Financial Service Application Market Size 2025-2029

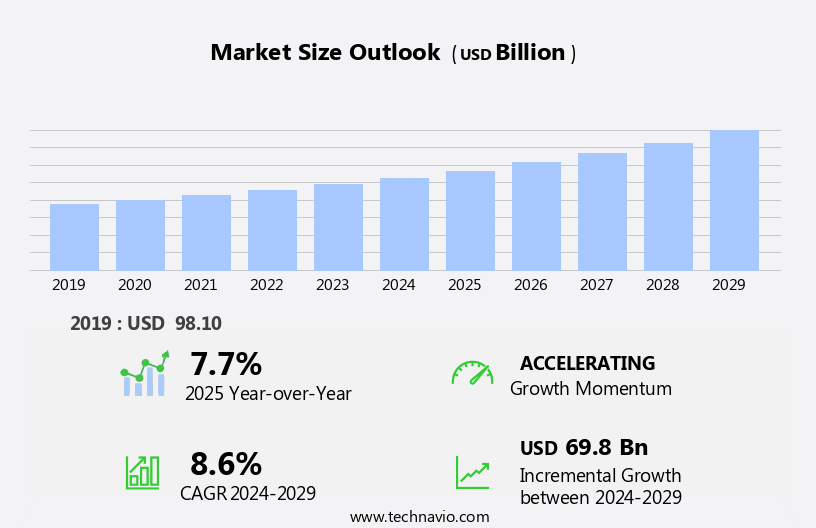

The financial service application market size is forecast to increase by USD 69.8 billion, at a CAGR of 8.6% between 2024 and 2029.

- The market is experiencing significant growth, driven by increasing government initiatives to digitalize the financial sector. This shift towards digitization is fueled by a growing recognition of the benefits it brings, including increased efficiency and accessibility. Software development and Network Security ensure the reliability and security of financial applications. However, this trend is not without challenges. One of the most pressing concerns is the rising awareness among customers about finance and digitization, which places heightened importance on the security and privacy of financial data. As a result, financial institutions must prioritize robust security measures to mitigate potential risks and maintain customer trust.

- Additionally, privacy concerns continue to pose a challenge, with stringent regulations requiring strict adherence to data protection policies. Navigating these challenges will be crucial for companies seeking to capitalize on the opportunities presented by the digital transformation of the financial sector. By focusing on innovative solutions that address these concerns, organizations can differentiate themselves and position themselves for long-term success.

What will be the Size of the Financial Service Application Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

The market continues to evolve, with technology playing a pivotal role in shaping the industry's dynamics. Machine learning algorithms are integrated into investment platforms for predictive analysis and algorithmic trading, enhancing the efficiency of financial transactions. Tax planning tools assist users in optimizing their tax liabilities, while user interfaces are designed to offer seamless experiences. Wealth management and estate planning applications provide comprehensive solutions for managing assets and legacy planning. Account management and risk management tools enable users to monitor and mitigate financial risks.

Savings accounts, interest rates, and digital wallets offer convenience and flexibility for managing personal finances. Payment gateways and processing systems facilitate secure transactions, while fraud detection and data analytics help prevent financial losses. Insurtech and insurance products leverage technology to streamline insurance processes, from customer onboarding to claims processing. Open banking and loan origination systems enable financial institutions to offer more personalized services. High-frequency trading and financial modeling tools cater to the needs of institutional investors. Retirement planning tools help individuals plan for their future, while blockchain technology ensures secure and transparent transactions. The continuous unfolding of market activities and evolving patterns underscores the importance of staying informed and adaptable in the ever-changing market.

How is this Financial Service Application Industry segmented?

The financial service application industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

- Large enterprises

- SMEs

- Deployment

- On-premises

- Cloud-based

- Application

- Banking

- Payment gateways

- Insurance

- Wealth management

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Switzerland

- UK

- APAC

- China

- India

- Japan

- South America

- Brazil

- Rest of World (ROW)

- North America

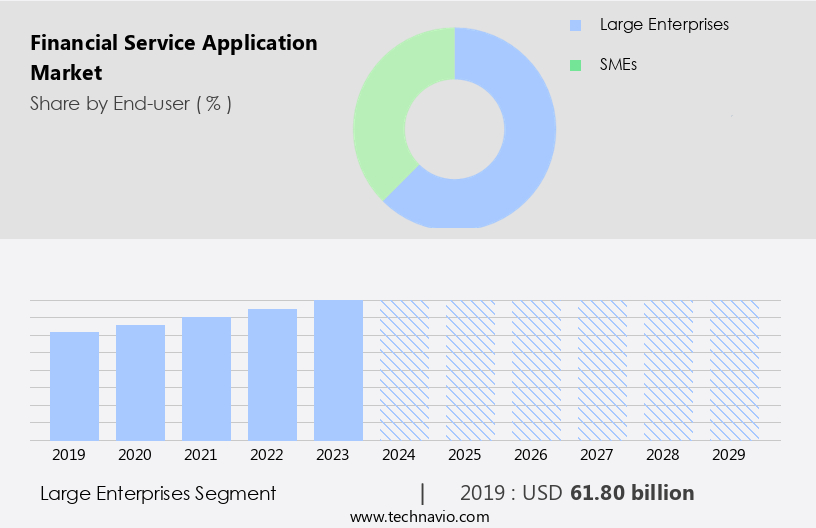

By End-user Insights

The large enterprises segment is estimated to witness significant growth during the forecast period. The market is experiencing significant growth due to the increasing adoption of digital payments and online banking services. Companies in the banking, financial services, and insurance (BFSI), IT, and manufacturing sectors are major contributors to this trend, as they generate a large volume of transactions. The expansion of BFSI enterprises and the intensification of intraregional cross-border banking activity are also driving the demand for financial service applications. Modern vending machines equipped with contactless and card-based payments are another factor fueling market growth. Financial technology (fintech) innovations, such as fraud detection, data analytics, algorithmic trading, and API integration, are enhancing the functionality of financial service applications.

cloud computing, data security, and user experience (UX) are also critical factors influencing the market's evolution. Insurance technology (insurtech) and machine learning (ML) are transforming the insurance industry, leading to the development of new insurance products and services. Mobile banking, investment platforms, and digital wallets are becoming increasingly popular, offering convenience and accessibility to customers. Wealth management, estate planning, account management, risk management, and tax planning are also key areas where financial service applications are making a significant impact. High-frequency trading, loan origination systems, financial modeling, and portfolio management are other applications that are gaining traction. Open banking and big data are emerging trends in the financial services industry, enabling more personalized and efficient services.

Retirement planning and blockchain technology are also areas of interest, offering new opportunities for innovation and growth. The market is expected to continue its upward trajectory, driven by these trends and the increasing demand for digital financial services.

The Large enterprises segment was valued at USD 61.80 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

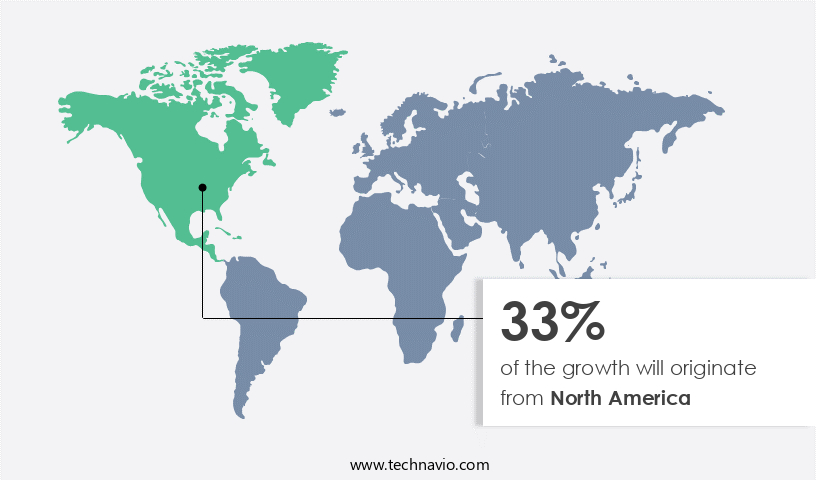

North America is estimated to contribute 33% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in North America is experiencing significant growth, accounting for the largest share in the global market in 2024. This expansion is driven by the rapid advancement of digital connectivity and the increasing presence of prominent companies in the region. The proliferation of online trading and finance platforms, technological innovations, evolving business and finance environments, and the presence of local and global players are fueling the market's growth. Banks and financial institutions in North America are embracing technology, with IoT integration being a notable trend. For instance, Bank of America, a leading US-based banking and financial services institution, has made strides in enhancing its mobile wallet capabilities for corporate clients.

Financial technology is revolutionizing the industry, with mobile application development, payment gateways, and processing gaining popularity. Debit cards, exchange-traded funds (ETFs), and investment platforms are increasingly being accessed via mobile devices. Data security, fraud detection, and customer support are essential components of these applications, ensuring a seamless user experience (UX). Artificial intelligence (AI) and machine learning (ML) are transforming financial services, enabling algorithmic trading, risk management, and tax planning. Data analytics and financial modeling are crucial for portfolio management, open banking, and retirement planning. Cloud computing, network security, and user interface (UI) design are essential for the development and implementation of these applications.

Savings accounts, checking accounts, mutual funds, and insurance products are also being offered through digital channels. Digital wallets, credit cards, and loan origination systems are streamlining transactions and reducing transaction fees. High-frequency trading, wealth management, estate planning, account management, and risk management are other areas benefiting from the advancements in financial technology. Big data and blockchain technology are also gaining traction, offering new opportunities for innovation and growth. The integration of artificial intelligence and big data in financial applications offers endless possibilities for innovation.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Financial Service Application Industry?

- The government's escalating efforts to digitize the financial sector serve as the primary catalyst for market growth. The market is witnessing significant growth due to the increasing government investment in digitizing the financial sector. This trend is driven by the need for improved work efficiency and flexibility across financial institutions. However, data security remains a major concern, leading to the increased adoption of advanced technologies such as data encryption and artificial intelligence (AI) for enhancing data security. Cloud computing is also gaining popularity in the financial sector due to its ability to provide scalability and cost savings. Financial service applications offer various features such as mobile banking, checking accounts, investment platforms, and insurance products.

- Customer onboarding and support are also crucial aspects of these applications, ensuring a seamless user experience. Mutual funds and insurance technology (insurtech) are some of the key areas where financial service applications are making a significant impact. Despite the benefits, the threat of data breaches continues to pose a challenge, necessitating continuous innovation and investment in data security solutions.

What are the market trends shaping the Financial Service Application Industry?

- The increasing importance of customer awareness regarding finance and digitization represents a significant market trend. This developing trend underscores the need for professionals to stay informed about the latest financial technologies and digital solutions. In today's digital age, financial institutions are adapting to disruptive technologies to meet the evolving needs of tech-savvy customers, particularly millennials. These customers prefer IoT platforms for executing daily transactions, leading to the integration of financial services from tech giants like Amazon, Google, Apple, Square, and PayPal into traditional banking networks. Millennials' financial requirements span payments, investments, remittances, crowdfunding, consumer banking, and lending, which are efficiently addressed through FinTech platforms.

- Software development and network security are prioritized to safeguard savings accounts and digital wallets, with interest rates remaining a critical factor. Overall, the market is driven by the demand for advanced technology, convenience, and personalized services. For instance, SimpleTax simplifies income-tax filing by automatically updating tax regulations within the system. Certified by the Canada Revenue Agency, SimpleTax undergoes rigorous testing annually to ensure user-friendliness and 100% accuracy.

What challenges does the Financial Service Application Industry face during its growth?

- The growth of the industry is significantly impacted by privacy and security concerns, which represent a major challenge that must be addressed by professionals in a knowledgeable and formal manner. The market is witnessing significant growth, driven by the increasing adoption of advanced technologies such as user experience (UX) design, financial modeling, portfolio management, and open banking. In the realm of credit cards, UX design plays a pivotal role in attracting and retaining customers. High-frequency trading firms leverage technology for faster and more accurate transactions. Loan origination systems are being modernized with digital solutions, streamlining the application process.

- The market is also witnessing the emergence of new players and business models, fueled by the increasing acceptance of fintech solutions. However, data privacy and security concerns remain key challenges. Policyholders and market leaders must prioritize these issues to ensure customer trust and compliance with regulatory requirements. The adoption of open banking and APIs is expected to further drive innovation and competition in the market. Overall, the market is poised for robust growth, with technology-driven solutions at the forefront. Moreover, the integration of big data and analytics in financial services is revolutionizing retirement planning and investment management. Blockchain technology is another disruptive force, offering enhanced security and transparency.

Exclusive Customer Landscape

The financial service application market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the financial service application market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, financial service application market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accenture PLC - This company specializes in innovative financial services applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture PLC

- Alkami Technology Inc.

- Avaloq Group AG

- Fidelity National Information Services Inc.

- Finastra

- Fiserv Inc.

- Infosys Ltd.

- International Business Machines Corp.

- Mambu BV

- Microsoft Corp.

- NCR Voyix Corp.

- Oracle Corp.

- Perfect Ltd.

- Salesforce Inc.

- SAP SE

- SBS

- ServiceNow Inc.

- SS and C Technologies Holdings Inc.

- Tata Consultancy Services Ltd.

- Temenos AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Financial Service Application Market

- In January 2024, Mastercard and Microsoft announced a strategic partnership to develop digital payment solutions using Microsoft Azure and Mastercard's technology (Mastercard press release, 2024). This collaboration aimed to enhance security and convenience for digital transactions, marking a significant step forward in the financial technology sector.

- In March 2024, Goldman Sachs completed a USD1.5 billion investment round in its digital platform, Marcus by Goldman Sachs, valuing the business at USD7.5 billion (Goldman Sachs press release, 2024). This substantial funding injection underscored the growing importance of digital financial services and the potential for significant returns in this market.

- In May 2024, Visa secured regulatory approval to acquire Plaid, a fintech company specializing in financial data access and transfer services, for approximately USD5.3 billion (Visa press release, 2024). This acquisition was a key strategic move to strengthen Visa's digital capabilities and expand its offerings in the rapidly evolving financial services landscape.

- In February 2025, JPMorgan Chase launched its digital-only bank, Chase FirstBank, in the United Kingdom, marking its first international expansion outside the United States (JPMorgan Chase press release, 2025). This move signaled the bank's commitment to the global digital banking market and its ambition to compete with leading fintech players in Europe.

Research Analyst Overview

In the dynamic financial services application market, governance models continue to evolve, with peer-to-peer lending platforms gaining traction. Vulnerability assessments and encryption algorithms are essential components of secure financial applications, ensuring data protection in decentralized finance (DeFi) and blockchain applications. Financial crime remains a persistent threat, necessitating robust anti-money laundering (AML) and terrorist financing measures. Data governance is crucial, with multi-factor authentication, security protocols, and sanctions screening safeguarding digital assets. Financial inclusion is a growing trend, with non-fungible tokens (NFTs) and decentralized applications (DApps) offering new opportunities for underserved populations. Penetration testing and incident response plans are essential for business continuity in the face of cyber threats.

Biometric authentication, including facial and voice recognition, adds an extra layer of security. Smart contracts and decentralized finance are revolutionizing traditional financial services, but they also introduce new risks. AML and terrorist financing regulations must be integrated into these systems, and business continuity plans must account for the unique challenges posed by decentralized applications. Financial literacy is vital in this complex landscape, with two-factor authentication and sanctions screening becoming standard practices for secure financial transactions. Incident response plans and disaster recovery strategies are essential for mitigating risks and ensuring business resilience.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Financial Service Application Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

220 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.6% |

|

Market growth 2025-2029 |

USD 69.8 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

7.7 |

|

Key countries |

US, UK, China, Germany, Brazil, Canada, India, France, Switzerland, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Financial Service Application Market Research and Growth Report?

- CAGR of the Financial Service Application industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the financial service application market growth of industry companies

We can help! Our analysts can customize this financial service application market research report to meet your requirements.

RIA -

RIA -