Saudi Arabia Food Retail Market Size 2026-2030

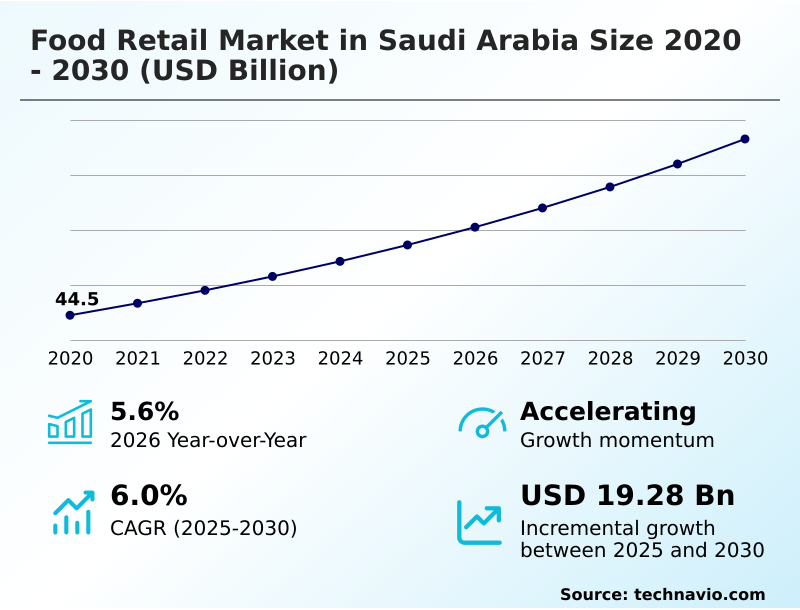

The Saudi Arabia Food Retail Market size was valued at USD 57.28 billion in 2025, growing at a CAGR of 6% during the forecast period 2026-2030.

Major Market Trends & Insights

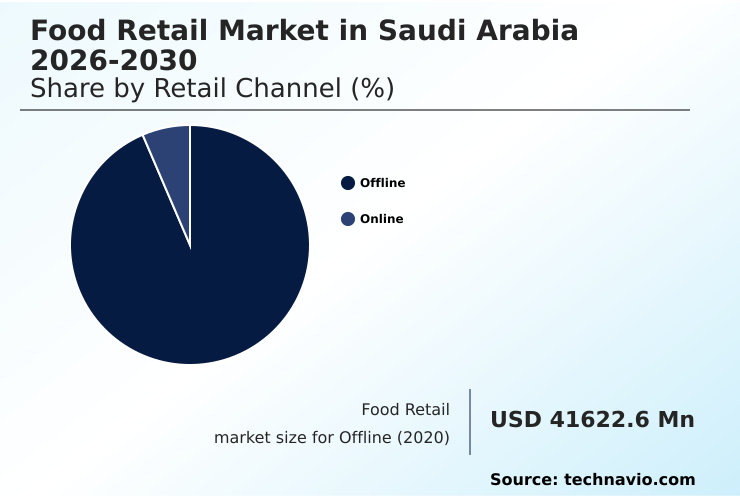

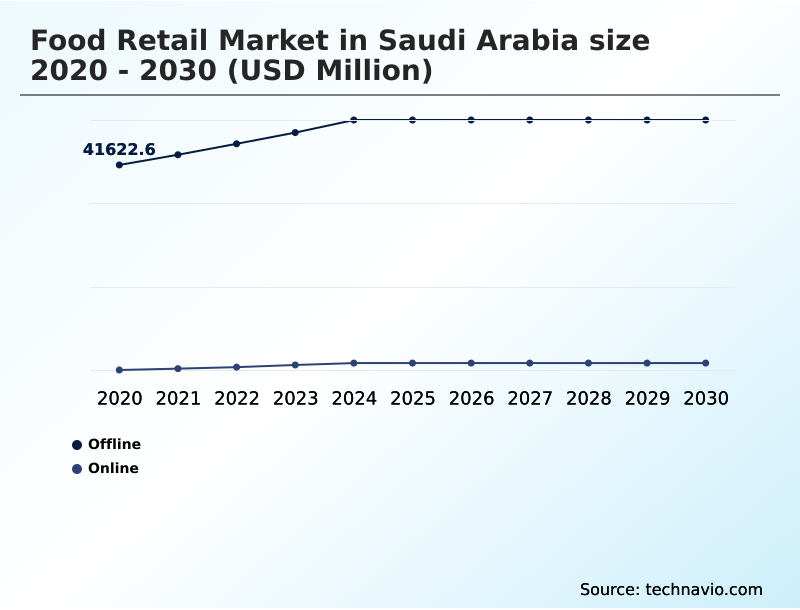

- By Retail Channel - Offline segment was valued at USD 50.12 billion in 2024

- By Packaging - Flexible segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 32.06 billion

