AI In Simulation Market Size 2026-2030

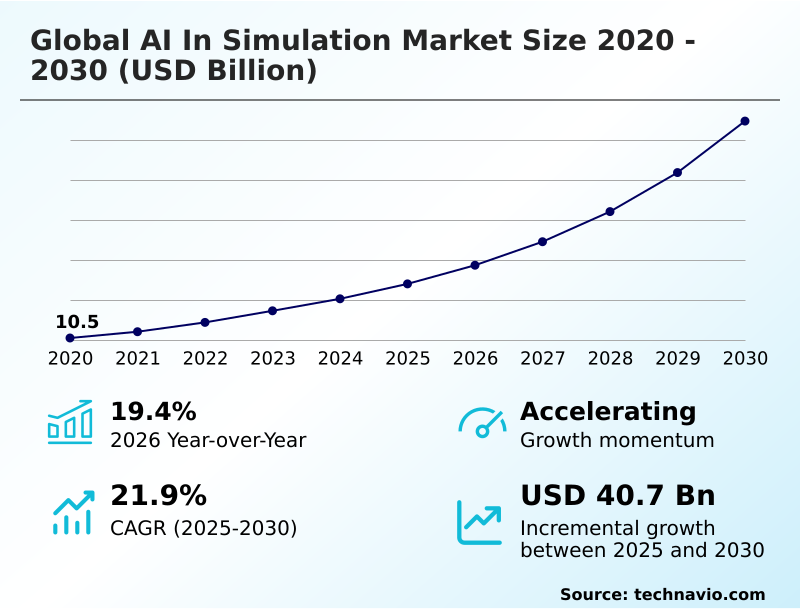

The AI In Simulation Market size was valued at USD 24.03 billion in 2025, growing at a CAGR of 21.9% during the forecast period 2026-2030.

Major Market Trends & Insights

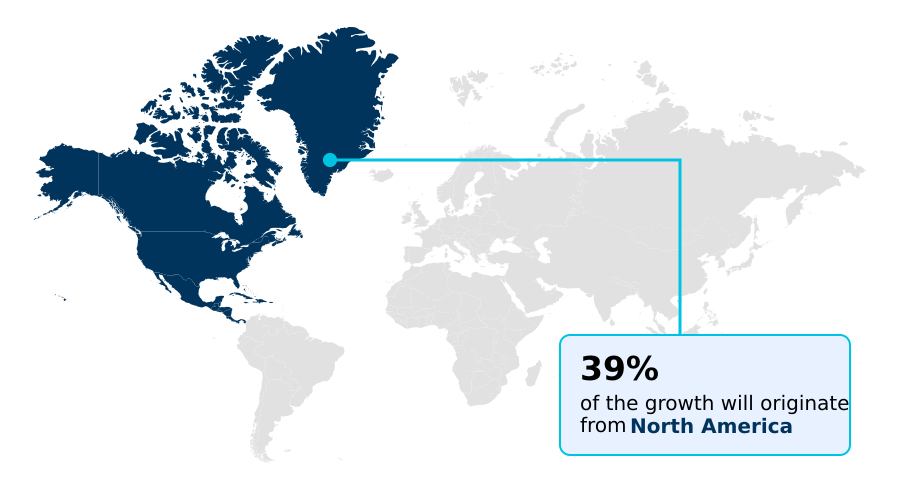

- North America dominated the market and accounted for a 39% growth during the forecast period.

