Endoscopic Closure Devices Market Size 2025-2029

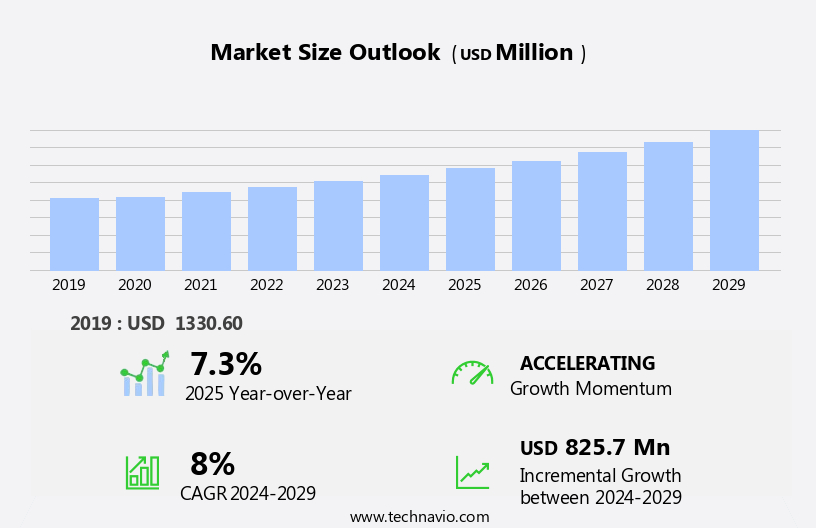

The endoscopic closure devices market size is forecast to increase by USD 825.7 million, at a CAGR of 8% between 2024 and 2029.

- The market is driven by the increasing incidence of gastrointestinal diseases, which necessitates the use of advanced endoscopic closure devices for effective treatment. These devices offer minimally invasive procedures, ensuring faster recovery times and reduced complications for patients. Technological advances in endoscopic devices continue to shape the market, with innovations such as radiofrequency ablation and endoscopic suturing gaining popularity. However, the high cost of endoscopy procedures poses a significant challenge for market growth. Healthcare providers and insurers must collaborate to develop cost-effective solutions, ensuring accessibility to these essential procedures for a larger patient population.

- Companies seeking to capitalize on market opportunities should focus on developing affordable, technologically advanced endoscopic closure devices that cater to the evolving needs of patients and healthcare providers. Navigating the challenges of cost and regulatory compliance will be crucial for market success.

What will be the Size of the Endoscopic Closure Devices Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

The market continues to evolve, driven by the ongoing quest for effective and safe solutions for various gastrointestinal applications. Complication mitigation strategies, such as endoscopic suturing techniques and ligation devices, have gained significant attention in recent years. Esophageal variceal banding and bleeding control methods have seen advancements in safety profiles, with biocompatibility testing playing a crucial role in ensuring patient safety. Colonic perforation repair and mucosal defect repair are key areas of focus, with tissue sealing mechanisms and device design features being continually refined to enhance procedural success rates. Device handling systems are also undergoing improvements to streamline procedures and reduce surgical complication rates.

Closure device materials, such as polymeric biomaterials, are being explored for their adhesive sealant properties and long-term stability. Clinical trial data and material degradation rates are closely monitored to assess the therapeutic efficacy and cost-effectiveness of these devices. Deployment time metrics and device sterilization methods are essential considerations in the market, with regulatory approvals and internal anastomosis also influencing market dynamics. Perforation closure systems and clip deployment systems are undergoing durability assessments to address the evolving needs of healthcare providers and patients. The market is characterized by continuous innovation and a dynamic landscape, with ongoing research and development efforts aimed at improving patient outcomes and reducing procedural risks.

How is this Endoscopic Closure Devices Industry segmented?

The endoscopic closure devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product

- Endoscopic closure systems

- Endoscopic clips

- Overstitch Endoscopic Suturing System

- Endoscopic Vacuum-Assisted Closure Systems

- Cardiac Septal Defect Occluders

- Sealants/Glues

- Staplers

- Others

- End-user

- Hospitals

- Ambulatory surgery centers

- Clinics

- Others

- Distribution Channel

- Direct

- Indirect

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- Middle East and Africa

- UAE

- APAC

- China

- India

- Japan

- South America

- Brazil

- Rest of World (ROW)

- North America

By Product Insights

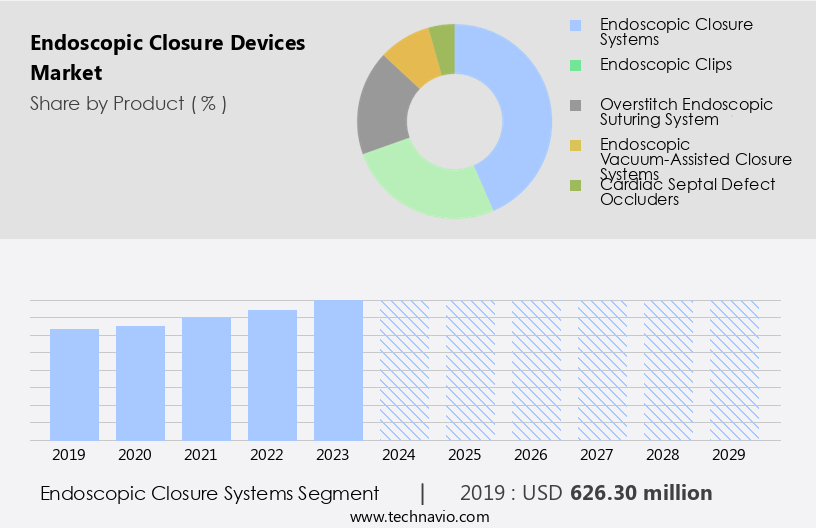

The endoscopic closure systems segment is estimated to witness significant growth during the forecast period.

The endoscopic closure systems market is witnessing significant growth due to the rising incidence of gastrointestinal (GI) diseases and advancements in technology leading to the development of new endoscopic closure systems. The increasing number of diagnostic and therapeutic endoscopic procedures, such as Endoscopic Mucosal Resection (EMR), Electrosurgical Dissection (ESD), and full-thickness resection of subepithelial tumors, is driving the demand for these systems. While through-the-scope (TTS) endoscopic closure clips are an option during endoscopic surgical treatments, they have limitations, including a limited opening span and closing strength, making them ineffective in fibrotic tissue settings. As a result, over-the-scope clips (OTSCs) are preferred by surgeons for closing large perforations.

Safety profiles, procedural success rates, and biocompatibility testing are crucial factors influencing the market. Polymeric biomaterials, tissue sealing mechanisms, and device design features are key areas of focus for manufacturers. Closure device materials, patient recovery times, adhesive sealant properties, clinical trial data, material degradation rates, insertion tube diameter, regulatory approvals, long-term stability, deployment time metrics, device sterilization methods, perforation closure systems, device cost-effectiveness, therapeutic efficacy metrics, clip deployment systems, durability assessments, and gastric ulcer closure are all integral aspects of the market. The market is also witnessing advancements in esophageal variceal banding, bleeding control methods, colonic perforation repair, and mucosal defect repair.

Regulatory approvals, device handling systems, surgical complication rates, and closure device materials are significant factors impacting the market dynamics. The market for endoscopic closure systems is expected to continue its growth trajectory due to its clinical benefits and the increasing number of indications.

The Endoscopic closure systems segment was valued at USD 626.30 million in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

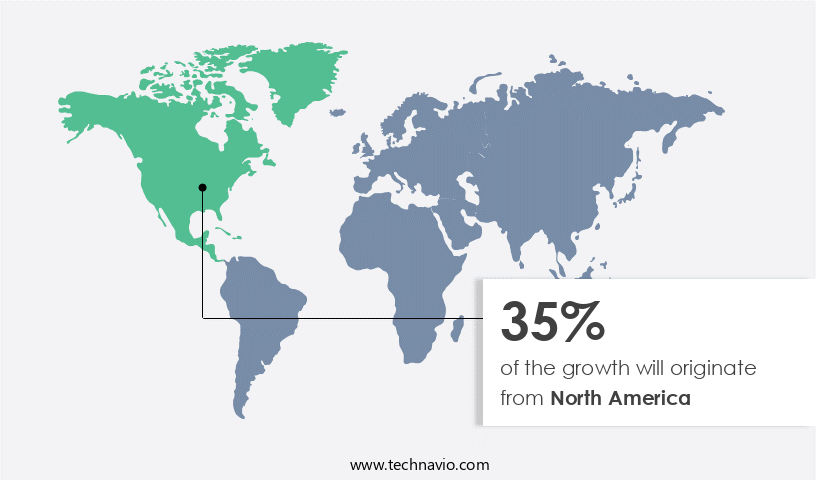

North America is estimated to contribute 35% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in North America is experiencing steady growth, driven by the region's high adoption of advanced technologies, increasing prevalence of chronic diseases, a growing geriatric population, and availability of reimbursement for endoscopic procedures. Chronic conditions such as inflammatory bowel diseases (IBDs), gastroesophageal reflux disease (GERD), stomach cancer, colon cancer, and pancreatic cancers necessitate endoscopic surgeries, fueling market expansion. Endoscopic suturing techniques, ligation devices, and esophageal variceal banding are among the advanced technologies used for bleeding control and mucosal defect repair. Safety profiles, procedural success rates, and biocompatibility testing are crucial factors influencing market trends.

Polymeric biomaterials, tissue sealing mechanisms, and device design features are key considerations for manufacturers. Device handling systems, surgical complication rates, closure device materials, patient recovery times, and adhesive sealant properties are essential aspects of the market. Clinical trial data, material degradation rates, insertion tube diameter, regulatory approvals, internal anastomosis, long-term stability, deployment time metrics, device sterilization methods, perforation closure systems, and cost-effectiveness are critical factors shaping market dynamics. The market is witnessing the development of innovative endoscopic closure devices, including clip deployment systems, durability assessments, and gastric ulcer closure solutions. These advancements aim to address surgical complications, improve therapeutic efficacy, and enhance patient outcomes.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The endoscopic closure device market continues to evolve, offering innovative solutions for various gastrointestinal procedures. One key aspect of these devices is the endoscopic closure process, which involves deploying the device to seal and repair damaged tissue. The closure mechanism often utilizes a polymeric biomaterial, which undergoes degradation over time to allow for tissue regeneration. Effectiveness metrics for tissue sealing mechanisms are crucial in evaluating the safety and efficacy of these devices. Clinical trials provide valuable data on the device's safety profile, with low complication rates reported for luminal occlusion techniques. Adhesive sealants used in these devices exhibit desirable properties, such as biocompatibility and ease of application. Endoscopic suturing techniques require specialized training programs to ensure proper handling and usage. Device handling systems are designed with user-friendly features, enabling efficient and precise deployment. Success rates for procedures like gastric ulcer closure and colonic perforation repair have shown promising outcomes. Therapeutic efficacy metrics in clinical trials demonstrate the superiority of endoscopic closure devices compared to traditional surgical alternatives. Cost-effectiveness is another significant factor, with the bioabsorbable polymer degradation time frame contributing to long-term savings. Minimally invasive procedures using these devices have lower complication rates and reduced surgical times. Device sterilization method validation protocols and material biocompatibility testing standard methods ensure the highest quality and safety for patients. A well-designed device maintenance protocol is essential for extended usage, while quality control measures in manufacturing processes adhere to market research report standards.

What are the key market drivers leading to the rise in the adoption of Endoscopic Closure Devices Industry?

- The rising prevalence of gastrointestinal diseases serves as the primary catalyst for market growth in this sector.

- The prevalence of gastrointestinal diseases, including conditions such as gallstones, ulcerative colitis, fissures, hemorrhoids, IBD, and GERD, has seen a significant increase worldwide. Factors contributing to this trend include poor diet, inactive lifestyle, stress, food sensitivity, and bacterial or viral infections. Chronic gastrointestinal diseases can lead to various medical complications and disabilities if left untreated. Inflammatory bowel disease (IBD), which causes inflammation of the gastrointestinal tract, is a common gastrointestinal condition. Crohn's disease and ulcerative colitis are the most prevalent forms of IBD. For instance, in 2022, the National Health Service (NHS) reported that one in every 420 individuals in the UK had ulcerative colitis.

- Endoscopic closure devices have emerged as essential tools for treating gastrointestinal diseases and mitigating complications. These devices employ various techniques, including endoscopic suturing and ligation, to facilitate healing and control bleeding. Esophageal variceal banding is a common application of these devices, used to treat esophageal varices, a complication of cirrhosis. Safety profiles and procedural success rates are crucial considerations in the selection of endoscopic closure devices. Advancements in polymeric biomaterials have significantly enhanced the functionality and efficacy of endoscopic closure devices. These materials enable the development of biocompatible and biodegradable devices that minimize the risk of complications and promote faster healing.

- As a result, endoscopic closure devices have become indispensable in gastrointestinal procedures, offering improved patient outcomes and reducing healthcare costs.

What are the market trends shaping the Endoscopic Closure Devices Industry?

- Endoscopic technology is currently experiencing significant advancements, emerging as a notable market trend in the healthcare industry. Innovations in endoscopic devices continue to shape the future of diagnostic and therapeutic procedures.

- The market is witnessing significant advancements as companies invest in research and development to expand their product offerings and maintain a competitive edge. These devices are designed to repair mucosal defects and colonic perforations, utilizing tissue sealing mechanisms and biocompatible materials. companies are focusing on innovative designs, including imaging systems for enhanced organ visibility, and device handling systems to ensure efficient and effective use. The market is driven by the increasing incidence of gastrointestinal disorders and the need for minimally invasive surgical procedures.

- The market's growth is further propelled by the decreasing surgical complication rates associated with these devices. companies are prioritizing biocompatibility testing to ensure the safety and efficacy of their products. Cook Group, a leading player in the market, introduced the Instinct Endoscopic Hemoclip, showcasing the market's technological advancements.

What challenges does the Endoscopic Closure Devices Industry face during its growth?

- The escalating costs of endoscopy procedures pose a significant challenge to the industry's growth trajectory.

- Endoscopic closure devices are essential tools used in surgical procedures for managing leaks, perforations, and fistulas. The global demand for these devices is growing due to the increasing prevalence of gastrointestinal (GI) diseases, which necessitate various endoscopic procedures, such as upper endoscopy, colonoscopy, and laparoscopy. These procedures are commonly used for treating patients with GI diseases, cancer, and kidney and liver diseases. Despite the growing demand, the high cost of endoscopic procedures can hinder the adoption of endoscopic closure devices. The cost includes the radiological examination before surgery, the surgical procedure itself, fees of healthcare professionals, and hospital stay.

- However, advancements in endoscopic closure devices, such as adhesive sealant properties and long-term stability, are encouraging clinical trial data and regulatory approvals. Additionally, material degradation rates and insertion tube diameter are crucial factors influencing the market dynamics. Overall, the market for endoscopic closure devices is expected to continue its growth due to the increasing need for minimally invasive surgical procedures and the advantages these devices offer in terms of patient recovery times and internal anastomosis.

Exclusive Customer Landscape

The endoscopic closure devices market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the endoscopic closure devices market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, endoscopic closure devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abbott Laboratories - The company specializes in providing advanced endoscopic closure solutions, including the Perclose ProGlide SMC System, enhancing surgical efficiency and reducing complications in various medical procedures.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- Ackermann Instrumente GmbH

- AHM Grup

- Ambu AS

- B.Braun SE

- Boston Scientific Corp.

- Cardinal Health Inc.

- Changzhou Jiuhong Medical Instrument Co.

- Cook Group Inc.

- Endocor GmbH and Co. KG

- Era Endoscopy Srl

- Haemonetics Corp.

- Johnson and Johnson Inc.

- Medtronic Plc

- Micro Tech Nanjing Co. Ltd.

- Olympus Corp.

- Ovesco Endoscopy AG

- STERIS plc

- Teleflex Inc.

- The Cooper Companies Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Endoscopic Closure Devices Market

- In January 2024, Ethicon, a subsidiary of Johnson & Johnson, announced the FDA approval of its ENDO-Flex180 Endoscopic Suturing System. This innovative device allows for endoscopic suturing and closure with a single instrument, addressing the need for multiple devices in the procedure (Johnson & Johnson press release, 2024).

- In March 2024, Medtronic and Apollo Endosurgery entered into a strategic partnership to co-develop and commercialize endoscopic suturing technologies. This collaboration aims to expand Medtronic's portfolio in gastrointestinal therapies and enhance Apollo Endosurgery's offerings (Medtronic press release, 2024).

- In May 2024, Boston Scientific completed the acquisition of EndoChoice, a leading provider of endoscopic devices and solutions. This acquisition strengthened Boston Scientific's gastroenterology portfolio and expanded its presence in the market (Boston Scientific press release, 2024).

- In January 2025, Olympus received CE mark approval for its OverStitch Sx Endoscopic Suturing System. This system enables endoscopic full-thickness suturing and offers advantages such as reduced procedure time and improved patient outcomes (Olympus Europe press release, 2025).

Research Analyst Overview

- The market encompasses advanced sealant formulations, luminal occlusion techniques, and hemostasis technologies, aimed at minimizing post-operative complications and enhancing clinical outcome measures. Cost-benefit analysis frameworks are crucial for evaluating device maintenance protocols, quality control measures, and device shelf-life determination against material biocompatibility standards and sterilization validation. Distribution networks play a significant role in ensuring efficient supply chain management and patient access to these devices. Luminal occlusion techniques and endoscopic closure mechanisms have revolutionized intestinal perforation repair, leading to reduced surgical time and improved patient comfort levels. Training curriculum and operator experience are vital factors in optimizing device usability and ensuring successful tissue regeneration.

- Reimbursement pathways and competitive landscape analysis are essential aspects of the market, with bioabsorbable polymers and ergonomic designs offering competitive advantages. Wound healing assessment and device ergonomics are critical in maintaining patient comfort levels during procedures. Device maintenance protocols and quality control measures are essential for ensuring device longevity and optimal performance. Longitudinal clinical studies provide valuable insights into the efficacy and safety of these devices, while minimally invasive procedures continue to drive market growth. The competitive landscape is shaped by ongoing innovation in hemostasis technologies and tissue regeneration, with companies investing in R&D to address unmet clinical needs and improve patient outcomes.

- Packaging considerations and patient comfort levels are also crucial factors influencing market trends.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Endoscopic Closure Devices Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

207 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8% |

|

Market growth 2025-2029 |

USD 825.7 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

7.3 |

|

Key countries |

US, China, Germany, UK, Canada, Japan, France, Brazil, UAE, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Endoscopic Closure Devices Market Research and Growth Report?

- CAGR of the Endoscopic Closure Devices industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the endoscopic closure devices market growth of industry companies

We can help! Our analysts can customize this endoscopic closure devices market research report to meet your requirements.

RIA -

RIA -