Frozen Breakfast Foods Market Size 2026-2030

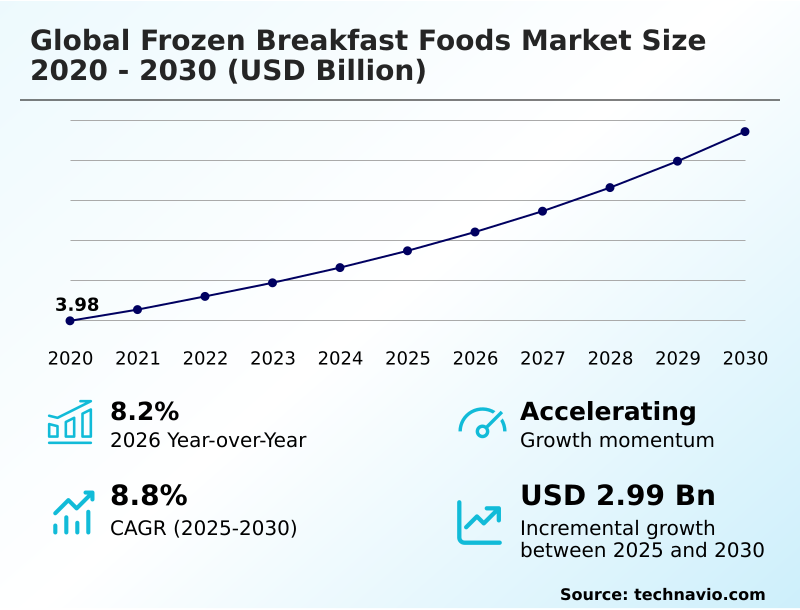

The Frozen Breakfast Foods Market size was valued at USD 5.73 billion in 2025, growing at a CAGR of 8.8% during the forecast period 2026-2030.

Major Market Trends & Insights

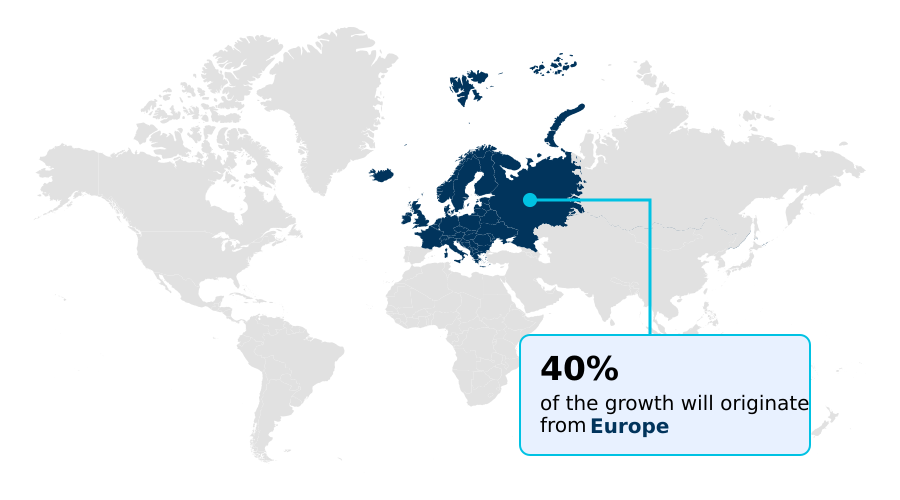

- Europe dominated the market and accounted for a 39.7% growth during the forecast period.

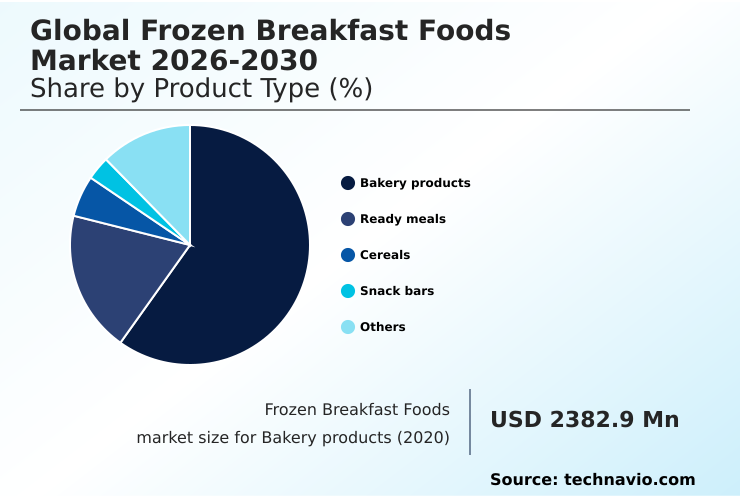

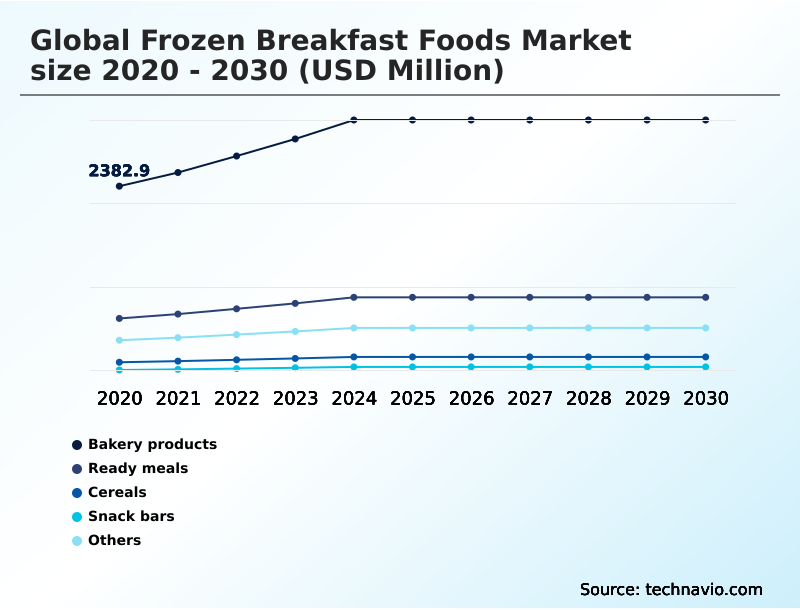

- By Product Type - Bakery products segment was valued at USD 3.20 billion in 2024

- By Distribution Channel - Offline segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 4.73 billion

- Market Future Opportunities 2025-2030: USD 2.99 billion

- CAGR from 2025 to 2030 : 8.8%

Market Summary

- The frozen breakfast foods market is defined by a strategic pivot toward nutrient-density, with products fortified with protein outpacing traditional offerings by a growth margin of nearly 15%.

- This shift is evident in supply chain operations, where manufacturers are retooling production lines to accommodate high-protein flour blends and plant-based ingredients, a move that increases raw material costs but reduces spoilage by 5% due to improved ingredient stability. A primary driver is the expansion of all-day breakfast consumption, which industrializes handheld formats for on-the-go consumers.

- However, the market faces a significant challenge from widespread consumer skepticism of ultra-processed foods. This forces a clean-label imperative, requiring the removal of artificial preservatives and enhancers, which complicates formulation and can impact shelf-life stability and texture in products like frozen waffles and breakfast sandwiches.

What will be the Size of the Frozen Breakfast Foods Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Frozen Breakfast Foods Market Segmented?

The frozen breakfast foods industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product type

- Bakery products

- Ready meals

- Cereals

- Snack bars

- Others

- Distribution channel

- Offline

- Online

- Flavor

- Sweet

- Savory

- Plain

- Geography

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- South Korea

- Middle East and Africa

- Saudi Arabia

- UAE

- Turkey

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- Europe

How is the Frozen Breakfast Foods Market Segmented by Product Type?

The bakery products segment is estimated to witness significant growth during the forecast period.

The bakery products segment, accounting for over 60.3% of the frozen breakfast foods market, is fundamentally driven by consumer demand for convenient, heat-and-eat morning staples like waffles and croissants.

This segment is experiencing a shift toward premiumization, with a 15% rise in products featuring artisanal textures and gourmet flavor profiles.

Advancements in flash-freezing technology and the use of high-protein flour blends are enabling manufacturers to create functional bakery goods that appeal to health-conscious demographics.

The logistical advantages, including extended shelf life and reduced food waste for both retailers and households, continue to support steady revenue growth, positioning this segment as a resilient and high-volume component of the international breakfast landscape.

The Bakery products segment was valued at USD 3.20 billion in 2024 and showed a gradual increase during the forecast period.

How demand for the Frozen Breakfast Foods market is rising in the leading region?

Europe is estimated to contribute 39.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Frozen Breakfast Foods Market demand is rising in Europe Request Free Sample

Regional dynamics in the frozen breakfast foods market show significant variance, with Europe holding a 39.7% share of the incremental growth, marginally ahead of North America's 37.6%.

This European dominance is largely propelled by Germany, which contributes over 18% to the regional market, where consumer demand for organic and non-GMO certified bakery products is highest.

In contrast, the North American market, led by the US, focuses more on high-protein, handheld formats like breakfast sandwiches and burritos, reflecting a faster-paced, convenience-driven lifestyle.

This divergence necessitates distinct product strategies; for instance, European product lines emphasize clean-label formulations and sustainable packaging, while North American innovation centers on functional benefits and portability. These regional preferences directly influence cold chain logistics and private-label premiumization strategies.

What are the key Drivers, Trends, and Challenges in the Frozen Breakfast Foods Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decisions in the frozen breakfast foods sector are increasingly data-driven, with manufacturers analyzing consumer queries to refine product development. For example, the search for the best high-protein frozen breakfast has led to a 20% increase in new product launches featuring fortified protein content over the last two years.

- This is nearly double the growth rate of traditional sweet bakery items. Consumers exploring plant-based frozen breakfast options are influencing supply chains, pushing for greater transparency in ingredient sourcing and prompting investment in next-generation soy and pea protein analogs.

- The demand for convenience is evident in searches for frozen breakfast for quick mornings, which directly correlates with the rising popularity of handheld formats and advanced microwaveable packaging that preserves texture. Families seeking gluten-free frozen breakfast sandwiches represent a key niche, driving innovation in alternative flours and clean-label formulations that avoid common allergens.

- Similarly, inquiries about low-sugar frozen breakfast foods are compelling brands to adopt natural sweeteners and reduce overall carbohydrate content, aligning with broader wellness trends. Understanding these specific consumer needs allows companies to create targeted products that resonate more effectively than mass-market offerings.

What are the key market drivers leading to the rise in the adoption of Frozen Breakfast Foods Industry?

- The expansion of all-day breakfast consumption, coupled with growing demand for handheld and portable formats, is a key driver for the market.

- The expansion of all-day breakfast consumption is a critical driver for the frozen breakfast foods market, with data showing that over 40% of such items are now consumed outside of traditional morning hours, a 15% increase from five years ago.

- This behavioral shift fuels demand for high-portability, handheld formats such as breakfast burritos and stuffed waffles that require minimal preparation.

- The industrialization of these convenient, on-the-go options is essential for capturing sales in non-traditional channels like convenience stores and quick-service restaurants.

- This trend aligns with modern, fragmented schedules, positioning frozen breakfast foods as versatile snacks or meal replacements and driving innovation in microwaveable packaging to enhance food quality and texture.

What are the market trends shaping the Frozen Breakfast Foods Industry?

- The institutionalization of private-label premiumization is an emerging market trend, characterized by tiered retail strategies that challenge established national brands.

- A primary trend reshaping the frozen breakfast foods market is the institutionalization of private-label premiumization, where retailer-owned brands now capture over 25% of the market share in some European countries, growing 1.5 times faster than national brands. This shift is driven by consumers seeking gourmet-style frozen waffles and organic breakfast bowls at a lower price point without sacrificing quality.

- This trend forces established CPG firms to accelerate innovation, particularly in clean-label formulations and the development of plant-based protein alternatives. Consequently, the freezer aisle is becoming a more competitive space, characterized by a rapid introduction of high-quality, house-branded products that often set the pace for removing artificial ingredients and adopting sustainable packaging, ultimately improving ingredient transparency for the end consumer.

What challenges does the Frozen Breakfast Foods Industry face during its growth?

- A key challenge affecting industry growth is the proliferation of skepticism toward ultra-processed foods and the corresponding imperative for clean-label formulations.

- A formidable challenge for the frozen breakfast foods market is the growing consumer skepticism toward ultra-processed foods (UPFs), with surveys indicating that nearly 49% of consumers are actively trying to limit their intake. This movement pressures manufacturers to pursue clean-label formulations, a costly process that can increase production expenses by up to 20%.

- The technical difficulty lies in removing synthetic preservatives and stabilizers from products like frozen breakfast sandwiches while maintaining expected taste, texture, and shelf life. Failure to transition toward nutrient-dense, whole-food-based alternatives risks significant market share loss to fresh and refrigerated options perceived as healthier by an increasingly ingredient-savvy consumer base.

Exclusive Technavio Analysis on Customer Landscape

The frozen breakfast foods market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the frozen breakfast foods market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Frozen Breakfast Foods Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, frozen breakfast foods market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ajinomoto Co. Inc. - Analysis reveals a portfolio focused on diversified frozen breakfast solutions, encompassing bowls and handheld formats engineered for consumer convenience and modern lifestyles.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ajinomoto Co. Inc.

- Al Kabeer Group

- Conagra Brands Inc.

- Corporativo Bimbo SA de CV

- Dr August Oetker KG

- General Mills Inc.

- Gujarat Co. Milk Ltd.

- Hormel Foods Corp.

- iD Fresh Food India Pvt. Ltd

- ITC Ltd.

- Kellanova

- McCain Foods Ltd.

- Nestle SA

- Nomad Foods Ltd.

- Quirch Foods LLC

- Rich Products Corp.

- The Kraft Heinz Co.

- Turano Baking Co.

- Tyson Foods Inc.

- Unilever PLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Packaged Foods and Meats industry, heightened regulatory scrutiny on ultra-processed foods and mandatory front-of-pack nutritional labeling are compelling a reformulation of frozen breakfast foods. This requires a significant reduction in sodium and the removal of artificial preservatives to meet new health standards.

- The widespread adoption of sustainable packaging solutions, driven by new government mandates targeting single-use plastics, is impacting the frozen breakfast foods market by necessitating a shift to recyclable and compostable materials, which can increase packaging costs but enhances brand perception among eco-conscious consumers.

- The integration of IoT sensors and AI-driven analytics into cold chain logistics has become standard practice, improving temperature monitoring for temperature-sensitive products. This has successfully reduced spoilage rates by over 15% for items like frozen breakfast foods.

- The mainstreaming of plant-based proteins, moving beyond niche vegan markets, is compelling the frozen breakfast foods sector to innovate with next-generation meat and egg analogs, which now constitute a significant portion of new product launches in the category.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Frozen Breakfast Foods Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 305 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 8.8% |

| Market growth 2026-2030 | USD 2985.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 8.2% |

| Key countries | Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, China, Japan, South Korea, India, Australia, Indonesia, Saudi Arabia, UAE, Turkey, South Africa, Israel, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The frozen breakfast foods market ecosystem is a complex interplay of stakeholders, where raw material suppliers of items like high-protein flour and plant-based proteins form the foundational layer. These inputs are transformed by manufacturers, who must adhere to stringent food safety regulations, with compliance audits reducing recall incidents by up to 25%.

- The value chain is heavily influenced by distribution channels, where offline supermarkets and hypermarkets still account for over 80% of sales, leveraging their established cold chain infrastructure. However, online DTC subscription models and e-commerce platforms represent the fastest-growing channel, enabling niche brands to bypass traditional retail gatekeepers.

- End-users, ranging from time-constrained professionals to families, drive demand based on convenience, nutritional value, and flavor innovation. Supporting entities, including logistics providers specializing in the cold chain and packaging firms developing sustainable solutions, are critical for maintaining product integrity and meeting consumer expectations for environmental responsibility.

What are the Key Data Covered in this Frozen Breakfast Foods Market Research and Growth Report?

-

What is the expected growth of the Frozen Breakfast Foods Market between 2026 and 2030?

-

The Frozen Breakfast Foods Market is expected to grow by USD 2.99 billion during 2026-2030, registering a CAGR of 8.8%. Year-over-year growth in 2026 is estimated at 8.2%%. This acceleration is shaped by expansion of all-day breakfast consumption and handheld portability, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Product Type (Bakery products, Ready meals, Cereals, Snack bars, and Others), Distribution Channel (Offline, and Online), Flavor (Sweet, Savory, and Plain) and Geography (Europe, North America, APAC, Middle East and Africa, South America). Among these, the Bakery products segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers Europe, North America, APAC, Middle East and Africa and South America. Europe is estimated to contribute 39.7% to market growth during the forecast period. Country-level analysis includes Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, China, Japan, South Korea, India, Australia, Indonesia, Saudi Arabia, UAE, Turkey, South Africa, Israel, Brazil, Argentina and Chile, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is expansion of all-day breakfast consumption and handheld portability, which is accelerating investment and industry demand. The main challenge is proliferation of ultra-processed food skepticism and clean label imperative, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Frozen Breakfast Foods Market?

-

Key vendors include Ajinomoto Co. Inc., Al Kabeer Group, Conagra Brands Inc., Corporativo Bimbo SA de CV, Dr August Oetker KG, General Mills Inc., Gujarat Co. Milk Ltd., Hormel Foods Corp., iD Fresh Food India Pvt. Ltd, ITC Ltd., Kellanova, McCain Foods Ltd., Nestle SA, Nomad Foods Ltd., Quirch Foods LLC, Rich Products Corp., The Kraft Heinz Co., Turano Baking Co., Tyson Foods Inc. and Unilever PLC. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape for frozen breakfast foods is highly consolidated, with the top five vendors commanding over 45% of the market share through aggressive innovation in nutrient-density. Key players like Conagra Brands and Kellanova are focusing on high-protein and restaurant-inspired formats to meet evolving consumer demands.

- For instance, recent product launches feature over 20% more protein per serving compared to legacy items. This strategic shift directly addresses the all-day breakfast trend, where breakfast items are consumed as snacks or meal replacements. This innovation push is a response to the challenge posed by premium private-label offerings from major retailers, which have intensified price competition.

- To maintain margins, companies are optimizing cold chain logistics and investing in automated production to offset the rising costs of clean-label ingredients.

We can help! Our analysts can customize this frozen breakfast foods market research report to meet your requirements.

RIA -

RIA -