Disposable Urinary Drainage Bag Market Size 2024-2028

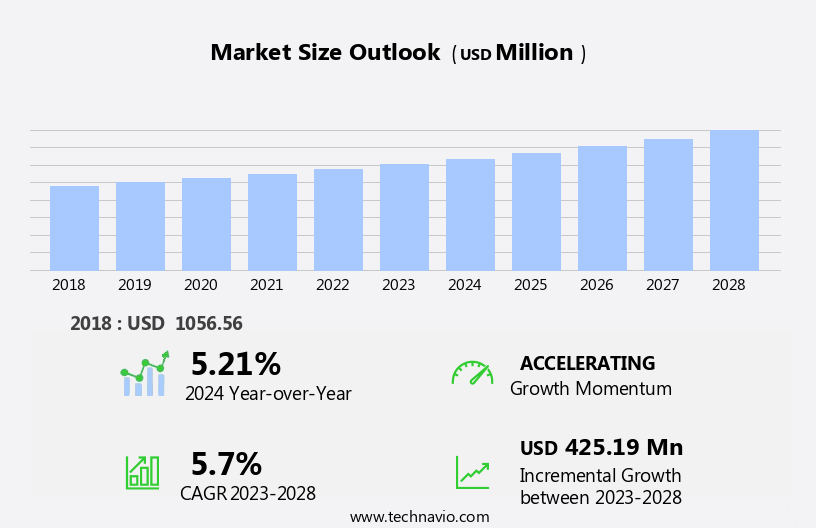

The disposable urinary drainage bag market size is forecast to increase by USD 425.19 million, at a CAGR of 5.7% between 2023 and 2028.

- The market is experiencing significant growth, driven by the rising incidence of targeted diseases necessitating long-term urinary catheterization. This trend is particularly prominent in an aging population, where chronic conditions such as urinary incontinence and benign prostatic hyperplasia are increasingly common. Furthermore, technological innovations continue to shape the market, with advancements in materials, design, and functionality enhancing patient comfort and reducing the risk of complications. However, challenges persist in the form of issues arising due to catheters in urinary drainage bags.

- These complications, including urinary tract infections and catheter-associated bladder injuries, necessitate careful management and ongoing research to mitigate risks and improve patient outcomes. Companies seeking to capitalize on market opportunities must remain agile and responsive to these trends and challenges, focusing on product innovation, patient-centric design, and rigorous quality control to meet evolving customer needs and expectations.

What will be the Size of the Disposable Urinary Drainage Bag Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by advancements in technology and growing demand across various healthcare sectors. Single-use drainage bags, a key component of urinary catheterization systems, are integral to maintaining patient mobility and managing urine output. These bags come in various sizes and materials, including latex-free options and those made from non-woven fabric, ensuring patient safety and comfort. Drainage system components, such as connectors, inflation prevention mechanisms, and antimicrobial tubing, play a crucial role in preventing complications and ensuring efficient urine collection. Closed drainage systems and gravity drainage systems are two common types, each with unique advantages.

Patient safety features, such as leak prevention technology and spill-proof designs, are increasingly important considerations in the development of disposable drainage bags. Urine output monitoring and sterile packaging requirements are essential aspects of infection control practices, ensuring the highest standards of healthcare waste management and decontamination processes. Flow control mechanisms, such as spigot valve mechanisms and leg bag straps, offer added convenience and patient comfort. The ongoing unfolding of market activities reveals a focus on enhancing patient mobility, improving user experience, and minimizing the risk of complications. Medical-grade polymers and pressure-sensitive adhesives are among the materials used to create durable, reliable, and easy-to-use drainage bags.

Urinary catheter size and leg bag volume are essential factors in selecting the right drainage bag for each patient. Sterile packaging requirements and measurement scale markings are essential for maintaining infection control and ensuring accurate monitoring of urine output. The evolving nature of the market underscores the importance of staying informed about the latest trends and advancements in this dynamic field.

How is this Disposable Urinary Drainage Bag Industry segmented?