- Market Future Opportunities 2025-2030: USD 19.28 billion

- CAGR from 2025 to 2030 : 6%

Market Summary

- The food retail market in Saudi Arabia is defined by a rapid structural shift, where modern retail formats now account for over 70% of grocery sales, a significant increase from a decade ago. This transition is driven by the expansion of hypermarkets and supermarkets, which cater to the demand for one-stop shopping.

- For instance, a retailer optimizing its supply chain through direct partnerships with local farmers can reduce spoilage rates for fresh produce by up to 15%, enhancing both profitability and sustainability. However, the sector faces considerable challenges, primarily the operational burden of food waste, which costs the national economy billions annually despite a 16% reduction achieved through national programs.

- Another significant driver is the digital transformation of retail, with companies leveraging data analytics to personalize the customer experience and streamline operations. The competitive environment and evolving consumer price sensitivity compel companies to innovate continuously, balancing physical expansion with robust e-commerce capabilities to maintain market share.

What will be the Size of the Saudi Arabia Food Retail Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Saudi Arabia Food Retail Market Segmented?

The saudi arabia food retail industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Retail channel

- Offline

- Online

- Packaging

- Flexible

- Semi-rigid

- Rigid

- Product type

- Fresh food

- Packaged or processed food

- Organic and health food

- Geography

- Middle East and Africa

- Saudi Arabia

- Middle East and Africa

How is the Saudi Arabia Food Retail Market Segmented by Retail Channel?

The offline segment is estimated to witness significant growth during the forecast period.

The offline segment's modernization represents a significant investment, with some major chains upgrading over 60% of their physical network to enhance the in-store experience.

This transformation involves redesigning the retail store layout and integrating advanced point-of-sale systems to improve transaction speed by up to 25% compared to legacy setups.

The adoption of automated checkout systems and the introduction of a click-and-collect service bridge the gap between physical and digital channels. These modern trade formats are supported by sophisticated supermarket procurement strategies and vendor managed inventory to ensure product availability.

Such enhancements to physical stores, from hypermarkets to convenience store merchandising, remain critical as they are pivotal in shaping consumer purchasing behavior and strengthening customer loyalty programs.

The Offline segment was valued at USD 50.12 billion in 2024 and showed a gradual increase during the forecast period.

What are the key Drivers, Trends, and Challenges in the Saudi Arabia Food Retail Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic planning in the food retail market in Saudi Arabia 2026-2030 requires a multi-faceted approach addressing distinct consumer segments and operational pressures. A key area of focus is understanding food retail market in saudi arabia 2026-2030 fresh food trends, where consumer demand for locally sourced, high-quality produce necessitates investment in cold chain logistics and direct farm partnerships.

- This shift can improve product freshness, a key differentiator, and reduce transport-related spoilage by over 10% compared to traditional import-heavy models. Simultaneously, retailers must navigate food retail market in saudi arabia 2026-2030 online grocery challenges, such as managing last-mile delivery costs and ensuring order accuracy, which can impact customer retention.

- Developing a robust food retail market in saudi arabia 2026-2030 private label strategy is crucial for competing on price, as these products offer consumers significant savings and provide retailers with higher margins.

- Furthermore, a focus on the food retail market in saudi arabia 2026-2030 supply chain localization not only supports national food security goals but also builds resilience against global disruptions.

- Finally, implementing food retail market in saudi arabia 2026-2030 sustainable retail operations, including energy-efficient stores and waste reduction programs, is becoming a critical factor for brand reputation and long-term operational cost management.

What are the key market drivers leading to the rise in the adoption of Saudi Arabia Food Retail Industry?

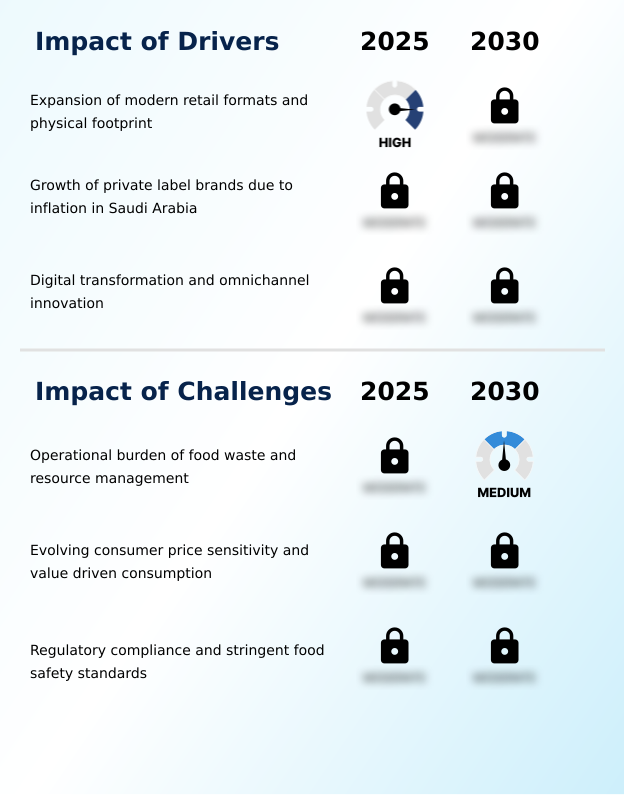

- The expansion of modern retail formats and the extension of physical footprints are the primary drivers of market growth.

- Digital transformation in retail is a primary driver, with the adoption of dynamic pricing algorithms increasing margins on select items by up to 5%, while demand forecasting analytics improve inventory accuracy.

- This technological shift is accelerating the growth of the online grocery business model.

- Another key driver is the expansion of private label manufacturing, which addresses consumer price sensitivity analysis by offering alternatives that are on average 20% more cost-effective than national brands.

- This strategy enhances hypermarket operational efficiency and allows for personalized marketing using customer data analytics. Some operators are also exploring an asset-light retail model, focusing on smaller formats to expand reach without significant capital outlay.

What are the market trends shaping the Saudi Arabia Food Retail Industry?

- An emphasis on sustainability and the localization of the food supply chain is emerging as a significant market trend, reshaping procurement and operational strategies.

- A significant trend is the push toward sustainability, with retailers adopting sustainable packaging solutions and smart refrigeration, reducing energy consumption by over 15%. This focus on energy efficient operations aligns with national goals, bolstering food security contribution through robust local sourcing initiatives.

- Concurrently, the integration of health services is reshaping retail spaces, with some chains seeing a 10% increase in foot traffic after adding integrated pharmacy services. This convergence improves the handling of perishable goods through better quality control mechanisms.

- These shifts, coupled with advanced e-commerce platform integration, demonstrate a move toward a holistic, service-oriented model that follows circular economy principles and strengthens the domestic supply chain.

What challenges does the Saudi Arabia Food Retail Industry face during its growth?

- The operational burden of food waste and inefficient resource management presents a key challenge to the industry's growth trajectory.

- Operational challenges are significant, with food waste reduction targets pressuring retailers to improve shelf-life management, as nearly 16% of food loss occurs at the retail stage. This requires stringent quality control mechanisms and advanced stock keeping unit (sku) rationalization to minimize spoilage of perishable goods.

- Furthermore, navigating complex regulatory framework adherence for food safety adds another layer of operational cost, demanding investments that can reduce margins by 3-5%. The increasing consumer demand for rapid delivery also tests supply chain resilience, particularly in last-mile delivery from both traditional stores and dark store fulfillment centers, where inconsistent performance can negatively impact consumer purchasing behavior.

Exclusive Technavio Analysis on Customer Landscape

The saudi arabia food retail market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the saudi arabia food retail market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Saudi Arabia Food Retail Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, saudi arabia food retail market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abdullah Al Othaim Markets Co. - Key offerings encompass a multi-format retail model, providing groceries and household goods through hypermarkets, supermarkets, and integrated digital platforms.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abdullah Al Othaim Markets Co.

- Al Dabbagh Group

- Al Raya Supermarket

- Aljazera

- Al Nahda Group

- Alsadhan Trading Co

- Amazon.com Inc.

- Astra Food Co.

- Bindawood Holding Co.

- Carrefour SA

- Jeddah Central Markets Co.

- Lulu Group International

- Manuel Market

- Nana

- One Meem

- Savola Group

- SPAR Group Inc.

- Speedy

- Tamimi Markets

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Broadline Retail industry, the accelerated adoption of omnichannel strategies has become standard, directly impacting the food retail market by forcing incumbents to integrate physical stores with seamless e-commerce platform integration and click-and-collect service options to meet evolving consumer purchasing behavior.

- The widespread deployment of advanced data analytics and AI for personalized marketing has enabled broadline retailers to improve customer retention by over 15%, compelling food retailers to adopt similar customer data analytics to refine product assortment strategy and loyalty programs.

- Heightened focus on supply chain resilience has led to increased investment in localized sourcing and advanced warehouse management systems, influencing the food retail market by prioritizing local sourcing initiatives to mitigate global disruptions and improve food security contribution.

- An industry-wide push toward sustainable operations has resulted in significant capital expenditure on energy efficient operations, with retailers achieving up to 20% reduction in energy consumption, creating a competitive pressure on food retailers to adopt green technologies and circular economy principles.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Saudi Arabia Food Retail Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 179 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6% |

| Market growth 2026-2030 | USD 19277.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.6% |

| Key countries | Saudi Arabia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The food retail ecosystem in Saudi Arabia operates on a complex value chain, where over 80% of products move through modern trade formats. The ecosystem begins with a mix of international and increasingly local suppliers providing raw and processed goods, who must adhere to stringent SFDA quality control mechanisms.

- Major retailers like hypermarkets and supermarkets act as the primary distribution channels, leveraging advanced warehouse management systems and their vast physical footprints. The regulatory framework adherence, including halal certification standards, is a non-negotiable aspect overseen by government bodies. Technology providers are critical enablers, offering solutions from point-of-sale systems to e-commerce platform integration.

- The final link is the consumer, whose purchasing behavior is increasingly shaped by price sensitivity and a demand for convenience, driving the growth of both private labels and quick commerce operations.

What are the Key Data Covered in this Saudi Arabia Food Retail Market Research and Growth Report?

-

What is the expected growth of the Saudi Arabia Food Retail Market between 2026 and 2030?

-

The Saudi Arabia Food Retail Market is expected to grow by USD 19.28 billion during 2026-2030, registering a CAGR of 6%. Year-over-year growth in 2026 is estimated at 5.6%%. This acceleration is shaped by expansion of modern retail formats and physical footprint, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Retail Channel (Offline, and Online), Packaging (Flexible, Semi-rigid, and Rigid), Product Type (Fresh food, Packaged or processed food, and Organic and health food) and Geography (Middle East and Africa). Among these, the Offline segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers Middle East and Africa. Country-level analysis includes Saudi Arabia, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is expansion of modern retail formats and physical footprint, which is accelerating investment and industry demand. The main challenge is operational burden of food waste and resource management, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Saudi Arabia Food Retail Market?

-

Key vendors include Abdullah Al Othaim Markets Co., Al Dabbagh Group, Al Raya Supermarket, Aljazera, Al Nahda Group, Alsadhan Trading Co, Amazon.com Inc., Astra Food Co., Bindawood Holding Co., Carrefour SA, Jeddah Central Markets Co., Lulu Group International, Manuel Market, Nana, One Meem, Savola Group, SPAR Group Inc., Speedy and Tamimi Markets. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape in Saudi Arabia’s food retail market is highly active, with major players driving consolidation and expansion, capturing over 65% of the modern trade sector. Abdullah Al-Othaim Markets' move to acquire a majority stake in Manuel Market signals a strategy to absorb premium chains and diversify its customer base.

- Similarly, Lulu Group International’s expansion, marked by the opening of its 70th hypermarket, underscores the ongoing investment in physical store footprints, particularly in secondary cities. This physical growth is complemented by significant investments in localization, such as Almarai’s multi-billion dollar plan to boost domestic production, which aims to reduce import reliance.

- These strategic maneuvers reflect a direct response to rising consumer demand for both value and convenience. The primary challenge remains balancing the high capital expenditure of brick-and-mortar growth with the necessary investments in e-commerce and last-mile delivery infrastructure.

We can help! Our analysts can customize this saudi arabia food retail market research report to meet your requirements.

RIA -

RIA -