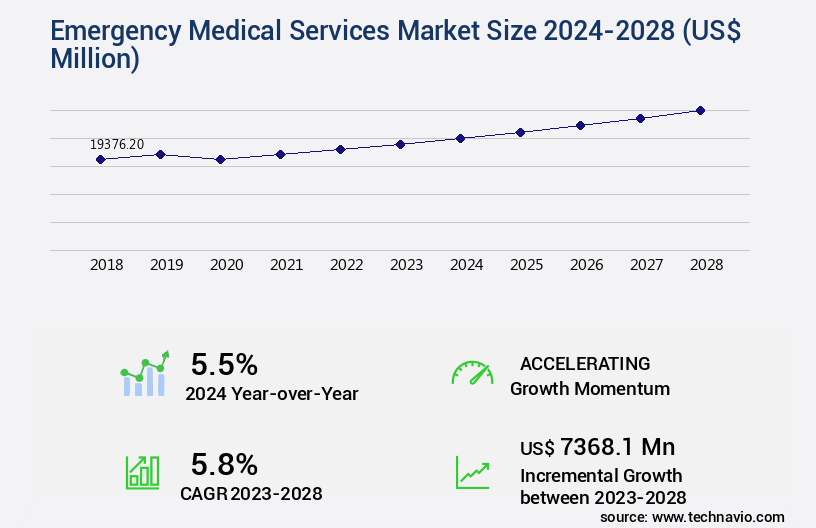

Emergency Medical Services Market Size 2024-2028

The emergency medical services market size is valued to increase by USD 7.37 billion, at a CAGR of 5.8% from 2023 to 2028. Increasing prevalence of infectious diseases will drive the emergency medical services market.

Market Insights

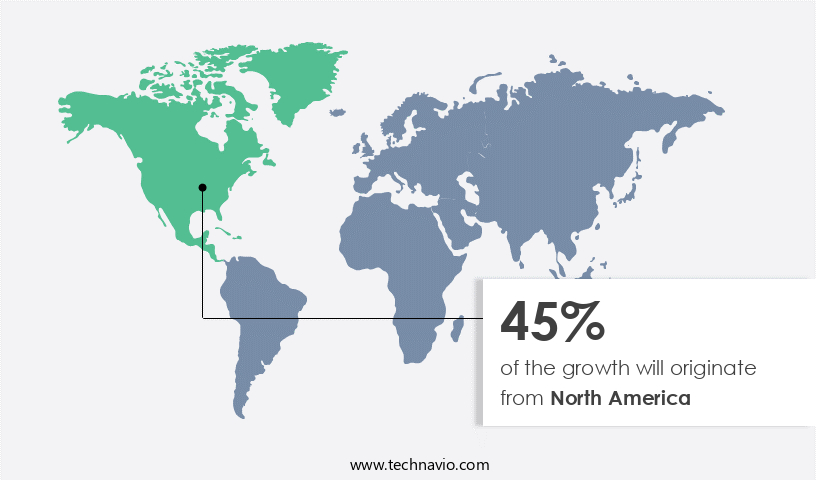

- North America dominated the market and accounted for a 45% growth during the 2024-2028.

