Mobile Gaming Market Size 2026-2030

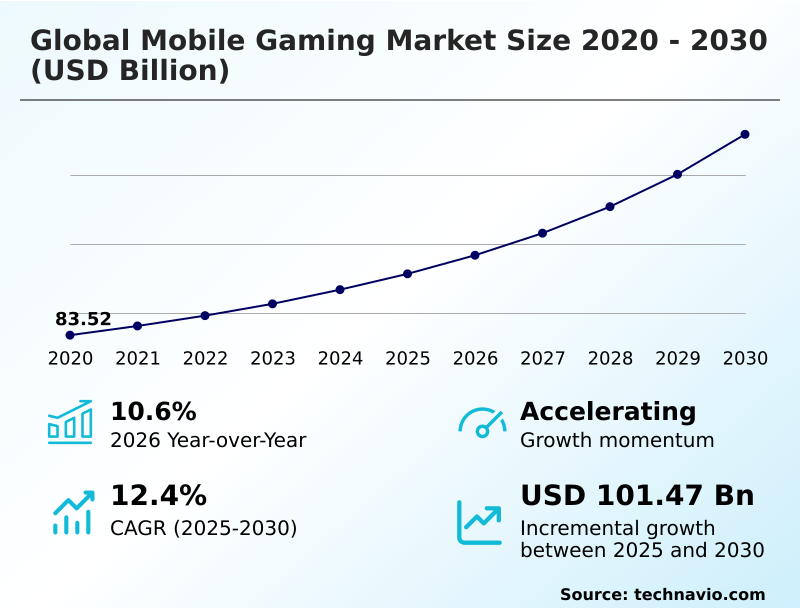

The mobile gaming market size is valued to increase by USD 101.47 billion, at a CAGR of 12.4% from 2025 to 2030. Institutionalization of high-fidelity cloud streaming and hyper-connectivity will drive the mobile gaming market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 54.9% growth during the forecast period.

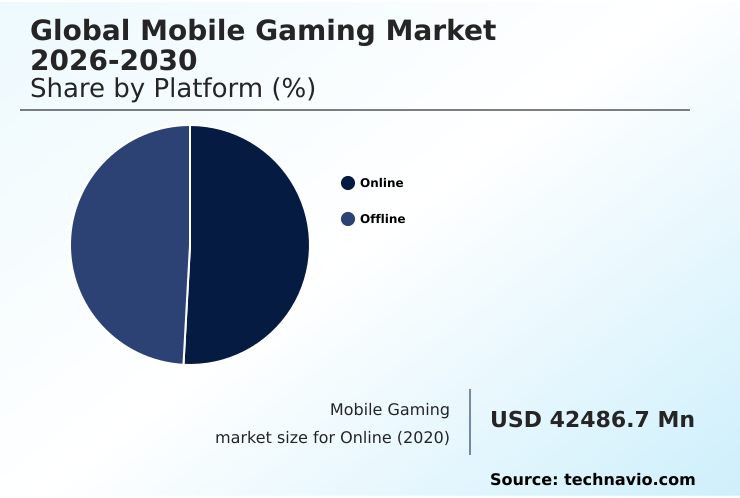

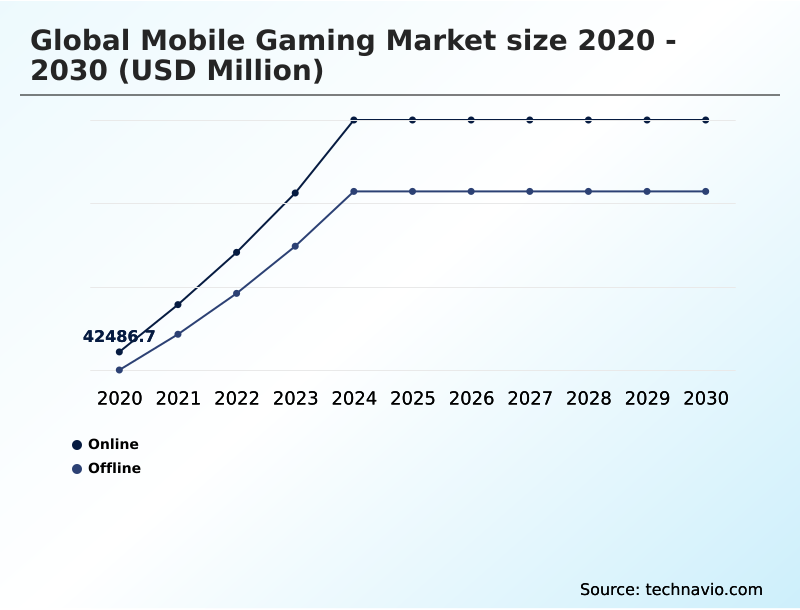

- By Platform - Online segment was valued at USD 61.18 billion in 2024

- By Type - Casual gaming segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 146.07 billion

