Electric Motors For IC Engine Vehicles Market Size 2026-2030

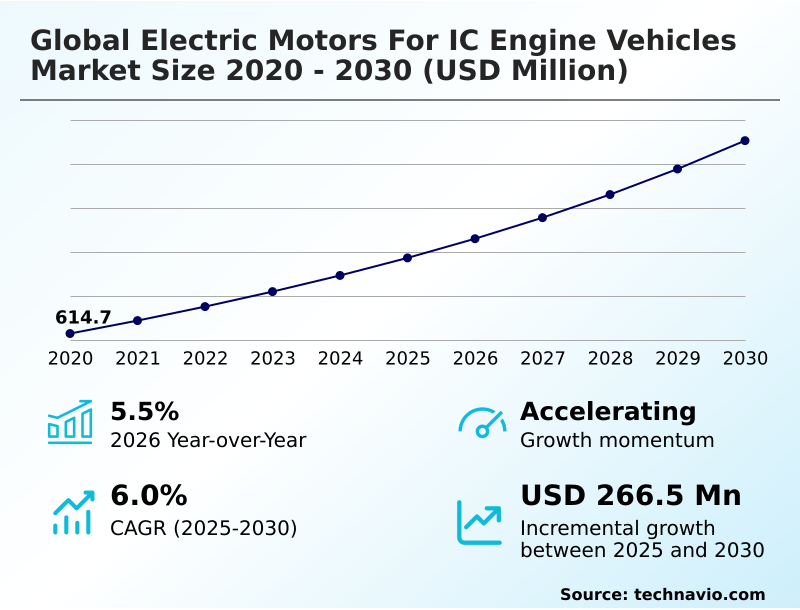

The electric motors for ic engine vehicles market size is valued to increase by USD 266.5 million, at a CAGR of 6% from 2025 to 2030. Electrification of ancillary components for thermal and mechanical efficiency will drive the electric motors for ic engine vehicles market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 60.5% growth during the forecast period.

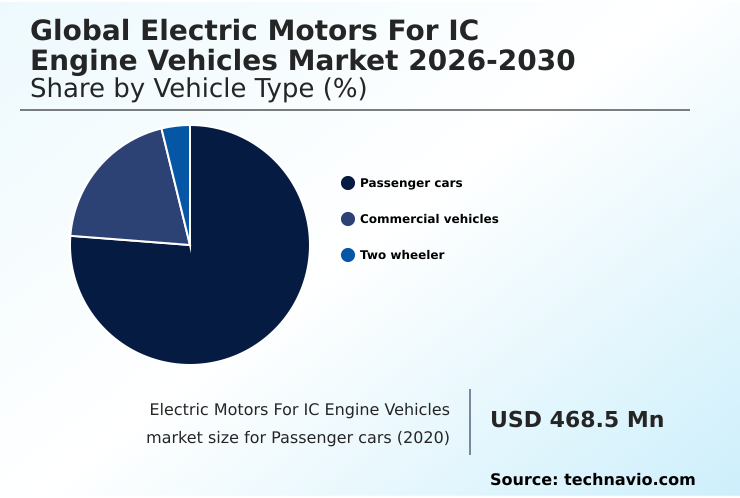

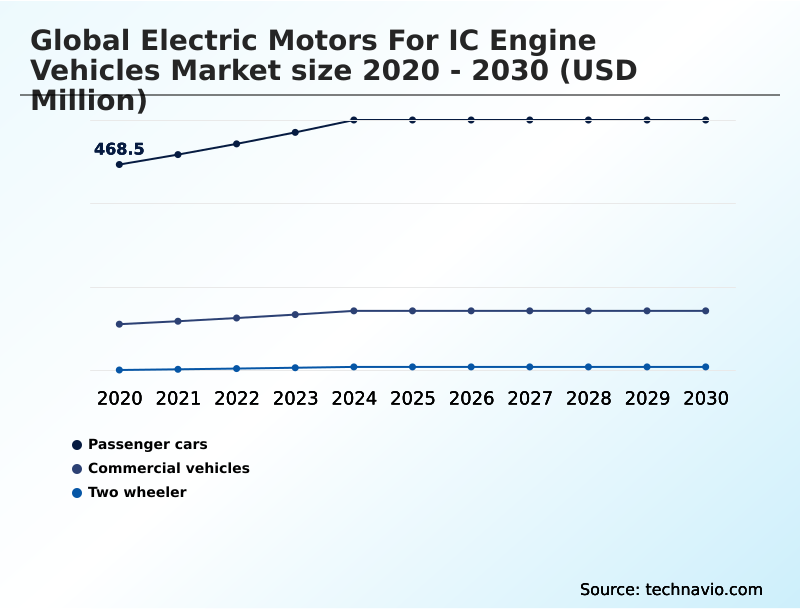

- By Vehicle Type - Passenger cars segment was valued at USD 564.9 million in 2024

- By Type - AC motor segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 438.4 million

- Market Future Opportunities: USD 266.5 million

- CAGR from 2025 to 2030 : 6%

Market Summary

- The electric motors for ic engine vehicles market is shaped by the persistent need to enhance vehicle efficiency and functionality. This demand is driven by the systematic replacement of mechanical components with sophisticated electric motors to reduce parasitic engine load and meet stringent emissions targets. Key applications include electric power steering, advanced thermal management systems, and a multitude of comfort-related actuators.

- The industry is witnessing a definitive transition from brushed DC motors to more durable and efficient brushless DC motors, particularly in critical safety and comfort systems. This technological shift requires suppliers to navigate a complex landscape, balancing investment in legacy ICE platforms with the broader industry pivot toward full electrification.

- A central operational scenario involves Tier-1 suppliers making strategic R&D allocation decisions, weighing the short-term revenue from high-volume orders for components like integrated starter-generator units against long-term investments in traction motors for electric vehicles.

- This dynamic forces a focus on creating modular and scalable motor designs that can serve both hybrid and conventional architectures, ensuring operational agility in a competitive environment where both cost-effectiveness and technological innovation are paramount.

What will be the Size of the Electric Motors For IC Engine Vehicles Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Electric Motors For IC Engine Vehicles Market Segmented?

The electric motors for ic engine vehicles industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Vehicle type

- Passenger cars

- Commercial vehicles

- Two wheeler

- Type

- AC motor

- DC motor

- Distribution channel

- OEM

- Aftermarket

- Geography

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Vehicle Type Insights

The passenger cars segment is estimated to witness significant growth during the forecast period.

The passenger cars segment is driven by consumer demand for comfort, safety, and advanced driver-assistance systems.

Modern vehicles integrate dozens of electric motors beyond the primary starter motors and alternators, powering features like window regulators, seat adjustments, and electronic parking brakes.

A significant trend is the adoption of 48-volt mild hybrid systems, which utilize an advanced integrated starter-generator to enhance fuel economy.

This push for efficiency also drives demand for precision motion control motors in steering and braking systems, including electronic stability control. Thermal management is critical, with electric water pumps and cooling fan motors becoming standard to optimize engine temperature.

Suppliers are focusing on compact, lightweight brushless DC motors that offer higher power density and lower noise, meeting refined market expectations.

The Passenger cars segment was valued at USD 564.9 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 60.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Electric Motors For IC Engine Vehicles Market Demand is Rising in APAC Get Free Sample

The geographic landscape is dominated by a massive manufacturing infrastructure and a substantial consumer base, particularly in the APAC region.

High vehicle production volumes ensure a constant demand for both standardized and cost-effective motor components, as well as high-performance hybrid architectures.

Regional export activity for automotive electrical parts, including starter motors and alternators, has surged by 8% as suppliers fill gaps in the global supply chain.

In contrast, other markets emphasize high-precision motors and the integration of advanced electronics for hybrid-capable engines.

This diversity requires manufacturers to offer a broad range of motor specifications, including AC induction motors and permanent magnet motors, to meet varied price points and performance needs.

The use of high-grade magnetic materials remains a key differentiator across all regions.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the global electric motors for ic engine vehicles market is increasingly focused on optimizing component-level performance to achieve system-wide efficiency gains. Improving fuel efficiency with electric ancillaries is a core objective, leading to intense evaluation of electric water pump vs mechanical pump efficiency.

- For instance, the electric motor for ic engine cooling fans is now designed with variable speed controls, unlike older fixed-speed units. The 48v mild hybrid integrated starter generator has become a pivotal technology for reducing emissions, with starter motor requirements for stop-start systems becoming more stringent.

- For powertrain applications, the brushless dc motor for power steering systems offers superior reliability, while the high-voltage motor for hybrid powertrain modules delivers necessary torque. This extends to precise components like the advanced actuator for electronic wastegate control and motor selection for active grille shutter systems.

- Inside the cabin, a dc motor design for power window regulators and a compact motor design for automated seat adjustment enhance user experience.

- Next-generation thermal management motor for turbocharged engines and electric supercharger motor power requirements are also key R&D areas, with some integrated designs showing a component count reduction of over 20% compared to legacy setups, simplifying assembly line operations and improving reliability for systems like regenerative braking motor for mild hybrids.

What are the key market drivers leading to the rise in the adoption of Electric Motors For IC Engine Vehicles Industry?

- The primary market driver is the ongoing electrification of ancillary components, which enhances both thermal and mechanical efficiency in vehicles.

- The comprehensive electrification of ancillary vehicle systems is a primary market driver, aimed at eliminating parasitic mechanical losses to improve fuel efficiency by up to 15%.

- Traditional designs with belt-driven components continuously drained engine power, but engineers are systematically replacing them with electrically driven alternatives offering precise, on-demand control.

- Electric water pumps, for example, can vary coolant flow independent of engine speed, ensuring optimal turbocharged engine cooling.

- This granular level of electrification, supported by innovations in waste heat energy recovery and active suspension actuators, creates sustained demand for specialized transmission oil pumps and variable valve timing actuators.

- The adoption of advanced electrical architectures provides the necessary power to support high-load consumers, enabling automakers to package engines more compactly and reduce emissions.

What are the market trends shaping the Electric Motors For IC Engine Vehicles Industry?

- A significant market trend is the accelerated integration of high-voltage motors within hybrid powertrains. This shift is driven by the increasing need for enhanced vehicle performance and efficiency.

- The market is undergoing a transformation driven by aggressive hybridization strategies, as manufacturers move beyond traditional architectures to deploy high-voltage systems. This trend is characterized by the proliferation of P2 hybrid architecture and P4 hybrid architecture modules, which integrate powerful high-voltage hairpin motors directly into the powertrain.

- These systems enable efficient torque vectoring capabilities and regenerative braking systems, extending the life of the combustion engine while meeting carbon reduction targets. The shift requires a robust supply chain for motors that withstand high thermal stress.

- The adoption of advanced round-wire windings contributes to a 10% increase in power density over previous designs, enabling performance enhancements in new energy vehicle platforms. The transition toward electrified ancillary components, including high-voltage efan solutions, is a critical enabler for next-generation vehicles.

What challenges does the Electric Motors For IC Engine Vehicles Industry face during its growth?

- A key challenge impacting industry growth involves the financial strain of regulatory compliance costs and associated investment dilemmas.

- The market is navigating a landscape of declining long-term volumes coupled with increasing short-term technical demands. As governments enforce stricter emission standards, manufacturers must install highly sophisticated electric actuators, pumps, and cooling fan motors. This forces suppliers to invest heavily in R&D for a technology stack with a finite commercial lifespan, leading to a diminishing return on investment.

- The cost of compliance rises while the addressable market contracts, with re-engineering efforts to meet extended durability compliance requirements increasing validation expenses by over 20%. This financial strain is exemplified by the need to upgrade motors for exhaust gas recirculation systems and electronic wastegates to meet new lifecycle mandates, diverting capital from future-focused technologies.

Exclusive Technavio Analysis on Customer Landscape

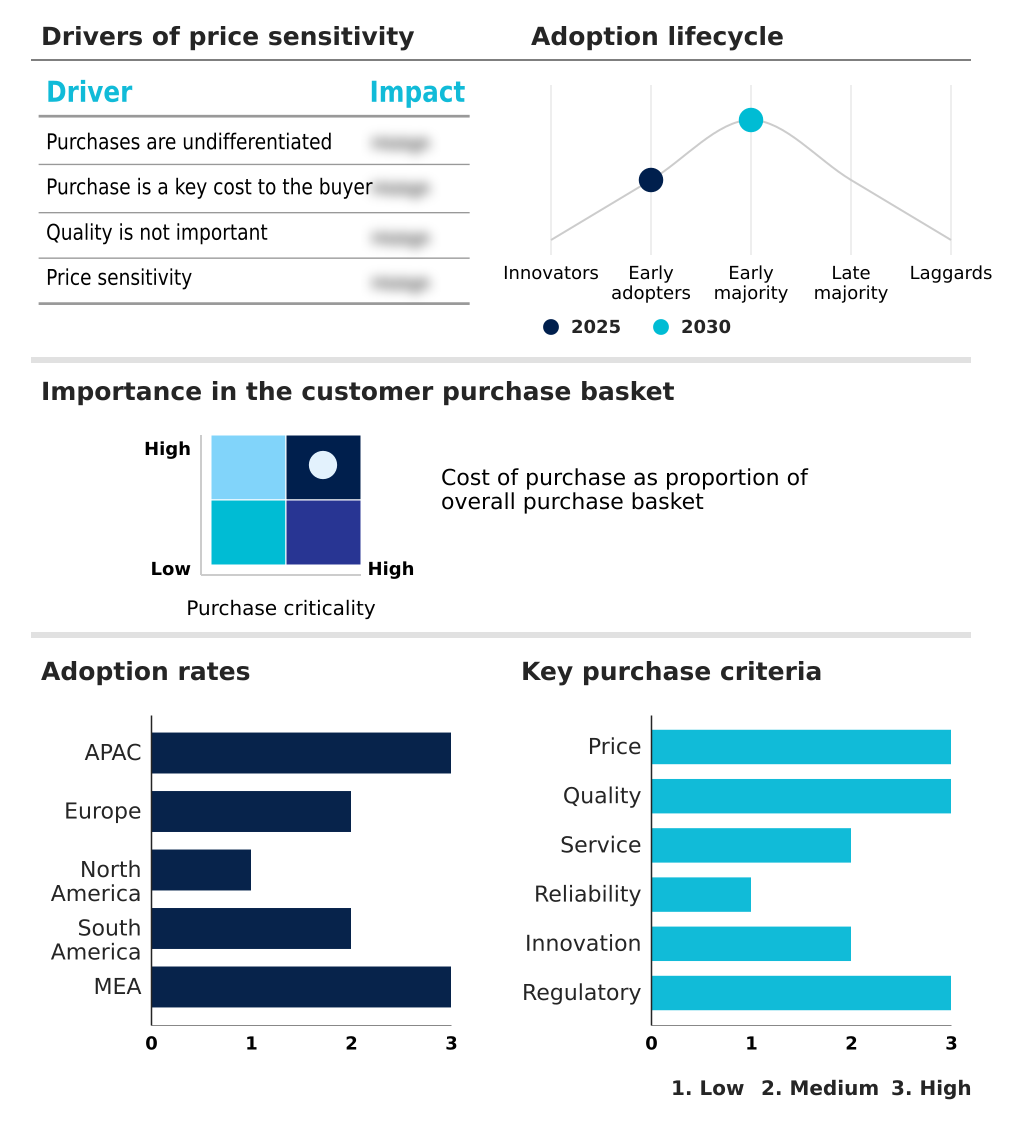

The electric motors for ic engine vehicles market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the electric motors for ic engine vehicles market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Electric Motors For IC Engine Vehicles Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, electric motors for ic engine vehicles market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AMETEK Inc. - Key offerings include specialized electric motors, starter-generators, and auxiliary drives, which are pivotal for enhancing the efficiency and functionality of internal combustion engine platforms.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AMETEK Inc.

- Arc Systems Inc.

- BorgWarner Inc.

- Brose SE and Co. KG

- Continental AG

- DENSO Corp.

- Emerson Electric Co.

- Hitachi Ltd.

- Johnson Electric Holdings Ltd.

- Marelli Holdings Co. Ltd.

- Mazda Motor Corp.

- Mitsuba Corp.

- Mitsubishi Electric Corp.

- Nidec Corp.

- Regal Rexnord Corp.

- Robert Bosch GmbH

- Valeo SA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Electric motors for ic engine vehicles market

- In August 2025, BorgWarner Inc. commenced production of its 400V High-Voltage Hairpin (HVH) motors for a major Chinese New Energy Vehicle supplier, targeting high-performance hybrid platforms.

- In September 2025, the European Commission published implementing regulations for Euro 7 emission standards, mandating advanced on-board emissions monitoring and extending durability requirements for vehicle components.

- In October 2025, Nidec Corp. executed a strategic reorganization of its Automotive Motor and Electronic Control unit, establishing a new Business Strategy and Sales Division to accelerate motor solution development.

- In May 2025, Robert Bosch GmbH introduced an enhanced line of AC induction motors designed for the thermal management systems of large-scale commercial diesel vehicles, improving operational reliability.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Electric Motors For IC Engine Vehicles Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 285 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6% |

| Market growth 2026-2030 | USD 266.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.5% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is navigating a complex trajectory defined by sustained demand for auxiliary electrification and increasingly sophisticated automotive systems. Despite the industry's shift toward full electrification, the internal combustion engine sector continues to drive substantial volume for specialized electric motors.

- Growth is primarily fueled by the replacement of traditional mechanical components like power steering pumps with electrically driven alternatives, such as brushless DC motors, which reduce parasitic engine load and improve fuel efficiency. In some applications, this transition has reduced system energy consumption by over 15%.

- A key boardroom-level decision revolves around R&D investment, balancing the need to support legacy ICE architectures with the pivot to hybrid and EV platforms. Technologically, the market is witnessing a transition to advanced solutions like the integrated starter-generator and thermal management systems that use electric coolant pumps.

- This evolution requires suppliers to innovate in areas such as high-torque micro-motors and mechatronic components to maintain a competitive edge, ensuring that both powertrain hybridization and comfort-related functions are supported with reliable, high-performance units.

What are the Key Data Covered in this Electric Motors For IC Engine Vehicles Market Research and Growth Report?

-

What is the expected growth of the Electric Motors For IC Engine Vehicles Market between 2026 and 2030?

-

USD 266.5 million, at a CAGR of 6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Vehicle Type (Passenger cars, Commercial vehicles, and Two wheeler), Type (AC motor, and DC motor), Distribution Channel (OEM, and Aftermarket) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Electrification of ancillary components for thermal and mechanical efficiency, Regulatory compliance costs and investment dilemmas

-

-

Who are the major players in the Electric Motors For IC Engine Vehicles Market?

-

AMETEK Inc., Arc Systems Inc., BorgWarner Inc., Brose SE and Co. KG, Continental AG, DENSO Corp., Emerson Electric Co., Hitachi Ltd., Johnson Electric Holdings Ltd., Marelli Holdings Co. Ltd., Mazda Motor Corp., Mitsuba Corp., Mitsubishi Electric Corp., Nidec Corp., Regal Rexnord Corp., Robert Bosch GmbH and Valeo SA

-

Market Research Insights

- The market for electric motors in internal combustion engine vehicles is defined by a push for greater efficiency and system integration. The electrification of ancillary vehicle systems is a primary driver, with advanced electric water pumps demonstrating a 10% improvement in thermal management over traditional belt-driven components.

- This shift away from reliance on the engine crankshaft load reduces parasitic mechanical losses and supports powertrain hybridization. The adoption of 48-volt mild hybrid systems further propels demand for high-performance motors capable of supporting stop-start events and regenerative braking.

- This evolution creates a complex environment where vehicle platform integration is critical, as automakers require motors that are both compact and powerful. Consequently, suppliers are innovating to provide solutions that enhance engine performance, with some integrated starter-generator units improving fuel efficiency by up to 15%.

We can help! Our analysts can customize this electric motors for ic engine vehicles market research report to meet your requirements.

RIA -

RIA -