Food Service Equipment Market Size 2026-2030

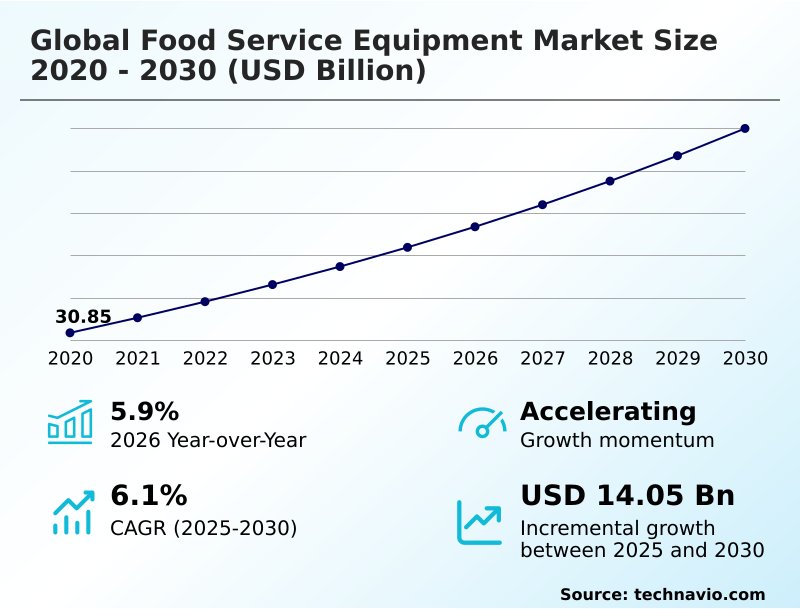

The food service equipment market size is valued to increase by USD 14.05 billion, at a CAGR of 6.1% from 2025 to 2030. Technological integration and proliferation of kitchen automation will drive the food service equipment market.

