Enterprise Generative AI Market Size 2025-2029

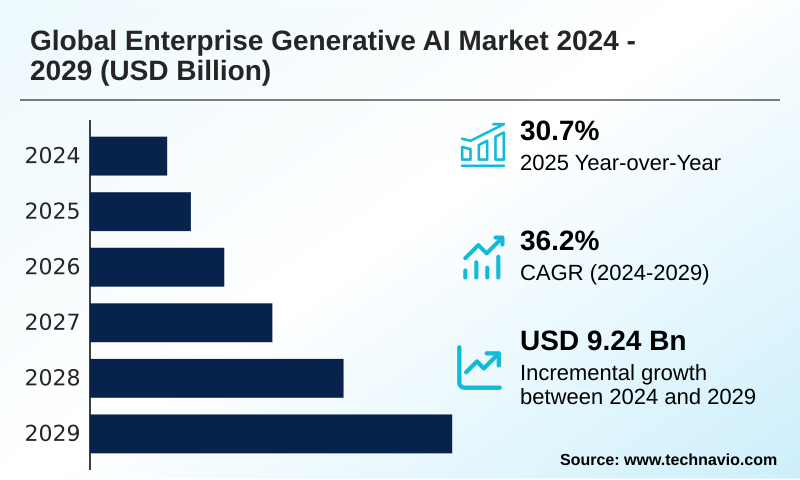

The enterprise generative ai market size is valued to increase by USD 9.24 billion, at a CAGR of 36.2% from 2024 to 2029. Surging demand for hyper-automation and operational efficiency will drive the enterprise generative ai market.

Major Market Trends & Insights

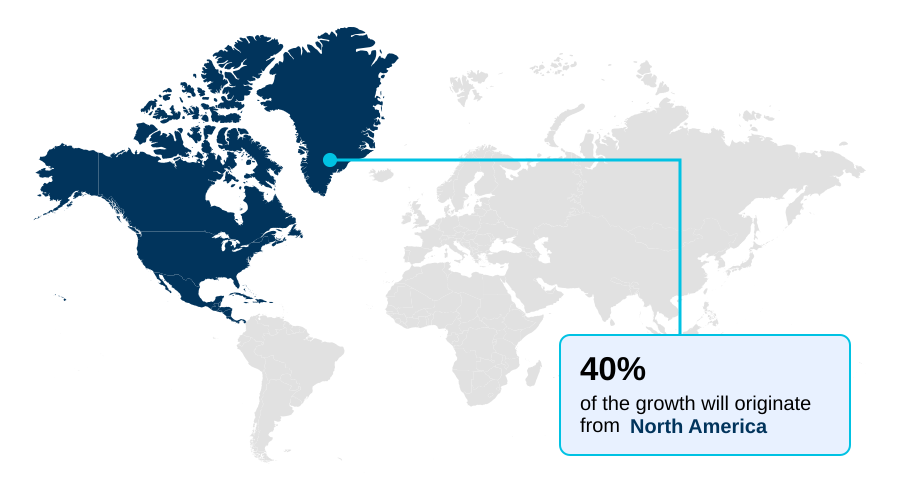

- North America dominated the market and accounted for a 40.1% growth during the forecast period.

- CAGR from 2024 to 2029 : 36.2%

Market Summary

- The Enterprise Generative AI market is transitioning from experimental phases to strategic, large-scale implementation across industries. This shift is driven by the clear value proposition of augmenting human productivity and achieving significant operational efficiencies. Organizations are moving beyond basic chatbots to deploy sophisticated systems for complex tasks like generative design, software development, and advanced data synthesis.

- For instance, in supply chain management, businesses use AI to generate synthetic logistics data, enabling them to model and stress-test their networks against potential disruptions without using sensitive real-world information. The technology, including advanced techniques like retrieval-augmented generation (RAG) and generative adversarial networks (GANs), helps create more resilient and predictive operational frameworks.

- However, this adoption is tempered by challenges such as ensuring data privacy, managing high computational costs, and navigating an evolving regulatory landscape, which demands robust governance and ethical oversight for sustainable, long-term deployment.

What will be the Size of the Enterprise Generative AI Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Enterprise Generative AI Market Segmented?

The enterprise generative ai industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029.

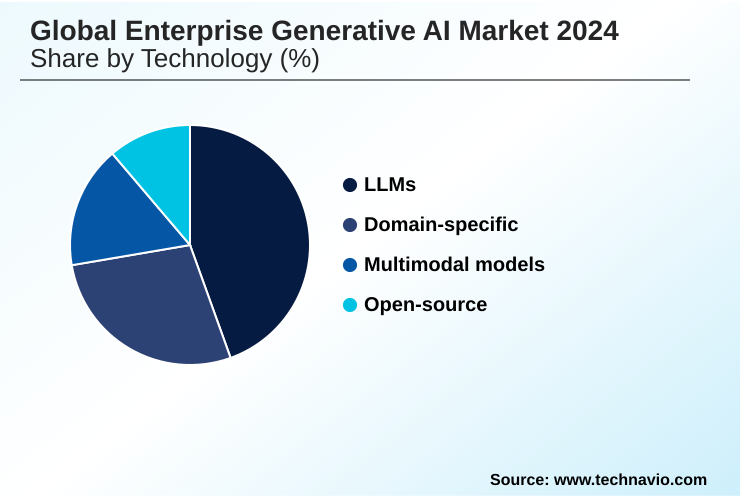

- Technology

- LLMs

- Domain-specific

- Multimodal models

- Open-source

- Application

- Content creation

- Code generation

- Data augmentation

- Others

- Deployment

- Cloud-based

- Hybrid

- On-premises

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- Middle East and Africa

- UAE

- Saudi Arabia

- Israel

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Technology Insights

The llms segment is estimated to witness significant growth during the forecast period.

The Enterprise Generative AI Market is fundamentally shaped by large language models, which leverage complex neural network architecture to power applications. These systems are pivotal for functions like cognitive process automation and advanced knowledge management AI.

Enterprises utilize these models for synthetic data generation and data augmentation techniques to train other machine learning systems, addressing data scarcity. The deployment landscape is increasingly favoring a hybrid AI infrastructure, balancing cloud flexibility with on-premise security.

A key focus is on AI risk management and enabling custom AI model training to refine outputs.

Through sophisticated natural language understanding (NLU) and expanded AI model context windows, these technologies are transforming AI-driven software development, with some firms improving code quality by over 25%.

This evolution is critical for building robust, enterprise-ready generative adversarial networks (GANs) and other advanced systems.

Regional Analysis

North America is estimated to contribute 40.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Enterprise Generative AI Market Demand is Rising in North America Get Free Sample

The global landscape is characterized by diverse adoption strategies, heavily influenced by regional infrastructure and regulatory priorities. North America leads in foundation model development, while APAC is seeing the fastest growth in enterprise generative AI applications.

The expansion of cloud-based deployment models and managed AI services is crucial for this growth, providing accessible API-based AI access.

In regions like Europe, the emphasis on data sovereignty solutions is driving demand for private cloud AI and secure, on-premise code generation tools.

Enterprises globally are deploying open-source models for custom solutions in areas like sales enablement AI and research assistance tools, ensuring both AI safety and reliability.

This distributed innovation is critical for building production-grade AI systems, with adoption in emerging markets showing a 2x increase in pilot projects over the last year. Enhanced enterprise search AI is becoming a standard feature.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- As organizations mature in their AI journey, strategic decisions are moving beyond initial adoption to focus on long-term value and risk mitigation. Boardroom conversations now center on the vertical integration impact on AI market dynamics and the necessity of custom silicon for AI model training to gain a competitive edge.

- A primary focus is on implementing secure on-premise generative AI to protect sensitive data, which is a critical aspect of managing generative AI intellectual property risks and ensuring data privacy with third-party AI models. The generative AI role in operational efficiency is undisputed, but leaders are now analyzing how to manage generative AI implementation costs effectively.

- This involves comparing cloud vs hybrid generative AI deployment models to balance scalability with control. Success hinges on robust enterprise AI platform governance strategies designed to minimize security vulnerabilities and reduce AI model hallucination in enterprise settings, with firms adopting such frameworks reporting 20% fewer data-related incidents.

- For specific sectors, applications like multimodal generative AI for manufacturing and generative AI for synthetic data in healthcare are unlocking new possibilities.

- Ultimately, leveraging AI for new revenue streams through initiatives like open-source generative AI model customization and generative AI for hyper-personalized marketing requires addressing ethical considerations in enterprise AI deployment and developing effective generative AI talent acquisition strategies to secure the necessary expertise.

- These factors are crucial for capitalizing on opportunities in generative AI for software development acceleration and generative AI applications in financial services.

What are the key market drivers leading to the rise in the adoption of Enterprise Generative AI Industry?

- The market is primarily driven by a surging enterprise demand for hyper-automation and enhanced operational efficiency.

- The primary market driver is the intense enterprise pursuit of hyper-automation and operational efficiency AI.

- Businesses are deploying AI-powered chatbots and virtual assistants to handle customer interactions, with some platforms managing workloads equivalent to hundreds of full-time agents and achieving a 25% reduction in repeat inquiries.

- This push extends to internal processes through AI-driven workflow automation and intelligent automation tools that accelerate the entire AI development lifecycle.

- The accessibility of enterprise-grade AI solutions, offered as model-as-a-service (MaaS) with strong AI model performance benchmarks, is democratizing access to both proprietary AI models and open-source alternatives.

- This is enabling widespread content creation automation and AI-driven personalization at scale, fundamentally altering how companies innovate and compete. This trend is unlocking unprecedented levels of productivity and creating new avenues for revenue generation across all sectors.

What are the market trends shaping the Enterprise Generative AI Industry?

- The market is undergoing a significant shift toward specialization. This is characterized by the rising adoption of multimodal and domain-specific foundation models.

- The market is pivoting from general-purpose tools to specialized systems, marked by a dual focus on multimodality and domain-specificity. Enterprises are increasingly demanding AI that performs multimodality reasoning, integrating text with image and audio analysis through technologies like diffusion models. This trend is unlocking advanced applications such as AI-driven generative design.

- Simultaneously, the adoption of domain-specific models and domain-aware models, especially in high-stakes industries, is improving accuracy by over 15% compared to generalist counterparts. The strategic push towards vertical integration stacks and walled garden ecosystems is another defining trend, as corporations build full-stack AI solutions to control the entire AI value chain.

- This allows for the creation of tightly integrated AI-native systems and specialized AI copilots. Techniques like retrieval-augmented generation (RAG) are becoming standard for enhancing the factual accuracy of these sophisticated systems.

What challenges does the Enterprise Generative AI Industry face during its growth?

- Navigating the complexities of data privacy, security, and intellectual property rights presents a key challenge to industry growth.

- Navigating significant implementation hurdles is a key challenge for enterprises. The high AI inference costs and the soaring expense of GPU acceleration create substantial financial barriers, with on-premise AI deployment requiring millions in upfront hardware investment. This is compounded by a severe AI talent gap, making it difficult to source experts for prompt engineering and responsible AI implementation.

- Furthermore, ensuring data security within enterprise AI platforms is paramount, as firms strive to create secure AI environments and mitigate risks of data leakage, which have reportedly increased by 15% with the use of public tools. Addressing AI ethics and model bias mitigation through robust AI governance frameworks is now a critical compliance requirement.

- Even with advanced foundation model development and custom AI silicon, achieving explainable AI (XAI) remains a complex technical challenge that hinders trust and full-scale adoption in regulated industries.

Exclusive Technavio Analysis on Customer Landscape

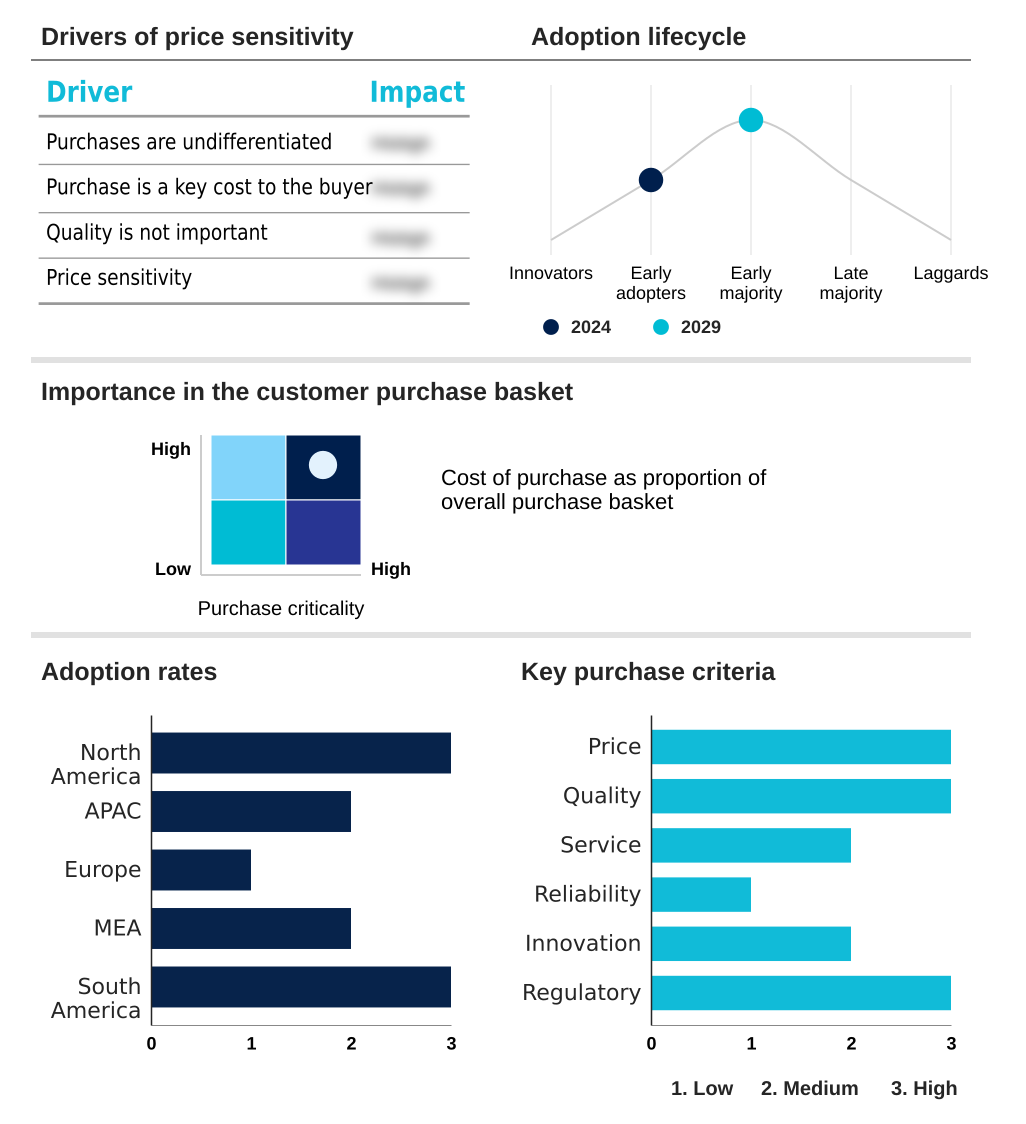

The enterprise generative ai market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the enterprise generative ai market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Enterprise Generative AI Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, enterprise generative ai market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Adobe Inc. - Delivers enterprise generative tools for scalable content creation, streamlining image, video, and copy production to boost creative workflow efficiency.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adobe Inc.

- AI21 Labs

- Amazon Web Services Inc.

- Anthropic

- Cohere

- Databricks Inc.

- Google Cloud

- Hugging Face

- IBM Corp.

- Meta Platforms Inc.

- Microsoft Corp.

- Mistral AI

- NVIDIA Corp.

- OpenAI

- Oracle Corp.

- Salesforce Inc.

- SAP SE

- Scale

- ServiceNow Inc.

