Fault Detection and Classification Market Size 2024-2028

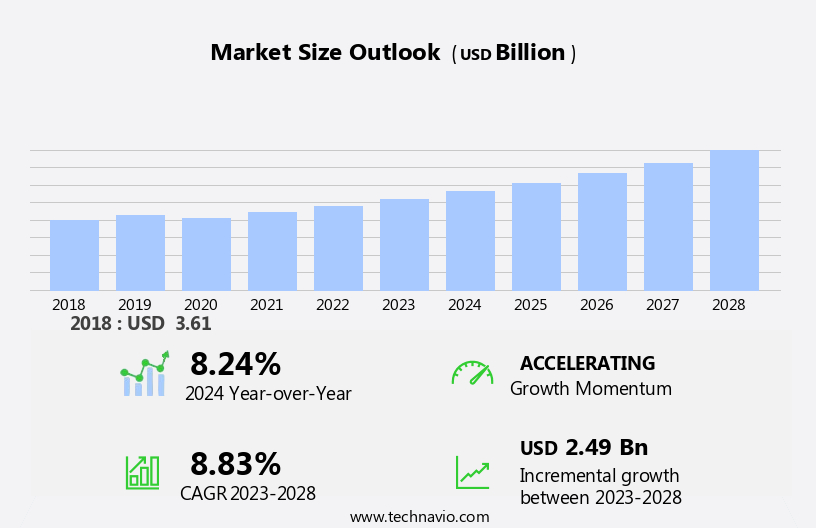

The fault detection and classification market size is forecast to increase by USD 2.49 billion at a CAGR of 8.83% between 2023 and 2028.

- The market is experiencing significant growth due to the increasing complexity in manufacturing processes and the integration of advanced technologies, such as artificial intelligence (AI), into industrial processes. Complex system integration, particularly in the manufacturing industry, is driving the need for robust fault detection and classification systems to ensure operational efficiency and maintain high-quality production processes. Machine vision systems are increasingly being used for inspection and fault diagnosis, employing various classification algorithms to identify and respond to faults in real-time. Fortunately, advancements in computer software, automation, and data-driven technologies offer data-driven solutions for early fault detection and classification. Real-time monitoring of vehicle components and industrial systems enables manufacturers to respond to abnormalities before they escalate into costly repairs.

- Moreover, these systems enable quality control to be performed more accurately and efficiently than with human senses alone. Throughput and response times are critical factors in the manufacturing industry, making the ability to quickly and accurately identify and classify faults essential for maintaining production and minimizing downtime. Baselines are established to monitor normal operating conditions and detect deviations, enabling proactive intervention and reducing the risk of more significant issues arising. Overall, the market for fault detection and classification solutions is poised for continued growth as industries seek to optimize their operations and improve the reliability of their complex systems.

What will be the Size of the Market During the Forecast Period?

- The industrial sector's increasing reliance on complex systems, such as engine monitoring, cybersecurity, and equipment reliability, has led to a significant demand for advanced fault detection and classification solutions. These systems, which include brake monitoring, remote monitoring, and transmission monitoring, among others, are integral to ensuring operational efficiency, system integration, and industrial data analysis. Fault detection and classification play a crucial role in optimizing cost and improving asset management in industries, such as semiconductor manufacturing and supply chain resilience.

- With the advent of Industry 4.0 and the Internet of Things (IoT), real-time diagnostics and predictive maintenance have become essential components of industrial operations. Error identification and anomaly detection are the foundation of fault detection and classification. Machine health monitoring and automated fault diagnosis enable proactive maintenance, reducing production downtime and increasing operational efficiency. Advanced analytics, condition monitoring, and sensor data analysis are key components of these solutions, providing data-driven decision-making capabilities. Cybersecurity is a critical aspect of fault detection and classification, ensuring the protection of complex systems from potential threats. Malfunction investigation and production line monitoring are essential for maintaining industrial data analysis and optimizing processes.

- Additionally, the market for fault detection and classification solutions is driven by several factors. The need for system integration and operational efficiency is a significant driver, as is the increasing complexity of industrial systems and the requirement for preventive maintenance. The adoption of digital twins and smart manufacturing is also fueling growth in this market. The cost optimization benefits of fault detection and classification are substantial. By identifying and addressing issues before they escalate, organizations can save on maintenance costs and minimize production downtime. Additionally, these solutions enable predictive maintenance, allowing for more efficient use of resources and improved asset management.