Major Market Trends & Insights

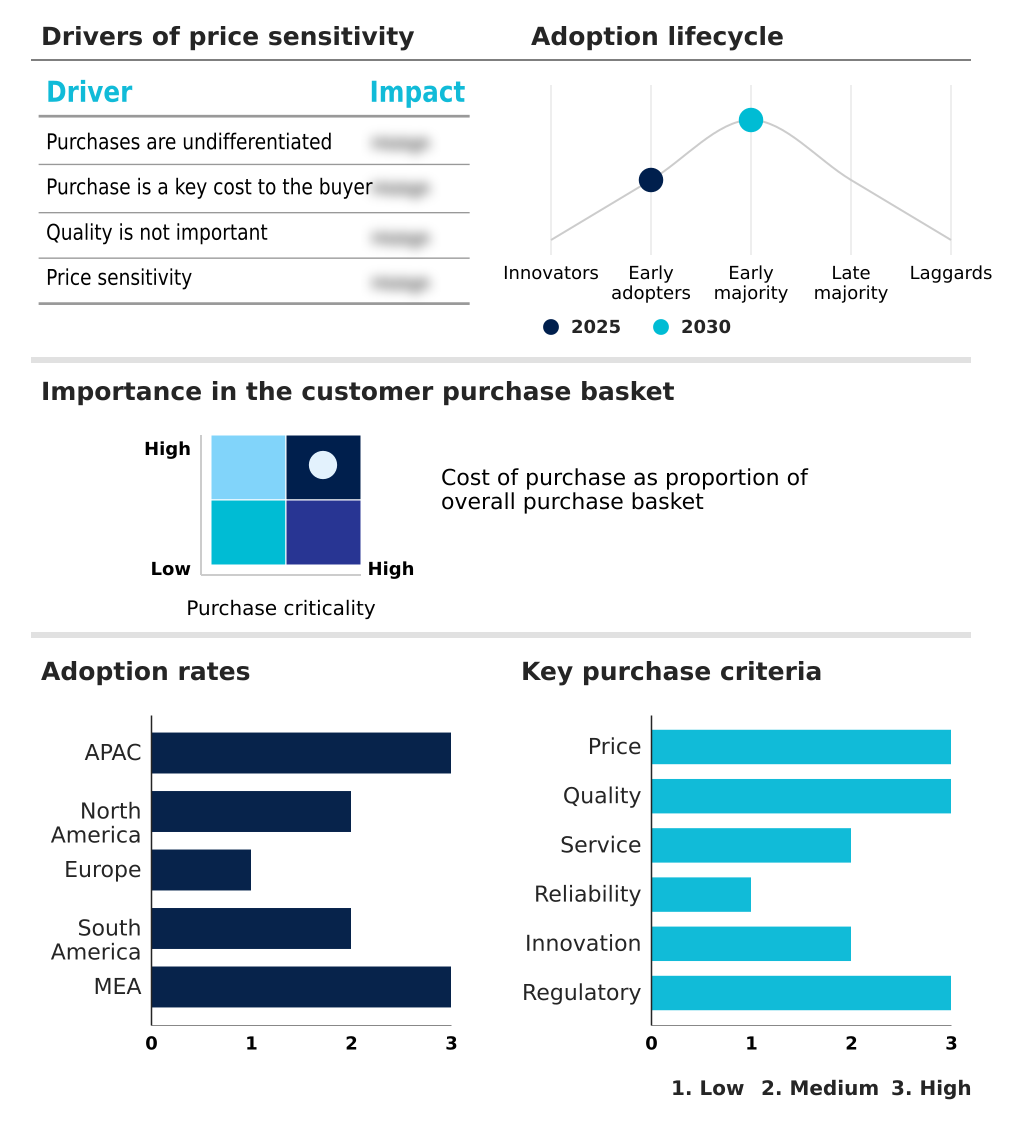

- APAC dominated the market and accounted for a 43.1% growth during the forecast period.

