In Building Wireless Market Size 2024-2028

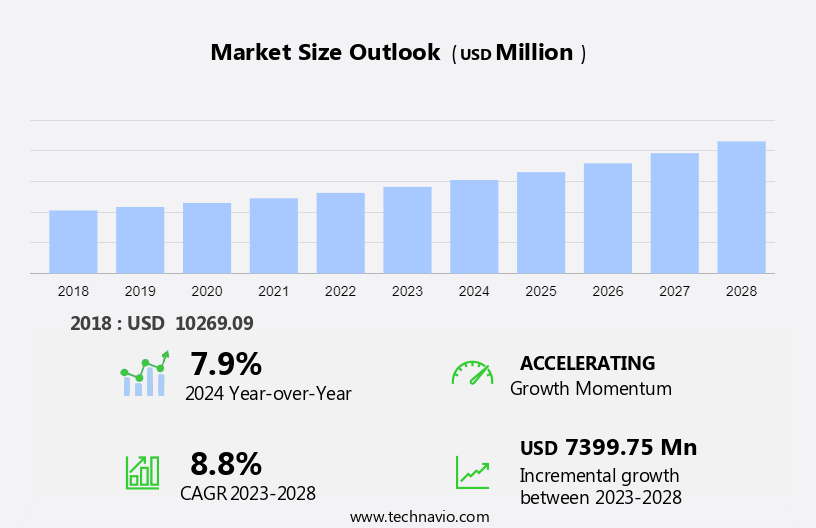

The in building wireless market size is forecast to increase by USD 7.40 billion at a CAGR of 8.8% between 2023 and 2028. The in-building wireless market is experiencing significant growth in the US, driven by the increasing demand for LTE/5G wireless connectivity in smart cities and the proliferation of intelligent and smart devices used by smartphone users. The number of mobile internet users and smartphone subscriptions continues to rise, leading to a growth in demand for reliable in-building wireless coverage. However, this growth comes with challenges, including the threat of cyberattacks targeting RAN users and the need to upgrade infrastructure components, such as base stations, to support the demands of 5G networks. Similarly, the in-building wireless market is witnessing the expansion of radio spectrum to accommodate the growing demand for wireless connectivity. IoT-focused Wi-Fi standards, such as 802.11ax, are being adopted to improve network performance and capacity. In conclusion, the in-building wireless market is an essential component of the digital transformation landscape. Companies like ExteNet Systems are at the forefront of addressing these challenges, providing innovative solutions to ensure seamless and secure wireless connectivity in various industries and commercial properties, including MGM properties and other high-traffic venues. The intelligent integration of these in-building wireless systems is crucial to support the increasing number of connected devices and ensure optimal network performance.

What will be the Size of the Market During the Forecast Period?

In-building wireless connectivity has emerged as a crucial element in the digital transformation of businesses and public institutions. As the reliance on mobile devices and smart technologies continues to grow, ensuring reliable network coverage within buildings is no longer an option but a necessity. Network coverage is essential for various mission-critical applications, including public safety measures, business assurance, and smart devices. With the increasing popularity of mobile internet and smartphone subscriptions, in-building wireless solutions have become indispensable. The digital change has led to a wave in the number of intelligent devices and smartphone users, resulting in a higher demand for in-building wireless connectivity.

In response, the market for in-building wireless solutions has witnessed significant growth. 5G network is poised to revolutionize the in-building wireless market by offering faster data transfer rates, lower latency, and higher bandwidth. This technology will enable seamless connectivity for a multitude of devices and applications, enhancing productivity and efficiency. However, with the increasing adoption of in-building wireless solutions comes the risk of cyberattacks. Ensuring the security of these networks is vital to protect sensitive data and maintain business continuity. The infrastructure components of in-building wireless systems include Wi-Fi, Bluetooth, Zigbee, LPWANs, and cellular networks. Cloud-managed Wi-Fi and RFID are also gaining popularity due to their ease of deployment and management. Providing reliable and secure wireless connectivity is crucial for businesses and institutions to remain competitive and efficient. As the number of connected devices continues to grow, the demand for in-building wireless solutions will only increase.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Government