The disposable urinary drainage bag industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

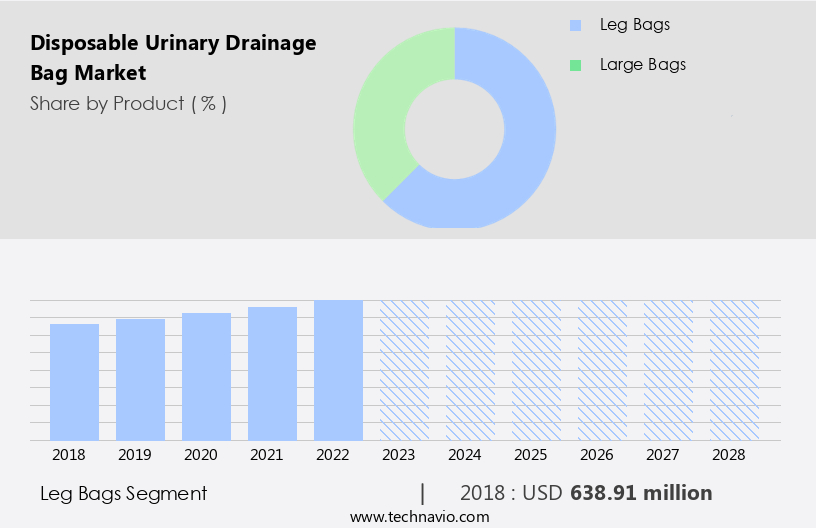

- Product

- Leg bags

- Large bags

- End-user

- Hospitals

- Clinics

- Others

- Geography

- North America

- US

- Canada

- Europe

- Germany

- UK

- APAC

- China

- Rest of World (ROW)

- North America

By Product Insights

The leg bags segment is estimated to witness significant growth during the forecast period.

Disposable urinary leg bags are a type of single-use drainage system designed for mobile patients, enabling them to collect urine effectively while maintaining mobility. These bags are strapped to the thigh or calf, allowing users to move freely in various healthcare settings, including hospitals, rehabilitation centers, and home care. Leg bags are essential for individuals with urinary incontinence, post-surgery recovery, or conditions requiring continuous urine drainage. The system's components include a drainage bag, connector, tubing, anti-kink and anti-reflux valves, and a spigot valve mechanism for controlled urine disposal. Closed drainage systems with bag inflation prevention are gaining popularity due to their enhanced leak prevention capabilities.

Latex- and PVC-free materials are used to ensure patient safety and comfort. Patient comfort is a crucial factor in leg bag design, with features such as non-woven fabric, adjustable leg straps, and a spill-proof design. Urine output monitoring, infection control practices, and sterile packaging requirements are essential considerations in the production process. Healthcare waste management and decontamination processes are essential aspects of leg bag disposal. Medical-grade polymers and infection control practices are integrated into the design to prevent bacterial contamination and ensure measurement scale markings for accurate monitoring. Leg bags come in various sizes, volumes, and urinary catheter compatibility, catering to diverse patient needs.

The flow control mechanism and drainage bag hanger facilitate easy handling and secure attachment, enhancing patient safety and convenience.

The Leg bags segment was valued at USD 638.91 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

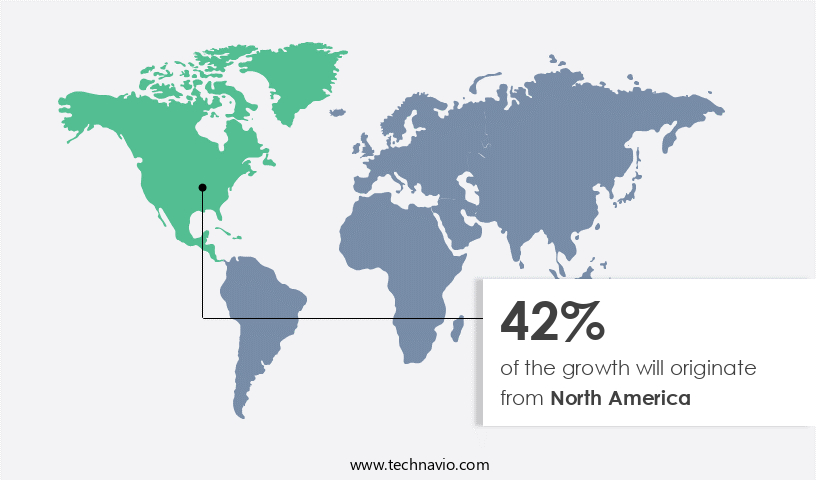

North America is estimated to contribute 42% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in North America holds a significant share due to the increasing prevalence of conditions such as bladder obstruction, urinary incontinence, Benign Prostate Hyperplasia (BPH), urinary retention, and bladder cancer. For instance, in the US, approximately 200,000 patients undergo surgical procedures for BPH annually. Similarly, in Canada, around 12,500 new bladder cancer cases and over 2,600 deaths were reported in 2020. This regional market growth can be attributed to the advanced healthcare infrastructure and high patient awareness. The market's evolution is marked by the development of innovative components, such as closed drainage systems, anti-kink tubing, anti-reflux valves, and leak prevention technology.

These advancements aim to improve patient comfort and safety, ensuring optimal urine collection and reducing the risk of complications. Disposable urinary drainage bags are typically made from medical-grade polymer materials and non-woven fabrics, ensuring sterile packaging requirements and infection control practices. Patient mobility devices and drainage bag hangers facilitate easier handling and positioning for patients. Gravity drainage systems and flow control mechanisms enable efficient urine output monitoring, while spill-proof designs and leg bag straps ensure secure attachment and leak prevention. Latex-free and PVC-free options cater to patient sensitivities and environmental concerns. Healthcare waste management and decontamination processes are crucial aspects of the market, ensuring proper disposal and sterilization of used bags to prevent bacterial contamination.

Pressure-sensitive adhesives and measurement scale markings further enhance the functionality and convenience of these products.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market encompasses a diverse range of products designed to manage urinary drainage for individuals with various medical conditions. These bags, an essential component of healthcare solutions, offer convenience and hygiene benefits for both patients and healthcare providers. Focusing on the evolving nature of this market, advancements in materials and design have led to the development of disposable urinary drainage bags with improved features. For instance, some bags are now made with soft, comfortable materials that minimize skin irritation, while others incorporate antimicrobial properties to reduce the risk of urinary tract infections. Key areas involve the continuous development of disposable urinary drainage bags to cater to specific patient needs. Through methods such as customizable sizes and shapes, these products can accommodate various clinical situations. Additionally, some bags are designed for use during specific medical procedures, such as urological surgeries or post-partum recovery. With considerations like patient comfort, ease of use, and infection prevention in mind, manufacturers are increasingly focusing on producing disposable urinary drainage bags that meet the unique requirements of various patient populations. This includes individuals with spinal cord injuries, urinary incontinence, or those undergoing urological treatments. Moreover, the use of disposable urinary drainage bags extends beyond hospitals and clinical settings. They have gained popularity in long-term care facilities, home healthcare, and even in the military for field medical care. The versatility of these products, combined with their disposable nature, makes them a valuable addition to various healthcare environments. In conclusion, the market is a dynamic and expanding sector that plays a crucial role in addressing the diverse needs of patients with urinary drainage requirements. By focusing on innovation, patient comfort, and infection prevention, manufacturers continue to develop advanced products that cater to the unique demands of various healthcare settings.

What are the key market drivers leading to the rise in the adoption of Disposable Urinary Drainage Bag Industry?

- The escalating prevalence of targeted diseases serves as the primary catalyst for market growth.

- The market is experiencing significant growth due to the increasing prevalence of diseases necessitating post-surgical urinary drainage. Conditions such as bladder obstruction, urinary incontinence, Benign Prostate Hyperplasia (BPH), urinary retention, and bladder cancer drive the demand for these bags. Following surgical interventions, patients undergo constant monitoring and care, leading to an increased need for disposable urinary drainage bags. Moreover, the COVID-19 pandemic has resulted in a surge in hospitalizations, particularly among elderly patients, who typically require these bags upon admission to minimize movement.

- Key components of disposable urinary drainage systems include single-use drainage bags, drainage bag connectors, closed drainage systems, anti-kink tubing, and anti-reflux valves. These systems ensure bag inflation prevention and extended bag lifespan, making them essential in healthcare settings. Disposable bag materials are chosen for their biocompatibility, transparency, and ease of use, contributing to the market's growth.

What are the market trends shaping the Disposable Urinary Drainage Bag Industry?

- The trend in the market is shaped by technological innovations.

- Urinary incontinence, a prevalent condition that affects many individuals, particularly women as they age, necessitates the use of urinary drainage systems. companies in the urinary drainage bag market are focusing on enhancing their offerings with advanced technology to prevent infections and improve patient comfort. Traditional urinary catheters can lead to urinary tract infections, prolonging hospital stays and increasing healthcare expenses. To mitigate this, antimicrobial-coated Foley catheters are being developed, which carry a lower risk of infection due to their antimicrobial coatings.

- These coatings incorporate nitrofurazone or various silver compounds. The gravity drainage system, a common feature in urinary drainage bags, allows for easy urine collection. Spigot valve mechanisms facilitate controlled drainage, while drainage bag disposal and patient comfort features ensure a harmonious patient experience. The focus on patient safety and cost reduction through infection prevention is a significant market driver.

What challenges does the Disposable Urinary Drainage Bag Industry face during its growth?

- The presence of issues related to catheters in urinary drainage bags poses a significant challenge to the growth of the industry. Specifically, complications arising from the use of these catheters, such as infection, clotting, and leakage, can negatively impact patient outcomes and increase healthcare costs. Addressing these challenges through technological advancements and improved clinical practices is essential for driving industry expansion.

- Urinary catheters are essential medical devices for managing urinary incontinence and post-surgery recovery. However, their use increases the risk of urinary tract infections (UTIs), which are the most common healthcare-associated infections according to the National Healthcare Safety Network (NHSN). These infections can lead to discomfort, increased healthcare costs, and potential complications. To mitigate these risks, disposable urinary drainage bags have gained popularity. These bags come with a flow control mechanism, ensuring efficient urine collection and reducing the risk of leakage. Additionally, latex-free drainage bags are available to cater to patients with allergies. Drainage bag hangers and leg bag straps provide patient mobility and ease of use.

- Non-woven fabric materials are often used in the production of these bags due to their absorbency and durability. Urine output monitoring is another crucial feature, allowing healthcare professionals to assess a patient's hydration levels and overall health. Sterile packaging requirements ensure the bags maintain aseptic conditions during storage and transportation. Maintaining proper catheter size and regular cleaning are essential to minimize the risk of UTIs. By addressing these concerns, disposable urinary drainage bags offer a more hygienic and efficient solution for managing urinary catheters.

Exclusive Customer Landscape

The disposable urinary drainage bag market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the disposable urinary drainage bag market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, disposable urinary drainage bag market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amsino International Inc. - Disposable urinary drainage bags from leading manufacturers feature needle-free sampling ports and anti-reflux devices, enhancing safety and infection prevention.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amsino International Inc.

- B.Braun SE

- Becton Dickinson and Co.

- Cardinal Health Inc.

- Coloplast AS

- ConvaTec Group Plc

- Flexicare Group Ltd.

- G.Surgiwear Ltd.

- Jolfamar

- McKesson Corp.

- Medline Industries LP

- Poly Medicure Ltd.

- Romsons

- Teleflex Inc.

- Urocare Products Inc.

- UROMED Kurt Drews KG

- Wujiang Evergreen EX IM Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Disposable Urinary Drainage Bag Market

- In January 2024, Medtronic plc, a global healthcare solutions company, announced the launch of its new line of disposable urinary drainage bags, the Convectus Drainage System. This innovative product features a unique design that reduces the risk of complications such as infection and leakage (Medtronic Press Release, 2024).

- In March 2024, Coloplast A/S, a leading medical devices company, entered into a strategic partnership with Merck KGaA to co-develop and commercialize a new range of disposable urinary drainage systems. This collaboration combines Coloplast's expertise in urological devices with Merck's strengths in research and development (Coloplast Press Release, 2024).

- In May 2024, ConvaTec Group plc, a global medical products and technologies company, completed the acquisition of Sensile Medical AG, a Swiss medical device company specializing in advanced wound care and continence solutions. This acquisition significantly expanded ConvaTec's portfolio in the market (ConvaTec Press Release, 2024).

- In February 2025, the U.S. Food and Drug Administration (FDA) granted 510(k) clearance to Smiths Medical, a global healthcare company, for its new line of disposable urinary drainage bags. These bags incorporate advanced design features that improve patient comfort and reduce the risk of complications (Smiths Medical Press Release, 2025).

Research Analyst Overview

- The market encompasses a range of products designed for the collection and management of urine during medical procedures or post-surgery. Key market trends include the development of patient education materials and user-friendly designs to ensure proper usage and patient safety. Quality control testing, disposal instructions, and infection control measures are essential considerations for manufacturers, along with tubing length options and medical-grade plastic materials. Manufacturers prioritize packaging integrity and shelf-life duration to maintain product safety and effectiveness. User safety guidelines, manufacturing specifications, and bag handling recommendations are crucial components of the design process. Clinical trial data and sterilization methods are integral to ensuring the performance indicators of these bags meet the highest standards.

- Bag dimensions, patient handling procedures, and material biocompatibility are essential factors in the fluid collection system's design. Infection control measures and sterilization methods are critical aspects of the market, as is healthcare waste disposal and product safety testing. Drainage bag attachment designs continue to evolve, focusing on ease of use and patient comfort. The market for disposable urinary drainage bags demands a strong focus on material properties, storage conditions, and post-operative care instructions. As the demand for these products grows, manufacturers must continually innovate to meet the needs of healthcare providers and patients alike.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Disposable Urinary Drainage Bag Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

161 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.7% |

|

Market growth 2024-2028 |

USD 425.19 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.21 |

|

Key countries |

US, Canada, Germany, UK, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Disposable Urinary Drainage Bag Market Research and Growth Report?

- CAGR of the Disposable Urinary Drainage Bag industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the disposable urinary drainage bag market growth of industry companies

We can help! Our analysts can customize this disposable urinary drainage bag market research report to meet your requirements.

RIA -

RIA -