- Market Future Opportunities: USD 101.47 billion

- CAGR from 2025 to 2030 : 12.4%

Market Summary

- The mobile gaming market is undergoing a sophisticated evolution, moving beyond simple diversions to become a primary ecosystem for immersive entertainment. This growth is underpinned by the adoption of high-performance mobile processors and 5G, enabling high-fidelity cloud streaming and complex real-time multiplayer performance. Developers utilize cloud-native architectures and agentic artificial intelligence for live-ops optimization, reducing overhead while enhancing user retention.

- A key business scenario sees studios implementing cross-platform interoperability and automated content pipelines, allowing users to transition seamlessly. This shift toward hardware-agnostic gaming is powered by cloud-native game development, redefining the experience. As a result, business models are shifting toward hybrid-casual monetization and direct-to-consumer monetization to maximize player retention and lifetime value.

- The focus on social ecosystem integration, data-driven personalization, and engaging single-player narratives ensures long-term player investment, solidifying mobile gaming as a cornerstone of digital entertainment.

What will be the Size of the Mobile Gaming Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Mobile Gaming Market Segmented?

The mobile gaming industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Platform

- Online

- Offline

- Type

- Casual gaming

- Professional gaming

- End-user

- Casual gamers

- Mid-core gamers

- Hardcore gamers

- Others

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- South Africa

- UAE

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

By Platform Insights

The online segment is estimated to witness significant growth during the forecast period.

The online segment represents the technological vanguard of the industry, characterized by persistent connectivity and real-time social interaction. This platform leverages powerful cloud-native architectures for high-fidelity cloud streaming and live-ops optimization, delivering console-quality titles to mobile devices.

Developers are implementing cross-platform interoperability and agentic artificial intelligence to create vast digital entertainment ecosystems. The adoption of generative AI narrative frameworks results in dynamic, player-responsive ecosystems that move beyond static scripts.

The re-launch of a major title following a platform dispute led to approximately 7.5 million downloads in a single month, underscoring the consumer appetite for this interconnected social experience, which fosters high-LTV genres and supports the use of procedural generation tools for continuous content delivery.

The Online segment was valued at USD 61.18 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 54.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Mobile Gaming Market Demand is Rising in APAC Get Free Sample

The geographic landscape is characterized by high-growth emerging markets and mature, high-value regions. APAC accounts for over 54% of the market’s incremental growth, driven by a mobile-first consumer psychology.

In contrast, regulatory maturation in regions like South America is evident; a recent tax framework adjustment in Brazil increased federal revenue from the sector by 23%.

This global diversity requires developers to use sophisticated game development engines and digital distribution platforms. Key considerations include implementing digital safety measures, addressing screen time management, and providing transparent loot box disclosures.

The focus is on creating sustainable in-game economies within the freemium monetization model, supported by robust anti-cheat systems and compelling single-player narratives, to drive both cognitive stimulation and long-term engagement across multiplayer online battle arenas and real-time strategy games.

Market Dynamics

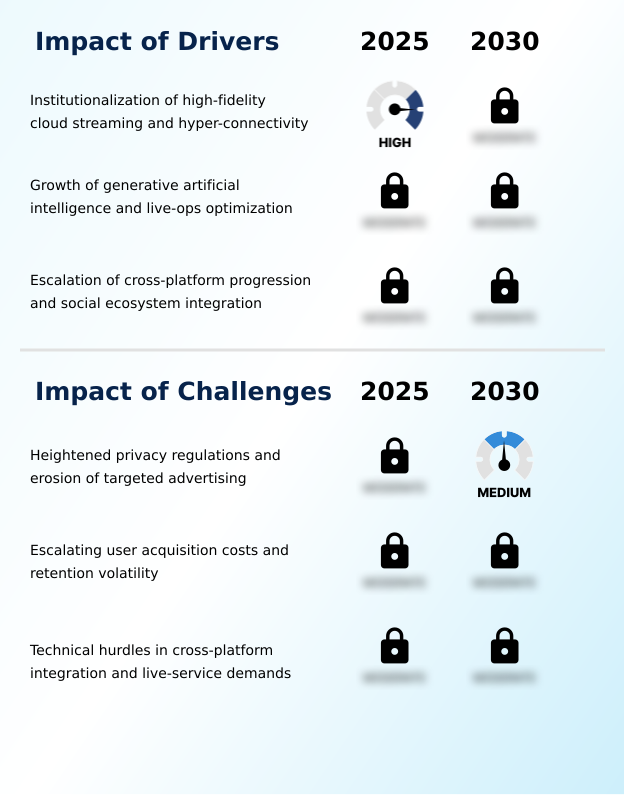

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the mobile gaming sector is increasingly complex, shaped by technological and regulatory shifts. A core consideration is the cross-platform progression for Global Mobile Gaming Market 2026-2030, which has become a standard user expectation, forcing a unified development approach.

- Simultaneously, the role of generative AI in Global Mobile Gaming Market 2026-2030 asset creation is transitioning from a novelty to a necessity, promising to reduce production timelines and operational costs significantly. The cloud streaming impact on Global Mobile Gaming Market 2026-2030 hardware requirements is another critical factor, decoupling premium experiences from on-device processing power and broadening the potential audience.

- To manage these new ecosystems, effective live-ops management strategies in Global Mobile Gaming Market 2026-2030 are paramount for maintaining player engagement and driving long-term revenue. This is particularly vital in a market where over 95% of users typically abandon new titles within thirty days, highlighting the razor-thin margins for error in player retention.

- Furthermore, exploring direct-to-consumer monetization models for Global Mobile Gaming Market 2026-2030 allows publishers to build direct relationships with their most valuable players, bypassing traditional storefront commissions and gaining deeper insights into player behavior.

What are the key market drivers leading to the rise in the adoption of Mobile Gaming Industry?

- A key driver for the market is the institutionalization of high-fidelity cloud streaming and hyper-connectivity, enabling premium gaming experiences on mobile devices.

- The institutionalization of high-fidelity cloud streaming and hyper-connectivity is a primary market driver. This is enabled by cloud-native game development and a move toward a hardware-agnostic future. The proliferation of automated content pipelines and social ecosystem integration enhances user engagement.

- The use of advanced neural networks for user modeling achieved a 20% reduction in churn rates, demonstrating the power of algorithmic precision.

- Furthermore, the focus on high-LTV genres has seen in-app purchase revenue increase by 20% in the strategy segment alone. These developments, supported by mobile-first cloud access and the implementation of cross-save and cross-play functionalities, create a stickier environment.

- The deployment of server-side ray tracing and interactive ad formats further pushes the boundaries of hardware-agnostic gaming, supporting community-driven content and digital wallets.

What are the market trends shaping the Mobile Gaming Industry?

- The mobile gaming market is witnessing the industrialization of AI narrative frameworks. This trend transitions mobile environments from static scripts to dynamic, player-responsive ecosystems.

- A structural shift is underway toward the industrialization of generative AI and direct-to-consumer monetization strategies. Studios are moving to player-responsive ecosystems using on-device neural processing for data-driven personalization. This focus on player retention and lifetime value is critical. The adoption of cloud-enabled architectures has already reduced latency for cross-platform infrastructure by nearly 30%, enabling high-quality real-time multiplayer performance.

- The use of user acquisition and retention modeling is also key, with advanced neural networks achieving a 20% reduction in churn rates. This trend is optimizing hybrid-casual monetization and creating digital third places within low-latency network environments, catering to a mobile-first consumer psychology and supporting the expansion of esports infrastructure through dynamic difficulty curves and targeted in-app purchase recommendations.

What challenges does the Mobile Gaming Industry face during its growth?

- A primary challenge affecting industry growth is the combination of heightened privacy regulations and the subsequent erosion of targeted advertising capabilities.

- The market faces structural challenges from escalating user acquisition costs and privacy-related advertising erosion. Publishers are forced to increase spending by over 20% just to maintain active users, a response to rapid player churn where over 95% of users abandon new titles within 30 days.

- This landscape is complicated by the variety of mobile operating systems and the performance demands on high-performance mobile processors. The reliance on digital storefronts and their commission structures puts pressure on in-game monetization strategies. To counter this, some are exploring user-generated content platforms and real-time narrative adjustments.

- However, the capital required to build out proprietary cloud-based gaming services remains high, challenging the viability of premium ad-free versions and data-efficient casual games without sophisticated advanced analytics software and mobile payment systems.

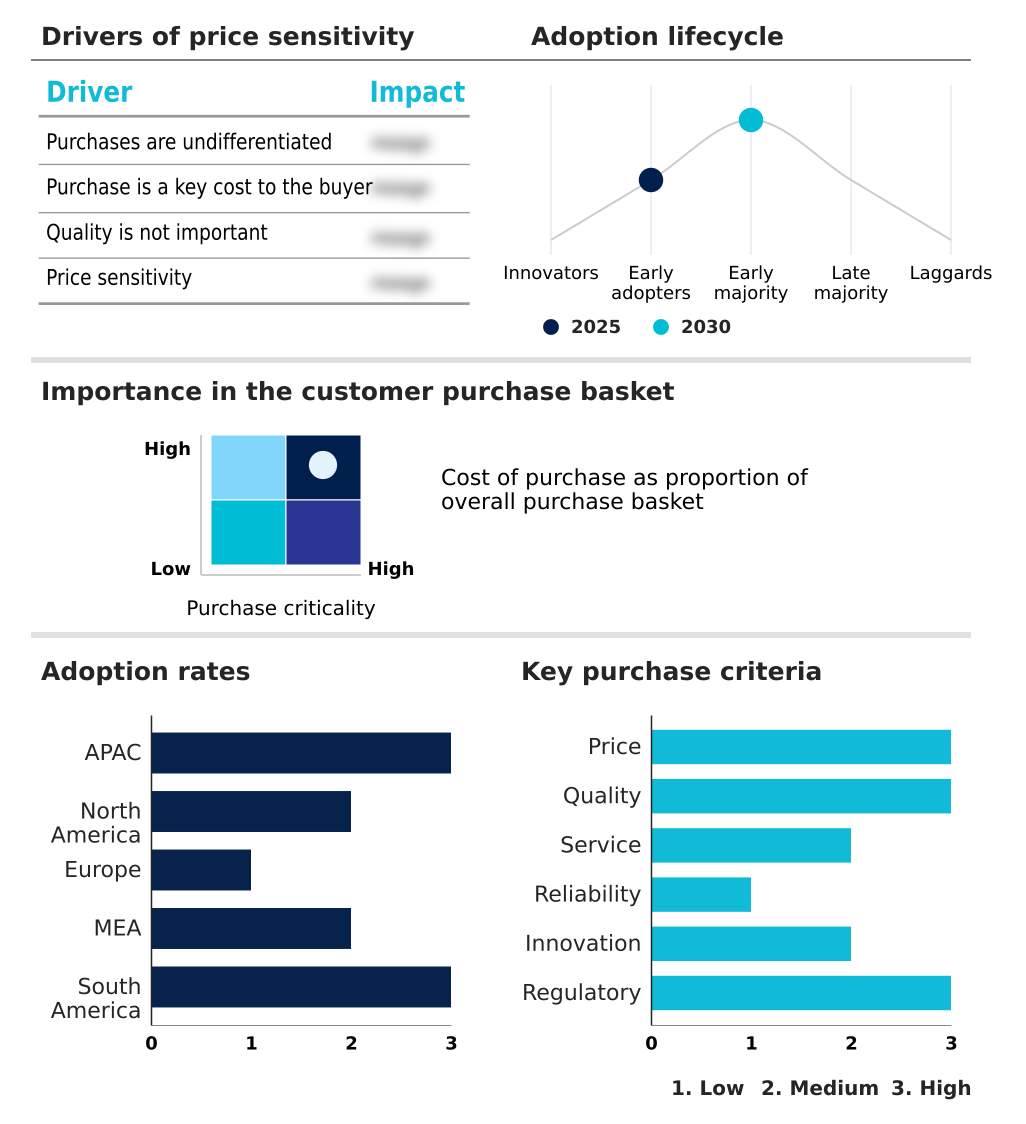

Exclusive Technavio Analysis on Customer Landscape

The mobile gaming market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the mobile gaming market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Mobile Gaming Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, mobile gaming market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

BANDAI NAMCO Europe S.A.S - Vendors provide a diverse portfolio, from casual puzzles to complex multiplayer experiences, leveraging mobile operating systems for broad distribution and engagement.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- BANDAI NAMCO Europe S.A.S

- Electronic Arts Inc.

- Epic Games Inc.

- King Digital Entertainment plc

- Konami Group Corp.

- Miniclip SA

- Moon Active Ltd.

- NetEase Inc.

- Netmarble Corp.

- NEXON Co. Ltd.

- Niantic Inc.

- Outfit7 Ltd.

- Playtika Holding Corp.

- Roblox Corp.

- Rovio Entertainment Corp.

- Scopely Inc.

- Supercell Oy

- Tencent Holdings Ltd.

- Voodoo SAS

- Zynga Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Mobile gaming market

- In April 2025, Roblox Corp. initiated a significant technological update by launching agentic artificial intelligence tools, including a novel Planning Mode and procedural mesh generation, which allow creators to transform single text prompts into editable, structured game development roadmaps.

- In April 2025, NetEase Inc. advanced its global reach by launching the competitive racing title Racing Master in Europe and North America, following a period of intensive regional localization and testing.

- In February 2025, Scopely Inc. solidified its position as a primary consolidator in the mobile sector by acquiring a majority stake in the Istanbul-based developer of a breakout puzzle title, in a transaction valuing the studio in excess of a billion dollars.

- In August 2024, Samsung Electronics initiated a comprehensive beta rollout of its mobile cloud gaming platform across the United Kingdom and Germany, allowing its device users to stream technically demanding titles without extensive local processing power.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Mobile Gaming Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 289 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 12.4% |

| Market growth 2026-2030 | USD 101469.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 10.6% |

| Key countries | China, Japan, India, South Korea, Indonesia, Australia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, South Africa, UAE, Turkey, Israel, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The mobile gaming market is characterized by a strategic fusion of advanced technologies. Cloud-native architectures and high-fidelity cloud streaming are enabling hardware-agnostic gaming, supported by the increasing power of high-performance mobile processors and diverse mobile operating systems. At the core of development, procedural generation tools and automated content pipelines are powered by agentic artificial intelligence and sophisticated cloud-native game development.

- This allows for generative AI narrative frameworks and real-time narrative adjustments, creating dynamic experiences. Monetization is evolving through direct-to-consumer monetization, hybrid-casual monetization, and complex in-game economies managed within a freemium monetization model. For live titles, live-ops optimization, robust anti-cheat systems, and constant data-driven personalization are key.

- Studios are leveraging user acquisition and retention modeling with algorithmic precision to combat high costs, especially as some face margin compression from increasing ad spend by over 20%. The focus is on seamless cross-platform interoperability, including cross-save and cross-play functionalities, within a unified social ecosystem integration. This necessitates low-latency network environments for real-time multiplayer performance.

- On the user end, features like on-device neural processing, server-side ray tracing, and engaging single-player narratives enhance the experience, while digital safety, screen time management, and cognitive stimulation become important considerations alongside the core gameplay offered via digital storefronts and cloud-based gaming services.

What are the Key Data Covered in this Mobile Gaming Market Research and Growth Report?

-

What is the expected growth of the Mobile Gaming Market between 2026 and 2030?

-

USD 101.47 billion, at a CAGR of 12.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Platform (Online, and Offline), Type (Casual gaming, and Professional gaming), End-user (Casual gamers, Mid-core gamers, Hardcore gamers, and Others) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Institutionalization of high-fidelity cloud streaming and hyper-connectivity, Heightened privacy regulations and erosion of targeted advertising

-

-

Who are the major players in the Mobile Gaming Market?

-

BANDAI NAMCO Europe S.A.S, Electronic Arts Inc., Epic Games Inc., King Digital Entertainment plc, Konami Group Corp., Miniclip SA, Moon Active Ltd., NetEase Inc., Netmarble Corp., NEXON Co. Ltd., Niantic Inc., Outfit7 Ltd., Playtika Holding Corp., Roblox Corp., Rovio Entertainment Corp., Scopely Inc., Supercell Oy, Tencent Holdings Ltd., Voodoo SAS and Zynga Inc.

-

Market Research Insights

- The market's dynamics are shaped by a strategic pivot from aggressive user acquisition to intensive monetization of existing player bases. This is evident in the rise of console-quality titles and high-LTV genres that leverage sophisticated live service operations.

- The effectiveness of this approach is quantifiable; studios using advanced analytics software for hyper-personalized content have achieved a 20% reduction in churn rates. Furthermore, the adoption of cloud-enabled architectures has reduced infrastructure latency by nearly 30%, which is crucial for the esports infrastructure.

- This focus on player retention and lifetime value, supported by the integration of digital wallets and transparent loot box disclosures within interconnected social experiences, is transforming the digital entertainment ecosystem. The shift supports a mobile-first consumer psychology, where players expect deep, persistent engagement.

We can help! Our analysts can customize this mobile gaming market research report to meet your requirements.

RIA -

RIA -