- Manufacturing

- Transportation and logistics

- Education

- Retail and others

- Type

- Infrastructure

- Services

- Geography

- North America

- US

- APAC

- China

- Japan

- South Korea

- Europe

- UK

- South America

- Middle East and Africa

- North America

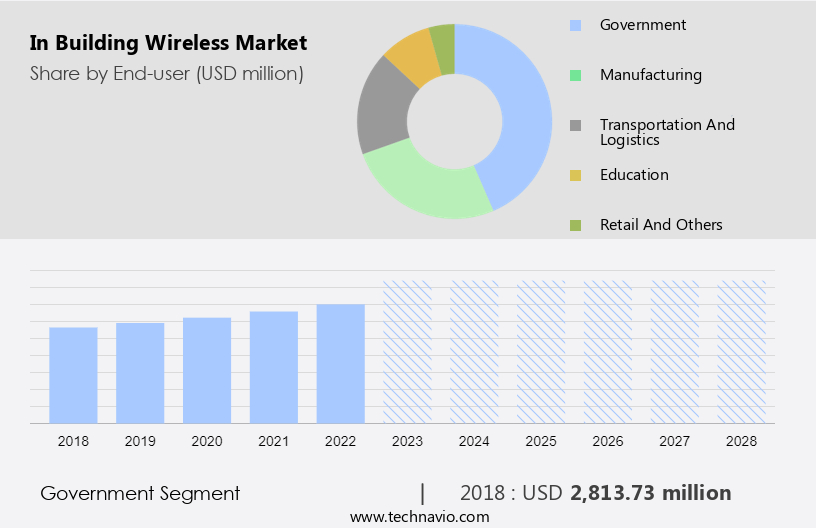

By End-user Insights

The government segment is estimated to witness significant growth during the forecast period. The market is experiencing significant growth, particularly within the government sector. Governments worldwide are investing in small cell infrastructure, including picocells, to improve cellular connectivity for all devices inside buildings. companies in this market catering to the government segment offer specialized in-building wireless solutions. These solutions are designed for various government entities such as local municipalities, cities, counties, state, and federal agencies. In-building wireless systems are deployed to boost indoor radio frequency and cellular signals in large government structures and sprawling campus environments. Public safety solutions are a growing focus, and there is an increasing emphasis on adhering to building codes and fire safety protocols.

Similarly, the National Fire Protection Agency (NFPA) and the International Fire Code (IFC) set strict requirements for emergency communication signal strength, coverage, and capacity. These regulations ensure effective communication during emergencies. Telecom equipment producers are developing Wi-Fi solutions, LPWANs, and IoT-focused Wi-Fi standards, such as Bluetooth, Zigbee, and Wi-Fi, to cater to the unique needs of the government sector. Cloud-managed Wi-Fi is also gaining popularity due to its ease of management and scalability. The government sector's demand for reliable, high-speed data throughput and secure communication networks is driving the growth of the in-building wireless market.

Get a glance at the market share of various segments Request Free Sample

The government segment was valued at USD 2.81 billion in 2018 and showed a gradual increase during the forecast period.

Regional Insights

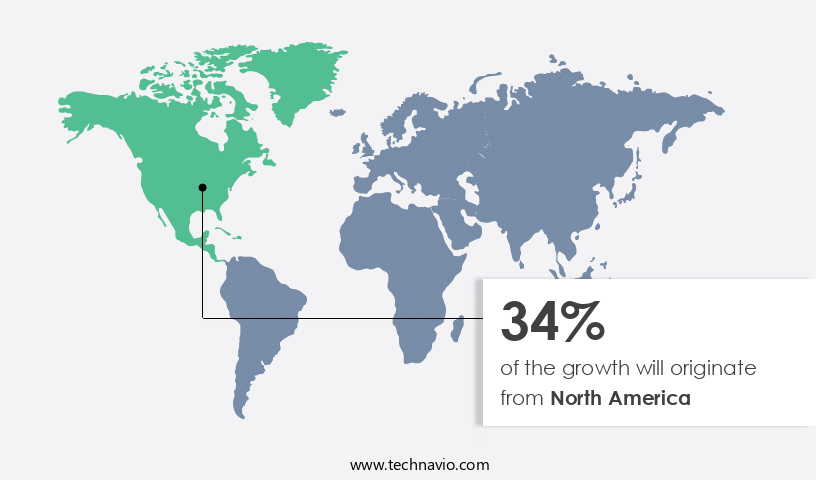

North America is estimated to contribute 34% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The proliferation of Internet-connected devices and the adoption of automation technologies are fueling the expansion of the in-building wireless market in the US. With the increasing number of smart homes and smart city initiatives, there is a growing need for reliable in-building connectivity, particularly in areas where cellular connectivity may be weak or nonexistent. These advanced technologies not only enhance network coverage but also support mission-critical applications and public safety measures, making them indispensable in various industries, including healthcare, education, and manufacturing. In summary, the US in-building wireless market is poised for significant growth due to the digital transformation, increasing investment in 5G, and the need for reliable in-building connectivity.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

An increase in demand for in building wireless due to growth of smart cities is the key driver of the market. In the realm of modern urban development, the concept of smart cities has gained significant traction. A smart city is an initiative to integrate various information and communication technologies into a city's infrastructure. This includes local government departments, educational institutions, transportation systems, power plants, water supply networks, and waste management facilities. The integration of these systems leads to enhanced connectivity and improved efficiency. One essential aspect of a smart city is the availability of reliable wireless coverage, particularly inside buildings. This need is met through the implementation of MulteFire bands, which provide cellular coverage within buildings, ensuring a seamless wireless experience for occupants.

Similarly, these inside-building projects require network management and the installation of third-party networking infrastructure, which may involve obtaining building permits. The adoption of in-building wireless solutions is not limited to new residential construction but extends to existing real estate assets, such as multi-tenant housing and residential communities. The integration of these technologies enhances the value of these properties by providing tenants with superior connectivity. In conclusion, the development of smart cities is a priority for many countries, and the integration of in-building wireless solutions is a crucial component. The use of MulteFire bands and third-party networking infrastructure enables reliable cellular coverage, enhancing the overall wireless experience for occupants of various facilities. This investment not only improves the functionality of buildings but also adds value to real estate assets.

Market Trends

Rising adoption of BYOD in enterprise is the upcoming trend in the market. The in-building wireless market in the US is poised for significant growth due to the increasing adoption of LTE/5G wireless technology and the proliferation of intelligent and smart devices among mobile internet users. According to recent studies, smartphone subscriptions in the country are on the rise, with a large portion of the workforce utilizing bring-your-own-device (BYOD) policies. MGM properties and other large enterprises are investing in advanced communication solutions to cater to the connectivity needs of their employees and customers. In response, infrastructure providers like ExteNet Systems are expanding their offerings to include distributed antenna systems (DAS) and small cell base stations. These infrastructure components are essential for enhancing indoor coverage and capacity for mobile networks, particularly in high-density areas such as offices, malls, and stadiums.

However, the increasing use of in-building wireless solutions also brings cybersecurity concerns, as these networks can be vulnerable to cyberattacks. As such, it is crucial for RAN users to prioritize network security and implement strong infrastructure and protocols to mitigate risks. In conclusion, the in-building wireless market in the US is expected to experience substantial growth due to the rising demand for enhanced connectivity and the increasing adoption of smart devices. By investing in advanced communication solutions, businesses can improve productivity, enhance the customer experience, and stay competitive in today's digital landscape.

Market Challenge

The threat of cybersecurity breaches is a key challenge affecting market growth. In Building Wireless solutions are gaining traction in the US market, particularly in smart cities and automated buildings, to ensure seamless communication among connected devices. Electronics and Telecommunications companies, such as Comba Network and Comba Telecom, are at the forefront of this development, introducing 5G extended picocells to enhance connectivity. Telecom operators are increasingly investing in these networks to cater to the growing demand for high-speed internet.