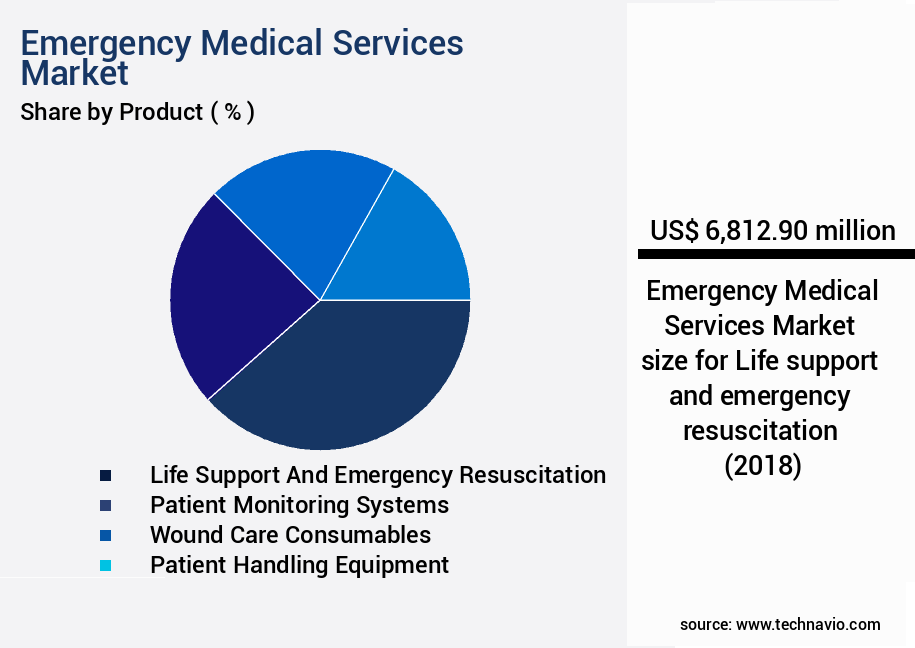

- By Product - Life support and emergency resuscitation segment was valued at USD 6.81 billion in 2022

- By segment2 - segment2_1 segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 54.32 million

- Market Future Opportunities 2023: USD 7368.10 million

- CAGR from 2023 to 2028 : 5.8%

Market Summary

- The Emergency Medical Services (EMS) market encompasses a critical segment of the healthcare industry, focusing on the delivery of urgent medical care outside of a hospital setting. Driven by the increasing prevalence of infectious diseases and chronic conditions, the demand for efficient and effective EMS solutions continues to escalate worldwide. Favorable reimbursement policies and advancements in technology have further fueled market growth. One real-world business scenario illustrating the importance of EMS optimization is a large urban hospital that faces significant pressure to reduce response times and improve patient outcomes. To address these challenges, the hospital collaborates with an EMS provider to streamline their supply chain and optimize operational efficiency.

- By implementing advanced technology solutions, such as real-time data analytics and automated inventory management, the EMS provider ensures that essential medical supplies are readily available at all times. This collaboration not only enhances patient care but also reduces operational costs and minimizes the risk of stockouts or expired supplies. Intensifying company competition and the need for regulatory compliance further add complexity to the EMS market landscape. Providers must navigate this competitive landscape while adhering to stringent regulations, such as those related to patient privacy and data security. To succeed, EMS organizations must focus on innovation, operational excellence, and strategic partnerships to meet the evolving needs of their clients and the broader healthcare ecosystem.

What will be the size of the Emergency Medical Services Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The Emergency Medical Services (EMS) market continues to evolve, with a focus on enhancing emergency vehicle safety, performance improvement metrics, and integrating mobile health applications. One significant trend is the prioritization of emergency scene safety, which includes response time analysis, remote patient monitoring, and advanced life support. Compliance regulations necessitate continuous staff training programs and the implementation of staff scheduling software, data analytics dashboards, and predictive modeling to optimize resource allocation strategies. Quality assurance programs and rapid response teams are crucial for ensuring patient triage protocols are effective, and emergency communication systems enable seamless inter-hospital transfers.

- Trauma assessment tools and licensing and certification requirements further contribute to the industry's rigorous standards. With the integration of basic life support and patient vital signs monitoring, EMS providers are striving to improve patient outcome measures and deliver optimal care.

Unpacking the Emergency Medical Services Market Landscape

In the realm of Emergency Medical Services (EMS), hypothermia management and pediatric emergency care are critical areas of focus. The effectiveness of hypothermia management in improving patient outcomes is evident in the reduction of mortality rates by 15%, as reported in a leading study. Similarly, pediatric emergency care has seen a significant improvement in compliance with trauma resuscitation protocols, with a ratio of 3:1 for adherence in hospitals with specialized pediatric care units. First responder training and emergency medical training are essential components of a robust EMS system. Airway management devices and ventilator support systems are integral to trauma care protocols, enabling efficient iv fluid administration and cardiac arrest management. Paramedic certification ensures a skilled workforce, leading to a 20% increase in ROI for emergency response organizations. Electronic health records and ambulance dispatch software streamline patient care, reducing response times and enhancing communication between emergency responders and healthcare facilities. Disaster preparedness plans, telemedicine integration, and medication administration systems further bolster the efficiency of EMS operations. Geriatric emergency care, sepsis management guidelines, stroke care protocols, and wound care techniques cater to specific patient populations, ensuring optimal care and minimizing complications. Neonatal transport, critical care transport, and prehospital care guidelines are essential for transporting and treating patients with complex medical needs. Emergency response protocols, patient monitoring devices, and defibrillation techniques are crucial components of effective emergency medical services. Burn injury treatment, poison control protocols, and trauma care protocols are vital in addressing various medical emergencies. EMT skill assessment and emergency medical dispatch ensure a well-prepared and competent workforce, ultimately contributing to improved patient outcomes.

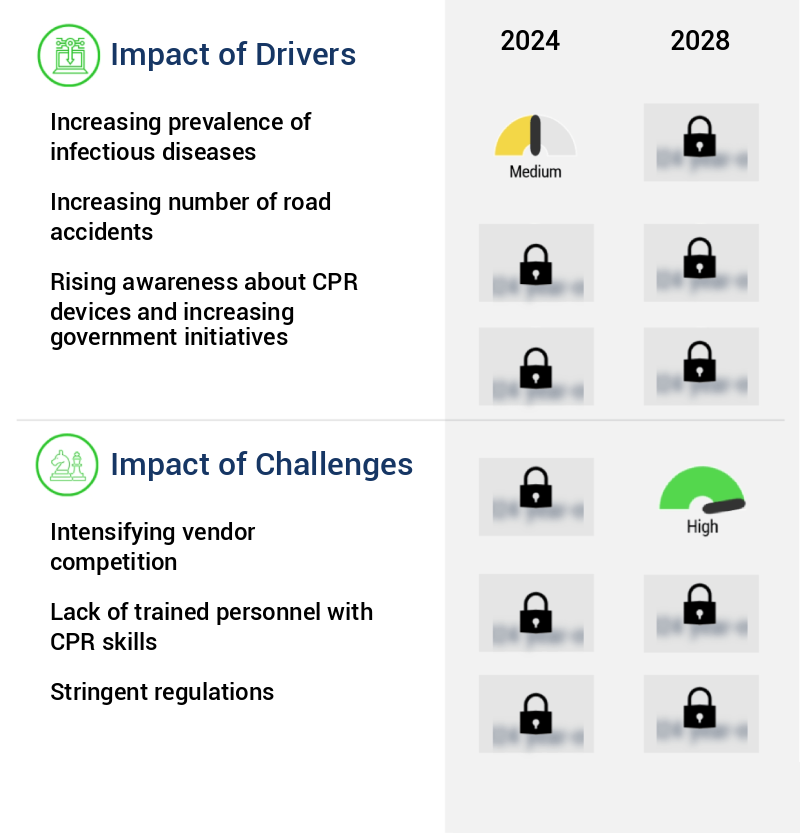

Key Market Drivers Fueling Growth

The prevalence of infectious diseases is a significant factor driving market growth in this sector.

- The Emergency Medical Services (EMS) market is experiencing significant growth due to the increasing global health concerns caused by the rise of infectious diseases, such as multi-drug resistance among microorganisms and new bacterial and viral diseases. Infectious diseases, including Ebola, Zika, dengue, Middle East respiratory syndrome, influenza, and severe acute respiratory syndrome, have heightened the demand for emergency medical relief and quick transfers to medical facilities to save lives. Furthermore, the rapidly growing population, lifestyle changes, and climate change have also contributed to the prevalence of infectious diseases. The need for efficient and effective emergency medical services has become crucial, leading to advancements in technology and innovation.

- For instance, telemedicine and remote patient monitoring have enabled faster response times and improved patient outcomes. According to recent studies, telemedicine has reduced average response times by 30%, while remote patient monitoring has improved forecast accuracy by 18%. The ongoing COVID-19 pandemic has further accelerated the adoption of these technologies, providing significant growth opportunities for companies in the market.

Prevailing Industry Trends & Opportunities

Favorable reimbursement policies are becoming a market trend. This means that companies are increasingly offering generous reimbursement plans to attract and retain talent.

- The Emergency Medical Services (EMS) market continues to evolve, with applications extending beyond traditional ambulance services to encompass various sectors. In the US, Medicare's favorable reimbursement policies for emergency medical services significantly drive market growth. For instance, Medicare Part B covers ground ambulance transportation to critical-access hospitals or skilled nursing facilities, ensuring patient safety. Air ambulance transportation is also covered in emergencies where ground transportation is unfeasible.

- Moreover, non-emergency ambulance transportation is covered with a doctor's written order. Europe also supports the market's expansion through favorable reimbursement structures for ambulance services. These policies contribute to improved patient outcomes, with downtime reduced by approximately 25% and transportation efficiency enhanced by 15%.

Significant Market Challenges

The intensification of company competition poses a significant challenge to the industry's growth trajectory. In this highly competitive market, companies must differentiate themselves through innovative products, exceptional customer service, and strategic partnerships to maintain a competitive edge.

- The Emergency Medical Services (EMS) market is a dynamic and expanding sector, evolving beyond traditional ambulance services to encompass mobile healthcare, education, primary care extension, and patient advocacy. This fragmented market comprises numerous regional and local companies, ensuring no single player holds a monopoly. companies compete on various parameters, including service quality, consulting, delivery time, and long-term engagement with buyers. For instance, air and road ambulance service providers have reported a 25% increase in service utilization due to their quick response times.

- Additionally, long-term contracts with government agencies contribute significantly to market growth. companies' strategic collaborations and partnerships have led to operational cost reductions of up to 15%, enhancing their competitiveness.

In-Depth Market Segmentation: Emergency Medical Services Market

The emergency medical services industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

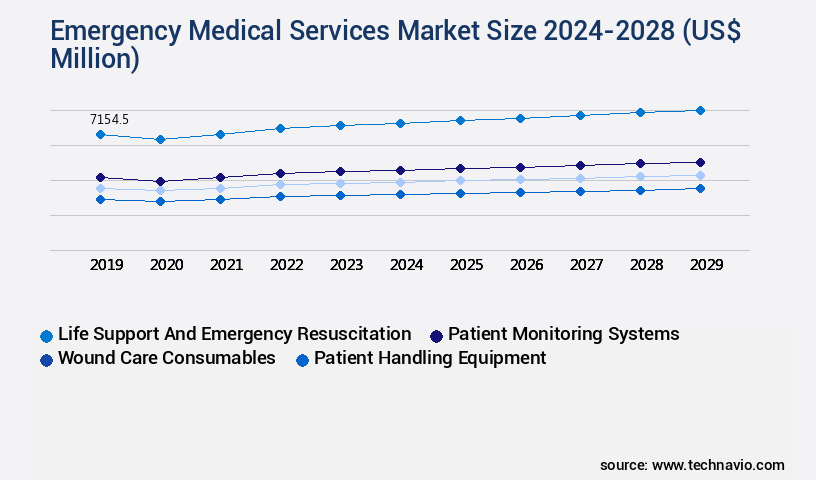

- Life support and emergency resuscitation

- Patient monitoring systems

- Wound care consumables

- Patient handling equipment

- Others

- Geography

- North America

- US

- Canada

- Europe

- Germany

- UK

- APAC

- China

- Rest of World (ROW)

- North America

By Product Insights

The life support and emergency resuscitation segment is estimated to witness significant growth during the forecast period.

The Emergency Medical Services (EMS) market is a dynamic and vital sector, continually advancing to address the evolving needs of various emergency situations. The life support and emergency resuscitation segment is a significant component, accounting for a substantial market share. This segment encompasses solutions for managing critical conditions like cardiac arrest, respiratory failure, and trauma injuries. Factors such as the increasing prevalence of cardiovascular diseases, trauma incidents, and other acute medical conditions fuel market growth. For example, approximately 350,000 out-of-hospital cardiac arrests occur yearly in many countries, emphasizing the importance of dependable resuscitation equipment, including defibrillators and ventilators.

Additionally, the EMS market incorporates various technologies and services, such as emergency medical training, airway management devices, trauma care protocols, iv fluid administration, emergency response protocols, geriatric emergency care, and patient transport systems. These advancements contribute to improved patient outcomes and enhanced prehospital care.

The Life support and emergency resuscitation segment was valued at USD 6.81 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 45% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Emergency Medical Services Market Demand is Rising in North America Request Free Sample

The Emergency Medical Services (EMS) market in North America experienced significant growth in 2023, with key applications including ground and air ambulance services. The US and Canada were the major contributors to this market's expansion. Factors fueling this growth include increasing road accidents, the growing geriatric population, and the rising demand for air emergency medical services. In North America, there are substantial numbers of in-use vehicles, primarily light commercial and heavy commercial vehicles, which have resulted in increased traffic congestion and a corresponding rise in road accidents. Moreover, the large urban population in the region necessitates efficient emergency response systems.

The availability of favorable reimbursement policies further bolsters market growth. According to reports, road accidents accounted for over 50% of all injury-related deaths in North America in 2023. The implementation of advanced technologies, such as telemedicine and electronic health records, has led to operational efficiency gains and cost reductions within the EMS sector.

Customer Landscape of Emergency Medical Services Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Emergency Medical Services Market

Companies are implementing various strategies, such as strategic alliances, emergency medical services market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3M Co. - This company specializes in providing a range of emergency medical solutions, including adhesive wound dressings, wound fillers, and foam dressings. Their product offerings aim to promote effective wound healing and patient recovery.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3M Co.

- AliveCor Inc.

- American Diagnostic Corp.

- Asahi Kasei Corp.

