Fermented Food And Drinks Market Size 2024-2028

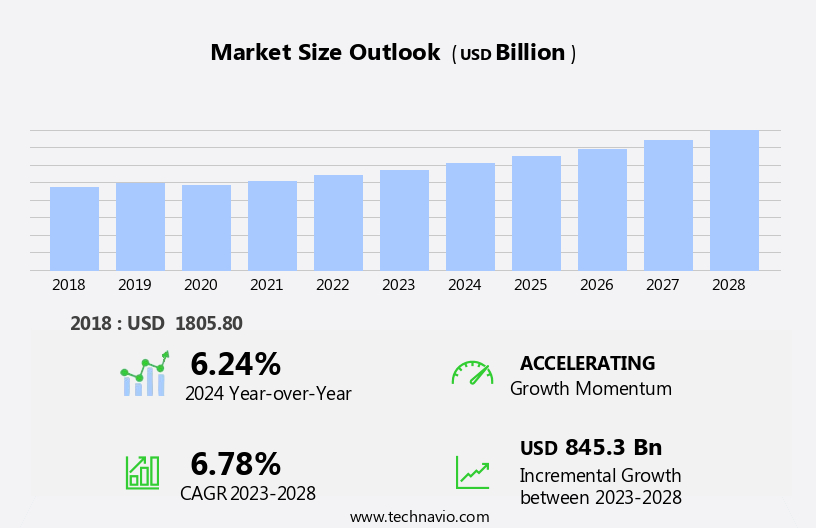

The fermented food and drinks market size is forecast to increase by USD 845.3 billion at a CAGR of 6.78% between 2023 and 2028.

- The market is experiencing significant growth driven by advances in packaging methods that extend shelf life and maintain product quality. This development is particularly notable in the beverage segment, where consumers increasingly seek convenient, on-the-go options for fermented drinks. Another key trend is the rising popularity of probiotics, which are gaining traction as consumers become more health-conscious and seek out foods and beverages that support gut health. However, the market is not without challenges. Substitute products, such as artificial alternatives and non-fermented probiotic supplements, pose a threat to market growth.

- To capitalize on opportunities and navigate these challenges effectively, companies should focus on innovation, product differentiation, and targeted marketing efforts to appeal to health-conscious consumers. By staying attuned to market dynamics and consumer preferences, market players can position themselves for long-term success in this dynamic and growing market.

What will be the Size of the Fermented Food And Drinks Market during the forecast period?

- The market in the United States continues to gain momentum, driven by consumer interest in wellness, digestive health, and the desirable sensory attributes of taste and texture. This market encompasses a wide range of products, including fermented beverages like kombucha and functional drinks, which offer digestibility benefits and nutritional content. Consumers increasingly seek out these options as remedies for various health problems, such as digestive disorders and obesity prevention.

- The market's growth is fueled by innovations in fermentation procedures, resulting in enhanced nutritional value, longer shelf life, and increased antioxidant activity. Consumers are drawn to the unique flavors and culinary experiences that fermented foods and drinks provide, making them a popular choice for those seeking health benefits and enjoyment.

How is this Fermented Food And Drinks Industry segmented?

The fermented food and drinks industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- Fermented alcoholic and non-alcoholic drinks

- Fermented diary food and drinks

- Fermented bakery food

- Others

- Distribution Channel

- Hypermarkets and supermarkets

- Independent retailers and convenience store

- Specialty food stores

- Online retailers

- Geography

- APAC

- China

- Japan

- Europe

- France

- Germany

- North America

- US

- South America

- Middle East and Africa

- APAC

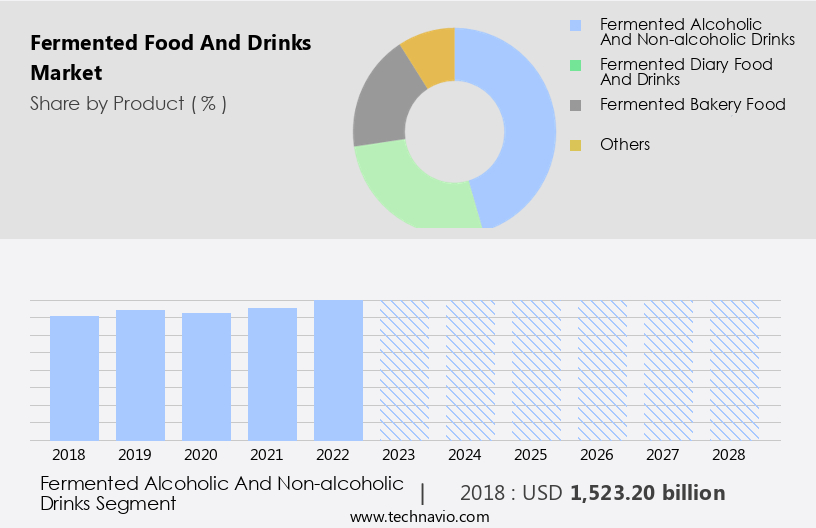

By Product Insights

The fermented alcoholic and non-alcoholic drinks segment is estimated to witness significant growth during the forecast period.

The market encompasses a range of alcoholic and non-alcoholic beverages, including wine, beer, cider, and kombucha. Wine, an alcoholic drink produced through the fermentation of grapes or other fruits, holds a significant share in the global alcoholic drinks market. Europe, particularly in countries like Germany, France, and Italy, is a mature market for wine. However, the APAC region presents the greatest expansion opportunities for manufacturers due to the increasing influence of Western culture. To cater to this growing demand, producers are expanding their base and increasing wine production worldwide. Fermented non-alcoholic drinks, such as kombucha, tempeh, sauerkraut, and kefir, offer numerous health benefits.

These foods are rich in nutritive value, including prebiotics, probiotics, and bioactive molecules. Consumer health consciousness and the rise of plant-based diets have fueled the demand for these foods. Innovations in smart packaging techniques and functional beverages have also attracted a wider consumer base. The fermentation process plays a crucial role in preserving the nutritional quality and taste of these foods while ensuring food safety and environmental sustainability. The market for fermented foods and drinks is expected to continue growing due to their health benefits, including improved digestion, immunity, and weight management. Consumer preferences for digestive disorders and wellness have also driven the market's growth.

Fermented alcoholic beverages, such as beer and wine, are not only enjoyed for their taste but also for their probiotic content and potential health benefits. However, the risk of contamination and shelf life are critical factors that manufacturers must consider to maintain consumer trust and safety. The market for fermented foods and drinks offers numerous opportunities for innovation, with a focus on natural compounds, antioxidant activity, and anti-inflammatory properties. The market also includes infant probiotics and dietary supplements. Producers must ensure the highest standards of food safety and environmental sustainability to meet consumer expectations and stay competitive.

Get a glance at the market report of share of various segments Request Free Sample

The Fermented alcoholic and non-alcoholic drinks segment was valued at USD 1523.20 billion in 2018 and showed a gradual increase during the forecast period.