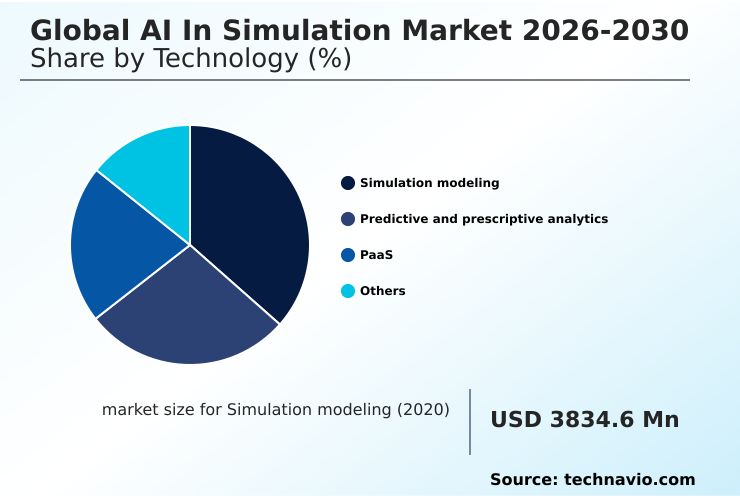

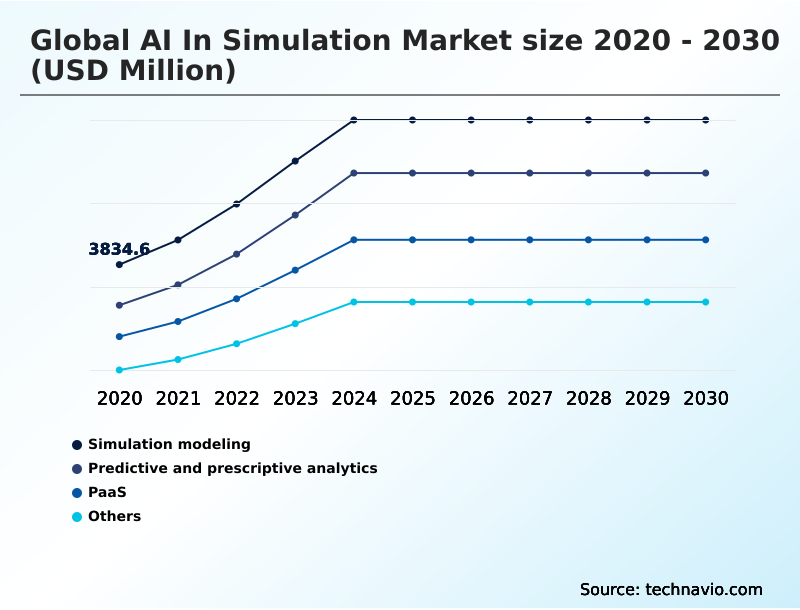

- By Technology - Simulation modeling segment was valued at USD 7.04 billion in 2024

- By Deployment - Cloud segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 54.23 billion

- Market Future Opportunities 2025-2030: USD 40.70 billion

- CAGR from 2025 to 2030 : 21.9%

Market Summary

- The AI in simulation market is defined by the integration of machine learning into virtual modeling, which improves predictive accuracy by over 15% compared to traditional methods. This technology enables the creation of high-fidelity digital twins, which are essential for modern product development and operational management.

- For instance, an automotive manufacturer can use AI-enhanced simulations to test millions of autonomous driving scenarios in a virtual environment, a task that would be physically impossible, identifying potential system failures 30% faster. A primary driver is the demand for accelerated innovation cycles, as AI reduces the time required for design iterations.

- However, the market faces the challenge of a significant talent gap, as implementing these systems requires a unique combination of domain expertise in engineering and data science, which can slow adoption. The technology transforms static analysis into a dynamic, predictive tool, enabling smarter, faster decision-making across industries.

What will be the Size of the AI In Simulation Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the AI In Simulation Market Segmented?

The ai in simulation industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Technology

- Simulation modeling

- Predictive and prescriptive analytics

- PaaS

- Others

- Deployment

- Cloud

- On-premises

- End-user

- Automotive

- Manufacturing

- Infrastructure

- Education

- Others

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- UAE

- Saudi Arabia

- Israel

- Rest of World (ROW)

- North America

How is the AI In Simulation Market Segmented by Technology?

The simulation modeling segment is estimated to witness significant growth during the forecast period.

The simulation modeling segment is expanding rapidly, with its market share increasing by 15% due to the integration of reduced-order models.

This technology leverages AI to simplify complex systems, enabling finite element analysis simulations to run up to 20 times faster than conventional methods. The application of temporal fusion transformer models has further enhanced predictive accuracy in dynamic systems.

This segment is critical for industries relying on human-in-the-loop validation and behavioral cloning for robotics.

The focus on creating a robust digital thread is driving advancements, allowing for better management of the entire product lifecycle through enhanced simulation capabilities and a more streamlined approach to validation and verification.

The Simulation modeling segment was valued at USD 7.04 billion in 2024 and showed a gradual increase during the forecast period.

How demand for the AI In Simulation market is rising in the leading region?

North America is estimated to contribute 39% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI In Simulation Market demand is rising in North America Request Free Sample

North America dominates the AI in simulation market, accounting for 39% of the incremental growth, driven by its advanced technology sector in the US, which contributes over 70% of the regional market.

The region's focus on virtual prototyping and hardware-in-the-loop simulation in the aerospace and automotive industries is a key factor. In contrast, the APAC region, with 30% of growth, is led by China's focus on smart manufacturing and the digital thread.