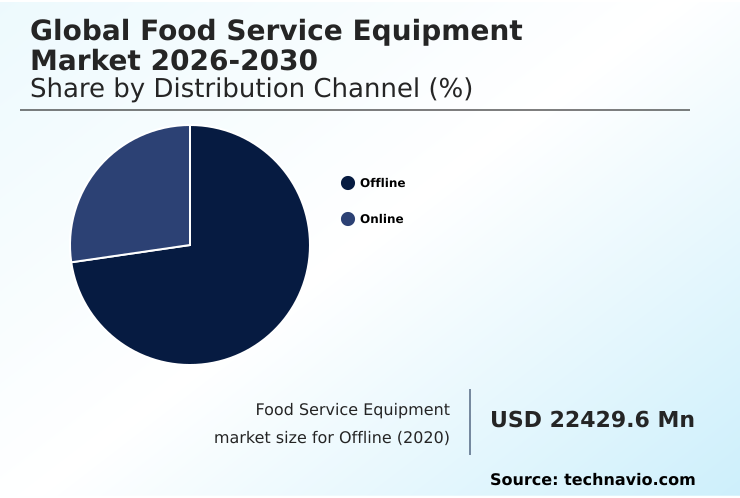

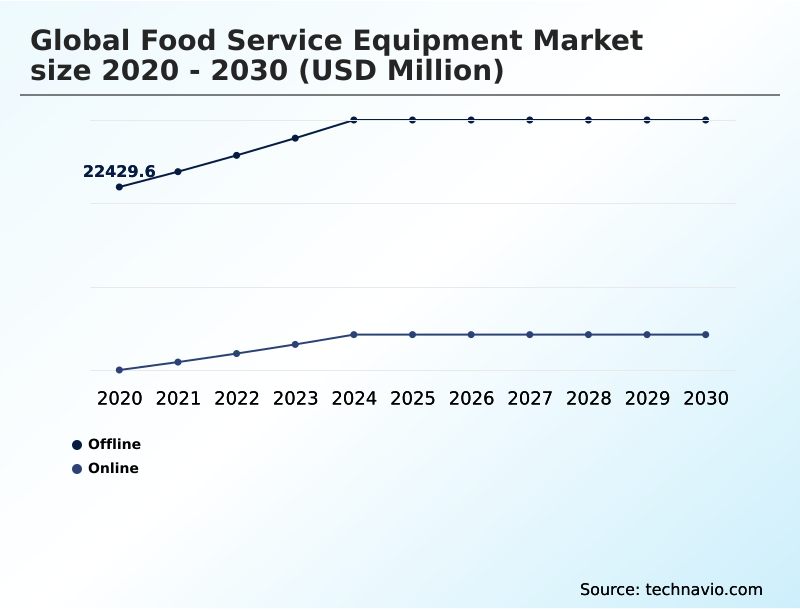

- By Distribution Channel - Offline segment was valued at USD 27.56 billion in 2024

- By Product - Cooking and preparation equipment segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 24.15 billion

- Market Future Opportunities: USD 14.05 billion

- CAGR from 2025 to 2030 : 6.1%

Market Summary

- The Food Service Equipment Market is undergoing a significant transformation, shaped by the convergence of operational efficiency demands and technological innovation. Key drivers include the pressing need for kitchen automation to address labor shortages and the adoption of sustainable kitchen infrastructure to meet stringent environmental regulations and reduce long-term utility costs.

- The rise of off-premise dining solutions has spurred demand for specialized ghost kitchen equipment and modular cooking suites that optimize space in urban environments.

- For instance, a large-scale catering company can leverage an integrated kitchen operating system to synchronize its blast chillers and combi-ovens, ensuring food safety standards are met across a distributed network of satellite kitchens while improving energy load balancing. This data-driven kitchen management enhances culinary production and reduces waste.

- However, the industry faces challenges from supply chain fragility, where shortages of key components like semiconductor modules can halt production, and the high capital outlay required for advanced culinary hardware. The technical skill gaps among staff to operate and maintain these complex systems also present a significant hurdle to widespread adoption.

- Successfully navigating these dynamics requires strategic investment in both technology and training to unlock the full potential of the modern commercial kitchen.

What will be the Size of the Food Service Equipment Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Food Service Equipment Market Segmented?

The food service equipment industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Distribution channel

- Offline

- Online

- Product

- Cooking and preparation equipment

- Refrigeration equipment

- Ware washing equipment

- Storage and handling equipment

- Others

- End-user

- Full-service restaurants and hotels

- Quick-service restaurants

- Institutional

- Others

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Distribution Channel Insights

The offline segment is estimated to witness significant growth during the forecast period.

The offline distribution channel remains fundamental to the Global Food Service Equipment Market 2026-2030, particularly for operators making investments involving high capital outlay.

This channel provides essential hands-on evaluation of culinary hardware, allowing buyers to assess the build quality of high-grade stainless steel equipment and witness demonstrations of thermal processing in combi-ovens and conveyor ovens.

Distributors offer critical consultation for complex installations, such as ware washing systems or steam-jacketed kettles for high-volume food preparation, which improves procurement accuracy and reduces costly post-purchase modifications by over 25%.

The physical presence of showrooms facilitates trust and supports the logistical complexities of delivering heavy machinery.

This segment's value is reinforced by indispensable after-sales support and maintenance, which are vital for ensuring the longevity of advanced equipment and upholding hygiene and safety standards.

The Offline segment was valued at USD 27.56 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 43.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Food Service Equipment Market Demand is Rising in APAC Get Free Sample

The market's geographic landscape is diverse, with North America and Europe leading in the adoption of advanced automation to counter high labor costs. In these regions, the deployment of robotic cooking systems and automated dishwashing units is common.

Data-driven kitchen management platforms, which utilize predictive maintenance algorithms, have improved operational uptime by 15%.

APAC is the fastest-growing region, contributing over 43% of the incremental growth, fueled by urbanization and the expansion of delivery-centric business models in countries like China and India.

The demand here is for high-speed ovens and induction ranges that support high-volume production.

South America and the Middle East and Africa are modernizing their hospitality infrastructure, creating opportunities for equipment featuring advanced thermal engineering and refrigeration cycles that use natural refrigerants.

Across all regions, remote diagnostics are becoming essential for servicing equipment in both dense urban centers and remote resort locations.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of the Global Food Service Equipment Market 2026-2030 is marked by a focus on targeted technological solutions. The benefits of open API in kitchen ecosystems are becoming clear, allowing for seamless integration across platforms. This is critical for the digital platforms for kitchen energy management that are now essential for optimizing operational costs.

- For instance, the use of smart combi-ovens with infrared sensors can reduce cooking inconsistencies by over 30% compared to manually operated units. The role of automation in mitigating labor shortages is driving investment in robotic systems for high-volume restaurants and automated warewashing with heat recovery.

- The comparison of HFCs vs natural refrigerants is a key consideration, pushing firms towards natural refrigerant based cooling systems to meet sustainability goals and regulatory mandates. The rise of delivery models has made optimizing food service equipment for delivery models a priority, with modular equipment for ghost kitchens and ventless cooking technology for urban spaces becoming standard.

- However, challenges in retrofitting smart kitchen tech persist, exacerbated by the impact of high capital outlay on SMEs. The industry is also grappling with supply chain risks for semiconductor modules and is addressing the training requirements for advanced kitchen systems.

- Sustainability drivers in commercial kitchen design are now at the forefront, influencing everything from the adoption of energy-efficient induction cooking suites to the implementation of the circular economy in food service equipment manufacturing, while 5G network slicing for industrial kitchens enables the necessary connectivity for these advanced systems.

What are the key market drivers leading to the rise in the adoption of Food Service Equipment Industry?

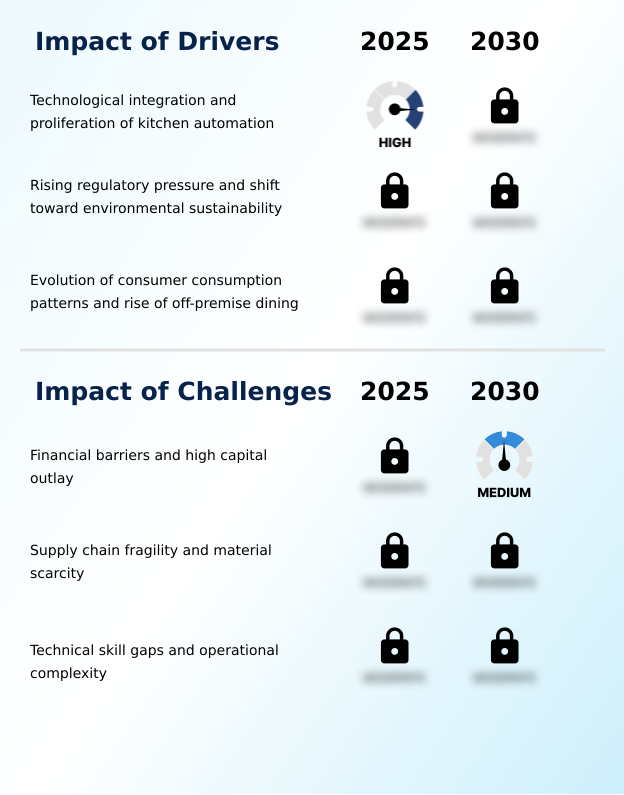

- Technological integration and the proliferation of kitchen automation are key drivers of the market.

- A key market driver is the need for enhanced kitchen operational efficiency, especially for high-volume food preparation.

- The shift toward off-premise dining has accelerated demand for specialized ghost kitchen equipment, including modular cooking suites and ventless cooking technology, which optimize kitchen workflow optimization in compact spaces.

- Resource efficiency is another significant driver, pushing for the replacement of systems using high-global-warming-potential hydrofluorocarbons. Advanced appliances such as combi-ovens and blast chillers are central to modern production, improving output consistency by over 25%.

- Enhanced ware washing systems contribute to both hygiene and resource conservation. The use of digital diagnostic tools for smart asset management enables operators to monitor performance remotely, leading to a 15% reduction in annual maintenance costs for connected equipment.

What are the market trends shaping the Food Service Equipment Industry?

- The advancement of integrated smart kitchen ecosystems is an upcoming market trend. This involves converging professional-grade hardware with sophisticated software platforms.

- A primary trend is the rapid advancement of the smart kitchen ecosystem, enabled by the internet of things for commercial kitchen automation. This trend supports delivery-centric business models by improving efficiency. The adoption of robotic cooking systems and automated dishwashing units reduces reliance on manual labor, with some operators reporting a 20% increase in throughput.

- Predictive maintenance algorithms are a cornerstone of data-driven kitchen management, decreasing equipment failure rates. Sustainable kitchen infrastructure is also gaining traction, marked by the use of natural refrigerants and the application of circular economy principles in manufacturing.

- The integration of remote diagnostics into equipment for off-premise dining solutions ensures that maintenance can be performed preemptively, with connected systems showing a 30% faster issue resolution time compared to non-connected counterparts.

What challenges does the Food Service Equipment Industry face during its growth?

- Financial barriers and high capital outlay are key challenges affecting industry growth.

- A significant challenge is the high upfront cost of advanced culinary technology, which can deter investment in energy-efficient equipment. The operational complexity of modern systems for industrial hospitality applications also creates hurdles. For instance, integrating automated beverage dispensing systems with centralized management platforms requires robust low-latency communication.

- The transition to carbon-neutral cooking equipment, while beneficial for energy load balancing, requires substantial capital. Even with proven benefits, such as water-recycling dishwashers reducing water use by up to 40%, the initial investment remains a barrier.

- The need for professional sanitation systems is non-negotiable, yet retrofitting conveyor ovens or steam-jacketed kettles with heat recovery modules and energy-efficient compressors adds to the financial strain. Properly functioning food holding systems are critical, but their integration into a smart kitchen network presents technical challenges.

Exclusive Technavio Analysis on Customer Landscape

The food service equipment market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the food service equipment market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Food Service Equipment Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, food service equipment market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ali Group Srl - An extensive portfolio of professional food service equipment, including cooking, refrigeration, and warewashing systems, is provided for the global hospitality and commercial kitchen markets.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ali Group Srl

- Alto Shaam Inc.

- Cambro Manufacturing Co.

- Duke Manufacturing

- Electrolux Professional AB

- Fagor Industrial S. Coop

- Hatco Corp.

- HOSHIZAKI Corp.

- Illinois Tool Works Inc.

- Maschinenfabrik GmbH Co. KG

- MEIKO Maschinenbau GmbH and Co.

- Panasonic Holdings Corp.

- RATIONAL Group

- ROBOT COUPE SNC.

- Sammic SL

- The Middleby Corp.

- The Vollrath Co. LLC

- True Manufacturing Co. Inc.

- UNOX S.p.A.

- Winterhalter Gastronom GmbH

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Food service equipment market

- In May 2025, a leading Japanese technology conglomerate introduced a universal software interface designed to synchronize different brands of kitchen appliances within a single management dashboard.

- In September 2025, a prominent European environmental commission finalized a comprehensive set of revised energy labeling requirements for all commercial-grade ware washing and cooling systems sold within the region.

- In October 2025, a prominent real estate development firm in the Asia-Pacific region completed a specialized industrial park exclusively designed for cloud kitchen operators, featuring standardized utility hookups for modular cooking suites.

- In August 2025, a major logistical bottleneck at a primary international shipping hub in East Asia caused a prolonged delay in the delivery of essential semiconductor modules used in digital oven controllers.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Food Service Equipment Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 306 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.1% |

| Market growth 2026-2030 | USD 14050.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.9% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The food service equipment market is defined by the integration of the internet of things to create a cohesive smart kitchen ecosystem. This evolution impacts boardroom decisions on capital expenditure, as investments shift toward robotic cooking systems and automated dishwashing units to combat labor shortages.

- Advanced thermal processing in combi-ovens and high-speed ovens, managed by digital oven controllers with infrared and spectral sensors, ensures consistency. Sustainability mandates drive the phase-out of high-global-warming-potential hydrofluorocarbons in favor of natural refrigerants, with refrigeration units now featuring energy-efficient and variable-speed compressors. Ware washing systems, including water-recycling dishwashers, incorporate heat recovery modules.

- The proliferation of ghost kitchen equipment and modular cooking suites relies on ventless cooking technology. Key components like programmable logic controllers, high-grade stainless steel with antimicrobial coatings, and crucial semiconductor modules are central to modern designs.

- The industry’s digital backbone is built on open application programming interfaces and enabled by technologies like the 5G-enabled network slice, which supports remote diagnostics and predictive maintenance algorithms, reducing equipment downtime by a significant margin.

- From steam-jacketed kettles to beverage dispensing systems and advanced food holding systems to blast chillers and conveyor ovens, technology is reshaping every aspect of kitchen operations.

What are the Key Data Covered in this Food Service Equipment Market Research and Growth Report?

-

What is the expected growth of the Food Service Equipment Market between 2026 and 2030?

-

USD 14.05 billion, at a CAGR of 6.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Distribution Channel (Offline, and Online), Product (Cooking and preparation equipment, Refrigeration equipment, Ware washing equipment, Storage and handling equipment, and Others), End-user (Full-service restaurants and hotels, Quick-service restaurants, Institutional, and Others) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Technological integration and proliferation of kitchen automation, Financial barriers and high capital outlay

-

-

Who are the major players in the Food Service Equipment Market?

-

Ali Group Srl, Alto Shaam Inc., Cambro Manufacturing Co., Duke Manufacturing, Electrolux Professional AB, Fagor Industrial S. Coop, Hatco Corp., HOSHIZAKI Corp., Illinois Tool Works Inc., Maschinenfabrik GmbH Co. KG, MEIKO Maschinenbau GmbH and Co., Panasonic Holdings Corp., RATIONAL Group, ROBOT COUPE SNC., Sammic SL, The Middleby Corp., The Vollrath Co. LLC, True Manufacturing Co. Inc., UNOX S.p.A. and Winterhalter Gastronom GmbH

-

Market Research Insights

- The market is defined by a push towards greater kitchen operational efficiency and commercial kitchen automation. This drive is reshaping culinary production through advanced thermal engineering, refrigeration cycles, and mechanical processing. Firms adopting data-driven kitchen management achieve superior kitchen workflow optimization and smart asset management, with integrated kitchen operating systems improving resource efficiency by 15%.

- This advanced culinary technology is crucial for delivery-centric business models and off-premise dining solutions. However, challenges like high capital outlay, technical skill gaps, and supply chain fragility persist. The adoption of sustainable kitchen infrastructure, incorporating circular economy principles in manufacturing and carbon-neutral cooking equipment, addresses these issues.

- Operators are leveraging digital diagnostic tools and professional sanitation systems to uphold stringent food safety and hygiene standards. These systems support the cold chain infrastructure and enable high-volume food preparation, with low-latency communication being essential for industrial hospitality applications, improving energy load balancing by up to 20% compared to legacy systems.

We can help! Our analysts can customize this food service equipment market research report to meet your requirements.

RIA -

RIA -