Food Hydrocolloids Market Size 2024-2028

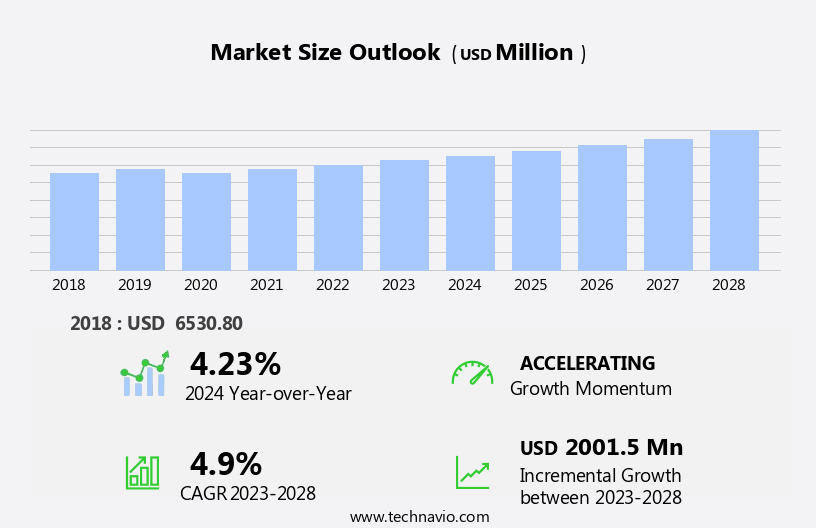

The food hydrocolloids market size is forecast to increase by USD 2 billion, at a CAGR of 4.9% between 2023 and 2028.

- The market is experiencing significant growth due to the increasing demand for convenience food products. Consumers' busy lifestyles have led to a surge in the popularity of ready-to-eat and ready-to-cook meals, which often incorporate hydrocolloids for texture and stability. Another key trend driving market expansion is the rising utilization of hydrocolloids in gluten-free food products. As the prevalence of celiac disease and gluten intolerance continues to increase, manufacturers are turning to hydrocolloids as a natural alternative to wheat-based binders. However, ethical concerns surrounding animal-derived food hydrocolloids pose a significant challenge to market growth. As consumer awareness and expectations for sustainable and ethical food production continue to rise, there is growing pressure on manufacturers to source alternative, plant-based hydrocolloids.

- This shift towards plant-based alternatives presents both an opportunity and a challenge for market participants. Companies that can successfully innovate and offer high-quality, sustainable, and cost-effective plant-based hydrocolloids will be well-positioned to capitalize on this trend and meet the evolving needs of consumers.

What will be the Size of the Food Hydrocolloids Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by the dynamic interplay of various factors. These include advances in technology, changing consumer preferences, and regulatory requirements. Hydrocolloids, such as carrageenan, pectin types, locust bean gum, and protein hydrocolloids, play a crucial role in food and beverage production, providing water binding capacity, viscosity control, and texture modification. Quality control is paramount in the production of hydrocolloids, ensuring consistent molecular weight distribution, syneresis reduction, and interaction effects. Carrageenan, for instance, exhibits unique rheological behavior, making it an effective stabilizing agent in various applications. Hydrocolloid blends and mixtures, such as those containing gum arabic and xanthan gum, offer enhanced functionalities.

The cosmetics industry also benefits from hydrocolloids, with applications ranging from thickening agents to rheology modifiers. In pharmaceutical applications, hydrocolloids serve as gelling agents and provide freeze-thaw stability. Process optimization is a continuous focus, with ongoing research aimed at improving gel strength and sensory attributes. Cellulose derivatives and emulsifying agents further expand the functionality of hydrocolloids, while alginate properties enable their use in food applications as thickening agents. Starch modification and protein hydrocolloids offer additional possibilities for texture modification. The gelation mechanism of hydrocolloids continues to be a subject of ongoing research, with potential applications in various sectors.

How is this Food Hydrocolloids Industry segmented?

The food hydrocolloids industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

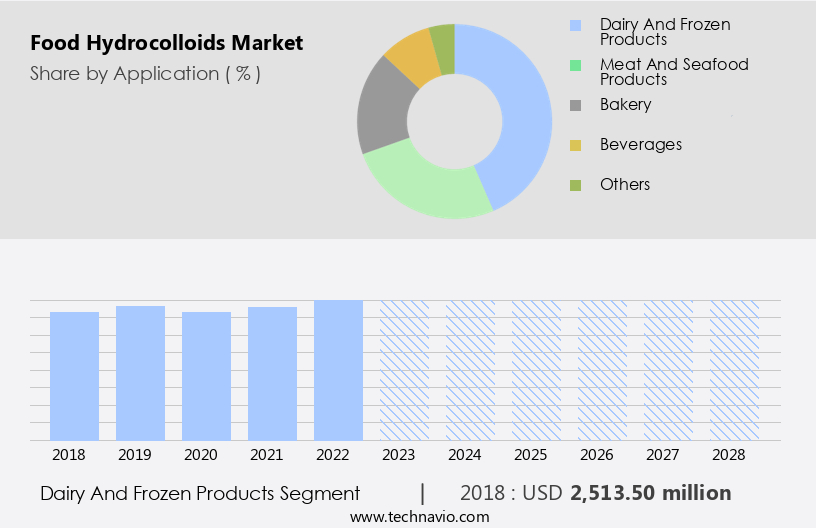

- Dairy and frozen products

- Meat and seafood products

- Bakery

- Beverages

- Others

- Source Type

- Plant-Based

- Animal-Based

- Microbial

- Distribution Channel

- B2B

- Supermarkets

- Online Retail

- Specialty Stores

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- Russia

- UK

- Middle East and Africa

- South Africa

- UAE

- APAC

- China

- India

- Japan

- South Korea

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Application Insights

The dairy and frozen products segment is estimated to witness significant growth during the forecast period.

In the dynamic the market, the selection of a suitable gelling agent for a specific dairy product is crucial. For instance, alginate's ability to form stable gels makes it a popular choice for puddings and desserts, cold prepared bakery creams, and other applications. However, its incompatibility with milk limits its use in dairy products. In response, end-users turn to alternative food hydrocolloids. Pectin, for example, is widely employed in milk desserts and gelled or thickened milk products, such as yogurts. Low methoxyl pectin (LMP) is particularly effective due to its ability to react with calcium and other ingredients to form a stable gel.

Hydrocolloid blends, like those of pectin and carrageenan, offer additional benefits. Carrageenan's high water binding capacity and viscosity control contribute to the production of desirable textures. The molecular weight distribution and syneresis reduction properties of hydrocolloids are also essential for maintaining freeze-thaw stability and ensuring process optimization. Interaction effects between hydrocolloids and other ingredients can influence rheological behavior, gel strength, and sensory attributes. Stabilizing agents, such as cellulose derivatives and emulsifying agents, play a vital role in maintaining the stability and texture of food products. In the pharmaceutical sector, hydrocolloids serve as rheology modifiers and gelling agents, enhancing the functionality of various formulations.

Xanthan gum, locust bean gum, and protein hydrocolloids are among the widely used types. Food texture analysis is an essential aspect of quality control, ensuring the desired consistency and mouthfeel in various applications. The evolving market trends include the development of hydrocolloid mixtures and the exploration of new applications in cosmetics and pharmaceuticals. The versatility of food hydrocolloids continues to drive innovation and growth in the industry.

The Dairy and frozen products segment was valued at USD 2.51 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

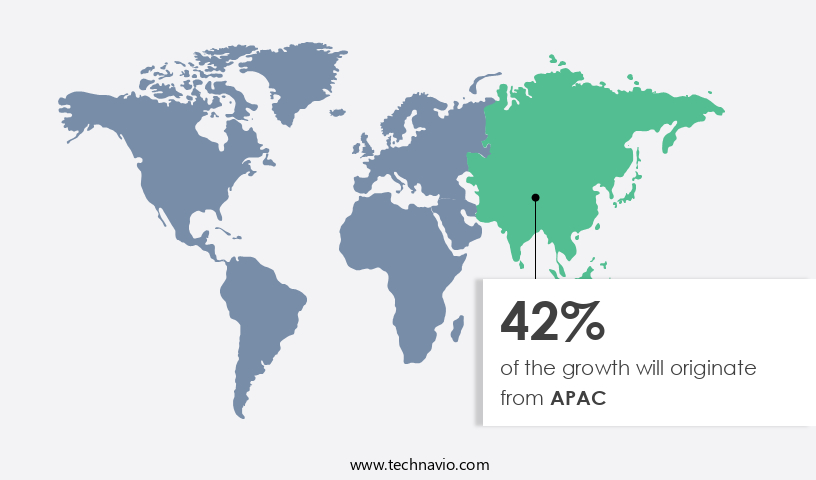

APAC is estimated to contribute 42% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market experiences significant growth, driven by developed regions such as North America. Countries like the US and Canada contribute substantially to this market due to their thriving food and beverage industries. The production of bakery products, in particular, is a major contributor, with the US bread industry reporting a 7.2% increase in exports in 2020. Hydrocolloids play a crucial role in various applications, including water binding, viscosity control, and texture modification. Carrageenan, a common hydrocolloid, offers desirable properties like syneresis reduction and interaction effects, making it a preferred choice for rheological behavior and stabilizing agents in food and pharmaceutical applications.

