Flight Simulator Market Size 2025-2029

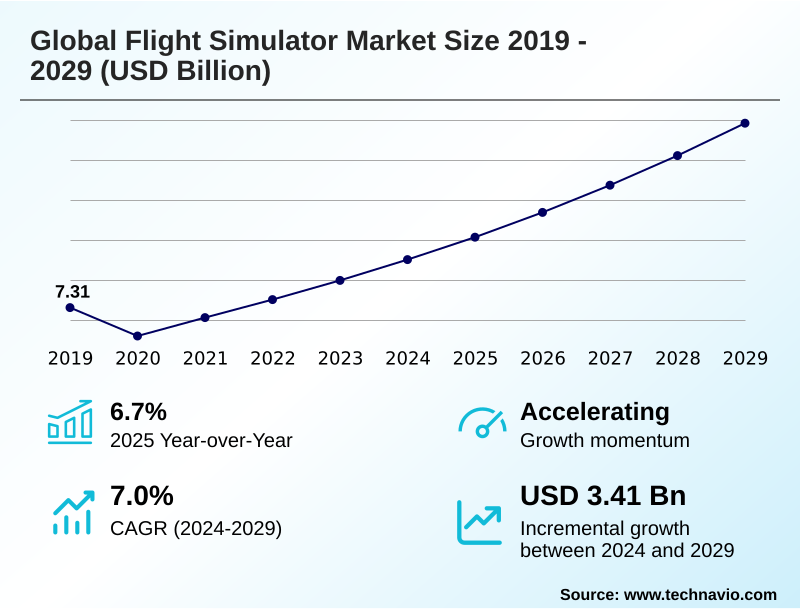

The flight simulator market size is valued to increase by USD 3.41 billion, at a CAGR of 7% from 2024 to 2029. Rising demand for cost-effective virtual training in aviation industry will drive the flight simulator market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 35.1% growth during the forecast period.

- By Application - Pilot training segment was valued at USD 5.15 billion in 2023

- By Platform - Rotary wing simulator segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 4.61 billion

- Market Future Opportunities: USD 3.41 billion

- CAGR from 2024 to 2029 : 7%

Market Summary

- The flight simulator market is fundamentally reshaping pilot education and certification by providing advanced, risk-free training environments. Growth is driven by the imperative to reduce operational costs and enhance safety, moving away from expensive and high-risk live aircraft training.

- Innovations such as high-fidelity motion platforms and adaptive learning modules are becoming standard, offering unprecedented realism in flight dynamics and cockpit controls. For instance, a major airline can leverage a synthetic training environment to optimize its pilot pipeline, using performance monitoring systems to identify skill gaps and tailor recurrent training requirements, thereby increasing pilot proficiency and ensuring operational readiness.

- However, the high capital expenditure for full-flight simulators and the need for continuous technological upgrades pose significant adoption barriers. The industry is also navigating the integration of virtual reality systems and real-time data analytics to further enhance situational awareness and decision-making exercises, ensuring alignment with stringent regulatory standards.

What will be the Size of the Flight Simulator Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Flight Simulator Market Segmented?

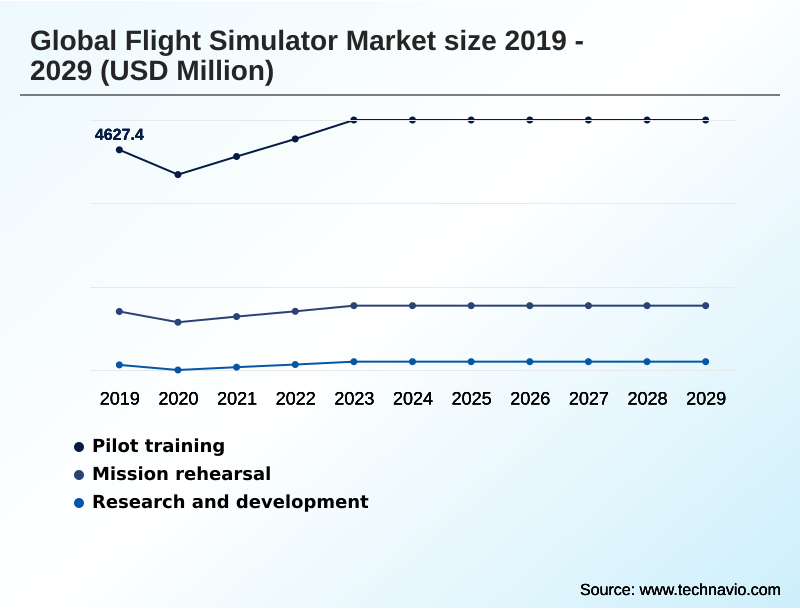

The flight simulator industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Pilot training

- Mission rehearsal

- Research and development

- Platform

- Rotary wing simulator

- Fixed wing simulator

- UAV simulator

- Product type

- Military flight simulator

- Commercial flight simulator

- Solution

- Hardware

- Software

- Services

- Geography

- North America

- US

- Canada

- APAC

- China

- India

- Japan

- Europe

- UK

- Germany

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- Rest of World (ROW)

- North America

By Application Insights

The pilot training segment is estimated to witness significant growth during the forecast period.

The pilot training segment is evolving to meet complex recurrent training requirements through the integration of advanced flight simulation training devices. These systems deliver structured, real-time feedback, enhancing pilot situational awareness and decision-making exercises, particularly for emergency procedure practice.

Modern full-flight simulators utilize multi-axis motion systems and high-resolution displays to provide realistic tactile feedback.

This focus on harmonized instructional methodologies, which include sophisticated cockpit controls and haptic feedback, is crucial for proficiency and has contributed to an industry-wide year-over-year expansion of 6.7%.

The emphasis remains on creating immersive environments that ensure pilots are prepared for a wide array of operational challenges, reinforcing safety and competency standards across the aviation industry.

The Pilot training segment was valued at USD 5.15 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 35.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Flight Simulator Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the market is characterized by mature demand in developed regions and rapid expansion in emerging economies.

While North America currently accounts for over 32% of the market, the APAC region is the primary growth engine, contributing more than 35% of incremental demand.

This expansion is fueled by investments in pilot training infrastructure and the need to fulfill mission-specific requirements with advanced synthetic training environments.

In these high-growth areas, there is a strong focus on adopting standardized training protocols and proprietary aircraft systems replication.

Simulators increasingly utilize sophisticated scenario libraries, real-time video generation with infrared and visual modes, and advanced projection systems to create a realistic tactical environment with detailed real geological features, supporting the development of a highly skilled aviation workforce.

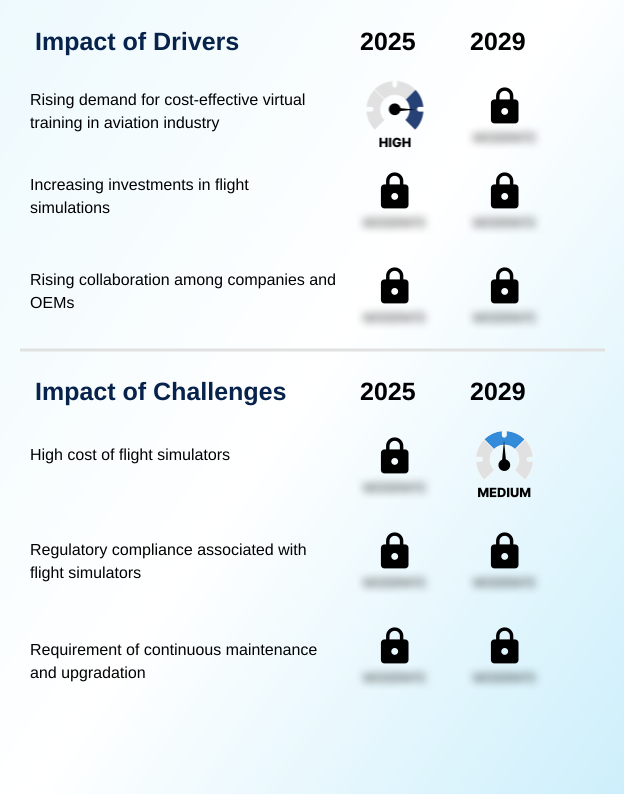

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic adoption of flight simulators is driven by the need for cost-effective virtual training in aviation, which addresses the high expense and risk of live-flight hours. A key industry focus is ensuring regulatory compliance for flight simulators, a complex process that influences both design and operational protocols.

- The continuous need for maintenance and upgradation of simulators remains a significant operational consideration for training centers. However, ongoing technological advancements in flight simulators are introducing new capabilities.

- For instance, the fixed wing simulator for commercial airlines is evolving with enhanced data analytics for pilot performance, while the rotary wing simulator for helicopter training incorporates superior haptic feedback in modern flight simulators. The uav simulator for unmanned aerial systems is a rapidly growing segment, distinct from the traditional full flight simulator vs fstd debate.

- Simulators excel at simulating emergency procedures in aviation, a core component of both commercial flight simulator pilot certification and military flight simulator mission rehearsal. The benefits of virtual boot camps and digital battlefield integration via simulation are particularly valued in the defense sector.

- On a technical level, flight simulator hardware component integration, alongside sophisticated flight simulator software scenario modeling, is critical for realism. The market is also supported by comprehensive flight simulator services and technical support.

- Moreover, the impact of cots components in simulators is notable, with their adoption reducing development costs by up to 20% compared to fully custom systems, demonstrating a clear advantage in operational budgeting. The trend towards vr and ar integration in simulators is further enhancing training immersion and effectiveness.

What are the key market drivers leading to the rise in the adoption of Flight Simulator Industry?

- The rising demand for cost-effective virtual training solutions within the aviation industry is a primary driver fueling market growth.

- The market is primarily driven by the pursuit of cost-effective virtual training and enhanced operational readiness. Organizations are increasingly investing in high-fidelity motion platforms and advanced visual systems that replicate real-world flight conditions with remarkable accuracy.

- Advanced simulation engines process complex flight dynamics, with responsive control interfaces providing realistic interactions. The use of commercial-off-the-shelf components has made these systems more accessible, reducing capital expenditure.

- The market's compound annual expansion, which exceeds 7%, is largely fueled by regions like APAC, where growth is nearly two percentage points higher than in South America.

- Joint research initiatives are focused on improving training effectiveness through dynamic operational scenarios and predictive maintenance capabilities, ensuring simulators remain reliable training assets.

What are the market trends shaping the Flight Simulator Industry?

- The increasing adoption of 3D simulation provisions for Unmanned Aerial Vehicle (UAV) training represents a significant upcoming trend, enhancing operator proficiency through realistic virtual environments.

- Key market trends are centered on enhancing training immersion and data intelligence. The integration of virtual reality systems and augmented reality systems is creating new paradigms for immersive visualization, particularly for uav training, where a 3d simulation model can replicate complex in-flight operations and problem-resolution protocols. These platforms leverage cloud-based analytics and real-time data analytics for granular performance assessment.

- Through knowledge sharing, developers are creating adaptive learning modules that customize immersive scenario modeling based on trainee performance. This focus on advanced simulation is driving significant investment, with the APAC region's growth rate outpacing Europe's by nearly a full percentage point. Innovations in generating payload output through these systems are further enhancing their utility across diverse applications.

What challenges does the Flight Simulator Industry face during its growth?

- The significant initial investment and ongoing maintenance expenses associated with flight simulators present a key challenge to market expansion.

- Significant challenges in the market stem from high capital costs and stringent operational requirements. The complexity of systems, which include a hydraulic lift system, an electronic motion base, and sophisticated control loading systems, requires substantial initial investment. Ensuring operational reliability involves continuous synchronized maintenance and adherence to rigorous safety standards.

- For initial certification, simulators must meet strict regulatory and operational objectives, a process overseen from an instructor operating station. While mature markets like Europe exhibit steady expansion, growth in regions like South America is nearly 20% slower, partly due to these financial barriers.

- Achieving pilot proficiency requires precise replication, from sound simulation systems to collimated displays, adding to the overall cost and complexity of maintaining these critical training tools.

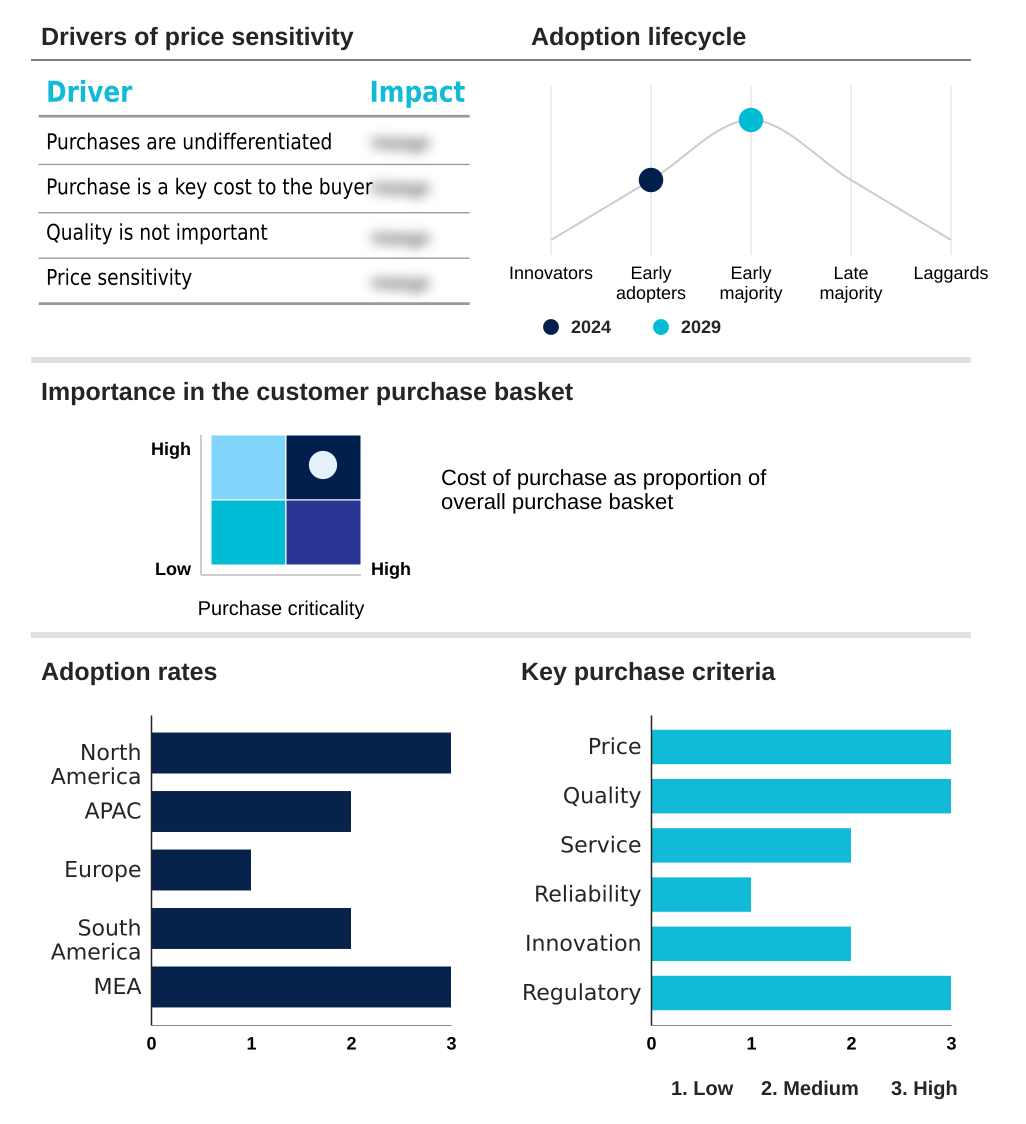

Exclusive Technavio Analysis on Customer Landscape

The flight simulator market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the flight simulator market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Flight Simulator Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, flight simulator market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aero Simulation Inc. - Offerings include the design and manufacturing of advanced flight simulators, with a focus on high-fidelity replicas of prevalent commercial aircraft for comprehensive pilot training.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aero Simulation Inc.

- Airbus SE

- Avenger Flight Group LLC

- CAE Inc.

- FenixSim Ltd.

- Flight Sim Labs Ltd.

- Flight Simulation Technique Centre Pvt. Ltd.

- FlightSafety International Inc.

- Gen24 Flybiz Pvt. Ltd.

- Indra Sistemas SA

- L3Harris Technologies Inc.

- Lockheed Martin Corp.

- RTX Corp.

- Textron Inc.

- Thales Group

- The Boeing Co.

- The Flight Experience

- VIER IM POTT

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Flight simulator market

- In October, 2024, Wizz Air inaugurated its new pilot training center in Rome, featuring advanced CAE Airbus A320 full-flight simulators designed to support recurrent training for more than 4,800 pilots annually.

- In November, 2024, Qantas and CAE opened a new flight training centre near Sydney Airport, housing five full-flight simulators, including Australia's first Airbus A350 simulator intended for ultra-long-haul Project Sunrise pilot training.

- In January, 2025, Airbus selected L3Harris Technologies to supply an A320-family full flight simulator for its Toulouse Training Centre, enhancing its training capacity for the popular aircraft series.

- In January, 2025, flydubai and CAE are scheduled to open a new flight training center in Dubai, which will feature six Boeing 737 MAX full-flight simulators to support both initial and recurrent pilot training.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Flight Simulator Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 282 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7% |

| Market growth 2025-2029 | USD 3414.9 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 6.7% |

| Key countries | US, Canada, China, India, Japan, South Korea, UK, Germany, France, Italy, Brazil, Argentina, Saudi Arabia and UAE |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The flight simulator market is defined by a sophisticated interplay of advanced hardware and software designed to achieve unparalleled realism in pilot training. The core technology includes high-fidelity motion platforms, such as the electronic motion base and hydraulic lift system, which work in tandem with control loading systems to replicate flight dynamics.

- Advanced visual systems, including collimated displays and high-resolution projection systems, create immersive environments, complemented by detailed sound simulation systems. Key components like the instructor operating station, joystick and rudder pedals, and cockpit controls are engineered for precise tactile feedback and haptic feedback. Modern systems leverage powerful simulation engines, adaptive learning modules, and extensive scenario libraries.

- The integration of virtual reality systems and augmented reality systems is a key trend, pushing the boundaries of immersive visualization. Data-driven approaches are enabled through real-time data analytics, cloud-based analytics, and performance monitoring systems, supporting predictive maintenance capabilities. This technological convergence within full-flight simulators and flight simulation training devices creates synthetic training environments that are crucial for modern aviation.

- Notably, the adoption of commercial-off-the-shelf components has streamlined production, reducing system integration costs by over 15% and influencing procurement strategies at a boardroom level.

What are the Key Data Covered in this Flight Simulator Market Research and Growth Report?

-

What is the expected growth of the Flight Simulator Market between 2025 and 2029?

-

USD 3.41 billion, at a CAGR of 7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Pilot training, Mission rehearsal, Research and development), Platform (Rotary wing simulator, Fixed wing simulator, UAV simulator), Product Type (Military flight simulator, Commercial flight simulator), Solution (Hardware, Software, Services) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rising demand for cost-effective virtual training in aviation industry, High cost of flight simulators

-

-

Who are the major players in the Flight Simulator Market?

-

Aero Simulation Inc., Airbus SE, Avenger Flight Group LLC, CAE Inc., FenixSim Ltd., Flight Sim Labs Ltd., Flight Simulation Technique Centre Pvt. Ltd., FlightSafety International Inc., Gen24 Flybiz Pvt. Ltd., Indra Sistemas SA, L3Harris Technologies Inc., Lockheed Martin Corp., RTX Corp., Textron Inc., Thales Group, The Boeing Co., The Flight Experience and VIER IM POTT

-

Market Research Insights

- The market's momentum is driven by a focus on enhancing training effectiveness and operational readiness. The adoption of harmonized instructional methodologies improves pilot proficiency, with performance data showing a 15% increase in skill retention. Meanwhile, the use of immersive scenario modeling for decision-making exercises and emergency procedure practice reduces critical errors by up to 25% compared to traditional methods.

- Strategic joint research initiatives are accelerating the development of advanced systems that provide structured, real-time feedback. This push for technological superiority supports both initial certification and complex recurrent training requirements, ensuring alignment with rigorous safety standards and regulatory objectives. The emphasis on knowledge sharing helps standardize training protocols, leading to greater operational reliability and improved situational awareness across fleets.

We can help! Our analysts can customize this flight simulator market research report to meet your requirements.

RIA -

RIA -