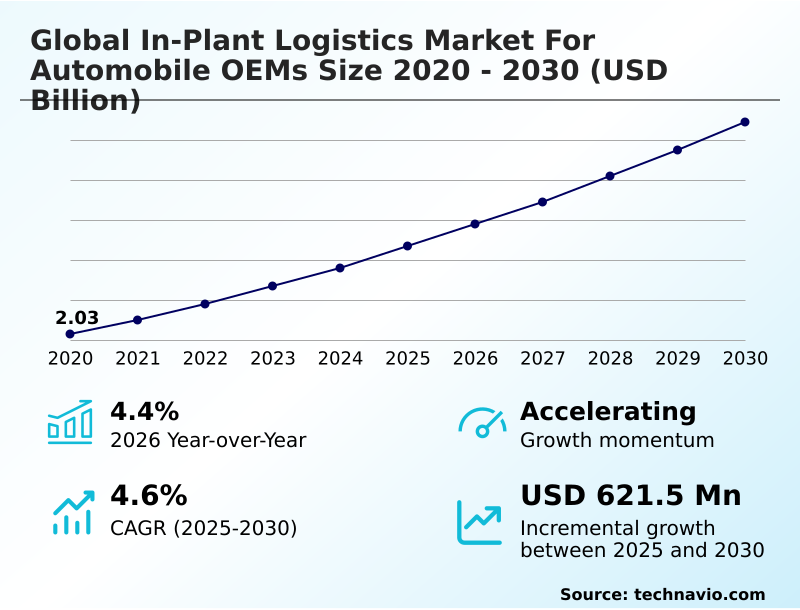

In-plant Logistics For Automobile Oems Market Size 2026-2030

The in-plant logistics for automobile oems market size is valued to increase by USD 621.5 million, at a CAGR of 4.6% from 2025 to 2030. Accelerating transition toward electric vehicle production will drive the in-plant logistics for automobile oems market.