Other hydrocolloids, such as cellulose derivatives, emulsifying agents, pectin types, xanthan gum, locust bean gum, protein hydrocolloids, and starch modification agents, contribute to the market's diversity. Food texture analysis is essential for ensuring product quality, with alginate properties and thickening agents playing significant roles. Hydrocolloid blends and gelling agents are also essential components, enhancing gel strength and freeze-thaw stability. Process optimization is a critical factor in the market, with rheology modifiers ensuring desirable rheological behavior and sensory attributes. Cosmetics applications and pharmaceutical uses further expand the market's scope. Gum arabic and hydrocolloid mixtures are essential in cosmetics for their emulsifying properties, while gelling agents are crucial in pharmaceuticals for their ability to form stable gels.

Overall, the market continues to evolve, driven by the diverse applications and growing demand for improved food and beverage quality and consistency.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Food Hydrocolloids Industry?

- The increasing preference for convenient food solutions is the primary market motivator, driven by consumers' busy lifestyles and the desire for time-saving meal options.

- Packaged food and beverages, including ready-to-eat meals, instant mixes, and canned food, have gained significant popularity in developed markets due to increasing consumer awareness and preference for safer, longer-lasting options. These foods offer numerous advantages, such as extended shelf life, protection from contamination, and improved quality through barrier packaging. In the realm of food additives, hydrocolloids play a crucial role in enhancing the texture and sensory attributes of these packaged products. Two common types of hydrocolloids are locust bean gum and protein hydrocolloids. Locust bean gum, derived from the seeds of the carob tree, is widely used for texture modification in various food applications.

- It exhibits excellent water-holding capacity and thickening properties, making it suitable for use in beverages, baked goods, and dairy products. Protein hydrocolloids, derived from animal or plant sources, are employed for starch modification and gelation mechanism in food systems. They provide enhanced texture, stability, and mouthfeel to the final product. The sensory attributes of food products are significantly influenced by the use of these hydrocolloids, ensuring a harmonious balance of taste, texture, and appearance. Guar gum, another hydrocolloid, is also used for similar purposes but is not mentioned in the context. In conclusion, the use of hydrocolloids, such as locust bean gum and protein hydrocolloids, is essential in the production of packaged food and beverages, contributing to improved texture, extended shelf life, and enhanced sensory attributes.

What are the market trends shaping the Food Hydrocolloids Industry?

- The increasing usage of hydrocolloids in gluten-free products represents a significant market trend. Hydrocolloids, a common ingredient in food manufacturing, provide texture and stability to gluten-free products, making them a popular choice for consumers with dietary restrictions.

- The market encompasses a range of natural and synthetic substances used for various applications in the food industry. These include carrageenan, hydrocolloid blends, pectin, and gum arabic, among others. These additives offer benefits such as water binding capacity, viscosity control, and syneresis reduction. Carrageenan, a common hydrocolloid, is known for its gelling, thickening, and stabilizing properties. Quality control is crucial in the production of food hydrocolloids, ensuring consistent molecular weight distribution and rheological behavior. Interaction effects between different hydrocolloids and their impact on texture and stability are also essential considerations. Understanding these properties can help optimize formulations and enhance the overall sensory experience of food products.

- Hydrocolloids can be derived from various sources, including algae, plants, and microorganisms. Their use allows for the creation of innovative, immersive, and harmonious textures, striking a balance between taste, texture, and nutritional value. Recent research in this field continues to uncover new applications and potential benefits, further expanding the market's growth potential.

What challenges does the Food Hydrocolloids Industry face during its growth?

- The growth of the food industry is significantly impacted by ethical concerns surrounding the use of animal-derived hydrocolloids as food additives. These concerns represent a major challenge that must be addressed to ensure industry expansion and maintain consumer trust.

- Food hydrocolloids are essential additives used in various industries, including food, cosmetics, and pharmaceuticals, to enhance product properties. Traditional hydrocolloids are derived from animal sources, such as gelatin from cattle, swine, and fish, and chitosan from insects and crustaceans. These hydrocolloids serve multiple functions, including thickening, gelling, emulsifying, and stabilizing agents. Gelatin, a widely used animal-derived hydrocolloid, is essential in food applications, such as dressings, sauces, and confectionery. Chitosan, a fiber derived from the exoskeleton of insects and crustaceans, is gaining popularity due to its antimicrobial properties against foodborne bacteria, yeast, and filamentous fungi. Cellulose derivatives and emulsifying agents are other essential hydrocolloids used in various applications.

- Cellulose derivatives, such as carboxymethylcellulose and sodium carboxymethylcellulose, provide excellent freeze-thaw stability and gel strength, making them suitable for various food and pharmaceutical applications. Emulsifying agents, such as carrageenan and pectin, are used to stabilize oil-in-water emulsions, ensuring process optimization and product consistency. In cosmetics applications, hydrocolloids are used as thickeners, gelling agents, and stabilizers, enhancing the texture and appearance of various products. Pharmaceutical applications of hydrocolloids include their use as binders, disintegrants, and suspending agents, ensuring the effective delivery of active ingredients. In conclusion, food hydrocolloids are essential additives used across various industries for their unique functional properties.

- Animal-derived hydrocolloids, such as gelatin and chitosan, and plant-derived hydrocolloids, such as cellulose derivatives and emulsifying agents, offer multiple benefits, including thickening, gelling, emulsifying, and stabilizing properties, making them indispensable in food, cosmetics, and pharmaceutical applications.

Exclusive Customer Landscape

The food hydrocolloids market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the food hydrocolloids market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, food hydrocolloids market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Archer Daniels Midland Co. - The company specializes in providing a diverse selection of food hydrocolloids, including Xanthan Gum (PurelyForm Xanthan) and Hydrocolloid, enhancing food texture and stability in various applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Archer Daniels Midland Co.

- Ashland Inc.

- B and V srl

- Behn Meyer Deutschland Holding AG and Co. KG

- Cargill Inc.

- Compania Espanola de Algas Marinas S.A.

- CP Kelco US Inc.

- Darling Ingredients Inc.

- DuPont de Nemours Inc.

- Hebei Xinhe Biochemical Co. Ltd.

- Herbstreith and Fox GmbH and Co. KG

- Hispanagar S A

- Ingredion Inc.

- J.F. Hydrocolloids Inc.

- Kerry Group Plc

- Koninklijke DSM NV

- NEXIRA

- Silvateam Spa

- Tate and Lyle PLC

- W Hydorcolloids Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Food Hydrocolloids Market

- In January 2024, Danisco A/S, a leading producer of food ingredients, announced the launch of their new line of microbial hydrocolloids, Danisco PureGel, designed to enhance texture and stability in various food applications (Danisco A/S Press Release).

- In March 2024, DuPont Nutrition & Health entered into a strategic partnership with Ingredion Incorporated to expand their joint venture, NutriScience Innovation, focusing on the development of innovative food and beverage solutions using hydrocolloids and other functional ingredients (DuPont Nutrition & Health Press Release).

- In May 2024, Cargill, a global food ingredients supplier, completed the acquisition of the texturizing business of Ingredion Incorporated, significantly expanding their hydrocolloids product portfolio and capabilities (Cargill Press Release).

- In April 2025, the European Food Safety Authority (EFSA) approved the use of a new hydrocolloid, sodium alginate from Lithuanian producer, Geltex, as a thickener and stabilizer in various food applications, marking a significant regulatory milestone for the company (EFSA Journal).

Research Analyst Overview

- The market experiences continuous evolution, driven by advancements in chemical modification and application technology. Dispersion techniques play a crucial role in enhancing the functional properties of hydrocolloids, ensuring cost effectiveness and improved textural profile analysis. Shelf life is a significant concern, leading to extensive stability studies and regulatory compliance. Product formulation innovation relies on interaction studies, characterization techniques, and concentration effects to optimize gelation kinetics for quality improvement. Process parameters, including extraction methods and purification processes, are essential in selecting food grade materials for various application methods.

- Ingredient selection and viscosity measurement are critical in food matrices, ensuring emulsion stability and sensory evaluation. Regulatory compliance and cost effectiveness remain key market trends, while innovation in application technology continues to shape the future of the food hydrocolloids industry.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Food Hydrocolloids Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

167 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.9% |

|

Market growth 2024-2028 |

USD 2001.5 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.23 |

|

Key countries |

Brazil, South Africa, UAE, US, Canada, Germany, UK, China, France, Italy, Japan, India, South Korea, Argentina, and Russia |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Food Hydrocolloids Market Research and Growth Report?

- CAGR of the Food Hydrocolloids industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the food hydrocolloids market growth of industry companies

We can help! Our analysts can customize this food hydrocolloids market research report to meet your requirements.

RIA -

RIA -