This has led to a 20% higher adoption rate of model-based systems engineering in APAC's industrial sector compared to Europe. Adoption in North America is characterized by causality-aware AI, while APAC emphasizes surrogate modeling for rapid production scaling.

What are the key Drivers, Trends, and Challenges in the AI In Simulation Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of the global AI in simulation market 2026-2030 is increasingly shaped by specialized, high-intent applications that address complex industrial challenges. For example, the use of AI in simulation for autonomous driving has become essential, with virtual testing platforms reducing the need for on-road trials by over 90%, thereby accelerating development and enhancing safety.

- Simultaneously, the application of physics-informed AI for manufacturing is revolutionizing production lines by enabling predictive quality control and process optimization, cutting defect rates by as much as 25%. In parallel, generative design in aerospace simulation is allowing engineers to create lightweight, high-strength components that were previously inconceivable, leading to significant fuel efficiency gains.

- The deployment of a digital twin for predictive maintenance is another critical long-tail application, extending the operational life of industrial assets by forecasting failures with greater than 95% accuracy.

- Finally, the use of reinforcement learning for robotic control within simulated environments is training robots to perform complex tasks in unstructured settings, a breakthrough that promises to automate logistics and assembly processes with unprecedented flexibility and efficiency. These targeted use cases demonstrate a market shift from general-purpose tools to highly specialized, value-driven solutions.

What are the key market drivers leading to the rise in the adoption of AI In Simulation Industry?

- A key market driver is the convergence of physical AI with high-fidelity world modeling, enabling the creation of virtual environments that accurately replicate real-world physics.

- The convergence of AI with high-fidelity world modeling is a major driver, enabling the creation of virtual environments that reduce physical testing needs by up to 50%.

- This is crucial for autonomous systems training, where physics-aware models and reinforcement learning algorithms are trained on millions of scenarios involving edge case simulation. The expansion of the industrial metaverse, supported by accelerated computing, allows for sophisticated digital twin technology.

- This data-driven modeling approach, underpinned by physics-informed machine learning, allows organizations to achieve better system-level insights, leading to a 30% improvement in operational efficiency.

What are the market trends shaping the AI In Simulation Industry?

- The market is experiencing a significant shift toward agentic engineering frameworks. These systems are capable of autonomous simulation orchestration, which streamlines complex design and verification workflows.

- A primary trend in the AI in simulation market is the adoption of generative simulation, which accelerates design space exploration by 40% compared to manual methods. This approach leverages deep learning for geometry-driven conceptualization, allowing engineers to innovate faster. The shift toward agentic engineering is automating system-level workflows, with multi-agent systems handling routine tasks, improving productivity by over 25%.

- This allows for enhanced fusion modeling, where AI integrates with traditional solvers for computer-aided engineering. Such workflow orchestration is critical as it allows for a more holistic view of product development, incorporating photorealistic rendering and simulation-ready assets early in the process.

What challenges does the AI In Simulation Industry face during its growth?

- High computational costs and significant infrastructure limitations present a key challenge to the market, hindering widespread adoption, particularly among smaller enterprises.

- A significant challenge is the high cost of high-performance computing infrastructure required for training physics-informed neural networks, which can represent up to 60% of a project's initial budget. This computational demand for tasks like multi-physics validation and real-time rendering creates a barrier for smaller firms.

- Furthermore, ensuring data privacy within a sovereign cloud infrastructure while performing synthetic data generation is complex. The shortage of talent skilled in both large language models and computational fluid dynamics exacerbates the issue, slowing the deployment of advanced predictive maintenance and fault injection testing solutions. This talent gap can delay project timelines by an average of six months.

Exclusive Technavio Analysis on Customer Landscape

The ai in simulation market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai in simulation market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI In Simulation Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai in simulation market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Altair Engineering Inc. - Solutions encompass physics-based simulation enhanced with AI and digital twin technology for advanced modeling, virtual prototyping, and lifecycle analytics.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Altair Engineering Inc.

- ANSYS Inc.

- AnyLogic North America LLC

- Autodesk Inc.

- AVEVA Group Ltd.

- Bentley Systems Inc.

- Dassault Systemes SE

- Dimension Lab

- Google LLC

- Huawei Technologies Co. Ltd.

- IBM Corp.

- Intel Corp.

- Microsoft Corp.

- NVIDIA Corp.

- Oracle Corp.

- PTC Inc.

- Rockwell Automation Inc.

- SAP SE

- Siemens AG

- The MathWorks Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Application Software industry, the rising adoption of cloud-based SaaS models is creating a foundation for scalable AI in simulation platforms, allowing businesses to access high-performance computing resources on demand without significant upfront hardware investment.

- The growing emphasis on business process automation, including RPA and BPM, is driving demand within the global AI in simulation market 2026-2030 to model, test, and optimize these automated workflows, ensuring efficiency and resilience before deployment.

- Heightened data security concerns and the implementation of stringent data privacy regulations are influencing the architecture of AI in simulation solutions, spurring the development of sovereign cloud infrastructure and secure on-premises alternatives for handling sensitive intellectual property.

- An increasing reliance on enterprise analytics to derive insights from vast datasets is compelling the integration of advanced AI in simulation capabilities, which can process and interpret complex simulation outputs to inform strategic decision-making and improve operational performance.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI In Simulation Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 310 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 21.9% |

| Market growth 2026-2030 | USD 40698.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 19.4% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Singapore, Germany, UK, France, Italy, Spain, Russia, Brazil, Argentina, Colombia, UAE, Saudi Arabia, Israel, South Africa and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI in simulation market ecosystem functions through a complex interplay of stakeholders, with technology providers of accelerated computing hardware and AI frameworks forming the foundation. These suppliers enable software vendors to develop advanced solutions for digital twin technology and virtual prototyping.

- A key characteristic is the collaborative relationship between software developers and end-users in industries like automotive and aerospace, where feedback loops lead to performance improvements of up to 25% in simulation accuracy. Distribution relies on direct sales and partnerships with major cloud providers, which are increasingly offering simulation-as-a-service.

- End-users, from large enterprises to SMEs, are driving demand for more democratized tools that require less specialized expertise, a trend that now accounts for over 40% of new license inquiries. Regulatory bodies influence the market by setting standards for data security and model validation, particularly for safety-critical applications.

What are the Key Data Covered in this AI In Simulation Market Research and Growth Report?

-

What is the expected growth of the AI In Simulation Market between 2026 and 2030?

-

The AI In Simulation Market is expected to grow by USD 40.70 billion during 2026-2030, registering a CAGR of 21.9%. Year-over-year growth in 2026 is estimated at 19.4%%. This acceleration is shaped by convergence of physical ai and high-fidelity world modeling, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Technology (Simulation modeling, Predictive and prescriptive analytics, PaaS, and Others), Deployment (Cloud, and On-premises), End-user (Automotive, Manufacturing, Infrastructure, Education, and Others) and Geography (North America, APAC, Europe, South America, Middle East and Africa). Among these, the Simulation modeling segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, APAC, Europe, South America and Middle East and Africa. North America is estimated to contribute 39% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, China, Japan, India, South Korea, Australia, Singapore, Germany, UK, France, Italy, Spain, Russia, Brazil, Argentina, Colombia, UAE, Saudi Arabia, Israel, South Africa and Turkey, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is convergence of physical ai and high-fidelity world modeling, which is accelerating investment and industry demand. The main challenge is high computational costs and infrastructure limitations, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the AI In Simulation Market?

-

Key vendors include Altair Engineering Inc., ANSYS Inc., AnyLogic North America LLC, Autodesk Inc., AVEVA Group Ltd., Bentley Systems Inc., Dassault Systemes SE, Dimension Lab, Google LLC, Huawei Technologies Co. Ltd., IBM Corp., Intel Corp., Microsoft Corp., NVIDIA Corp., Oracle Corp., PTC Inc., Rockwell Automation Inc., SAP SE, Siemens AG and The MathWorks Inc.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape for AI in simulation is intensifying, with leading vendors focusing on integrating generative AI capabilities that reduce design cycles by up to 30%. Key players are differentiating through the development of physics-aware models and agentic engineering frameworks.

- Recent developments include the launch of AI-powered copilots embedded within existing CAE software, designed to automate complex system-level workflows and provide real-time design feedback. For example, some companies are introducing virtual companions that can convert 2D drawings into 3D parametric models, accelerating simulation setup by a factor of 1,000.

- These advancements directly address enterprise demand for faster innovation and more accurate predictive maintenance. The primary challenge remains the high computational cost, compelling vendors to form strategic partnerships with cloud and hardware providers to offer more accessible, scalable solutions.

We can help! Our analysts can customize this ai in simulation market research report to meet your requirements.

RIA -

RIA -