However, the integration of 5G networks brings new security challenges. Cyber-attacks on these networks can lead to data breaches or Distributed Denial of Service (DDoS) attacks. As the use of wireless technology continues to evolve, it is crucial for organizations to prioritize cybersecurity measures to safeguard their networks and consumer data. Wireless router technology plays a significant role in securing these networks, with advanced features like encryption and firewalls becoming essential. The future of in-building wireless networks lies in continued innovation and collaboration between technology providers and telecom operators to address the evolving needs of businesses and consumers.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Airspan Networks Holdings Inc: The company offers in-building wireless solutions such as Neutral Host Networks, which optimize shared infrastructure and are perfect for small and medium-sized buildings with lower densities.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced RF Technologies Inc.

- Airspan Networks Holdings Inc.

- American Tower Corp.

- AT and T Inc.

- BTI wireless

- Cellnex Telecom SA

- CommScope Holding Co. Inc.

- Corning Inc.

- Dali Wireless

- Huawei Technologies Co. Ltd.

- LBA Group Inc.

- MILLER ELECTRIC CO.

- NEC Corporation

- PBE Group

- Samsung Electronics Co. Ltd.

- SOLiD

- Telefonaktiebolaget LM Ericsson

- Uniinfo Telecom Services Ltd.

- Verizon Communications Inc.

- WESCO International Inc.

- Wilson Electronics

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

In-building wireless solutions have gained significant attention in the worldwide market due to the increasing demand for reliable network coverage in various facilities. With the digital change, mission-critical applications and smart devices have become an integral part of our daily lives, leading to a growth in mobile internet usage and smartphone subscriptions. In-building wireless solutions provide uninterrupted cellular connectivity, ensuring business assurance and public safety measures in buildings and rural areas. The use of smart technologies such as 5G extended picocells, routers, and antennas has revolutionized in-building wireless technology. Telecom operators are investing in small cell infrastructure, including picocells and small cells, to expand their network coverage and enhance data throughput.

Additionally, unlicensed spectrum, such as CBRS and MulteFire bands, is being utilized to provide in-building wireless connectivity without the need for building permits or third-party networking infrastructure. Real estate assets, including multi-tenant housing, residential communities, and commercial facilities, are increasingly adopting in-building wireless solutions to meet the growing demand for reliable connectivity. In-building wireless market is witnessing significant growth due to the increasing penetration of digital technologies and the increasing use of intelligent devices and smartphones. Cyberattacks and RAN users are driving the need for advanced infrastructure components, including base stations, small cells, and repeaters. The development of wireless technology, including router technology and Wi-Fi solutions, is a key factor in the growth of the in-building wireless market.

In conclusion, the in-building wireless market is witnessing significant growth due to the increasing demand for reliable network coverage, the adoption of smart technologies, and digital transformation. The use of various wireless technologies, including LTE/5G wireless, Wi-Fi, Bluetooth, Zigbee, and Li-Fi, is driving the growth of the market. The market is expected to continue growing due to the increasing penetration of digital technologies, the increasing use of intelligent devices, and the expanding use cases for in-building wireless solutions.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

186 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.8% |

|

Market growth 2024-2028 |

USD 7.40 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

7.9 |

|

Regional analysis |

North America, APAC, Europe, South America, and Middle East and Africa |

|

Performing market contribution |

North America at 34% |

|

Key countries |

US, China, Japan, South Korea, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Advanced RF Technologies Inc., Airspan Networks Holdings Inc., American Tower Corp., AT and T Inc., BTI wireless, Cellnex Telecom SA, CommScope Holding Co. Inc., Corning Inc., Dali Wireless, Huawei Technologies Co. Ltd., LBA Group Inc., MILLER ELECTRIC CO., NEC Corporation, PBE Group, Samsung Electronics Co. Ltd., SOLiD, Telefonaktiebolaget LM Ericsson, Uniinfo Telecom Services Ltd., Verizon Communications Inc., WESCO International Inc., and Wilson Electronics |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -