption of the Internet of Things (IoT) among end-users, leading to an escalating need for digital ICs in various applications such as wearable devices and smart home systems. However, the market faces challenges in the form of high manufacturing costs, which can hinder the growth of smaller players and limit their competitiveness.

- Furthermore, the integration of advanced technologies like artificial intelligence and machine learning into digital ICs is becoming increasingly essential, adding to the complexity and cost of production. Companies in the market must navigate these challenges by exploring cost-effective manufacturing methods and collaborating with technology partners to stay competitive and capitalize on emerging opportunities. Additionally, the increasing integration of IoT (Internet of Things) in various sectors is another major trend, requiring advanced digital ICs for efficient data processing and connectivity.

What will be the Size of the Digital IC Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

- The Integrated Circuit (IC) market continues to evolve, driven by advancements in design methodology, reliability analysis, and performance optimization. IC design outsourcing and verification tools facilitate design complexity reduction and ensure quality control. Chip packaging materials and manufacturing process innovations contribute to power consumption minimization and failure analysis. IC industry growth is fueled by technology advancement and the increasing demand for electronic design services.

- IC design innovation and the adoption of design verification tools are essential for addressing the challenges of IC design and meeting the demands of diverse applications. IC patents play a crucial role in fostering competition and driving progress in this dynamic industry. Design validation, security, and supply chain management are critical areas of focus. Chip manufacturing equipment and design software enable cost reduction and standardization. The market encompasses various components, including voltages, logic gates, multiplexers, magnitude comparators, priority encoders, and microprocessor chips.

How is this Digital IC Industry segmented?

The digital IC industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

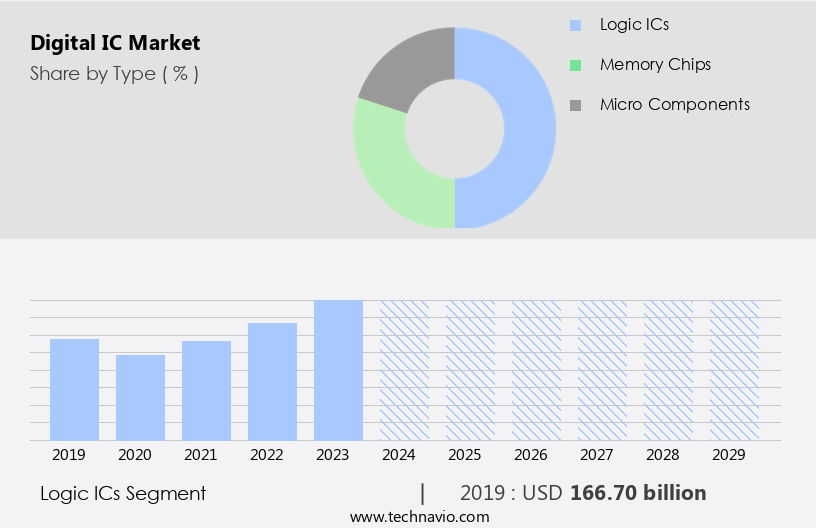

- Type

- Logic ICs

- Memory chips

- Micro components

- End-user

- Computer

- Telecommunication

- Automotive

- Consumer Electronics

- Others

- Product Type

- Greater than 45 nm

- 10 to 20 nm

- Less than 10 nm

- 20 to 45 nm

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- Australia

- China

- Japan

- South Korea

- Taiwan

- Rest of World (ROW)

- North America

By Type Insights

The logic ICs segment is estimated to witness significant growth during the forecast period. In the realm of digital integrated circuits (ICs), logic ICs occupy a significant role in semiconductor technology. These circuits perform fundamental logical operations on digital input signals and are indispensable in various industries, including consumer electronics, telecommunications, and automotive sectors. Innovative applications such as state machines, controllers, and data processing circuits have been developed using logic ICs. The preference for logic ICs stems from their power efficiency, cost-effectiveness, and advanced features that surpass those of alternative solutions. Logic design involves digital IC design, design libraries, routing algorithms, logic synthesis, and physical design, ensuring the optimal layout and functionality of these circuits.

Machine learning (ML) and artificial intelligence (AI) applications are also benefiting from the advancements in logic IC technology, as these circuits are essential components in the development of complex algorithms and neural networks. The semiconductor manufacturing process involves wafer processing, defect analysis, and yield optimization, ensuring the production of high-quality logic ICs. The integration of AI and the need for yield optimization are additional factors contributing to the market's growth. Digital ICs are a crucial component in various applications, and their role will continue to be essential in the future. Technological advancements in smartphones, tablets, laptops, PCs, cloud computing, and big data are fueling the demand for digital ICs across multiple industries in the US.

The Logic ICs segment was valued at USD 166.70 billion in 2019 and showed a gradual increase during the forecast period.

Fault simulation and verification techniques, including functional verification and reliability testing, are crucial to maintaining high-quality logic ICs. Integration of intellectual property (IP) cores, such as digital-to-analog converters (DACs) and analog-to-digital converters (ADCs), and other advanced components, like power management and voltage regulators, further enhances logic ICs' capabilities. Wireless communication, thermal management, and power optimization are essential considerations in modern logic IC design. Logic ICs are increasingly used in emerging technologies, such as wearable electronics, system-on-chip (SoC) designs, and Internet of Things (IoT) devices. In the healthcare sector, logic ICs are utilized in medical devices and healthcare ICs, while the military, aerospace, and industrial automation industries rely on logic ICs for their robustness and reliability.

The Digital IC Market continues to expand with innovations in integrated circuit fabrication, enabling higher efficiency and reliability. Precise layout verification ensures optimal circuit performance, while wire bonding enhances connectivity in packaging. The demand for consumer electronics ICs drives advancements in storage technologies like flash memory. Modern digital devices rely on analog-to-digital converters (ADC) and digital-to-analog converters (DAC) to process signals effectively. Communication between components is streamlined through inter-integrated circuit (I²C) protocols, ensuring seamless data exchange. The integration of artificial intelligence (AI) into various sectors, including electric vehicles (EVs) and renewable energy, is also expected to boost the market.

Regional Analysis

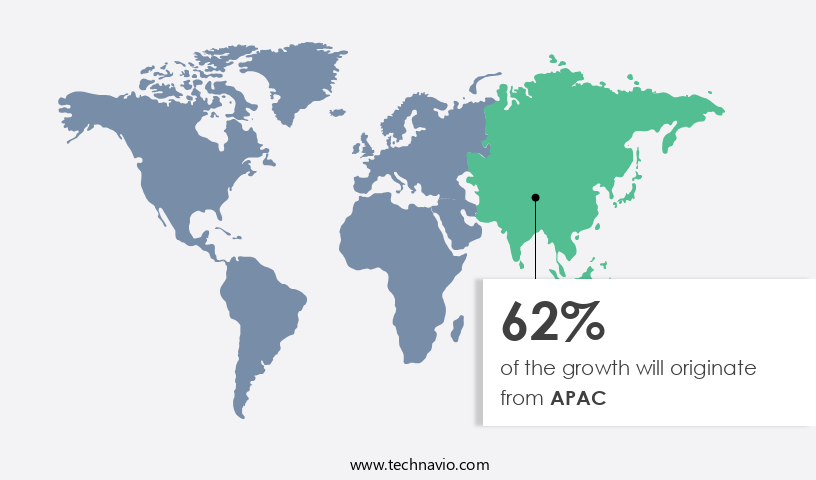

APAC is estimated to contribute 62% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market is witnessing significant growth, driven by the increasing demand for energy-efficient solutions in both industrial and consumer electronics sectors. The APAC region is at the forefront of this trend, with countries like Taiwan, South Korea, Japan, and China leading the way due to their role as manufacturing hubs for major semiconductor companies. In this dynamic landscape, several entities are shaping the market's evolution. Layout optimization and digital IC design are essential for creating efficient and cost-effective circuits. Key components, such as NAND Flash Memory ICs, priority encoders, and magnitude comparators, are integral to Digital ICs. Design libraries and simulation software facilitate the design process, ensuring accuracy and reliability. Fault simulation and functional verification are crucial for detecting and correcting errors before mass production.

Wireless communication, digital-to-analog and analog-to-digital converters, and high-speed interfaces are essential components in various applications, from healthcare ICs to wearable electronics and IoT devices. Power optimization and thermal management are key concerns in the design of system-on-chip (SoC) and other complex digital circuits. Military, aerospace, and automotive ICs require high reliability and robustness, driving the demand for advanced design methodologies and manufacturing processes. Machine learning and artificial intelligence are also transforming the IC design landscape, with applications ranging from power management and yield optimization to failure analysis and process control. Semiconductor manufacturing involves various processes, including wafer processing, defect analysis, and die bonding, to create high-quality ICs.

Intellectual property (IP) cores and synthesis tools are essential for designing and implementing complex digital and mixed-signal circuits. Battery management and voltage regulators are critical components in powering various electronic devices. In summary, the market is a complex and dynamic ecosystem, driven by the demand for energy-efficient solutions and the need for advanced design methodologies and manufacturing processes. The entities involved, from layout optimization and digital IC design to power management and failure analysis, are working together to push the boundaries of innovation and efficiency. Materials like gallium arsenide and silicon are used in the manufacturing process, and US professionals in digital electronics are driving advancements in 5G, cloud computing, and big data applications.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Digital IC market drivers leading to the rise in the adoption of Industry?

- The widespread adoption of smartphones and tablets on a global scale serves as the primary catalyst for market growth in this sector. Digital Integrated Circuits (ICs) are essential components in various applications, including consumer electronics and industrial automation. In consumer electronics, digital ICs are utilized in smartphones for functions such as memory management, microcontroller, and processor optimization. The demand for smartphones is projected to grow due to increasing Internet penetration and the availability of affordable devices in emerging markets. This trend is anticipated to drive the market for digital ICs, particularly in the form of Analog ICs, such as Analog-to-Digital Converters (ADCs), and Data Converters. In industrial automation, digital ICs play a vital role in power supplies, testing and validation, and failure analysis.

- Industrial applications require high precision and reliability, making digital ICs an indispensable part of the solution. Furthermore, the integration of Artificial Intelligence (AI) in industrial processes necessitates the use of advanced digital ICs for processing and analyzing data. Semiconductor manufacturing is another significant market for digital ICs. The production process involves various stages, including design, fabrication, and testing. Digital ICs are used in every stage, from IP cores to power supplies, ensuring the manufacturing process runs efficiently and effectively. The market is expected to grow significantly due to the increasing demand for consumer electronics and industrial automation applications.

What are the Digital IC market trends shaping the Industry?

- The increasing preference for Internet of Things (IoT) technology among end-users represents a significant market trend. This adoption is driven by the benefits that IoT provides, such as enhanced connectivity, automation, and data analysis. The Internet of Things (IoT) market encompasses a vast array of applications, from consumer electronics to industrial automation and healthcare. For consumers, IoT brings the convenience of affordable and efficient devices to optimize daily tasks. Businesses, meanwhile, benefit from automation process optimization, inventory management, energy efficiency, security, and energy conservation. With billions of devices in IoT technology, designers face challenges in accommodating incompatible interfaces and handling the performance requirements of these devices.

- Key components, such as digital-to-analog converters (DACs), wireless communication systems, and power optimization circuits, are integral to IoT applications. Intellectual property (IP) cores and flip chip technology further enhance the functionality of digital ICs. Market dynamics include the increasing demand for healthcare ICs, military ICs, and power optimization in IoT devices. Fault simulation plays a crucial role in ensuring the reliability and functionality of these advanced digital ICs. To address these challenges, advanced technology developments will necessitate the use of complex programmable logic devices, fueling the demand for digital Integrated Circuits (ICs). Digital IC design involves layout optimization, routing algorithms, and the utilization of design libraries and simulation software.

How does Digital IC market face challenges during its growth?

- The escalating costs linked to the manufacturing of digital Integrated Circuits (ICs) poses a significant challenge to the industry's growth trajectory. The market entails substantial investment for manufacturers due to the complex and evolving nature of the semiconductor industry. Factors contributing to the increased cost of production include the high capital requirements for constructing new factories and the rapid depreciation of facilities due to technological advancements. Machine learning, functional verification, high-speed interfaces, logic synthesis, physical design, wafer processing, defect analysis, thermal management, and voltage regulators are essential aspects of digital IC manufacturing.

- Additionally, the production of digital ICs for high-performance applications, such as system-on-chip (SoC) and high-speed interfaces, requires advanced equipment and expertise, leading to higher production costs. The market's capital-intensive nature necessitates a significant investment in facilities, equipment, and research and development to remain competitive and meet the evolving demands of various industries. Incorporating these technologies into the production process adds to the overall cost. Furthermore, the integration of digital ICs into various industries, such as aerospace, wearable electronics, and IoT devices, necessitates stringent quality control and rigorous testing, further increasing the manufacturing expenses.

Exclusive Customer Landscape

The digital IC market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the digital IC market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, digital IC market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Analog Devices Inc. - This company specializes in providing advanced digital integrated circuits (ICs) for various applications, encompassing the automotive, portable, motor control, power management, security, and test and measurement sectors.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Analog Devices Inc.

- Broadcom Inc.

- Huawei Technologies Co. Ltd.

- Infineon Technologies AG

- Intel Corp.

- Lattice Semiconductor Corp.

- MediaTek Inc.

- Micron Technology Inc.

- Micross Inc.

- NXP Semiconductors NV

- Qualcomm Inc.

- Renesas Electronics Corp.

- Samsung Electronics Co. Ltd.

- Semiconductor Manufacturing International Corp.

- STMicroelectronics NV

- Taiwan SEMICONDUCTOR CO. LTD.

- Taiwan Semiconductor Manufacturing Co. Ltd.

- Texas Instruments Inc.

- Toshiba Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Digital IC Market

- In February 2024, Intel unveiled its new FPGA-based digital IC, the Agilex FPGA, designed for artificial intelligence (AI) and 5G applications, marking a significant technological advancement in the market (Intel Press Release, 2024).

- In May 2024, Samsung Electronics and AMD entered into a strategic partnership to co-develop next-generation graphics processors, merging AMD's high-performance computing expertise with Samsung's advanced semiconductor technology, potentially increasing competition in the market (Samsung Newsroom, 2024).

- In March 2025, GlobalFoundries announced a USD 10 billion investment in its Fab 8 facility in New York, expanding its manufacturing capabilities and aiming to increase its market share in the market (GlobalFoundries Press Release, 2025).

Research Analyst Overview

The digital integrated circuit (IC) market continues to evolve, with dynamic market dynamics shaping its applications across various sectors. Digital IC design, layout optimization, and design libraries are crucial elements in creating efficient and reliable circuits. Fault simulation plays a vital role in identifying and rectifying design errors, ensuring the integrity of digital-to-analog converters (DACs) and analog-to-digital converters (ADCs). Wireless communication, a key application of digital ICs, is driving innovation in routing algorithms and power optimization. Flip chip technology and wafer processing enable high-speed interfaces and system-on-chip (SoC) integration. Intellectual property (IP) and simulation software are essential tools for functional verification and logic synthesis.

Healthcare ICs, military ICs, aerospace ICs, and industrial automation ICs require stringent power optimization and reliability testing. Wearable electronics and IoT devices demand power management, battery management, and thermal management solutions. Automotive ICs focus on power management, yield optimization, and process control. Advancements in machine learning (ML) and artificial intelligence (AI) are transforming digital IC design, with applications in chip architecture, data converters, and semiconductor manufacturing. Power supplies, voltage regulators, and die bonding are critical components in maintaining the performance and longevity of digital ICs. The ongoing unfolding of market activities reveals evolving patterns in digital IC design, with a focus on high-speed interfaces, chip architecture, and mixed-signal ICs.

Synthesis tools and simulation software continue to play a pivotal role in the development of advanced digital ICs. The Digital IC Market is evolving rapidly, driven by advancements in IC design software and IC technology advancement. The demand for high-performance IC applications has increased, necessitating robust IC testing equipment and improved IC security measures. Companies focus on IC innovation to optimize IC power consumption and enhance IC reliability. Efficient IC design methodology aids in reducing IC design complexity, ensuring better IC performance optimization and IC cost reduction. The IC supply chain plays a critical role in seamless production, from IC manufacturing process to IC packaging process. Rigorous IC quality control, including IC failure analysis and IC reliability analysis, ensures market competitiveness. Industry-wide IC standardization facilitates IC design verification and IC design validation, reinforcing reliability and efficiency in modern digital circuits.

Dive into Technavio's strong research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Digital IC Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

237 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 35.2% |

|

Market growth 2025-2029 |

USD 2,496.3 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

26.1 |

|

Key countries |

China, US, Japan, South Korea, Taiwan, Australia, Germany, UK, Canada, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Digital IC Market Research and Growth Report?

- CAGR of the Digital IC industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the digital ic market growth of industry companies

We can help! Our analysts can customize this digital ic market research report to meet your requirements.

RIA -

RIA -