Major Market Trends & Insights

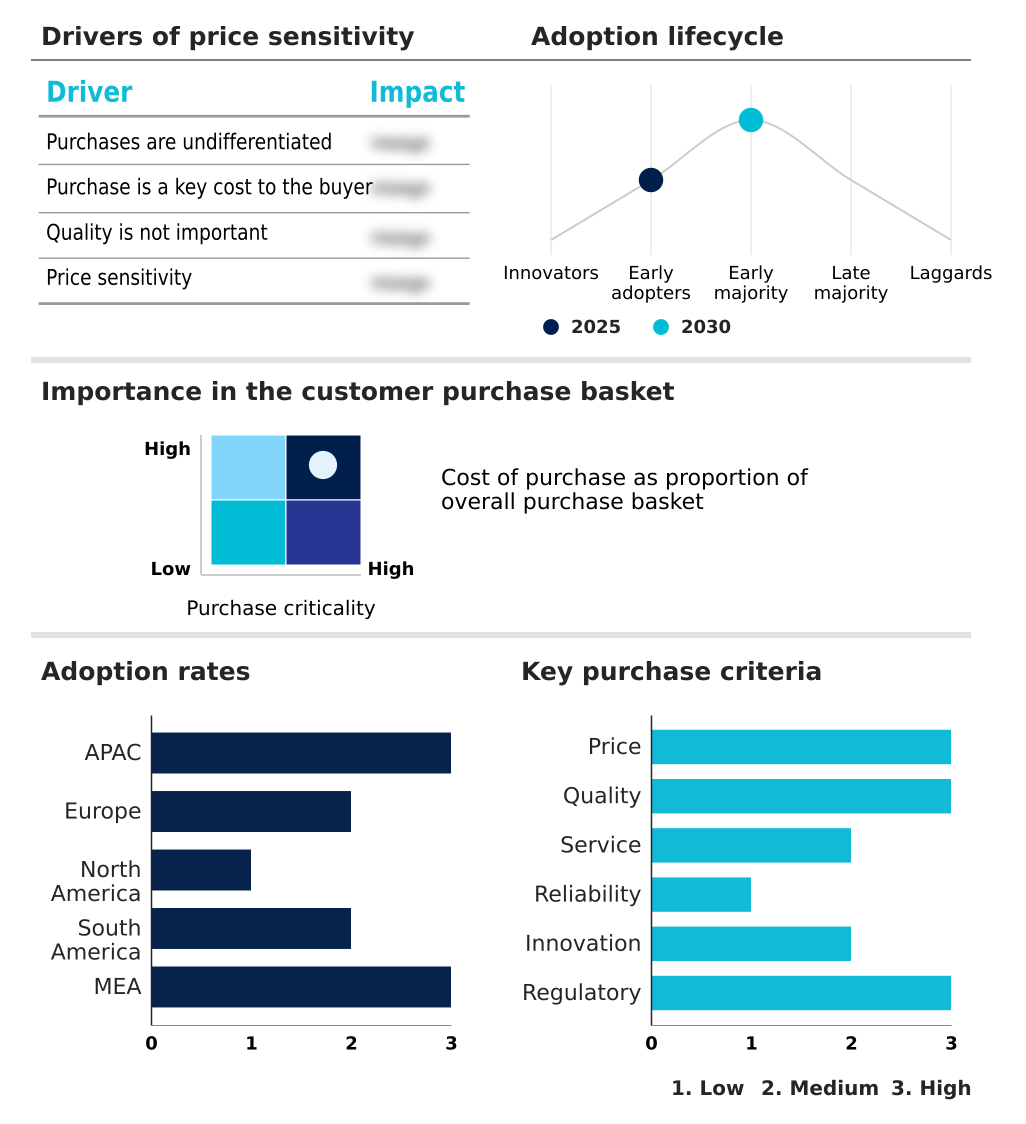

- APAC dominated the market and accounted for a 45.4% growth during the forecast period.

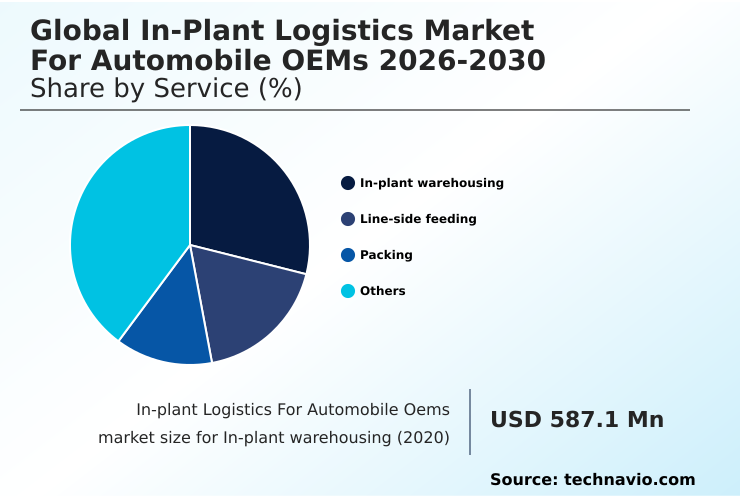

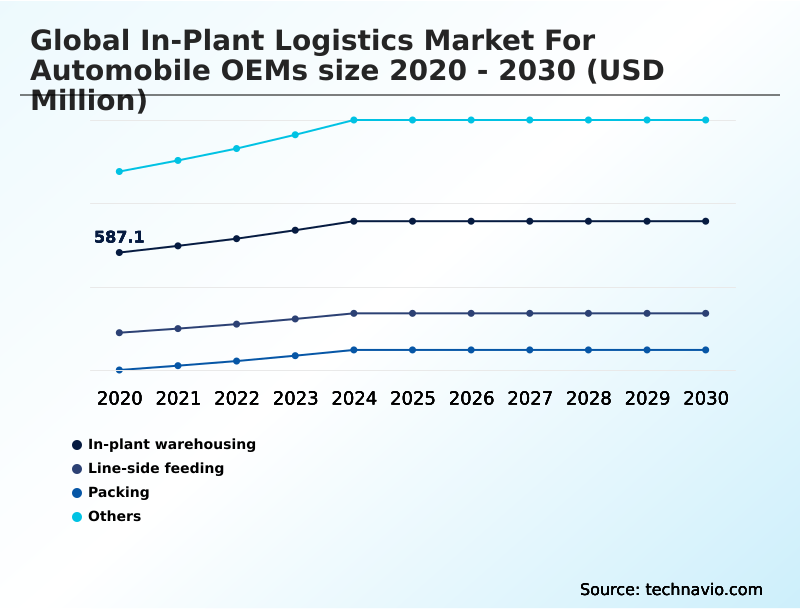

- By Service - In-plant warehousing segment was valued at USD 672.6 million in 2024

- By Product Type - Semi automated segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 1.06 billion

- Market Future Opportunities: USD 621.5 million

- CAGR from 2025 to 2030 : 4.6%

Market Summary

- The in-plant logistics market for automobile oems is defined by the strategic management of material flow and inventory control within the physical confines of a vehicle manufacturing plant. This domain is critical for achieving lean manufacturing goals, driven by the need for operational efficiency and waste reduction.

- As manufacturers navigate the shift from internal combustion engine (ICE) vehicles to electric vehicle (EV) production, the complexity of the internal supply chain escalates, demanding more sophisticated solutions. For example, a facility producing both vehicle types must implement flexible logistics to manage two different material streams, including the specialized handling of high-voltage battery components, without creating bottlenecks.

- This dual-production scenario highlights the market's evolution toward intelligent automation and digitized systems that support just-in-time and just-in-sequence delivery models. The integration of autonomous mobile robots (AMRs) and automated guided vehicles (AGVs) is becoming standard to replace rigid conveyance, enabling a dynamic response to fluctuating production schedules and the high degree of mass customization demanded by consumers.

- This transformation ensures that the correct parts reach the assembly line with precision, minimizing downtime and inventory holding costs.

What will be the Size of the In-plant Logistics For Automobile Oems Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the In-plant Logistics For Automobile Oems Market Segmented?

The in-plant logistics for automobile oems industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Service

- In-plant warehousing

- Line-side feeding

- Packing

- Others

- Product type

- Semi automated

- Manual

- Fully automated

- Vehicle type

- Passenger cars

- LCVs

- HCVs

- Others

- Geography

- APAC

- China

- Japan

- India

- Europe

- Germany

- France

- UK

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Service Insights

The in-plant warehousing segment is estimated to witness significant growth during the forecast period.

The in-plant warehousing segment is a critical junction for the in-plant material flow within automotive manufacturing, moving beyond static storage to dynamic inventory control.

Modern production warehousing solutions are driven by the need to manage components for both internal combustion engine (ICE) and electric vehicle (EV) production, including specialized protocols for high-voltage battery handling.

The integration of a warehouse management system (WMS) enables real-time inventory tracking and facilitates predictive replenishment, ensuring parts availability. This shift is crucial for optimizing space and capital, particularly in the context of brownfield facility automation where physical constraints exist.

Efficient reverse logistics management for containers and the adoption of vendor managed inventory (VMI) models have led to a documented 10% reduction in line-side stock-outs.

The In-plant warehousing segment was valued at USD 672.6 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 45.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How In-plant Logistics For Automobile Oems Market Demand is Rising in APAC Request Free Sample

The geographic landscape is marked by a divergence in technological adoption. In APAC, greenfield project logistics for new EV plants allows for the immediate deployment of fully automated systems and automated guided vehicles (AGVs) for manufacturing passenger cars.

In contrast, North America and Europe often retrofit existing plants, focusing on targeted automation in line-side feeding and packing. The production of heavy commercial vehicles (HCVs) across regions requires robust material handling equipment (MHE) and yard management system.

Logistics providers are implementing milk run optimization for line-side parts delivery and leveraging automated storage and retrieval system (ASRS) to increase density.

The use of predictive maintenance for MHE has proven to reduce unexpected equipment failure by more than 30%, a critical metric for maintaining production velocity. This regional variation underscores the different paths toward modernizing automotive manufacturing.

Market Dynamics

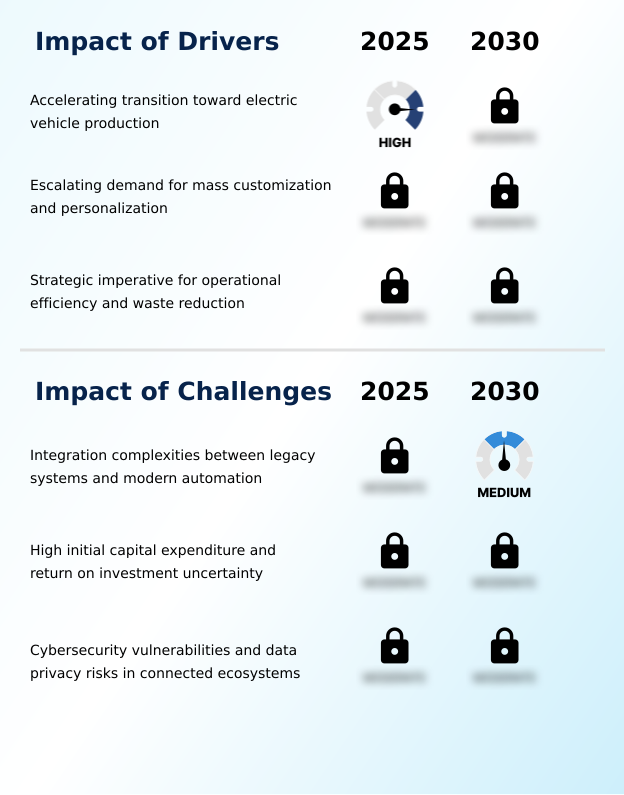

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic implementation of advanced logistics is becoming a key differentiator in the automotive sector. A primary focus is on in-plant logistics for automobile oems for EV battery handling, a process fraught with safety and weight challenges that traditional systems cannot manage.

- Success hinges on integrating wms with mes for just-in-sequence delivery, ensuring that customized components arrive at the assembly line with precision, a factor that can improve production throughput by double-digit percentages compared to less integrated systems. However, the roi calculation for autonomous mobile robots in assembly remains a critical consideration for executives, balancing high capital outlay against long-term operational savings.

- One of the clearest benefits is reducing line stoppages with predictive logistics, which leverages data analytics to anticipate needs before they become critical problems. Further de-risking these investments are the benefits of digital twin simulation in plant layout, allowing for virtual stress-testing of material flows.

- There are significant challenges of automating brownfield automotive facilities, where legacy infrastructure conflicts with modern robotics. Concurrently, cybersecurity risks in connected in-plant logistics are a growing boardroom concern, as interconnected systems create new vulnerabilities. To manage this complexity, many OEMs are adopting 4PL models for managing automotive supply chains.

- These partners often pioneer innovations like smart packaging benefits for component traceability. The in-plant logistics strategies for LCV manufacturing differ from those for passenger cars, focusing on modularity, while optimizing material flow for heavy commercial vehicles requires robust, heavy-duty automation. Even semi-automated kitting process for passenger cars is being refined.

- Firms are leveraging AGVs for finished vehicle logistics and deploying comprehensive container management solutions for returnable packaging. The implementation of yard management systems for plant efficiency, coupled with milk run optimization for lean manufacturing goals, demonstrates a holistic approach.

- Best practices for line-side feeding automation, the central role of ERP in integrated plant logistics, and managing CKD kits for international assembly all reflect the diverse demands of the industry. Ultimately, addressing the impact of mass customization on in-plant logistics is the central challenge that will define the next generation of automotive manufacturing.

What are the key market drivers leading to the rise in the adoption of In-plant Logistics For Automobile Oems Industry?

- The accelerating transition toward electric vehicle production is a key driver, forcing a comprehensive overhaul of material handling strategies within automotive plants.

- The relentless pursuit of operational efficiency in automotive plants is a primary driver, compelling the adoption of lean manufacturing logistics to eliminate waste.

- This focus on material flow optimization supports just-in-time and the more demanding just-in-sequence delivery models, which are essential for aligning with production takt time alignment and achieving perfect assembly line synchronization.

- The rise of mass customization and the production of varied vehicle types, such as light commercial vehicles (LCVs), has made processes like kitting and sequencing critical.

- As a result, investment in automated guided vehicles (AGVs) has surged, with some companies reporting a 15% increase in line-side delivery accuracy.

- The integration of multimodal transport logistics within the plant's inbound and outbound processes further contributes to waste reduction in manufacturing.

What are the market trends shaping the In-plant Logistics For Automobile Oems Industry?

- The widespread adoption of digital twin technology and virtual simulation represents a fundamental shift in logistics planning. This trend moves the industry from a reactive model toward a proactive, predictive approach.

- The adoption of digital twin technology and virtual simulation is a defining trend, enabling manufacturers to de-risk investments in autonomous mobile robots (AMRs) and optimize layouts. Concurrently, the shift toward strategic lead logistics partner (LLP) and fourth-party logistics (4PL) models reflects the growing complexity of operations, particularly in managing logistics for mass customization.

- These partners deploy advanced digital logistics platforms, creating a connected logistics ecosystem that provides end-to-end supply chain visibility solutions. This digital transformation improves forecast accuracy by up to 18%.

- The proliferation of smart packaging and circular packaging, key components of sustainable logistics practices, transforms containers into data nodes, while yard management automation streamlines the movement of finished goods and trailers, reducing vehicle wait times by over 20%.

What challenges does the In-plant Logistics For Automobile Oems Industry face during its growth?

- Integration complexities between legacy systems and modern automation are a key challenge, hindering the widespread advancement of in-plant logistics in existing manufacturing environments.

- A formidable challenge is integrating legacy enterprise resource planning (ERP) platforms with modern manufacturing execution system (MES) and operational technology (OT) infrastructure. This digital friction complicates logistics process automation across the internal supply chain, from receiving dock logistics to finished vehicle logistics.

- The growing threat of cybersecurity for OT systems introduces significant risk, as a breach could paralyze semi-automated systems and disrupt workflows. Managing the intricate logistics for sub-assembly and completely knocked down (CKD) kits for export adds another layer of complexity. Inefficient container management can lead to shortages, while a lack of integration can cause bottlenecks in cross-docking services.

- The application of robotic process automation (RPA) in logistics helps bridge some gaps, but a holistic solution remains elusive, with integration projects sometimes exceeding budgets by 20%.

Exclusive Technavio Analysis on Customer Landscape

The in-plant logistics for automobile oems market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the in-plant logistics for automobile oems market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of In-plant Logistics For Automobile Oems Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, in-plant logistics for automobile oems market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AP Moller Maersk AS - Specializing in integrated in-plant logistics, the focus is on sequencing, line-side supply, and sub-assembly to support just-in-time manufacturing for automotive original equipment manufacturers.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AP Moller Maersk AS

- BLG Logistics

- BR Williams Trucking

- CEVA Logistics SA

- CJ Darcl Logistics Ltd.

- DACHSER SE

- Deutsche Post AG

- Expeditors International Inc.

- GEFCO Group

- GEODIS

- Hellmann Worldwide Logistics

- Imperial Logistics Ltd.

- Kuehne Nagel Management AG

- Mahindra Logistics Ltd.

- Nissin Foods Holdings Co. Ltd.

- Penske Truck Leasing Co. LP

- Ryder System Inc.

- Schenker AG

- Schnellecke Group AG

- United Parcel Service Inc.

- XPO Inc.

- YUSEN LOGISTICS CO. LTD.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in In-plant logistics for automobile oems market

- In January 2025, BMW Manufacturing announced the successful deployment of the Figure 02 humanoid robot at its Spartanburg facility for automating difficult material handling tasks and precise manipulation of sheet metal parts.

- In January 2025, Ryder System Inc. announced significant enhancements to its RyderShare digital platform, providing automobile OEMs with deeper real-time visibility into inventory movement and yard management.

- In February 2025, ORBIS Corporation released the Odyssey Pallet, a new reusable packaging solution engineered to enhance the stability and trackability of automotive components within automated in-plant logistics systems.

- In January 2025, Mahindra Logistics Ltd. announced the operational expansion of its contract logistics network in India, integrating new technology-enabled warehousing solutions to support domestic automotive manufacturers.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled In-plant Logistics For Automobile Oems Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 303 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.6% |

| Market growth 2026-2030 | USD 621.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.4% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, Germany, France, UK, Italy, Spain, The Netherlands, US, Canada, Mexico, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The in-plant logistics market for automobile oems is undergoing a significant transformation, driven by the dual pressures of electrification and mass customization. The core of this evolution lies in sophisticated material flow optimization and tight inventory control. Processes like in-plant warehousing, line-side feeding, and packing are being reimagined through technology.

- The industry's reliance on just-in-time and the more complex just-in-sequence methodologies necessitates flawless execution. This is where advanced systems come into play, including autonomous mobile robots (AMRs) and automated guided vehicles (AGVs), which are managed by a central warehouse management system (WMS).

- This integration of digital twin technology and virtual simulation allows for predictive replenishment and route optimization before physical deployment. To handle the unique demands of electric vehicle (EV) production, especially high-voltage battery handling, and the simultaneous manufacturing of internal combustion engine (ICE) vehicles, new strategies are essential.

- Concepts like the lead logistics partner (LLP) and fourth-party logistics (4PL) are gaining traction, alongside the use of smart packaging and circular packaging in returnable packaging systems. These systems connect with enterprise resource planning (ERP) and manufacturing execution system (MES) platforms, bridging operational technology (OT) with enterprise data.

- Services like kitting, sequencing, sub-assembly, container management, and finished vehicle logistics are becoming more automated, with some facilities managing completely knocked down (CKD) kits for export. This shift is evident across semi-automated systems and fully automated systems for passenger cars, light commercial vehicles (LCVs), and heavy commercial vehicles (HCVs), representing a move that improves parts availability by over 20%.

What are the Key Data Covered in this In-plant Logistics For Automobile Oems Market Research and Growth Report?

-

What is the expected growth of the In-plant Logistics For Automobile Oems Market between 2026 and 2030?

-

USD 621.5 million, at a CAGR of 4.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Service (In-plant warehousing, Line-side feeding, Packing, and Others), Product Type (Semi automated, Manual, and Fully automated), Vehicle Type (Passenger cars, LCVs, HCVs, and Others) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Accelerating transition toward electric vehicle production, Integration complexities between legacy systems and modern automation

-

-

Who are the major players in the In-plant Logistics For Automobile Oems Market?

-

AP Moller Maersk AS, BLG Logistics, BR Williams Trucking, CEVA Logistics SA, CJ Darcl Logistics Ltd., DACHSER SE, Deutsche Post AG, Expeditors International Inc., GEFCO Group, GEODIS, Hellmann Worldwide Logistics, Imperial Logistics Ltd., Kuehne Nagel Management AG, Mahindra Logistics Ltd., Nissin Foods Holdings Co. Ltd., Penske Truck Leasing Co. LP, Ryder System Inc., Schenker AG, Schnellecke Group AG, United Parcel Service Inc., XPO Inc. and YUSEN LOGISTICS CO. LTD.

-

Market Research Insights

- The evolution of the internal supply chain is reshaping automotive manufacturing, focusing on optimizing in-plant material flow from the receiving dock to the assembly line. Modern production warehousing solutions now prioritize real-time inventory tracking and assembly line synchronization to support demanding production takt time alignment.

- As a result of digital logistics platforms, some facilities have seen a 15% reduction in inventory-related errors. Logistics for mass customization drives the need for precise component sequencing for assembly, managed through a connected logistics ecosystem. To achieve lean manufacturing logistics, firms focus on operational efficiency in automotive plants and waste reduction in manufacturing.

- This has led to the adoption of robotic process automation (RPA) in logistics and predictive maintenance for MHE, which can decrease equipment downtime by up to 25%. However, brownfield facility automation presents integration challenges, and cybersecurity for OT systems is a critical concern. Success requires end-to-end supply chain visibility solutions.

We can help! Our analysts can customize this in-plant logistics for automobile oems market research report to meet your requirements.

RIA -

RIA -