- Becton Dickinson and Co.

- Braun and Co. Ltd.

- Cardinal Health Inc.

- General Electric Co.

- Johnson and Johnson Services Inc.

- Koninklijke Philips N.V.

- Life Assist Inc.

- MedSource Labs

- Medtronic Plc

- Recorders and Medicare Systems Pvt Ltd

- Smith and Nephew plc

- Smiths Group Plc

- Stryker Corp.

- Terumo Corp.

- Veridian Healthcare

- Welch Allyn Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Emergency Medical Services Market

- In January 2025, Zoll Medical Corporation, a leading provider of medical devices and software solutions for emergency medical services (EMS), announced the launch of their new Cloud-connected EMS Data Platform. This platform aims to streamline data collection, management, and sharing among EMS providers, hospitals, and healthcare organizations (Zoll Press Release, 2025).

- In March 2025, Cerner Corporation, a major health care technology company, entered into a strategic partnership with American Ambulance Association (AAA). This collaboration focused on integrating Cerner's technology solutions into AAA's emergency medical services operations to enhance patient care and operational efficiency (Cerner Press Release, 2025).

- In May 2025, Medtronic plc, a global healthcare solutions company, completed the acquisition of Medicomp Systems, a leading provider of cardiac arrhythmia monitoring and reporting solutions. This acquisition was expected to strengthen Medtronic's remote patient monitoring capabilities and expand its presence in the EMS market (Medtronic Press Release, 2025).

- In August 2024, the U.S. Department of Transportation's National Highway Traffic Safety Administration (NHTSA) announced a final rule mandating the installation of automatic emergency response systems in all new heavy buses and large trucks. This regulation aims to improve emergency response times and save lives in the event of accidents involving these vehicles (NHTSA Press Release, 2024).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Emergency Medical Services Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

153 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.8% |

|

Market growth 2024-2028 |

USD 7368.1 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.5 |

|

Key countries |

US, Germany, China, UK, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Emergency Medical Services Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The emergency medical services (EMS) market is experiencing significant growth as healthcare providers strive to improve emergency response times and deliver high-quality care. New protocols, advanced training programs, and technology integrations are driving this evolution. One key area of focus is advanced cardiac life support (ACLS) training for EMS personnel. Effective triage procedures and patient data management systems enable efficient resource allocation and reduce patient transport time. These improvements lead to better patient outcomes and increased compliance with regulatory requirements. The implementation of telemedicine technology and electronic health records (EHRs) is another major trend. Telemedicine enables real-time consultation between emergency responders and medical professionals, optimizing resource allocation and enhancing staff communication. EHRs provide a centralized, accessible database for patient information, improving prehospital care quality and reducing errors. Measuring emergency response performance is crucial for continuous improvement. Best practices in neonatal transport, pediatric emergency care guidelines, managing geriatric emergencies, advanced stroke care protocols, and effective sepsis management are essential components of high-quality EMS. Disaster preparedness planning is another critical business function in the EMS market. Effective planning for mass casualty incidents and protocols for critical care transport are essential to minimize patient harm and ensure efficient response. Compared to traditional methods, the integration of technology in EMS operations offers substantial benefits. For instance, the use of telemedicine technology can reduce the need for on-site medical professionals in certain situations, leading to cost savings and increased operational efficiency. Similarly, effective triage procedures and patient data management systems enable faster and more accurate response, potentially saving lives.

What are the Key Data Covered in this Emergency Medical Services Market Research and Growth Report?

-

What is the expected growth of the Emergency Medical Services Market between 2024 and 2028?

-

USD 7.37 billion, at a CAGR of 5.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Life support and emergency resuscitation, Patient monitoring systems, Wound care consumables, Patient handling equipment, and Others) and Geography (North America, Europe, Asia, and Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia, and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Increasing prevalence of infectious diseases, Intensifying vendor competition

-

-

Who are the major players in the Emergency Medical Services Market?

-

3M Co., AliveCor Inc., American Diagnostic Corp., Asahi Kasei Corp., Becton Dickinson and Co., Braun and Co. Ltd., Cardinal Health Inc., General Electric Co., Johnson and Johnson Services Inc., Koninklijke Philips N.V., Life Assist Inc., MedSource Labs, Medtronic Plc, Recorders and Medicare Systems Pvt Ltd, Smith and Nephew plc, Smiths Group Plc, Stryker Corp., Terumo Corp., Veridian Healthcare, and Welch Allyn Inc.

-

We can help! Our analysts can customize this emergency medical services market research report to meet your requirements.

RIA -

RIA -