Gastrointestinal Stromal Tumors Therapeutics Market Size 2025-2029

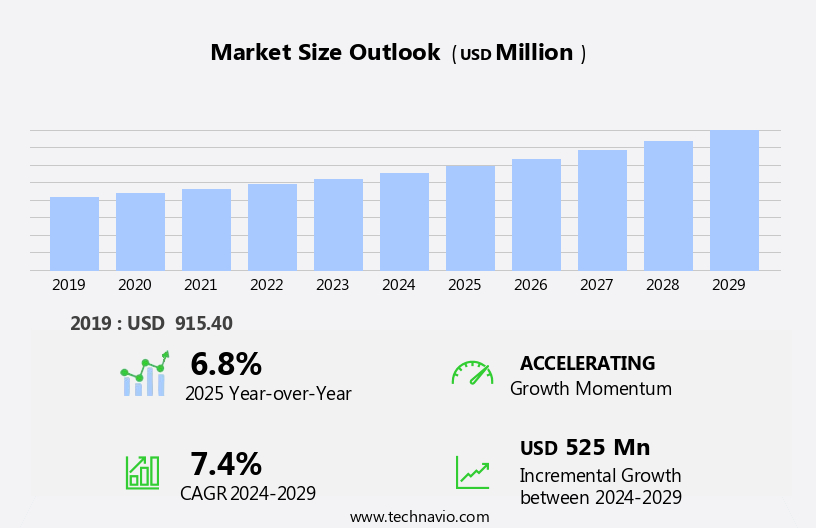

The gastrointestinal stromal tumors therapeutics market size is forecast to increase by USD 525 million at a CAGR of 7.4% between 2024 and 2029.

- The Gastrointestinal Stromal Tumors (GIST) Therapeutics Market is experiencing significant growth, driven by the increasing prevalence of the disease among the aging population. The geriatric demographic, which is more susceptible to GIST, is expanding globally, leading to a rise in demand for effective therapeutic solutions. Additionally, the advent of regenerative therapy for GIST presents an opportunity for market expansion. However, the high costs associated with these advanced therapies pose a challenge to market growth, particularly for those without adequate insurance coverage or financial resources.

- Strategic collaborations and partnerships, focusing on research and development, could further strengthen market positions and enable players to capitalize on the growing demand for GIST therapeutics. The integration of advanced technologies and cost-effective treatment strategies could potentially mitigate this obstacle and enhance market prospects for companies operating in this space. Medical devices and molecular diagnostics also contribute to improved patient care and treatment outcomes.

What will be the Size of the Gastrointestinal Stromal Tumors Therapeutics Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

- Gastrointestinal stromal tumors (GISTs), a rare subtype of sarcomas, pose significant challenges in diagnosis and treatment due to their complex molecular landscape. PDGFRA and KIT mutations are the most common drivers of GIST disease progression. Liquid biopsy, a non-invasive diagnostic approach, offers potential for early detection and monitoring of tumor mutations. Car T-cell therapy, a novel immunotherapeutic approach, targets tumor microenvironment and shows promise in overcoming drug resistance mechanisms. Healthcare costs, a critical market dynamic, are influenced by patient satisfaction, long-term follow-up, treatment adherence, and multidisciplinary care. Survival analysis using Kaplan-Meier curves provides valuable insights into patient outcomes.

- Molecular subtypes and family history play essential roles in prognosis and treatment decisions. Drug repurposing and genetic counseling are emerging trends in GIST therapeutics. Clinical trial design, patient-reported outcomes, insurance coverage, and randomized controlled trials are crucial factors shaping the market landscape. Tumor response and treatment adherence are key determinants of patient outcomes in the long run. Observational studies offer valuable real-world data to supplement clinical trial findings.

How is this Gastrointestinal Stromal Tumors Therapeutics Industry segmented?

The gastrointestinal stromal tumors therapeutics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Route Of Administration

- Oral

- Parenteral

- Distribution Channel

- Hospital pharmacies

- Retail pharmacies

- Online pharmacies

- Therapy

- Targeted therapy

- Chemotherapy

- Immunotherapy

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- Rest of World (ROW)

- North America

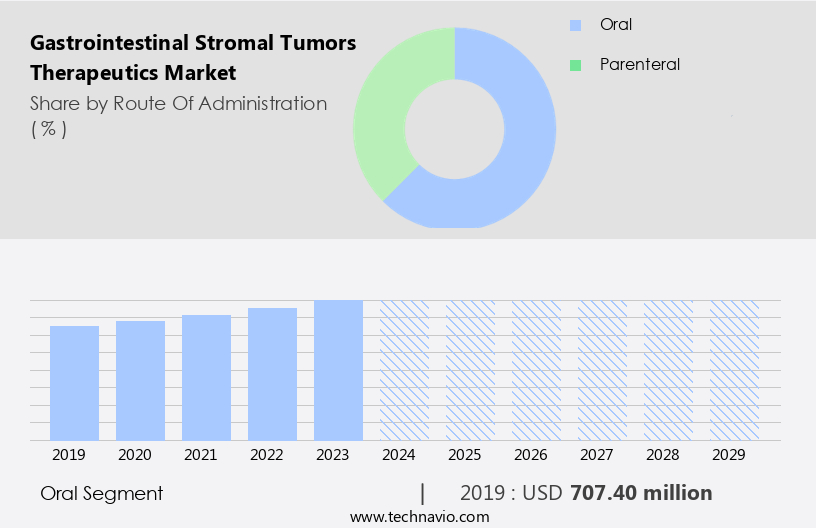

By Route Of Administration Insights

The oral segment is estimated to witness significant growth during the forecast period. Currently, the oral segment is dominating the global gastrointestinal stromal tumors therapeutics market, primarily due to the presence of large pharmaceutical companies such as Bayer, Novartis, and Pfizer with their specialty drugs for the treatment of the indication. Drugs such as STIVARGA by Bayer, GLEEVEC by Novartis, and SUTENT by Pfizer have gained popularity due to their ability to target multiple proteins in the body and inhibit the abnormal division of the cells in the body. For instance, GLEEVEC, the most popular drug for the treatment of gastrointestinal stromal tumors, has been designed to target multiple proteins such as c-kit and platelet-derived growth factor receptor alpha (PDGFRA).

The ease of administration is also increasing patient adherence to the treatment using these drugs, which will aid in the growth of the oral segment during the forecast period.However, the oral segment faces a heavy threat from the patent expiry of these major drugs. As these drugs have either lost most or all of the patents in the major markets, the oral segment is expected to witness a number of generic drugs entering the market. Despite the expected volume growth, the entry of generics is expected to cause value erosion owing to their low prices. This is expected to result in the oral segment losing some of its market share to the parenteral segment. However, the demand for these drugs is expected to remain higher than the generic drugs during the forecast period, which results in a partial offset of the damage caused by generics.

The parenteral route involves the administration of drugs into the body through subcutaneous, intravenous, and intramuscular routes. Currently, this segment has a few traditional chemotherapy drugs that are approved for the treatment of the indication. The share of the segment in the market remained very low for a long time due to the poor efficacy of traditional chemotherapies for the treatment of gastrointestinal stromal tumors. Patients do not always respond well to the treatment using chemotherapy, as it often fails to shrink the tumor completely. In some cases, the treatment using traditional chemotherapy drugs does not show any improvement in patients. As a result, traditional chemotherapy, which is often administered through the parenteral route, has remained a less preferred treatment option.

The Oral segment was valued at USD 707.40 million in 2019 and showed a gradual increase during the forecast period.

However, the market witnesses the presence of various companies that are developing novel drugs for administration through this route. Most of the drugs that are being developed in the late stages of the gastrointestinal stromal tumors pipeline are biologics. The parenteral route remains the most preferred route for biologics, as the administration through the oral route often results in the drug losing its efficacy. Various novel checkpoint inhibitors or targeted therapies, such as KEYTRUDA by Merck and OPDIVO by BMS, are being studied in the late stages of clinical trials for the treatment of this indication. For instance, KEYTRUDA is being studied in Phase III of clinical trials, while OPDIVO is being studied in Phase II of clinical trials for the treatment of gastrointestinal stromal tumors.

These drugs are expected to receive marketing approval during the forecast period and are expected to add significant value to the market growth owing to their high efficacy and demand. The popularity of these drugs for the treatment of various cancer indications has led them to receive blockbuster status, which is expected to attract a major share of patients to undergo treatment using these drugs during the forecast period. The pipeline for the indication also witnesses the presence of cancer vaccines in the early stages of clinical trials. For instance, Mendus is currently conducting studies on Intuvax, which is a novel cancer vaccine that is being studied in Phase I of clinical trials. The diagnostic process for GIST involves medical history, physical examination, and various tests such as CT scan, MRI, endoscopic ultrasonography, and biopsy, followed by immunohistochemistry and mitotic rate assessment.

Similarly, various other companies in the early stages of the pipeline are developing novel therapies that are administered through the parenteral route. Although these drugs are not expected to receive marketing approval from the US FDA and the EMA during the forecast period, these drugs are expected to add significant value to the growth of the parenteral segment. Owing to the advances in research and the expected launch of novel drugs during the forecast period, the parenteral segment is expected to witness an accelerating growth momentum and become the fastest-growing segment of the global gastrointestinal stromal tumors therapeutics market during the forecast period.

Regional Analysis

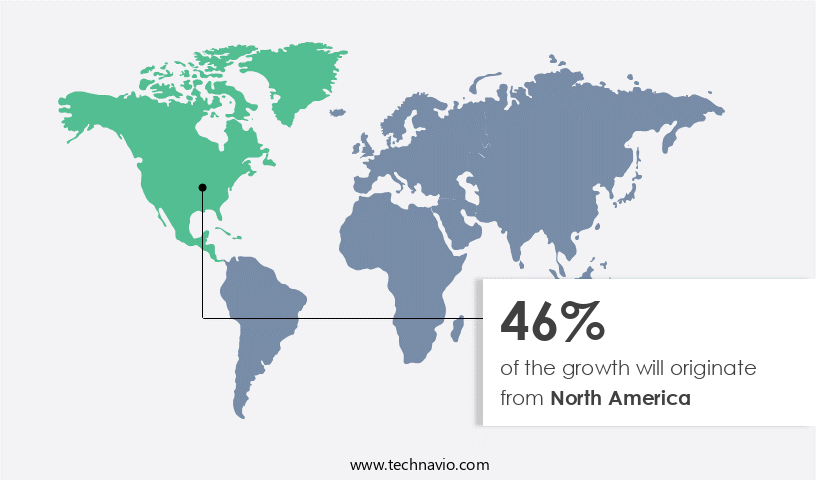

North America is estimated to contribute 46% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

In the US, the gastrointestinal stromal tumors (GIST) therapeutics market is experiencing growth due to the large pharmaceutical market in North America. While surgery remains a prominent treatment option, there has been a rising adoption of therapeutics for managing GIST. Despite the approaching patent expiry of drugs like GLEEVEC, STIVARGA, and SUTENT, the market demand for these medications has remained relatively stable. Several companies are introducing generic versions of these drugs in the region. Patient advocacy groups and increased disease awareness have led to a greater focus on improving patient management and clinical outcomes. End-of-life care and palliative care are essential components of GIST treatment, with a growing emphasis on value-based healthcare.

Drug development in the GIST therapeutics market is ongoing, with a focus on precision oncology, targeted therapies, and combination therapies. Tyrosine kinase inhibitors, such as imatinib mesylate and sunitinib malate, continue to be key players in the market. Research funding, including foundation grants and government grants, is crucial for advancing the understanding of GIST and developing new treatments. Adverse events and drug interactions are significant concerns, necessitating rigorous clinical trials and patient education. Synergistic effects of combination therapies and radiation therapy are being explored to enhance treatment efficacy. Hospice care and pain management are essential aspects of GIST treatment, particularly during the end stages of the disease.

The market is expected to continue evolving, with a focus on personalized medicine and combination therapies to improve patient outcomes.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Gastrointestinal Stromal Tumors Therapeutics market drivers leading to the rise in the adoption of Industry?

- The geriatric population's expansion is the primary factor fueling market growth. The Gastrointestinal Stromal Tumors (GIST) therapeutics market is witnessing significant growth due to the increasing prevalence of the disease among the aging population. With the global geriatric population projected to reach 802 million by 2023, according to UN World Population Prospects, the market is expected to expand. The advances in healthcare infrastructure and the availability of various treatment options for indications like cancer have led to improved survival rates. Furthermore, disease awareness campaigns and patient advocacy initiatives have contributed to earlier diagnosis and better patient management. The European Medicines Agency (EMA) and the US Food and Drug Administration (FDA) have approved several therapeutic options for GIST, including imatinib mesylate.

- Imatinib mesylate is a tyrosine kinase inhibitor that targets the KIT and PDGFRA proteins, which are overexpressed in GIST. Its mechanism of action inhibits the proliferation and survival of tumor cells, leading to improved clinical outcomes. However, patient management for GIST involves careful monitoring for drug interactions and potential side effects. Palliative care is essential for managing symptoms and improving the quality of life for patients with advanced or metastatic GIST. Health economics plays a crucial role in determining the affordability and accessibility of these treatments, making it essential to understand the clinical outcomes and cost-effectiveness of various therapeutic options.

What are the Gastrointestinal Stromal Tumors Therapeutics market trends shaping the Industry?

- Regenerative therapies for GIST (Gastrointestinal Stromal Tumors) are gaining significant attention in the medical community as the next market trend. The advent of these innovative treatments offers new hope for patients with this type of cancer. The gastrointestinal stromal tumors (GIST) therapeutics market faces a significant challenge due to the disease's recurrent nature. Surgical procedures only remove a portion of the tumor, necessitating the use of adjuvant therapies. Even after complete tumor removal, the disease can recur. To address this issue, targeted therapies, including molecular-targeted agents like sunitinib malate, are being developed.

- Adverse events, including nausea and vomiting, are common with current treatment regimens, emphasizing the need for value-based healthcare. The drug approval process is rigorous, involving extensive clinical trials and regulatory oversight. Biotech companies play a crucial role in advancing research and innovation. Overall survival and progression-free survival rates are essential measures of treatment efficacy. The market is witnessing significant growth with the integration of gene therapy and biotech advancements, offering innovative treatments that target the genetic mutations associated with these tumors and improving patient outcomes.

How does Gastrointestinal Stromal Tumors Therapeutics market faces challenges face during its growth?

- The escalating treatment costs for GIST (Gastrointestinal Stromal Tumors) pose a significant challenge and hinder the growth of the healthcare industry. The gastrointestinal stromal tumors (GIST) therapeutics market primarily consists of specialized drugs, such as GLEEVEC, STIVARGA, and SUTENT, accounting for approximately 70% of the market revenue. These drugs, which include tyrosine kinase inhibitors, offer precision oncology treatments that target multiple proteins, justifying their high price points. For instance, the annual cost of GLEEVEC treatment ranges from USD 110,000 to USD 120,000, while STIVARGA's yearly cost falls between USD 30,000 and USD 50,000.

- Furthermore, public awareness campaigns, genetic testing, and foundation grants are essential for improving patient education and access to these life-saving treatments. The GIST therapeutics market's growth is influenced by the need for innovative treatments, clinical advancements, and patient access initiatives. However, these exorbitant costs limit access for patients without health insurance or financial assistance, leading to decreased adherence and market growth challenges. To expand market reach, drug development companies are focusing on clinical trials, particularly in Phase II, to explore synergistic effects of combination therapies and radiation therapy.

Exclusive Customer Landscape

The gastrointestinal stromal tumors therapeutics market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the gastrointestinal stromal tumors therapeutics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, gastrointestinal stromal tumors therapeutics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AB Science SA - The company specializes in the development of gastrointestinal stromal tumors (GIST) therapeutics, featuring masitinib as a prominent solution.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AB Science SA

- AROG Pharmaceuticals Inc.

- Ascentage Pharma Group International

- Bayer AG

- Blueprint Medicines Corp.

- Bristol Myers Squibb Co.

- Daiichi Sankyo Co. Ltd.

- Deciphera Pharmaceuticals Inc.

- Ipsen Pharma

- Mendus AB

- Merck KGaA

- Novartis AG

- Pfizer Inc.

- Sun Pharmaceutical Industries Ltd.

- Takeda Pharmaceutical Co. Ltd.

- Xencor Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Gastrointestinal Stromal Tumors Therapeutics Market

- In February 2023, Pfizer Inc. Announced the U.S. Food and Drug Administration (FDA) approval of its novel targeted therapy, Axitinib, in combination with sunitinib, for the treatment of adult patients with metastatic or unresectable gastrointestinal stromal tumors (GIST) who have already tried prior therapy (Pfizer press release, 2023). This dual-tyrosine kinase inhibitor therapy aims to improve progression-free survival in patients.

- In March 2024, Merck KGaA and Pfizer entered into a strategic collaboration to co-develop and commercialize a potential new treatment for GIST, MK-8628, a potent and selective inhibitor of KIT and PDGFRA mutations (Merck KGaA press release, 2024). This partnership combines Merck KGaA's expertise in oncology and Pfizer's global reach to bring this innovative therapy to patients.

- In May 2024, Blueprint Medicines Corporation received FDA approval for its targeted therapy, Ayvakit (palladitaxel), for the treatment of adult patients with advanced systemic mastocytosis, including mast cell leukemia and aggressive systemic mastocytosis, as well as advanced or metastatic, unresectable, or recurrent GIST (Blueprint Medicines press release, 2024). This approval marks the first FDA approval for a treatment specifically designed to target the KIT D816V mutation in GIST.

Research Analyst Overview

The gastrointestinal stromal tumors (GIST) therapeutics market continues to evolve as new treatments and technologies emerge, addressing the complexities of managing this rare and often challenging disease. The ongoing unfolding of market activities is driven by a range of factors, including advancements in our understanding of the disease mechanism, the development of new therapeutic approaches, and the evolving landscape of healthcare delivery and reimbursement. Five-year survival rates for GIST patients have improved significantly in recent years, thanks to the availability of targeted therapies such as imatinib mesylate and sunitinib malate. However, these treatments come with their own challenges, including nausea and vomiting, adverse events, and the need for ongoing monitoring and management.

Research funding plays a critical role in advancing our understanding of GIST and developing new treatments. Biotech companies are at the forefront of this research, leveraging precision oncology and molecular diagnostics to develop targeted therapies and personalized treatment regimens. Value-based healthcare is also influencing the GIST therapeutics market, with a growing focus on clinical outcomes, patient education, and symptom management. Drug development is a complex and lengthy process, with various phases of clinical trials and regulatory approvals required before a new treatment can reach patients. The drug approval process involves close collaboration between regulatory agencies, such as the European Medicines Agency (EMA) and the US Food and Drug Administration (FDA), and biotech companies.

Adverse events and drug interactions are closely monitored throughout the approval process to ensure patient safety. Medical devices and molecular diagnostics are also playing an increasingly important role in GIST management, from surgical interventions and pain management to disease burden assessment and targeted therapy resistance monitoring. The ongoing evolution of the GIST therapeutics market is shaped by a range of factors, from disease awareness and public education to synergistic effects of combination therapies and the role of checkpoint inhibitors in targeted therapy resistance. The market is expected to continue unfolding in the coming years, with a focus on improving patient outcomes, reducing disease burden, and enhancing quality of life for GIST patients. Additionally, research is ongoing for regenerative therapies, such as gene therapy, to ensure complete tumor remission. Genetic research reveals various genes linked to GIST progression.

The Gastrointestinal Stromal Tumors (GIST) Therapeutics Market is advancing with rigorous Phase I trials, evaluating safety and dosage parameters for novel treatments. Successful candidates progress to Phase II trials, where efficacy and side effects are assessed in a larger patient group. Later-stage Phase III trials focus on confirming effectiveness across diverse populations, ensuring robust clinical validation before regulatory submission. Achieving EMA approval is a crucial milestone, facilitating wider access to innovative therapies in Europe. Optimized treatment regimens are key to improving patient outcomes, integrating targeted therapies, immunotherapy, and precision medicine approaches.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Gastrointestinal Stromal Tumors Therapeutics Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

214 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.4% |

|

Market growth 2025-2029 |

USD 525 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

6.8 |

|

Key countries |

US, Germany, China, Canada, France, Japan, UK, Italy, India, and Mexico |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Gastrointestinal Stromal Tumors Therapeutics Market Research and Growth Report?

- CAGR of the Gastrointestinal Stromal Tumors Therapeutics industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the gastrointestinal stromal tumors therapeutics market growth of industry companies

We can help! Our analysts can customize this gastrointestinal stromal tumors therapeutics market research report to meet your requirements.

RIA -

RIA -