High Purity Alumina Market Size 2026-2030

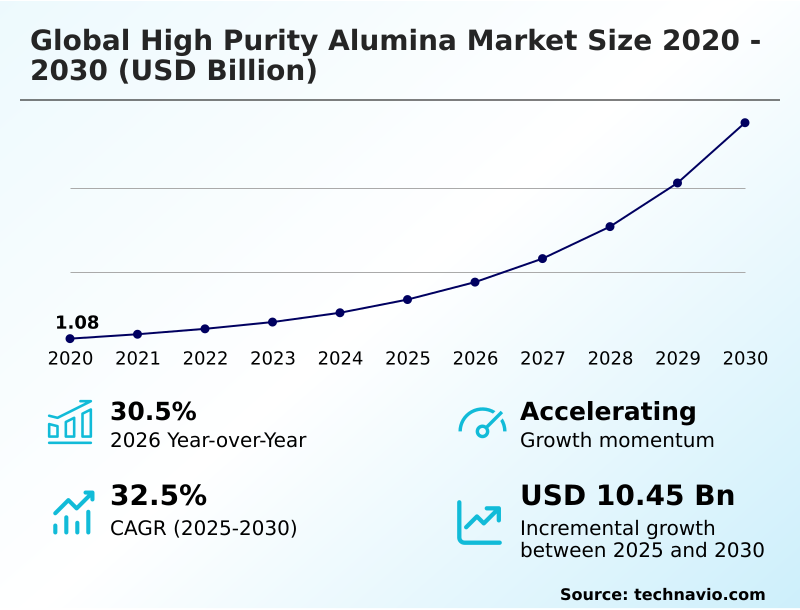

The high purity alumina market size is valued to increase by USD 10.45 billion, at a CAGR of 32.5% from 2025 to 2030. Rising integration within lithium-ion battery supply chain will drive the high purity alumina market.

Major Market Trends & Insights

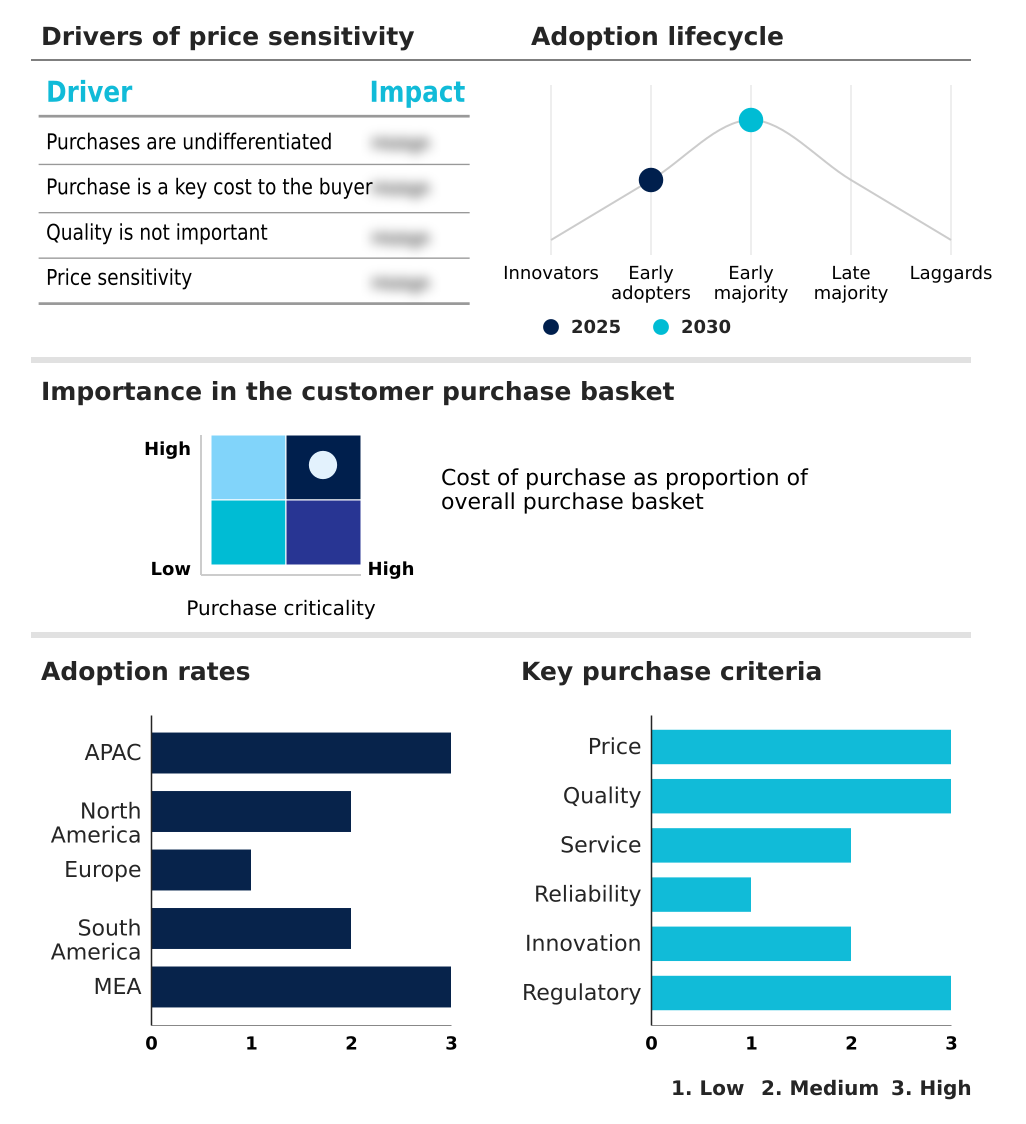

- APAC dominated the market and accounted for a 72.5% growth during the forecast period.

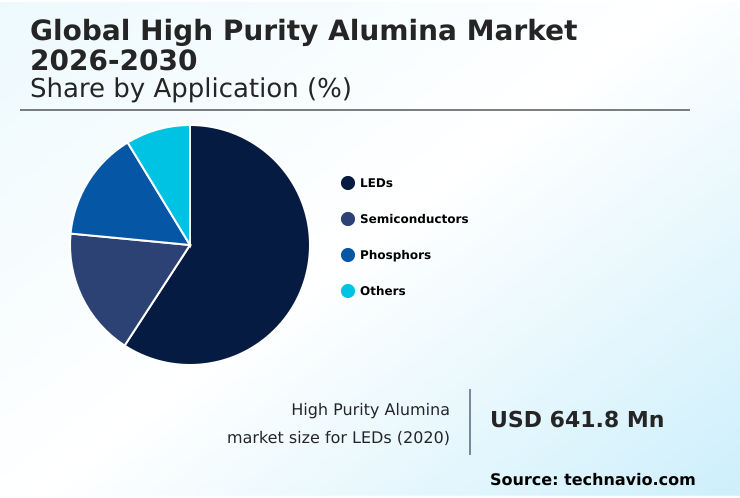

- By Application - LEDs segment was valued at USD 1.56 billion in 2024

- By Type - 4N HPA segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 12.76 billion

- Market Future Opportunities: USD 10.45 billion

- CAGR from 2025 to 2030 : 32.5%

Market Summary

- The high purity alumina market is defined by its critical role in high-technology sectors. Demand is propelled by its use as a coating for the lithium-ion battery separator to ensure thermal runaway prevention in electric vehicles, as a light emitting diode substrate for energy-efficient lighting, and in semiconductor processing components that withstand corrosive environments.

- A significant trend reshaping the industry is the pivot toward sustainable production methods, with producers exploring kaolin clay feedstock and innovative refining to reduce carbon footprints. However, achieving ultra-high purity alumina specifications involves substantial capital investment and high operational costs, a persistent challenge for market participants.

- For a manufacturer of advanced microchips, this presents a strategic dilemma: investing in higher-cost, five-nines pure alumina for chemical mechanical planarization slurries could improve wafer yields by a few percentage points, justifying the expense, whereas a lower-grade material risks costly defects in advanced nodes.

- This trade-off between performance, cost, and supply chain resilience, amid a push for supply chain regionalization, dictates strategic planning and investment decisions across the ecosystem, highlighting the balance required for operational expenditure reduction.

What will be the Size of the High Purity Alumina Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the High Purity Alumina Market Segmented?

The high purity alumina industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

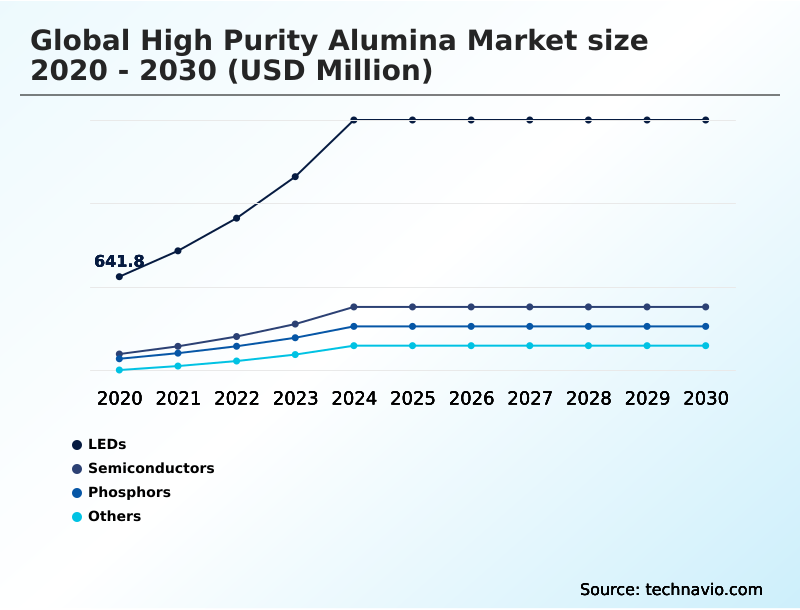

- LEDs

- Semiconductors

- Phosphors

- Others

- Type

- 4N HPA

- 5N HPA

- 6N HPA

- Technology

- Hydrolysis

- Hydrochloric acid leaching

- Others

- Geography

- APAC

- China

- South Korea

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Application Insights

The leds segment is estimated to witness significant growth during the forecast period.

The light emitting diode segment is a foundational application area, where high purity alumina serves as the primary precursor for producing synthetic sapphire substrates. This is achieved via high-temperature processes like the verneuil method or czochralski method.

The transition toward energy-efficient lighting and high-performance displays drives demand for this light emitting diode substrate. As consumer electronics evolve with micro-led display technology and the need for high-brightness leds, the requirement for pristine material for sapphire ingot growth intensifies.

The material's optical transparency and thermal stability are critical, with material customization enabling performance in advanced applications like high-frequency 5g infrastructure.

This demand for high-performance optical components has pushed the industry toward a specialty chemicals model where purity directly improves manufacturing yields, reducing downstream defects by over 20%.

The LEDs segment was valued at USD 1.56 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 72.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How High Purity Alumina Market Demand is Rising in APAC Get Free Sample

The APAC region dominates the geographic landscape, driven by its massive electronics and battery manufacturing sectors. Countries like China, Japan, and South Korea are epicenters for producing the ceramic separator coating essential for lithium-ion batteries.

This region accounts for over 72% of the market's incremental growth, reflecting its central role in the critical mineral supply chain. China's market is more than three times larger than Taiwan's, showcasing its scale.

The regional industry is addressing geopolitical supply risk by investing in local refining capabilities for materials used in applications from bioceramic medical implants to extreme ultraviolet lithography equipment, aligning with industrial electrification goals.

This concentration underscores APAC's influence on global supply and demand dynamics.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The market is evolving as demand for high purity alumina for leds continues to grow, driven by energy efficiency mandates. The material's role is also central to hpa in lithium-ion batteries, where hpa coated battery separators are standard for safety, directly addressing hpa's role in thermal runaway prevention.

- For next-generation power, hpa in solid state batteries is a key research area. The electronics industry relies on semiconductor grade alumina powder, especially low soda alumina for electronics, and uses nano alumina for cmp slurries to achieve perfect wafer finishes. The quest for higher purity is met with materials like 5n alumina for plasma etching components.

- Producers are innovating with sustainable hpa production methods, including the hydrochloric acid leaching process hpa which uses high purity alumina from kaolin. The industry is exploring high purity alumina recycling technologies to create a circular economy. The cost of 4n high purity alumina remains a key consideration for mass-market applications, while demand for synthetic sapphire crystal growth precursors is unwavering.

- The diverse high purity alumina market applications extend to biocompatible alumina for medical implants, transparent ceramics from high purity alumina for defense, and using spherical alumina for thermal management in electronics.

- This complexity requires careful analysis; for instance, adopting the hydrochloric acid leaching process hpa can lower carbon emissions by over 50% compared to traditional smelting routes, a crucial metric for compliance and supply chain planning. Finally, the use of HPA as doping agents for phosphors hpa highlights its versatility.

What are the key market drivers leading to the rise in the adoption of High Purity Alumina Industry?

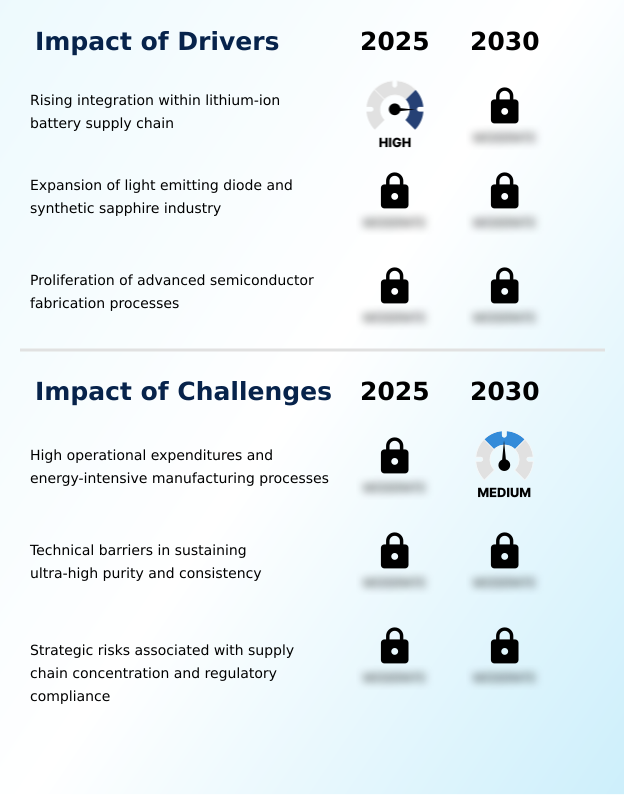

- The rising integration of high purity alumina within the lithium-ion battery supply chain, driven by the needs of the electric vehicle market, serves as a primary driver for industry growth.

- Market expansion is fundamentally driven by the material’s critical role in the green and digital transitions.

- The proliferation of high-energy-density cells for electric vehicle battery safety relies on ceramic separator coating for the lithium-ion battery separator, which offers thermal runaway prevention by enhancing thermal stability by over 30%. This aligns with global industrial electrification goals.

- Concurrently, the demand for light emitting diode substrate materials for high-brightness leds is unwavering.

- In the semiconductor sector, the move to advanced process nodes requires plasma-resistant ceramics for semiconductor processing components, where ultra-pure materials are credited with improving high-yield semiconductor fabrication by reducing defect-related failures by up to 25%.

What are the market trends shaping the High Purity Alumina Industry?

- The market is undergoing a strategic shift toward sustainable and low-carbon production methodologies. This transition is guided by environmental mandates and evolving supply chain priorities across global technology sectors.

- A primary trend is the strategic shift toward sustainable and low-carbon production of specialty alumina chemicals, utilizing feedstocks like aluminous chemical byproducts instead of energy-intensive primary aluminum. These innovative refining pathways can reduce electricity consumption by up to 70% compared to legacy methods. Simultaneously, demand for specialized particle characteristics is reshaping the industry.

- Advanced ceramic materials with controlled morphology, such as spherical particles, improve packing density by over 15% in coatings. This raw material diversification and focus on inorganic material science extends to nano-structuring for applications from bioceramic medical implants to quantum computing components and improving wafer surface planarity in chemical mechanical planarization.

What challenges does the High Purity Alumina Industry face during its growth?

- High operational expenditures coupled with energy-intensive manufacturing processes represent a key challenge that affects the industry's growth and profitability.

- Key challenges temper market growth, led by high operational expenditures and technical complexity. The processes for achieving ultra-high purity alumina, such as hydrochloric acid leaching or solvent extraction purification, are capital-intensive, with energy costs often representing over 40% of the total production outlay, complicating operational expenditure reduction goals.

- Maintaining purity is a technical hurdle; trace impurity contamination at the parts-per-billion level can cause catastrophic device failure, reducing yields by more than 50% in sensitive applications.

- Furthermore, the critical mineral supply chain faces geopolitical supply risk, with a significant portion of refining capacity concentrated in a few regions, which complicates efforts toward supply chain regionalization and ensuring stable supply lines.

Exclusive Technavio Analysis on Customer Landscape

The high purity alumina market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the high purity alumina market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of High Purity Alumina Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, high purity alumina market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AEM High Purity Alumina - Specializes in producing ultra-high purity alumina grades tailored for critical, high-performance technological applications demanding stringent material specifications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AEM High Purity Alumina

- ALB Materials Inc.

- Alcoa Corp.

- American Elements

- Baikowski SA

- Cabot Corp.

- Compagnie de Saint Gobain SA

- Denka Co. Ltd.

- Evonik Industries AG

- Inframat Corp.

- Merck KGaA

- Nippon Light Metal Holdings

- Polar Sapphire Ltd.

- Resonac Holdings Corp.

- Sasol Ltd.

- Stanford Advanced Materials

- Sumitomo Chemical Co. Ltd.

- Taimei Chemicals Co. Ltd.

- Thermo Fisher Scientific Inc.

- Zibo Honghe Chemical Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in High purity alumina market

- In April, 2025, Alpha HPA finalized a long-term supply agreement with a major European electric vehicle battery manufacturer, securing the provision of high purity alumina for critical separator coating applications.

- In August, 2025, Altech Batteries Limited announced the successful construction of its pilot plant in Saxony, Germany, a facility designed to produce high purity alumina-coated silicon anodes to support the European automotive sector.

- In September, 2025, Alpha HPA achieved the successful commencement of the first commercial-scale production cycle at its newly expanded high purity alumina refinery in Queensland, Australia, mitigating risks associated with supply chain concentration.

- In September, 2025, Nippon Light Metal Holdings Company Limited introduced a refined purification sequence at its research center, aiming to reduce the environmental impact of aluminum hydrate processing and enhance production sustainability.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled High Purity Alumina Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 308 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 32.5% |

| Market growth 2026-2030 | USD 10452.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 30.5% |

| Key countries | China, Taiwan, South Korea, Japan, India, Australia, US, Canada, Mexico, Germany, France, UK, The Netherlands, Italy, Spain, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Egypt and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market for ultra-high purity alumina is defined by its critical role in advanced manufacturing, where materials like 4n high purity alumina and 5n high purity alumina are essential.

- Its applications span from being a light emitting diode substrate made from synthetic sapphire substrate grown via the verneuil method or czochralski method, to being a key part of the lithium-ion battery separator. The use of a ceramic separator coating offers thermal runaway prevention, a non-negotiable for modern batteries, including future solid-state battery electrolyte designs.

- In electronics, semiconductor processing components and plasma-resistant ceramics rely on its purity, especially for extreme ultraviolet lithography and micro-led display technology. For a boardroom deliberating on capital expenditure, the decision to invest in low-carbon alumina production using hydrochloric acid leaching of kaolin clay feedstock over traditional bayer process refinement or aluminum alkoxide hydrolysis is now a strategic imperative.

- This shift, driven by ESG targets, can reduce energy consumption by over 40%, securing a competitive advantage despite initial costs. The material's versatility is seen in chemical mechanical planarization slurries, phosphor host lattice structures, and even bioceramic medical implants, showcasing inorganic material science innovation with specialty alumina chemicals and advanced ceramic materials.

- Producers are now focused on particle morphology control to create spherical alumina particles and nano-structured alumina powder from feedstocks like aluminous chemical byproducts, expanding the use of transparent alumina ceramic and high-k dielectric material, while managing the critical mineral supply chain.

- The precision needed for sapphire ingot growth and creating sub-micron alumina particles through methods like solvent extraction purification underscores the market's technical complexity.

What are the Key Data Covered in this High Purity Alumina Market Research and Growth Report?

-

What is the expected growth of the High Purity Alumina Market between 2026 and 2030?

-

USD 10.45 billion, at a CAGR of 32.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (LEDs, Semiconductors, Phosphors, and Others), Type (4N HPA, 5N HPA, and 6N HPA), Technology (Hydrolysis, Hydrochloric acid leaching, and Others) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rising integration within lithium-ion battery supply chain, High operational expenditures and energy-intensive manufacturing processes

-

-

Who are the major players in the High Purity Alumina Market?

-

AEM High Purity Alumina, ALB Materials Inc., Alcoa Corp., American Elements, Baikowski SA, Cabot Corp., Compagnie de Saint Gobain SA, Denka Co. Ltd., Evonik Industries AG, Inframat Corp., Merck KGaA, Nippon Light Metal Holdings, Polar Sapphire Ltd., Resonac Holdings Corp., Sasol Ltd., Stanford Advanced Materials, Sumitomo Chemical Co. Ltd., Taimei Chemicals Co. Ltd., Thermo Fisher Scientific Inc. and Zibo Honghe Chemical Co. Ltd.

-

Market Research Insights

- The market's dynamic nature is shaped by the rigorous demands of high-tech industries. A focus on electric vehicle battery safety has made high purity alumina coatings essential, achieving over a 95% reduction in separator shrinkage during thermal stress tests. This thermal stability enhancement is paramount.

- In parallel, the push toward advanced process nodes in semiconductor manufacturing necessitates ultra-pure materials to support high-yield semiconductor fabrication, with some processes showing a 15% decrease in wafer defects. These technical demands are set against a backdrop of strategic supply chain regionalization and raw material diversification to mitigate geopolitical risks and ensure stable supply for critical end-users.

We can help! Our analysts can customize this high purity alumina market research report to meet your requirements.

RIA -

RIA -