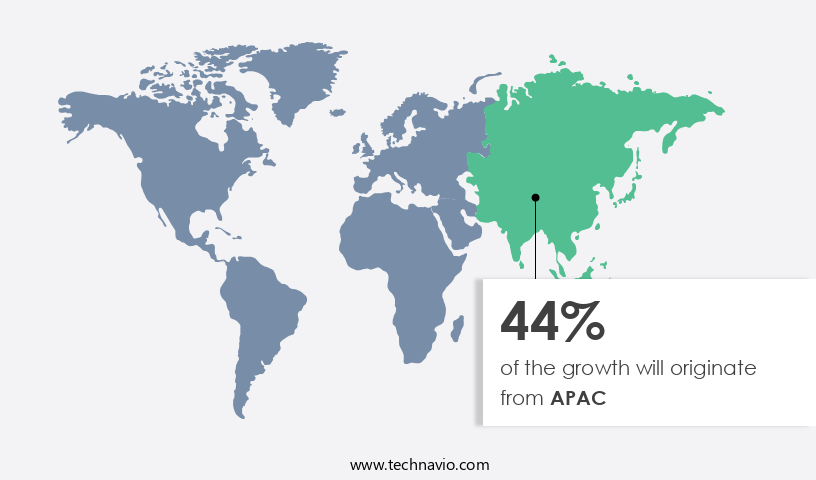

Regional Analysis

APAC is estimated to contribute 44% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The market is experiencing significant growth due to increasing consumer health consciousness and the recognition of the nutritive value of fermented products. Gut health is a key focus area, with veganism and plant-based diets gaining popularity driving demand for fermented foods like Tempeh and prebiotics. Innovations in fermentation processes, smart packaging techniques, and historical analysis are enhancing the market's expansion. Fermented beverages, including Bottlebrush Ferments, Kefir, Wine, and Beer, offer health benefits such as probiotic content, improved digestibility, and immunity support. The market caters to various consumer preferences, from sauerkraut and Kimchi for digestive disorders to dairy-based fermented foods for energy boost and taste enhancement.

Producers are focusing on the preservation of products and food safety while ensuring environmental sustainability and minimal environmental impact. Functional beverages, such as Remedy Kombucha, are gaining popularity for their antioxidant activity, anti-atherosclerotic properties, and anti-inflammatory benefits. Consumer interest in healthy eating habits and wellness has led to the production of infant probiotics and dietary supplements. The market's growth is driven by the increasing demand for fermented foods and beverages, with supermarkets and specialty stores catering to this trend. The fermentation process plays a crucial role in enhancing the nutritional quality of foods and beverages, providing essential nutrients and bioactive molecule content.

However, contamination risks and shelf life concerns necessitate ongoing research and innovation to ensure consumer safety and satisfaction. The market's growth is expected to continue as consumers seek out fermented foods and beverages for their health benefits and unique sensory attributes.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Fermented Food And Drinks Industry?

- Advances in packaging methods is the key driver of the market.

- Fermented food and drinks have gained popularity in the market due to their health benefits and unique flavors. companies in this industry focus on innovative packaging solutions to make their products more convenient for consumers. One such packaging option is stand-up pouches, which offer several advantages. These lightweight and portable containers are easier to carry than traditional jars, making the products more appealing for on-the-go consumption. The use of stand-up pouches also reduces logistics costs for producers, as they require less resources to ship compared to heavy packaging.

- As a result, the adoption of such packaging is likely to increase the likelihood of fermented food and drinks becoming a regular grocery item for consumers. The convenience and portability of these products, coupled with their health benefits, make them an attractive choice for health-conscious consumers.

What are the market trends shaping the Fermented Food And Drinks Industry?

- Rise in popularity of probiotics is the upcoming market trend.

- Fermented foods and drinks, particularly those rich in probiotics, have gained significant attention in the health and wellness industry. These foods are produced through the process of fermentation, during which beneficial bacteria convert sugars and starches into lactic acid, preserving the food and enhancing its nutritional value. Probiotics, found in cultured or fermented dairy products such as yogurt, kefir, whey, raw cheese, and raw milk, offer various vitamins and minerals while maintaining a healthy balance of gut flora. Vegetables like cabbage, cucumber, beetroot, carrot, and pepper undergo lacto-fermentation, extending their shelf life and increasing their nutritional benefits. Probiotics have been shown to strengthen the immune system, reducing the occurrence of respiratory infections and the need for antibiotics.

- Regular consumption of probiotic-rich foods, especially during childhood, can lower the risk of influenza and frequent sickness. The inherent advantages of probiotics have led healthcare professionals to endorse their inclusion in daily diets for overall health and well-being.

What challenges does the Fermented Food And Drinks Industry face during its growth?

- Presence of substitute products is a key challenge affecting the industry growth.

- The market encounters challenges from various substitute products available in the market. These substitutes, including baked goods, biscuits, confectionery, sauces, soups, and dairy products, can serve as alternatives to fermented food and drinks in various culinary applications. The market is witnessing an increasing number of launches and innovations in these substitute categories, which may hinder the growth of the market during the forecast period.

- Consequently, the presence of these alternatives poses a significant challenge to the market's expansion.

Exclusive Customer Landscape

The fermented food and drinks market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the fermented food and drinks market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, fermented food and drinks market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Anheuser Busch InBev SA NV - The company specializes in producing and marketing fermented food and beverage products, including beer. Through innovative processes and a commitment to quality, these offerings provide consumers with unique and flavorful options in the global market. The fermentation process enhances the natural flavors and nutritional benefits of the ingredients, resulting in delicious and healthful choices. With a focus on sustainability and consumer satisfaction, the company's diverse product line caters to various tastes and dietary preferences.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Anheuser Busch InBev SA NV

- Carlsberg Breweries AS

- Chobani Global Holdings LLC

- Chr Hansen Holding AS

- COFCO Corp.

- Constellation Brands Inc.

- Danone SA

- DuPont de Nemours Inc.

- Fonterra Cooperative Group Ltd.

- General Mills Inc.

- Heineken NV

- Koninklijke DSM NV

- Lifeway Foods Inc.

- Nestle SA

- PepsiCo Inc.

- Suntory Holdings Ltd.

- The Coca Cola Co.

- The Kraft Heinz Co.

- Treasury Wine Estates Ltd.

- Yakult Honsha Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The fermented food and drink market continues to gain traction as consumers increasingly prioritize gut health and plant-based diets. This trend is driven by the nutritive value of fermented foods and beverages, which offer various health benefits. These benefits include improved digestibility, enhanced immunity, and the presence of prebiotics and probiotics. Historically, fermentation has been used as a means of food preservation and enhancing flavor. However, modern innovations have expanded the market beyond traditional offerings. For instance, the use of smart packaging techniques and online portals has made it easier for consumers to access a wider range of fermented products.

The growing consumer health consciousness has led to an increase in demand for fermented foods and beverages. This trend is particularly noticeable in the plant-based food sector, where tempeh, sauerkraut, and kimchi have gained popularity. The use of natural compounds, such as antioxidants and anti-inflammatory agents, further adds to the nutritional quality of these products. Fermented alcoholic beverages, such as beer and wine, have also seen a rence in recent years. While these beverages offer some health benefits, it is essential to be mindful of their toxicity levels. Producers are addressing this concern by focusing on the probiotic content and antioxidant activity of their products.

The market for fermented foods and beverages is not limited to traditional supermarkets and specialty stores. Online platforms have emerged as a significant distribution channel, making it easier for consumers to access these products from the comfort of their homes. This trend is particularly noticeable in the area of infant probiotics, where online sales have grown significantly. The market for fermented foods and beverages is not without its challenges. Food safety and environmental sustainability are critical concerns for consumers. Producers must ensure that their products are free from contamination risk and have an acceptable shelf life. Sensory attributes, such as taste and texture, are also essential considerations for consumers.

Despite these challenges, the market for fermented foods and beverages is expected to continue expanding. The trend towards plant-based diets and consumer interest in health and wellness are driving demand for these products. Innovations in fermentation procedures and the use of natural compounds are also expected to contribute to the growth of the market. In , the fermented food and drink market is poised for continued growth as consumers increasingly prioritize gut health and plant-based diets. Producers must focus on food safety, environmental sustainability, and innovation to meet consumer preferences and stay competitive in this dynamic market.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

194 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.78% |

|

Market growth 2024-2028 |

USD 845.3 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.24 |

|

Key countries |

US, China, Germany, Japan, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Fermented Food And Drinks Market Research and Growth Report?

- CAGR of the Fermented Food And Drinks industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the fermented food and drinks market growth of industry companies

We can help! Our analysts can customize this fermented food and drinks market research report to meet your requirements.

RIA -

RIA -