- Snowflake Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Enterprise generative ai market

- In September, 2024, Salesforce Inc. announced a strategic collaboration with a leading open-source AI firm to integrate advanced, multilingual code generation tools directly into its developer platform, aiming to accelerate custom application development for its global enterprise clients.

- In November, 2024, IBM Corp. launched watsonx.gov, a new government-focused cloud platform offering a suite of generative AI models and governance tools designed to meet the stringent security and compliance requirements of public sector agencies.

- In February, 2025, Databricks Inc. acquired a prominent AI observability startup for approximately USD 500 million, enhancing its Lakehouse AI platform with advanced model monitoring and performance management capabilities to ensure enterprise-grade reliability.

- In April, 2025, Amazon Web Services Inc. announced a USD 2 billion investment to expand its sovereign cloud and AI infrastructure in Southeast Asia, launching new data center regions in Malaysia and Thailand to support growing enterprise demand for localized generative AI services.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Enterprise Generative AI Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 290 |

| Base year | 2024 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 36.2% |

| Market growth 2025-2029 | USD 9243.5 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 30.7% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, The Netherlands, Spain, Italy, UAE, Saudi Arabia, Israel, South Africa, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Enterprise Generative AI market is defined by a strategic arms race toward vertical integration stacks, a trend compelling boardroom decisions on long-term capital allocation for custom AI silicon. This move is driven by the need for optimized neural network architecture and more efficient foundation model development.

- The landscape is populated by a range of technologies, from proprietary AI models to open-source models, all accessible via cloud-based deployment or hybrid AI infrastructure. Key applications gaining traction include content creation automation, code generation tools, and advanced data augmentation techniques using synthetic data generation.

- Organizations are deploying AI-powered chatbots and virtual assistants for operational efficiency AI, while leveraging AI copilots for complex cognitive process automation tasks such as generative design and research assistance tools. Successful deployment relies on robust AI governance frameworks to manage AI ethics and model bias mitigation.

- Firms are utilizing prompt engineering and retrieval-augmented generation (RAG) to refine outputs, with some achieving a 30% reduction in data processing times. As adoption scales, managed AI services and API-based AI access become critical for on-premise AI deployment, sales enablement AI, and knowledge management AI.

What are the Key Data Covered in this Enterprise Generative AI Market Research and Growth Report?

-

What is the expected growth of the Enterprise Generative AI Market between 2025 and 2029?

-

USD 9.24 billion, at a CAGR of 36.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Technology (LLMs, Domain-specific, Multimodal models, Open-source), Application (Content creation, Code generation, Data augmentation, Others), Deployment (Cloud-based, Hybrid, On-premises) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Surging demand for hyper-automation and operational efficiency, Navigating data privacy, security, and intellectual property complexities

-

-

Who are the major players in the Enterprise Generative AI Market?

-

Adobe Inc., AI21 Labs, Amazon Web Services Inc., Anthropic, Cohere, Databricks Inc., Google Cloud, Hugging Face, IBM Corp., Meta Platforms Inc., Microsoft Corp., Mistral AI, NVIDIA Corp., OpenAI, Oracle Corp., Salesforce Inc., SAP SE, Scale, ServiceNow Inc. and Snowflake Inc.

-

Market Research Insights

- The market is defined by a push for intelligent automation and enterprise-grade AI solutions that deliver measurable outcomes. As businesses integrate AI-driven workflow automation, they report significant gains, with some achieving a 30% acceleration in their AI development lifecycle.

- This drive for efficiency is fueling the adoption of model-as-a-service (MaaS) platforms, which improve AI model performance benchmarks and lower initial investment. The focus is on creating secure AI environments and enabling AI risk management, with private cloud AI deployments growing to address data sovereignty concerns.

- This move toward production-grade AI is supported by a demand for full-stack AI solutions and enhanced enterprise search AI capabilities, which together are helping companies resolve the AI talent gap solutions by empowering existing teams. Firms leveraging these platforms see tangible results, including up to a 25% reduction in repeat customer inquiries.

We can help! Our analysts can customize this enterprise generative ai market research report to meet your requirements.

RIA -

RIA -