Electromagnetic Interference (EMI) Shielding Market Size 2024-2028

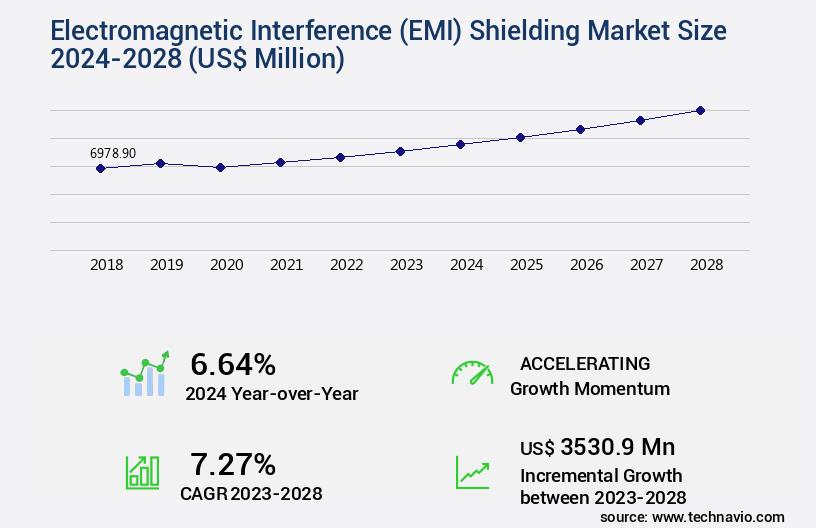

The electromagnetic interference (emi) shielding market size is valued to increase by USD 3.53 billion, at a CAGR of 7.27% from 2023 to 2028. Growth in global electronics production will drive the electromagnetic interference (emi) shielding market.

Market Insights

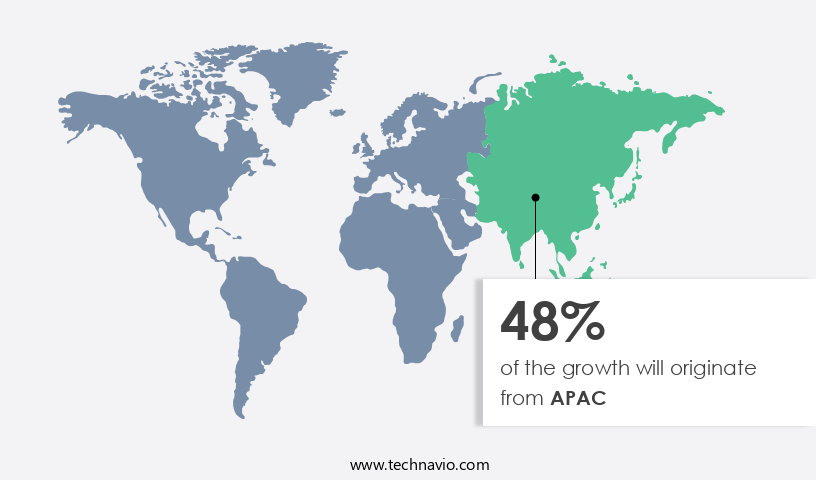

- APAC dominated the market and accounted for a 48% growth during the 2024-2028.

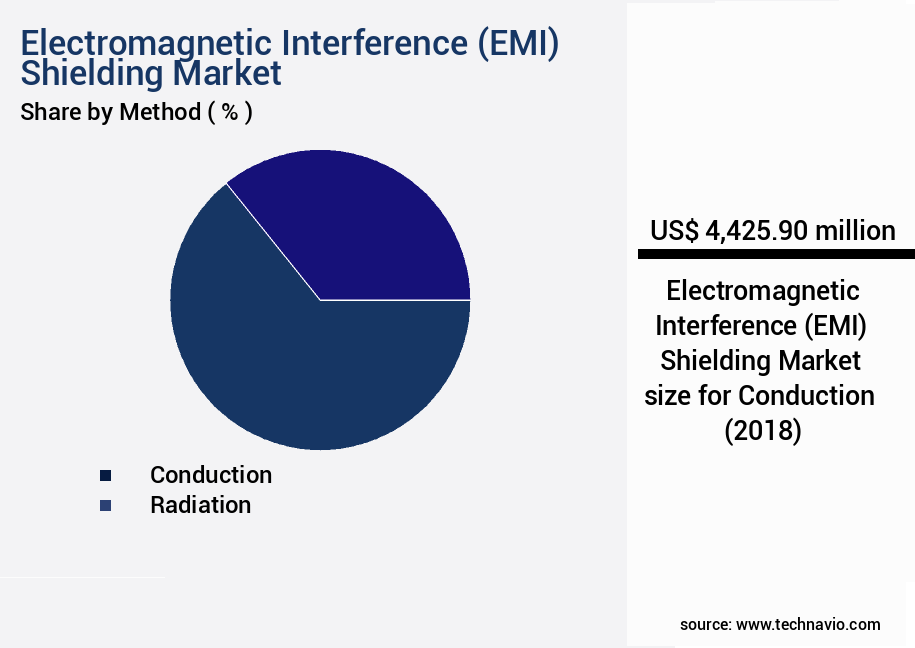

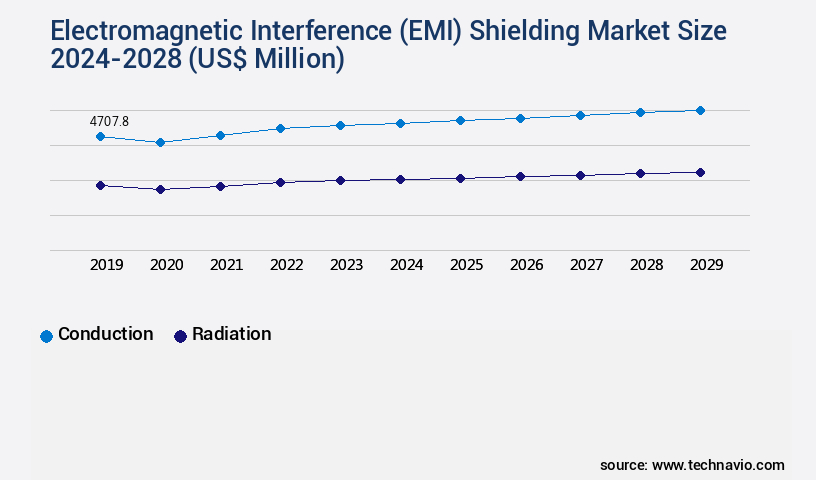

- By Method - Conduction segment was valued at USD 4.43 billion in 2022

- By End-user - Automotive segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 70.93 million

- Market Future Opportunities 2023: USD 3530.90 million

- CAGR from 2023 to 2028 : 7.27%

Market Summary

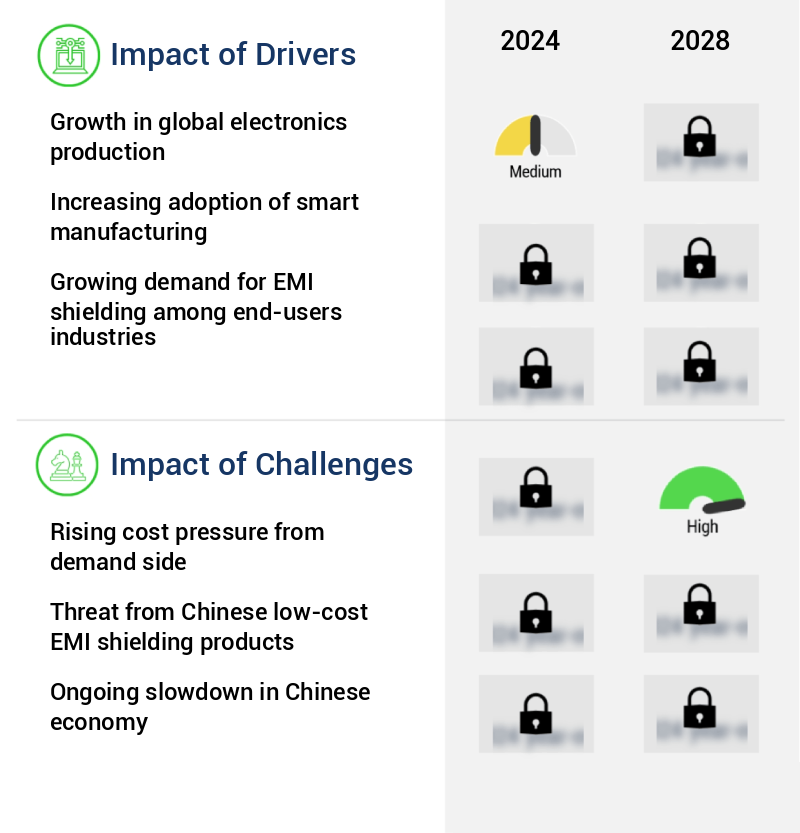

- The market is experiencing significant growth due to the increasing production of electronics on a global scale. With the proliferation of advanced technologies such as 5G, Internet of Things (IoT), and electric vehicles, the demand for effective EMI shielding solutions is escalating. EMI shielding is crucial to ensure the reliable operation of electronic devices by preventing electromagnetic interference from external sources and protecting against electromagnetic emissions. One of the key drivers for the EMI shielding market is the rising cost pressure from the demand side. As electronic devices become more complex and sophisticated, the need for advanced EMI shielding solutions to maintain operational efficiency and ensure compliance with regulatory standards becomes increasingly important.

- A prime example of this can be observed in the automotive industry, where the integration of advanced driver assistance systems (ADAS) and electric powertrains necessitates robust EMI shielding to ensure optimal performance and safety. Another trend in the EMI shielding market is the growing demand for package-level shielding. As electronic components become smaller and more densely packed, traditional shielding methods may no longer be sufficient. Package-level shielding offers improved protection against EMI and can help to minimize the risk of signal degradation and data loss. This is particularly important in applications where data integrity is critical, such as in telecommunications, aerospace, and defense.

- Despite these opportunities, the EMI shielding market also faces challenges. The development of cost-effective, lightweight, and flexible shielding materials remains an ongoing challenge. Additionally, the complex and evolving regulatory landscape can make it difficult for manufacturers to keep up with the latest requirements. However, with continued innovation and investment in research and development, the EMI shielding market is poised to meet the growing demand for reliable and effective shielding solutions.

What will be the size of the Electromagnetic Interference (EMI) Shielding Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, driven by the increasing demand for electromagnetic compatibility (EMC) in various industries. According to recent research, the EMI shielding materials market is projected to grow by 15% in the next five years, reaching a significant market share. This growth can be attributed to the rising adoption of advanced technologies, such as 5G networks and electric vehicles, which generate high-frequency interference and require robust shielding solutions. Shielding material selection plays a crucial role in EMI shielding. Conductive coatings, shielding enclosures, and EMI gaskets are popular choices for reducing electromagnetic interference.

- High-frequency interference, RF interference, and low-frequency interference all require different shielding techniques and performance levels. EMI shielding techniques include electromagnetic field modeling, EMC standards compliance, and EMI filter components. EMI shielding performance is essential for various applications, including wireless signal shielding, electromagnetic pulse shielding, and magnetic field shielding. EMI/RFI suppression is a critical aspect of signal integrity, ensuring the reliable transmission of data in various industries, such as telecommunications, automotive, and aerospace. EMI measurement equipment and EMC compliance solutions are essential tools for ensuring effective EMI shielding. These solutions help in identifying potential sources of interference and evaluating shielding effectiveness.

- By implementing these solutions, companies can minimize the risk of costly product recalls and ensure regulatory compliance. In summary, the EMI Shielding Market is a growing and evolving sector, driven by the increasing demand for electromagnetic compatibility in various industries. The selection of appropriate shielding materials, techniques, and equipment is crucial for ensuring effective EMI shielding and maintaining signal integrity.

Unpacking the Electromagnetic Interference (EMI) Shielding Market Landscape

Electromagnetic Interference (EMI) shielding is a critical component in ensuring Electromagnetic Compatibility (EMC) in various industries. Two primary methods for EMI shielding are metallic shielding and conductive polymers. Metallic shielding, with its magnetic shielding effectiveness up to 100 dB, offers superior attenuation of electromagnetic fields. In contrast, conductive polymers shielding, with its flexibility and lightweight properties, presents a viable alternative for wireless devices and shielded rooms. EMI absorption materials, high-frequency shielding, and EMI shielding fabrics further enhance shielding effectiveness, particularly in near-field and far-field environments. EMI/RFI filters, shielding effectiveness testing, and shielding effectiveness measurement are essential for compliance with EMI shielding standards. Conformal coating shielding and EMI gasket materials ensure effective shielding in complex designs. Low-frequency shielding, electromagnetic pulse protection, and shielded cables cater to specific industry requirements. EMI shielding design and simulation, anechoic chamber testing, and RF shielding enclosures facilitate efficient EMI shielding implementation. Overall, EMI shielding plays a pivotal role in reducing electromagnetic interference and maintaining electromagnetic compatibility in diverse applications.

Key Market Drivers Fueling Growth

The expansion of global electronics production serves as the primary catalyst for market growth.

- The market is experiencing significant growth due to the increasing demand for electronic products and advanced electronic equipment across various sectors. In 2023, the global electronics industry production reached an all-time high and is projected to continue expanding. The surge in big data analytics driven by the Internet of Things (IoT) technology further fuels the market's growth. Additionally, the automotive industry's transition towards autonomous and electric vehicles contributes to the increasing percentage of electronic equipment in vehicles. Moreover, the rising adoption of smartphones in emerging economies, such as India, due to affordable Internet charges, signifies a promising future for the EMI Shielding Market.

- These trends underscore the market's evolving nature and its crucial role in ensuring the optimal performance and reliability of electronic devices.

Prevailing Industry Trends & Opportunities

Package-level Electromagnetic Interference (EMI) shielding is an emerging market trend due to increasing demand for effective shielding solutions.

- The market is undergoing a significant transformation, with a notable trend being the shift from board-level EMI shielding to package-level EMI shielding. This transition is driven by the increasing demand for reliable shielding and adhesion performance in the face of high-populated PCBs in modern electronic equipment. Package-level EMI shielding offers several advantages, including smaller, thinner, and lighter designs compared to board-level EMI shielding.

- This shift is essential as customers seek additional functionalities and enhanced performance from their electronic devices. The growing complexity of PCBs is fueling the demand for reliable EMI shielding solutions, making package-level EMI shielding an increasingly popular choice. This transition not only enhances the electronic designs but also reduces downtime and improves overall performance.

Significant Market Challenges

The increasing cost pressure resulting from heightened demand represents a significant challenge to the industry's growth trajectory.

- The market continues to evolve, responding to the diverse needs of various sectors, including automotive, telecommunications, and healthcare. EMI shielding manufacturers face significant cost pressures due to the increasing demand for customized, flexible solutions from consumers. Adhering to stringent environmental and safety regulations adds to these costs, necessitating innovative approaches to maintain quality and competitiveness. For instance, a leading automotive manufacturer reported a 25% reduction in downtime by implementing advanced EMI shielding technologies. Similarly, a telecommunications company achieved a 20% improvement in signal quality through the adoption of optimized EMI shielding solutions.

- Addressing these challenges while catering to evolving customer demands will remain a critical focus for EMI shielding manufacturers. The electronics manufacturing industry's shift towards China post-2008 financial crisis further complicates the landscape, necessitating agile and cost-effective production strategies.

In-Depth Market Segmentation: Electromagnetic Interference (EMI) Shielding Market

The electromagnetic interference (emi) shielding industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Method

- Conduction

- Radiation

- End-user

- Automotive

- Consumer electronics

- Aerospace and defense

- Healthcare

- IT and telecom

- Geography

- North America

- US

- Europe

- Germany

- APAC

- China

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Method Insights

The conduction segment is estimated to witness significant growth during the forecast period.

Conduction EMI shielding is a critical technique in the market, employing conductive materials like copper, aluminum, and coatings to absorb and ground EMI through physical contact. This method's primary advantage lies in its ability to create a continuous path to ground, thereby preventing EMI from disrupting electronic devices' functionality, especially against low-frequency interference. An illustrative application of conduction shielding is the utilization of conductive gaskets around electronic device casings, ensuring effective grounding of any EMI that penetrates through joints or openings, thereby preserving the performance and integrity of sensitive electronic equipment.

The EMI shielding market continues to evolve, with advancements in materials like conductive polymers, EMI absorption materials, and non-metallic shielding, offering diverse solutions for various industries and applications.

The Conduction segment was valued at USD 4.43 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 48% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Electromagnetic Interference (EMI) Shielding Market Demand is Rising in APAC Request Free Sample

The market is experiencing significant growth, driven by the increasing demand for advanced electronic devices in various industries. In particular, the Asia Pacific (APAC) region, which includes major electronics producers such as China, Japan, India, Indonesia, and South Korea, is expected to lead the market's expansion. China, as the world's largest consumer, producer, and exporter of consumer electronics in 2023, holds a pivotal role in this growth. The region's strong electronics production setup and the presence of electronic manufacturing services are key factors fueling the demand for EMI shielding products. For instance, prominent electronic manufacturing service providers, like Foxconn Electronics Inc., are based in APAC.

The region's EMI shielding market is projected to grow at a faster rate than the developed regions, such as North America and Europe, due to the increasing focus on operational efficiency and cost reduction in electronics manufacturing. The market's growth is also driven by the need for compliance with stringent EMI regulations. According to a study, the APAC EMI shielding market is projected to grow at a Compound Annual Growth Rate (CAGR) of over 8% between 2023 and 2028.

Customer Landscape of Electromagnetic Interference (EMI) Shielding Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Electromagnetic Interference (EMI) Shielding Market

Companies are implementing various strategies, such as strategic alliances, electromagnetic interference (emi) shielding market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3M Co. - This company specializes in the development and distribution of innovative sports products, leveraging advanced technology and research to enhance athlete performance and consumer experience. Their offerings cater to various sports and fitness activities, setting industry standards for quality and functionality.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3M Co.

- Changzhou Pioneer Electronic Co. Ltd.

- Cybershield Inc.

- DuPont de Nemours Inc.

- EDOGAWA GOSEI CO. LTD.

- EIS Legacy LLC

- ESCO Technologies Inc.

- HEICO Corp.

- Henkel AG and Co. KGaA

- Integrated Polymer Solutions

- LG Chem Ltd.

- MAJR Products Corp.

- Miller Waste Mills Inc.

- NITTO KOGYO CORP.

- Nolato AB

- Omega Shielding Products

- Parker Hannifin Corp.

- PPG Industries Inc.

- Schaffner Group

- Tech Etch Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Electromagnetic Interference (EMI) Shielding Market

- In August 2024, TE Connectivity, a leading technology and manufacturing company, announced the launch of its new line of EMI shielding gaskets, designed to provide enhanced protection against electromagnetic interference for various industries, including automotive and telecommunications (TE Connectivity Press Release, 2024).

- In November 2024, Purdue University and 3M collaborated on a research project to develop advanced EMI shielding materials using nanotechnology, aiming to improve the performance and reduce the weight of current shielding solutions (Purdue University News, 2024).

- In March 2025, Honeywell International acquired Metallic Solutions, a leading provider of conductive elastomer materials for EMI shielding, expanding Honeywell's portfolio and strengthening its position in the EMI shielding market (Honeywell Press Release, 2025).

- In May 2025, the European Union's Radio Equipment and Telecommunications Terminal Equipment Directive (R&TTE) was updated to include stricter EMI shielding requirements, effective from September 2025, driving demand for advanced EMI shielding solutions (European Commission, 2025).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Electromagnetic Interference (EMI) Shielding Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

179 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.27% |

|

Market growth 2024-2028 |

USD 3530.9 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.64 |

|

Key countries |

US, China, Japan, Germany, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Electromagnetic Interference (EMI) Shielding Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market encompasses a range of solutions designed to mitigate the detrimental effects of electromagnetic radiation on electronic devices. EMI shielding effectiveness is a critical factor in ensuring reliable and uninterrupted operation, particularly in industries where signal integrity is paramount. Measuring EMI shielding effectiveness involves various techniques, including the use of test chambers and antennas to assess shielding efficiency. Design considerations for EMI shielding enclosures involve selecting appropriate materials based on frequency ranges and environmental conditions. Commonly used materials include conductive metals, such as copper and aluminum, and conductive polymers. Testing methods for high-frequency EMI shielding employ advanced techniques like the CISPR 25 standard, which ensures compliance with regulatory requirements. EMI shielding performance varies in different environments, necessitating robust design strategies. EMI shielding design software and simulation tools enable engineers to optimize shielding designs, reducing material usage and improving overall performance. Different shielding materials exhibit unique properties, with conductive metals offering superior shielding effectiveness but higher costs compared to conductive polymers. EMI reduction strategies for electronic devices include shielding, grounding, and filtering. Compliant EMI shielding design for wireless applications is crucial to maintain signal integrity and meet regulatory standards. Advanced EMI shielding technologies, such as frequency selective surfaces and metamaterials, offer enhanced performance and versatility. EMI shielding solutions for high-power electronic systems require robust techniques to handle intense electromagnetic fields. Performance optimization strategies, like the use of multi-layer shielding and shielding designs tailored to specific applications, contribute to cost savings in the supply chain by minimizing material usage and improving overall efficiency. Comparing different EMI shielding material properties, conductive metals offer superior shielding effectiveness but higher costs compared to conductive polymers. In aerospace applications, lightweight and high-performance materials are essential, making composite shielding materials an attractive alternative. Effective EMI shielding strategies for medical devices ensure patient safety and regulatory compliance. Cost-effective EMI shielding solutions, such as shielding paints and coatings, offer a more affordable alternative for applications with less stringent shielding requirements. Robust EMI shielding techniques for harsh environments, such as extreme temperatures and corrosive conditions, require materials with high durability and resistance to environmental factors. EMI shielding standards and regulations compliance is a critical business function, ensuring market access and reducing potential legal and reputational risks. Advanced EMI shielding design and modeling techniques enable engineers to create optimized shielding designs, reducing material usage and improving overall performance.

What are the Key Data Covered in this Electromagnetic Interference (EMI) Shielding Market Research and Growth Report?

-

What is the expected growth of the Electromagnetic Interference (EMI) Shielding Market between 2024 and 2028?

-

USD 3.53 billion, at a CAGR of 7.27%

-

-

What segmentation does the market report cover?

-

The report is segmented by Method (Conduction and Radiation), End-user (Automotive, Consumer electronics, Aerospace and defense, Healthcare, and IT and telecom), and Geography (APAC, North America, Europe, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Growth in global electronics production, Rising cost pressure from demand side

-

-

Who are the major players in the Electromagnetic Interference (EMI) Shielding Market?

-

3M Co., Changzhou Pioneer Electronic Co. Ltd., Cybershield Inc., DuPont de Nemours Inc., EDOGAWA GOSEI CO. LTD., EIS Legacy LLC, ESCO Technologies Inc., HEICO Corp., Henkel AG and Co. KGaA, Integrated Polymer Solutions, LG Chem Ltd., MAJR Products Corp., Miller Waste Mills Inc., NITTO KOGYO CORP., Nolato AB, Omega Shielding Products, Parker Hannifin Corp., PPG Industries Inc., Schaffner Group, and Tech Etch Inc.

-

We can help! Our analysts can customize this electromagnetic interference (emi) shielding market research report to meet your requirements.

RIA -

RIA -