Gastroesophageal Reflux Disease Market Size 2024-2028

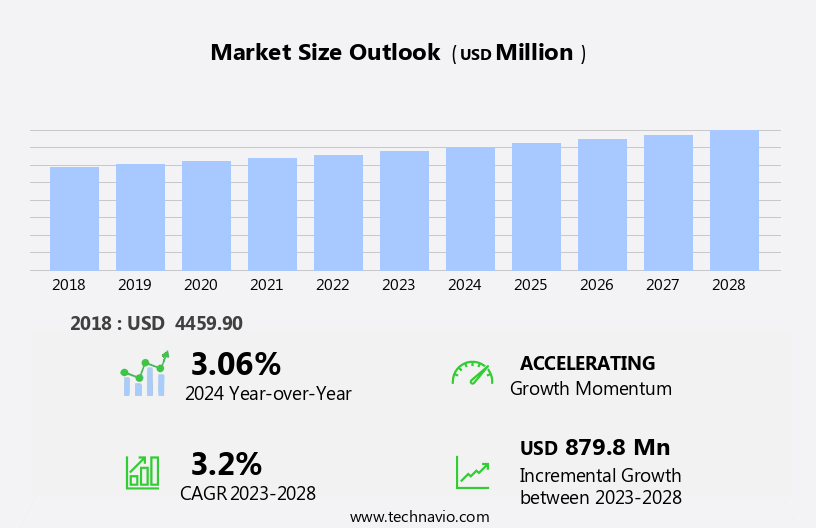

The gastroesophageal reflux disease (GERD) market size is forecast to increase by USD 879.8 mn at a CAGR of 3.2% between 2023 and 2028.

- The market is witnessing significant growth due to several key factors. The rising geriatric population and increasing prevalence of obesity are major drivers for the market. Additionally, there is an increased preference for complementary and alternative medicine (CAM), including cryotherapy and herbal remedies, which are gaining popularity in managing GERD symptoms. Digital health technologies, such as mobile apps, artificial intelligence (AI), and analytics, are revolutionizing the diagnosis and treatment of GERD. Telehealth, telemedicine, and virtual reality are also transforming patient care, enabling remote consultations and access to medical education. Medical devices, content, and network security are crucial considerations for the digital health sector.

- Emerging trends include stem cell therapy, data security, home healthcare, and dietary supplements. Type 2 diabetes, precision medicine, collagen, and digital therapeutics are also areas of focus for the market. The adoption of acupuncture, cell therapy, and music therapy is increasing, offering alternative treatment options. Population health management, insurance, and professional development are essential aspects of the market, with cloud security playing a vital role in ensuring data privacy and security. The market is expected to continue growing, driven by these trends and the increasing demand for effective GERD treatments.

What will be the Size of the Gastroesophageal Reflux Disease (GERD) Market During the Forecast Period?

- The market encompasses a range of treatments and interventions aimed at managing symptoms and preventing complications of this chronic condition. GERD, also known as acid reflux, affects millions worldwide, characterized by the backward flow of gastric acid into the esophagus, leading to heartburn and potential complications such as esophageal cancer. Market dynamics include the use of various treatments, including proton pump inhibitors (PPIs), antacids, and lifestyle changes. PPIs, prescription medications that reduce acid production, dominate the market due to their effectiveness in symptom relief. Diagnostic tests and endoscopic procedures are also utilized to diagnose and monitor the disease. Patient education and disease management are crucial aspects of the market, with a focus on symptom management and long-term care.

- Clinical trials continue to explore new treatment options and improve existing therapies. Lifestyle changes, such as dietary modifications and weight loss, are often recommended as first-line treatments. The market for GERD treatments is expected to grow due to the increasing prevalence of the disease and the availability of new treatment options. Antacids and PPIs remain popular choices for symptomatic relief, while diagnostic tests and endoscopic procedures aid in accurate diagnosis and monitoring. Ongoing research and development efforts aim to improve patient outcomes and reduce the burden of this chronic condition.

How is this Gastroesophageal Reflux Disease (GERD) Industry segmented and which is the largest segment?

The gastroesophageal reflux disease (GERD) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Route Of Administration

- Oral

- Parenteral

- Type

- Antacid

- PPI

- H2 receptor antagonist drugs

- Pro-Kinetic drugs

- Geography

- North America

- Canada

- US

- Europe

- Germany

- UK

- Asia

- China

- Rest of World (ROW)

- North America

By Route Of Administration Insights

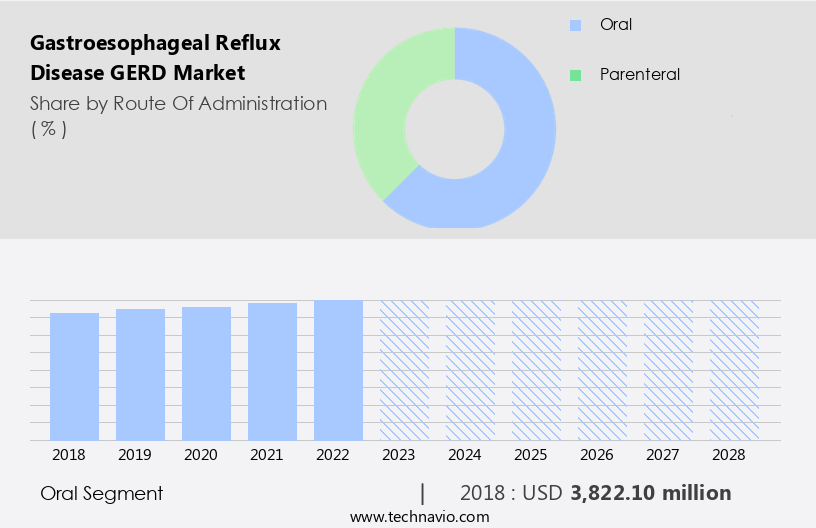

- The oral segment is estimated to witness significant growth during the forecast period. The oral segment is estimated to witness significant growth during the forecast period. The oral route of administration is the most commonly used route for GERD medication. The oral route is preferred to administer GERD drugs over other methods as it is a safe, non-invasive, cost-effective, and easy-to-use method. The oral drug route of administration segment includes GERD drugs that can be administered in the form of capsules, tablets, syrups, solutions, and suspensions. The growth of the segment is accelerating at a moderate pace owing to the ease of usage and an increasing number of government approvals for oral GERD treatment.

Get a glance at the market report of share of various segments Request Free Sample

The oral segment was valued at USD 3.82 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

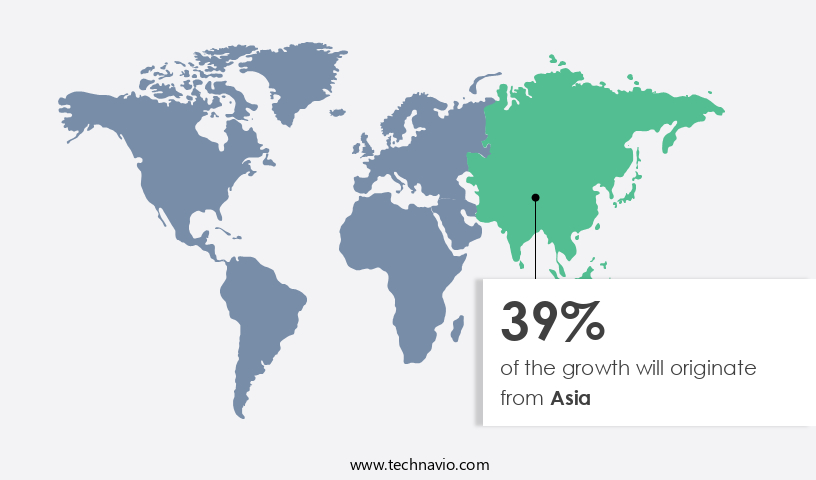

- Asia is estimated to contribute 39% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

Another region offering significant growth is North America. The market in North America is driven by its high prevalence rate and the increasing use of over-the-counter (OTC) medications. According to the International Foundation for Gastrointestinal Disorders (IFFGD), the estimated prevalence of GERD in North America is 20%. Moreover, the Consumer Healthcare Products Association reports that over three-quarters of the population in the region use OTC medications for self-medication. Factors such as poor lifestyle choices and the usage of non-steroidal anti-inflammatory drugs (NSAIDs) contribute to market growth. However, the presence of counterfeit drugs poses a challenge. GERD is a chronic condition characterized by symptoms such as heartburn, regurgitation, and acid reflux. Treatment options include lifestyle modifications, acid suppression through Proton Pump Inhibitors (PPIs) and H2 Receptor Antagonists (H2RAs), and surgical interventions.

Complications of GERD include esophageal cancer, Barrett's Esophagus, esophageal strictures, and hiatal hernia. Diagnostic tests like esophageal manometry, pH monitoring, and impedance testing aid in the diagnosis and monitoring of the disease. Pharmacological approaches include PPIs, H2RAs, antacids, and prescription medications. Non-pharmacological interventions include lifestyle changes, stress management, and patient education. Clinical trials and research focus on emerging therapies, personalized medicine, and precision medicine. The market faces challenges such as high treatment costs, health disparities, and the availability of alternative therapies. Regulatory frameworks, healthcare legislation, and insurance reimbursement policies play a significant role in market growth.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Gastroesophageal Reflux Disease (GERD) Industry?

The rising geriatric population is the key driver of the market.

- The aging population is a significant driving factor in the expansion of the global market for GERD treatment. As people grow older, the lower esophageal sphincter, which prevents gastric acid from flowing back into the esophagus, can weaken, leading to acid reflux and heartburn. Additionally, the digestive system's functionality may decrease with age, further contributing to acidity. GERD, a chronic digestive disorder, is also more prevalent among older adults. According to epidemiology data, the prevalence rates of GERD increase with age, making the aging population a substantial market opportunity. The GERD market encompasses various therapeutic approaches, including prescription medications like Proton Pump Inhibitors (PPIs) and H2 Receptor Antagonists, over-the-counter drugs such as antacids, and lifestyle changes.

- Diagnostic tests, such as esophageal manometry, pH monitoring, and impedance testing, are essential for proper diagnosis and treatment. Esophageal disorders related to GERD, such as Barrett's Esophagus, esophageal strictures, and esophageal cancer, also contribute to the market's growth. Complications of GERD, including respiratory symptoms like chronic cough and asthma, dental erosion, sleep disturbances, and chronic laryngitis, further necessitate effective treatment and management. Pharmacological interventions, such as PPIs and H2 receptor antagonists, and surgical procedures like laparoscopic fundoplication and esophageal resection, are essential components of the GERD market. Patient education, clinical trials, and emerging therapies, such as regenerative medicine and stem cell therapy, are crucial in improving patient care and quality of life.

- Health insurance coverage, economic impact, and patient satisfaction are essential factors influencing the market's growth. Adherence to treatment, nutritional counseling, and alternative therapies like herbal remedies and acupuncture, are also essential aspects of the GERD market. Market challenges include drug safety, regulatory framework, and healthcare disparities. The FDA approval process, ethical considerations, and informed consent are essential components of the regulatory framework. Healthcare providers, including gastroenterologists and primary care physicians, play a crucial role in the referral system and multidisciplinary care. Emerging therapies, such as personalized medicine and precision medicine, offer significant growth opportunities in the market.

What are the market trends shaping the Gastroesophageal Reflux Disease (GERD) Industry?

The rising prevalence of obesity is the upcoming market trend.

- The association between obesity and gastroesophageal reflux disease (GERD) has gained considerable attention in medical research due to the increasing prevalence of obesity and related disorders, such as esophageal erosions, Barrett's esophagus (BE), and esophageal adenocarcinoma. Several studies suggest that obesity may contribute to GERD through various mechanisms, including increased intra-abdominal pressure and esophageal dysmotility. The rising cases of obesity are expected to significantly increase the medical costs associated with its complications, including GERD. Obesity is a leading risk factor for various chronic conditions, including cardiovascular diseases, type 2 diabetes, and certain types of cancer, which can result in premature death.

- The economic impact of obesity is substantial, and the associated healthcare costs are projected to continue rising. In the context of GERD, lifestyle modifications, such as weight loss, smoking cessation, and diet modifications, are essential components of disease management. Clinical trials and research initiatives are ongoing to explore new therapeutic options, including pharmacological approaches, surgical interventions, and endoscopic treatments. Patient education, symptom management, and disease prevention are crucial aspects of GERD treatment. The diagnostic process involves various tests, including esophageal manometry, pH monitoring, and impedance testing, to assess esophageal motility and acid clearance. Complications of GERD include respiratory symptoms, dental erosion, sleep disturbances, and esophageal strictures, among others.

- Effective management of GERD requires a multidisciplinary approach, involving gastroenterology specialists, primary care physicians, and other healthcare providers. The regulatory framework and ethical considerations play a vital role in ensuring patient safety and informed consent. The market for GERD treatment is dynamic, with emerging therapies, personalized medicine, and digital health solutions offering significant growth opportunities. However, market challenges, such as healthcare disparities and treatment costs, require ongoing attention and innovation.

What challenges does the Gastroesophageal Reflux Disease (GERD) Industry face during its growth?

Increased preference for complementary and alternative medicine CAM is a key challenge affecting the industry growth.

- The global market for GERD treatment is influenced by the growing preference for complementary and alternative therapies (CAM) among patients. Approximately 70% of the population in the US have tried CAM treatments for GERD at least once. These therapies, which include acupuncture, massage, tai chi, herbs, and supplements, as well as mind and body therapies like yoga, meditation, exercise, and relaxation therapy, are increasingly popular due to their non-pharmacological approach. The trend towards CAM treatments for GERD is driven by a desire to avoid medication and focus on lifestyle modifications. Key CAM therapies for GERD include Proton Pump Inhibitors (PPIs) alternatives such as antacids, H2 receptor antagonists, and over-the-counter drugs.

- Other interventions include lifestyle changes like diet modifications, obesity management through smoking cessation and alcohol consumption reduction, and non-pharmacological approaches like esophageal clearance techniques and reflux monitoring devices. The market dynamics for GERD treatment are further shaped by the availability of diagnostic tests, endoscopic procedures, and surgical interventions, as well as the prevalence of complications such as esophageal cancer, esophageal strictures, and Barrett's esophagus. The epidemiology data and treatment guidelines for GERD continue to evolve, providing opportunities for therapeutic innovations and personalized medicine approaches. The market faces challenges such as healthcare disparities, treatment costs, and the need for regulatory compliance and ethical considerations.

Exclusive Customer Landscape

The gastroesophageal reflux disease (GERD) market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the gastroesophageal reflux disease (GERD) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, gastroesophageal reflux disease (GERD) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- Alkem Laboratories Ltd.

- Apotex Inc.

- AstraZeneca Plc

- Aurobindo Pharma Ltd.

- Bayer AG

- Cipla Inc.

- Dr Reddys Laboratories Ltd.

- Eisai Co. Ltd.

- Fresenius SE and Co. KGaA

- GlaxoSmithKline Plc

- inovapharma.com

- Johnson and Johnson Services Inc.

- Lupin Ltd.

- Perrigo Co. Plc

- Pfizer Inc.

- SRS Life Sciences Pte. Ltd.

- Sun Pharmaceutical Industries Ltd.

- Takeda Pharmaceutical Co. Ltd.

- The Procter and Gamble Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Gastroesophageal Reflux Disease (GERD) is a chronic condition characterized by the backward flow of stomach contents into the esophagus, leading to various symptoms and potential complications. This complex condition necessitates a multifaceted approach to treatment and management. The global market for GERD treatment encompasses a wide range of interventions, from lifestyle modifications and non-pharmacological approaches to pharmacological therapies and surgical interventions. Proton pump inhibitors (PPIs) and H2 receptor antagonists (H2RAs) are among the most commonly used medications for acid suppression. However, there is a growing interest in alternative therapies, such as herbal remedies, acupuncture, and stress management techniques. Diagnostic tests, including endoscopic procedures and esophageal manometry, play a crucial role in the identification and assessment of GERD.

Further, these tests help determine the presence and severity of conditions such as esophageal strictures, hiatal hernia, and Barrett's esophagus. Patient education is a crucial component of GERD management. This includes understanding risk factors, such as obesity, smoking, and alcohol consumption, and implementing diet modifications and lifestyle changes. Clinical trials and research initiatives continue to explore new therapeutic options, including emerging therapies in the fields of personalized medicine and precision medicine. The economic impact of GERD is significant, with high treatment costs and potential complications leading to increased healthcare utilization and decreased quality of life. Health insurance coverage and financial assistance programs are essential for ensuring access to care for those affected by this condition.

Moreover, the prevalence rates of GERD vary across populations, with epidemiology data indicating a higher incidence in industrialized countries and older adults. Complications of GERD include respiratory symptoms, such as chronic cough and asthma, dental erosion, and sleep disturbances. Complications management involves a multidisciplinary approach, including gastroenterology specialists, primary care physicians, and referral systems. The regulatory framework for GERD treatment and management is complex, with FDA approval, drug safety, and clinical practice guidelines playing essential roles in ensuring the safety and efficacy of various interventions. Healthcare providers must navigate ethical considerations, informed consent, and patient privacy concerns, while also addressing the challenges of adherence to treatment and long-term complications.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

176 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.2% |

|

Market Growth 2024-2028 |

USD 879.8 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.06 |

|

Key countries |

US, Germany, UK, China, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Gastroesophageal Reflux Disease (GERD) Market Research and Growth Report?

- CAGR of the Gastroesophageal Reflux Disease (GERD) industry during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the gastroesophageal reflux disease (GERD) market growth of industry companies

We can help! Our analysts can customize this gastroesophageal reflux disease (GERD) market research report to meet your requirements.

RIA -

RIA -