Flexible Industrial Packaging Market Size 2026-2030

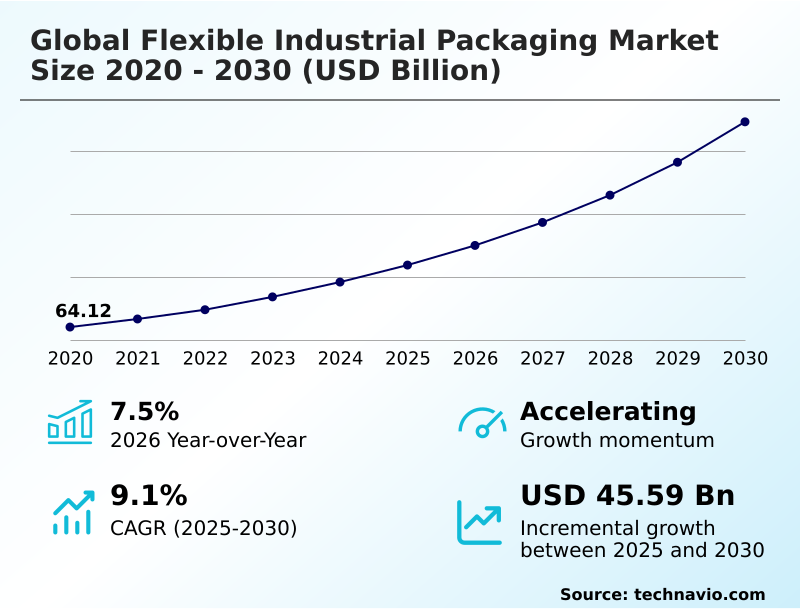

The flexible industrial packaging market size is valued to increase by USD 45.59 billion, at a CAGR of 9.1% from 2025 to 2030. Intensifying focus on sustainability and circular economy models will drive the flexible industrial packaging market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 42% growth during the forecast period.

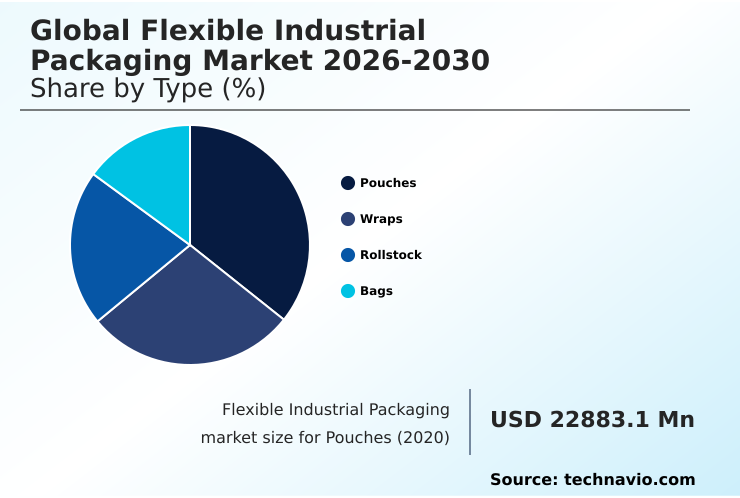

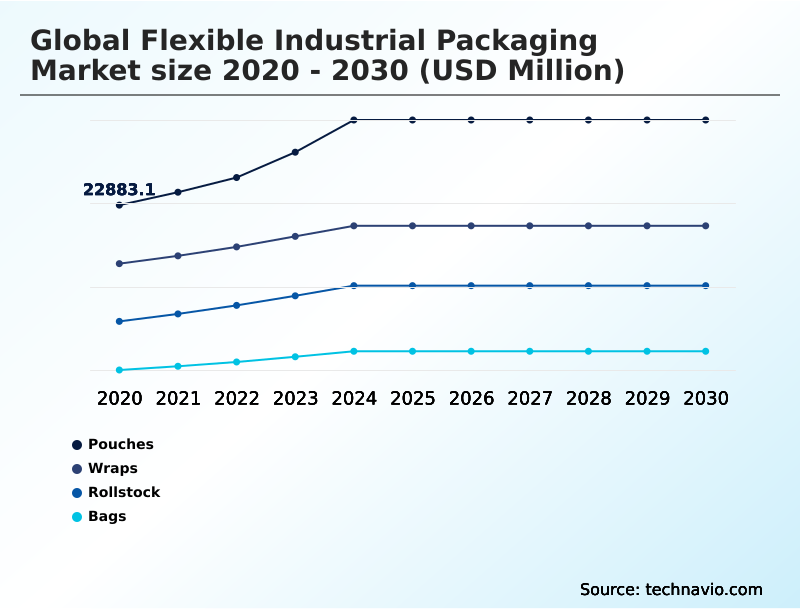

- By Type - Pouches segment was valued at USD 29.75 billion in 2024

- By Application - Chemical industry segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 65.31 billion

- Market Future Opportunities: USD 45.59 billion

- CAGR from 2025 to 2030 : 9.1%

Market Summary

- The flexible industrial packaging market is undergoing a significant transformation, evolving from a focus on basic containment to providing strategic, value-added solutions. This shift is driven by the dual imperatives of supply chain efficiency and sustainability. The adoption of lightweighting and downgauging principles, enabled by innovations in coextrusion technology and polymer science, directly addresses logistical cost pressures.

- Concurrently, a powerful regulatory and corporate push toward a circular economy is accelerating the development of mono-material solutions and increasing the use of post-consumer recycled content. As a result, packaging is becoming an active component in a connected industrial ecosystem.

- For instance, a specialty chemical firm can replace rigid drums with intelligent flexible intermediate bulk containers (FIBCs) equipped with flexible printed sensors. These containers not only reduce freight costs and warehouse space but also provide real-time data on temperature and humidity, ensuring product integrity and mitigating risks throughout the global supply chain.

- This convergence of material science, digital technology, and sustainability is redefining the role and value of flexible packaging in modern industry, moving it from a simple cost center to a critical enabler of operational excellence and corporate responsibility.

What will be the Size of the Flexible Industrial Packaging Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Flexible Industrial Packaging Market Segmented?

The flexible industrial packaging industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Pouches

- Wraps

- Rollstock

- Bags

- Application

- Chemical industry

- Construction industry

- Food and beverages industry

- Pharmaceutical industry

- Others

- Material

- Plastic

- Paper

- Metal

- Bioplastic

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Type Insights

The pouches segment is estimated to witness significant growth during the forecast period.

The industrial pouches segment is evolving beyond simple containment, driven by a transition from rigid containers to flexible formats. This shift is motivated by logistical advantages, including significant source reduction and enhanced user convenience.

Innovations in multi-layer laminated structures are engineered for high-performance applications demanding superior barrier protection and chemical resistance.

A key trend is the development of recyclable mono-material structures, such as all-polyethylene (PE) constructions, which aim to replicate the performance of traditional laminates.

This focus on sustainability is reshaping product design, with redesigns of spouted stand-up pouches, for example, achieving a reduction in plastic consumption by over 60% per unit, demonstrating a tangible alignment of functionality with circular economy principles.

The Pouches segment was valued at USD 29.75 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 42% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Flexible Industrial Packaging Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the flexible industrial packaging market is diverse, reflecting varied levels of industrial maturity and regulatory focus.

APAC leads in volume and growth, contributing over 42% of the market's incremental expansion, driven by its manufacturing dominance and demand for foundational products like woven polypropylene bags.

In contrast, North America is a mature market focused on supply chain optimization, with high adoption of automated systems using advanced stretch films.

Europe distinguishes itself with the most stringent regulatory framework, mandating the use of post-consumer recycled content and driving innovation in mono-material solutions.

While the adoption of recyclable materials is a global trend, the lack of comprehensive waste management infrastructure in many developing regions remains a significant barrier to achieving a true circular economy for industrial plastics.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decisions in the flexible industrial packaging market are increasingly complex, balancing cost, performance, and sustainability. Companies are navigating regulations for sustainable industrial packaging while contending with the impact of raw material volatility on packaging costs.

- The debate over spouted stand-up pouches vs rigid containers is a prime example, where lightweighting flexible packaging for cost reduction offers freight savings that can be twice as effective as those from route optimization alone.

- Advancements in coextrusion for industrial films are enabling the creation of high-barrier films for food ingredients and the downgauging of stretch film for pallet unitization, enhancing performance while reducing material use. The flexible industrial packaging for chemical industry, for instance, is seeing a shift toward mono-material polyethylene heavy duty sacks.

- Similarly, flexible packaging solutions for pharmaceutical APIs now involve sophisticated, sterile single-use systems. The adoption of intelligent packaging with sensor technology and the development of recyclable rollstock for FFS machines highlight the industry's technological pivot.

- Ultimately, the successful application of circular economy models in industrial packaging hinges on innovations ranging from flexible intermediate bulk container liner technology to the widespread use of post-consumer recycled content in industrial films, even as bioplastic applications in flexible industrial packaging present new opportunities and challenges for FIBCs for bulk commodity transport.

- The move to sustainable mono-material flexible packaging is therefore not just a trend but a fundamental reshaping of the industry.

What are the key market drivers leading to the rise in the adoption of Flexible Industrial Packaging Industry?

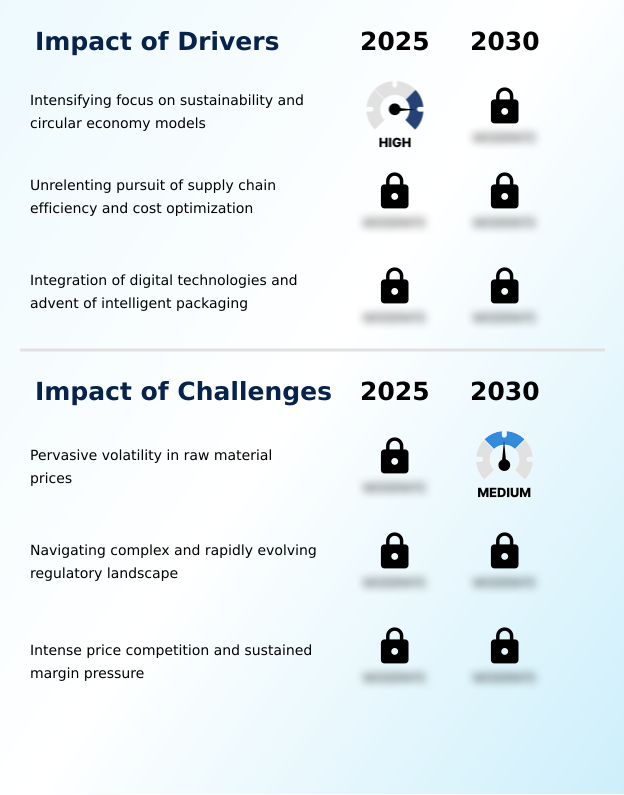

- A key driver for the market is the intensifying global focus on sustainability and the adoption of circular economy models.

- Market growth is propelled by three core drivers: sustainability, cost optimization, and digitalization. An intense focus on circular economy models has made sustainable packaging a primary driver, with regulatory pressures mandating changes in material use.

- The pursuit of supply chain efficiency is another powerful force; flexible formats offer significant lightweighting benefits, which directly lowers transportation costs and carbon footprints. For example, new regulations limiting empty parcel space to 40% favor form-fitting flexible options.

- Furthermore, the integration of digital technologies is transforming packaging into intelligent assets.

- The use of radio-frequency identification tags and flexible printed sensors provides unprecedented real-time tracking and condition monitoring, turning a cost center into a strategic tool for risk mitigation and quality assurance.

What are the market trends shaping the Flexible Industrial Packaging Industry?

- A primary market trend is the accelerated industry-wide shift from complex multi-material laminates. This pivot is toward innovative mono-material structures designed explicitly for recyclability.

- Key trends are reshaping the market, driven by a focus on sustainability and efficiency. There is an accelerated shift toward mono-material structures, particularly all-polyethylene constructions, to meet recyclability mandates. These new materials are being engineered to run on existing form-fill-seal machinery at up to 95% of the speed of traditional multi-material laminates, minimizing operational disruption.

- Concurrently, the rise of B2B ecommerce logistics is creating demand for durable, lightweight options like heavy-duty poly mailers and spouted stand-up pouches, which can reduce plastic use by over 60% compared to rigid alternatives.

- The development of functionally enhanced films, such as multi-layer nano-layer films for pallet unitization, further exemplifies the move toward high-performance, value-added solutions that optimize the supply chain.

What challenges does the Flexible Industrial Packaging Industry face during its growth?

- Pervasive volatility in the prices of petrochemical-derived raw materials presents a key challenge to industry growth and stability.

- The market grapples with significant structural challenges that impact stability and profitability. The pervasive volatility in raw material prices, with petrochemical-derived polymer resins subject to monthly adjustments, creates severe margin pressure for converters operating on longer-term contracts. This financial instability is compounded by the need to navigate a complex and fragmented regulatory landscape.

- Divergent rules on recyclability and post-consumer recycled content across regions create compliance hurdles and investment uncertainty. Furthermore, intense price competition, especially in commoditized segments, erodes margins and constrains the ability to reinvest in R&D for the very sustainable and high-performance materials the market demands, creating a difficult cycle to break.

Exclusive Technavio Analysis on Customer Landscape

The flexible industrial packaging market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the flexible industrial packaging market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Flexible Industrial Packaging Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, flexible industrial packaging market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aluflexpack AG - Offerings center on advanced flexible packaging, including specialized metal-free laminates and innovative blister systems designed for high-performance industrial applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aluflexpack AG

- Amcor Plc

- Anglo American plc

- Berry Global Inc.

- Bulk Lift International LLC

- Clifton Packaging Group Ltd.

- Eskay Flexible Packaging

- Filling and Packaging Material

- Global Pak Inc.

- Greif Inc.

- Industrial Packaging supply

- International Paper Co.

- Kiliper Corp.

- LC Packaging International BV

- Safepack

- Sealed Air Corp.

- SIG Group AG

- Sonoco Products Co.

- Surepak Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Flexible industrial packaging market

- In May, 2025, Sartorius Stedim Biotech, in partnership with Chronicled, launched its BioCertify single-use bag system, which incorporates a tamper-evident NFC chip linked to a blockchain ledger for enhanced security and traceability in transporting bulk Active Pharmaceutical Ingredients (APIs).

- In March, 2025, BASF announced the commercialization of its ChemCycle FIBC liner, a single-component, high-density polyethylene co-polymer engineered to provide significant chemical resistance while being fully integrable into existing HDPE recycling streams.

- In March, 2025, Mauser Packaging Solutions, in collaboration with PureCycle Technologies, announced a new line of Flexible Intermediate Bulk Containers (FIBCs) featuring an internal liner made with a minimum of 40% ultra-pure recycled polypropylene to meet new West Coast regulations.

- In February, 2025, Heidelberg Materials, in partnership with Dow, launched its ReCon Zero sack for dry-mix mortar products, featuring a composite design where the inner polymer lining delaminates during the paper recycling process, allowing for full recovery of paper fibers.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Flexible Industrial Packaging Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 335 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 9.1% |

| Market growth 2026-2030 | USD 45587.0 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 7.5% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The flexible industrial packaging market is defined by a pivotal shift from passive containment to active supply chain assets. Core products like heavy duty sacks, flexible intermediate bulk containers (FIBCs), and industrial liners are being reimagined through material science.

- The move toward mono-material solutions, such as all-polyethylene or all-polypropylene constructions, is a direct response to global circular economy models and extended producer responsibility mandates. This trend is enabled by advancements in coextrusion technology, which produces specialty films with enhanced barrier protection and puncture resistance using less material.

- The boardroom-level decision to invest in this technology is now directly linked to mitigating future regulatory risk and meeting corporate sustainability goals. For example, adopting multi-layer nano-layer films has enabled logistics operations to decrease plastic use by up to 40% per pallet.

- This evolution extends to intelligent packaging, with the integration of flexible printed sensors, near-field communication chips, and radio-frequency identification tags creating data-rich, traceable systems. The development of volatile corrosion inhibitors and static-dissipative properties in films further demonstrates the market's focus on high-value, functional solutions over purely commoditized woven polypropylene or basic rollstock.

What are the Key Data Covered in this Flexible Industrial Packaging Market Research and Growth Report?

-

What is the expected growth of the Flexible Industrial Packaging Market between 2026 and 2030?

-

USD 45.59 billion, at a CAGR of 9.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Pouches, Wraps, Rollstock, and Bags), Application (Chemical industry, Construction industry, Food and beverages industry, Pharmaceutical industry, and Others), Material (Plastic, Paper, Metal, and Bioplastic) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Intensifying focus on sustainability and circular economy models, Pervasive volatility in raw material prices

-

-

Who are the major players in the Flexible Industrial Packaging Market?

-

Aluflexpack AG, Amcor Plc, Anglo American plc, Berry Global Inc., Bulk Lift International LLC, Clifton Packaging Group Ltd., Eskay Flexible Packaging, Filling and Packaging Material, Global Pak Inc., Greif Inc., Industrial Packaging supply, International Paper Co., Kiliper Corp., LC Packaging International BV, Safepack, Sealed Air Corp., SIG Group AG, Sonoco Products Co. and Surepak Ltd.

-

Market Research Insights

- The market's dynamics are increasingly shaped by the pursuit of value-added functionalities that enhance supply chain optimization. The adaptation of packaging for B2B ecommerce is a significant factor, with new regulations limiting empty parcel space to 40%, thereby favoring form-fitting flexible options.

- This shift is driving demand for functionally enhanced films and innovative formats like spouted stand-up pouches, which can reduce plastic usage by more than 60% compared to traditional rigid containers. The commercialization of high-barrier adhesive technology is crucial, enabling the creation of high-performance, recyclable packaging.

- These advancements demonstrate a clear pivot toward intelligent, efficient, and sustainable solutions that deliver measurable business outcomes beyond basic product protection.

We can help! Our analysts can customize this flexible industrial packaging market research report to meet your requirements.

RIA -

RIA -