- Further, fault classification is a critical component of fault detection and classification, enabling organizations to prioritize maintenance activities and allocate resources effectively. By categorizing faults based on their severity and impact, organizations can focus on critical issues and prevent minor issues from escalating into major problems. In conclusion, the market for fault detection and classification solutions is growing rapidly, driven by the increasing complexity of industrial systems, the need for operational efficiency, and the adoption of Industry 4.0 and IoT technologies. These solutions provide significant benefits, including cost optimization, improved asset management, and enhanced cybersecurity. By investing in advanced fault detection and classification solutions, organizations can ensure the reliability and efficiency of their complex industrial systems.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Manufacturing

- Packaging

- Component

- Hardware

- Software

- Services

- Geography

- APAC

- China

- Japan

- North America

- US

- Europe

- Germany

- UK

- Middle East and Africa

- South America

- APAC

By Application Insights

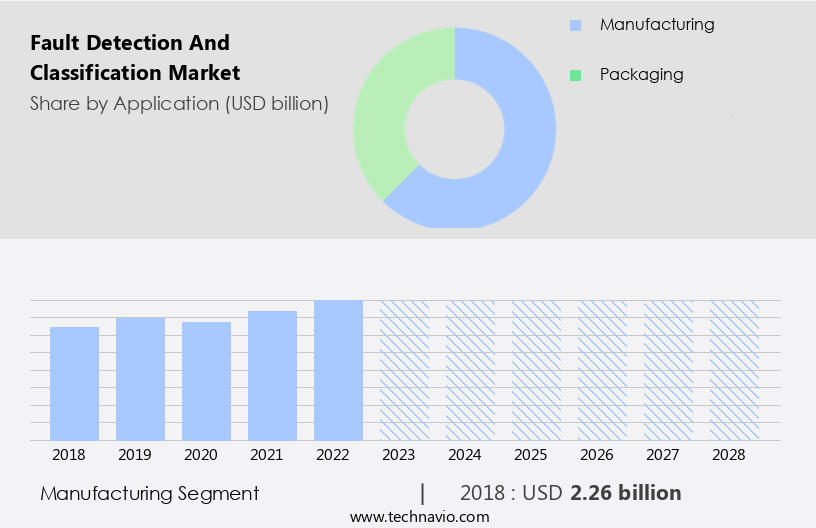

- The manufacturing segment is estimated to witness significant growth during the forecast period.

In the manufacturing sector, minor glitches or production halts can significantly affect productivity and profitability. Early identification of faults through advanced detection systems is crucial to minimize downtime and maintain optimal equipment performance. Unforeseen production stoppages can lead to substantial financial losses. By implementing fault detection solutions, manufacturers can predict and prevent unexpected breakdowns, thereby reducing associated repair costs and optimizing maintenance schedules. Maintaining product quality is a top priority in the industry. Fault detection systems can identify anomalies in the production process, preventing the manufacture of defective products and preserving quality standards. Expensive machinery and equipment are essential assets in manufacturing facilities.

Fault detection technologies assist in monitoring their health, extending their operational life, and enhancing their overall performance. The integration of Industry 4.0 technologies, such as machine learning algorithms and autonomous fault detection, further streamlines the manufacturing process and improves system reliability. Manufacturing workers depend on the seamless operation of transportation systems to ensure the timely movement of goods. Fault detection solutions can identify potential issues in these systems, preventing delays and minimizing waste. Transmission line faults can cause significant disruptions in power supply, affecting both production and worker safety. Advanced fault detection systems can quickly identify and classify these anomalies, ensuring uninterrupted power supply and reducing the risk of accidents.

In conclusion, fault detection and classification solutions play a vital role in enhancing productivity, ensuring accuracy, and improving system reliability in the manufacturing sector. These technologies help monitor complex operating conditions, reduce downtime, and optimize the performance of expensive machinery and equipment. By implementing advanced fault detection systems, manufacturers can maintain product quality, minimize waste, and create a safer working environment.

Get a glance at the market report of share of various segments Request Free Sample

The manufacturing segment was valued at USD 2.26 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

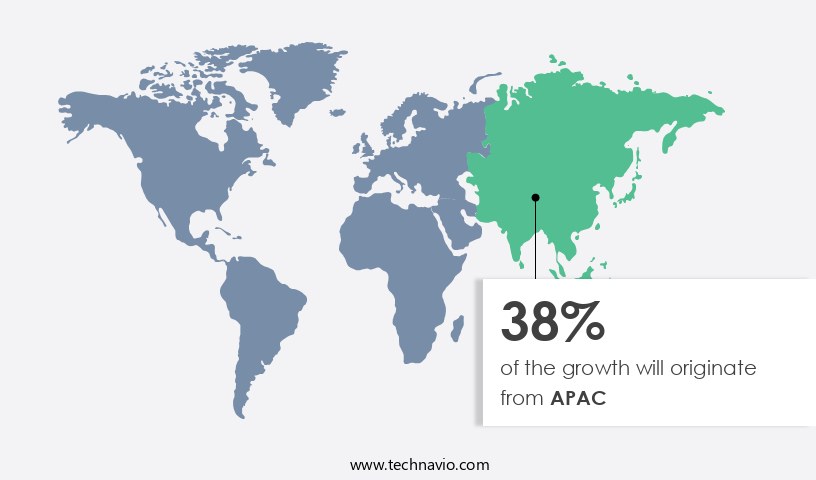

- APAC is estimated to contribute 38% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

In the Asia Pacific (APAC) region, industries such as manufacturing, automotive, electronics, and energy are experiencing significant growth. With this expansion comes the increased importance of minimizing equipment downtime and addressing electrical malfunctions, engine misfires, and other disruptions in real-time. To meet these demands, APAC industries are adopting Industry 4.0 practices, including automation, IoT, and data analytics. Fault detection systems play a crucial role in this trend, allowing for data-driven maintenance and predictive analysis of vehicle components and industrial machinery. Furthermore, in a region prioritizing energy efficiency, these solutions enable the monitoring of energy consumption, optimization of processes, and identification of inefficiencies for resource conservation.

As infrastructure development continues to expand in APAC, fault detection systems become essential for maintaining the health and reliability of critical infrastructure such as power grids, transportation systems, and utilities. By implementing these solutions, industries can reduce maintenance costs, enhance vehicle performance, and ensure operational excellence.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of Fault Detection and Classification Market?

Increasing complexity in the manufacturing process is the key driver of the market.

- The intricacy of modern systems and equipment in various industries has led to heightened demand for advanced fault detection solutions. As systems become increasingly interconnected, the likelihood of electrical malfunctions, engine misfires, disruptions, and other malfunctions in vehicle components, engines, automation, and manufacturing processes increases. To mitigate these issues, industries are integrating technologies such as computer software, real-time monitoring, machine learning, and data-driven analysis. Fault detection systems enable early identification of anomalies, improving system reliability and operational efficiency. These solutions are particularly crucial in industries with high equipment downtime costs, such as manufacturing, process industries, and the automotive sector.

- Further, fault detection devices, sensors, and machine vision systems help diagnose faults in complex systems, ensuring optimal vehicle performance and reducing maintenance costs. In the automotive segment, fault detection is essential for fuel efficiency, engine performance, and safety. Semiconductor manufacturers and automotive applications rely on application-specific integrated circuits and AI models for autonomous fault detection and deep learning models for predictive maintenance. In the energy sector, real-time monitoring of transmission line faults and power plant performance is vital for system failure prevention and productivity enhancement.

- In conclusion, customized solutions, including integration of robotics and machine learning algorithms, are increasingly popular. These solutions enable accurate classification of faults and responses, ensuring timely maintenance and minimizing downtime. As industries continue to adopt advanced technologies, the importance of fault detection systems in maintaining system performance, product quality, and worker safety will only grow.

What are the market trends shaping the Fault Detection and Classification Market?

Integration of AI with industrial processes is the upcoming trend in the market.

- The integration of Industry 4.0 technologies, such as IoT, AI, and machine learning, has significantly increased automation in various industries. This automation relies on the seamless functioning of machinery and processes, making fault detection systems essential. IoT sensors and devices collect copious amounts of data from industrial equipment, which is vital for fault detection systems. By analyzing patterns, trends, and abnormalities in this data, potential faults can be identified and addressed proactively. Predictive maintenance is facilitated through real-time data analysis, enabling preventive measures before equipment downtime occurs. The manufacturing, process industries, automotive, and energy sectors are among those benefiting from these advancements.

- Also, fault detection systems enhance operational efficiency, productivity, and system reliability while reducing maintenance costs and vehicle downtime. Application-specific integrated circuits, machine learning algorithms, and robotics play a crucial role in the integration and deployment of these systems. Semiconductor manufacturers and AI models are key contributors to the development of advanced fault detection solutions. In the automotive segment, fault detection devices monitor engine misfires, electrical malfunctions, fuel system faults, and transmission issues. In the packaging sector, sensors detect anomalies in packaging lines and brakes.

- In the manufacturing industry, machine vision systems ensure product quality and inspection, while in the energy sector, real-time monitoring of transmission line faults is crucial. Customized solutions cater to specific industry needs, ensuring scalability and integration with existing systems. The deployment of these systems is expected to continue, as the importance of early fault detection and classification becomes increasingly apparent.

What challenges does Fault Detection and Classification Market face during the growth?

Complex system integration is a key challenge affecting market growth.

- The market encompasses various industries, including manufacturing, automotive, and energy, where minimizing equipment downtime and ensuring system reliability are paramount. Electrical malfunctions in engines, engine misfires, and disruptions in vehicle components can significantly impact vehicle performance and incur substantial maintenance costs. Real-time monitoring of these malfunctions using computer software, automation, and fault-detection devices is essential for early detection and classification. In the manufacturing industry, fault detection is crucial for maintaining operational efficiency, productivity, and product quality. Machine learning algorithms, AI models, and deep learning models are increasingly being used for fault detection and classification in complex systems.

- Also, application-specific integrated circuits and sensor data play a vital role in detecting anomalies and system failures. In the automotive segment, fault detection is essential for maintaining fuel efficiency, ensuring safety, and minimizing vehicle downtime. Semiconductor manufacturers are developing customized solutions for automotive applications, including fault detection systems for transmissions, fuel systems, and brakes. The integration of fault detection systems into existing infrastructure can be complex, requiring expertise in data science, machine learning, and domain-specific knowledge. Bridging the gap between these disciplines within a team or finding individuals with a multidisciplinary skill set can be challenging. However, the benefits of early fault detection and classification, including reduced downtime, improved system performance, and increased productivity, make it a worthwhile investment for businesses across various industries.

- In the packaging sector, fault detection is critical for maintaining throughput and ensuring product quality. Machine vision systems and inspection technologies are used to detect defects and anomalies in packaging materials and products. The deployment times for these systems can be significant, and the response to faults must be quick to minimize waste and maintain production processes. In the energy sector, fault detection is essential for maintaining the reliability of power plants and transmission lines. Sensor data and AI models are used to detect anomalies and respond to fault scenarios in real-time. Government measures and regulations are driving the adoption of fault detection systems in this sector to ensure system reliability and prevent costly system failures.

- Overall, The market is expected to grow significantly during the forecast period due to the increasing demand for early fault detection and classification in various industries. The integration of fault detection systems into existing infrastructure and the development of accurate and customized solutions will continue to be key challenges for market growth.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Amazon.com Inc.

- Applied Materials Inc.

- Clockworks Analytics

- Cognex Corp.

- DNV Group AS

- einnoSys Technologies Inc.

- elunic AG

- INFICON Holding AG

- Keyence Corp.

- KLA Corp.

- Microsoft Corp.

- OMRON Corp.

- Siemens AG

- Synopsys Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

In today's industrial and transportation sectors, fault detection and classification are crucial for minimizing equipment downtime and maintaining optimal vehicle performance. Electrical malfunctions, engine misfires, and other disruptions can lead to significant losses in income levels, especially in process industries like manufacturing and automotive segments. Application-specific integrated circuits and machine learning algorithms play a vital role in fault detection and classification.

In summary, these technologies enable the identification of complex fault scenarios and the development of customized solutions for various industries, including packaging, energy, and transportation. Fault detection devices, such as sensors and machine vision systems, provide valuable data for classification algorithms. These algorithms analyze sensor data and compare it to baselines to identify anomalies and classify faults. The manufacturing industry benefits significantly from autonomous fault detection and classification, improving system reliability and operational efficiency. Skilled professionals can leverage AI models like AutoML and deep learning models to diagnose process issues and optimize production processes. The integration of robotics and machine learning further enhances the capabilities of fault detection and classification systems, enabling faster deployment times and increased scalability. As the importance of fault detection and classification continues to grow, it's essential to stay informed about the latest trends and government measures in this field.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

162 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.83% |

|

Market growth 2024-2028 |

USD 2.49 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

8.24 |

|

Key countries |

US, China, Japan, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -