Industrial Belt Tensioners Market Size 2025-2029

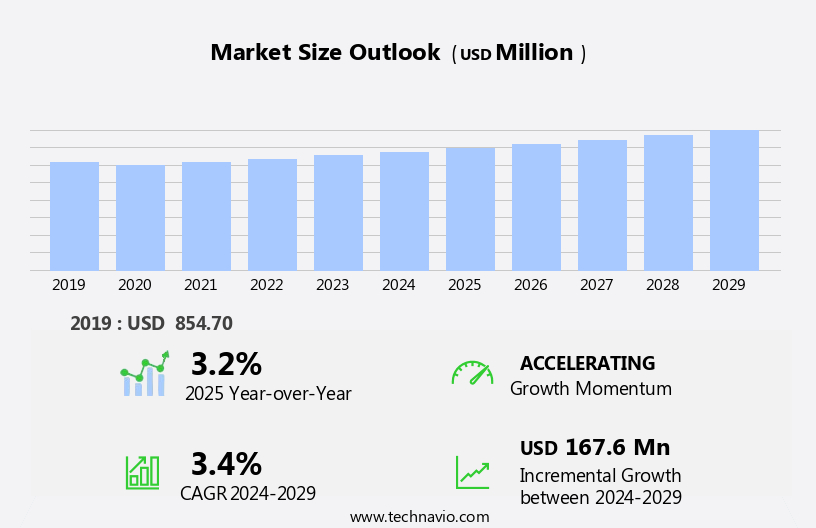

The industrial belt tensioners market size is forecast to increase by USD 167.6 million, at a CAGR of 3.4% between 2024 and 2029.

- The market is driven by the increasing investments in industrial assets, necessitating the need for efficient and reliable belt tensioning systems. Customization of belt tensioners to cater to specific industrial applications is another key trend, as industries seek to optimize their production processes and minimize downtime. The automotive, mining, and aerospace sectors heavily utilize tensioners in engines, automotive tensioners, and hydraulically operated systems. However, the market faces challenges due to the volatility in prices of raw materials used in manufacturing belt tensioners, such as steel and rubber. This price instability can impact the profitability of belt tensioner manufacturers and may lead to increased costs for end-users.

- Additionally, the automotive and manufacturing industries, major consumers of belt tensioners, are experiencing significant shifts towards electric vehicles and automation, respectively. Companies in the market must stay abreast of these trends and adapt their product offerings and business strategies accordingly to capitalize on new opportunities and navigate challenges effectively. AI-powered tensioners and finite element analysis are the future, offering advanced capabilities for predictive maintenance and improved operational efficiency.

What will be the Size of the Industrial Belt Tensioners Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

- The market is witnessing significant advancements, driven by the integration of technology and the pursuit of optimized performance and cost savings. Key trends include the adoption of IoT integration and cloud-based solutions for remote monitoring and virtual commissioning. Environmental impact is a growing concern, leading to the development of smart tensioning systems with noise reduction, dust and debris resistance, and material science advancements for improved wear resistance and temperature resistance. Data analytics and machine learning are revolutionizing belt dynamics analysis, enabling early detection of belt slip and vibration, resulting in extended belt life and reduced downtime.

- Torque measurement and simulation software are also crucial for ensuring belt performance under various environmental conditions. Abrasion and chemical resistance are essential considerations for belt tensioners in harsh industrial environments. Key industries, including the passenger car, 2-wheeler, and commercial vehicle sectors, rely on belt drives, V-belts, variable belts, synchronous timing belts, and accessory drive belts for power transmission.

How is this Industrial Belt Tensioners Industry segmented?

The industrial belt tensioners industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

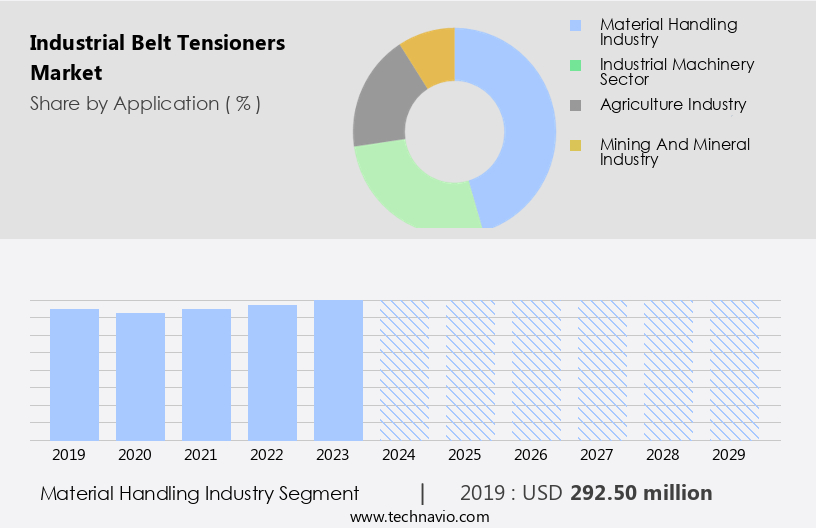

- Material handling industry

- Industrial machinery sector

- Agriculture industry

- Mining and mineral industry

- Type

- Automatic

- Non-automatic

- Material

- Steel tensioners

- Aluminum tensioners

- Plastic tensioners

- Composite material tensioners

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- Australia

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Application Insights

The material handling industry segment is estimated to witness significant growth during the forecast period. In material handling applications, conveyor belts play a crucial role in transporting heavy or bulky items efficiently. Proper belt tension is vital to prevent slippage, minimize wear and tear, and ensure consistent material transport. Belt tensioning devices, including hydraulic, pneumatic, mechanical, and motorized tensioners, help maintain the correct belt tension. Tension sensors and feedback systems enable real-time tension monitoring and optimization. Belt materials, such as rubber, polyurethane, and steel, vary based on application requirements. Belt width, capacity, and speed also influence tension management. Energy efficiency is a significant consideration in material handling, with tension optimization contributing to reduced power consumption and increased productivity.

Belt maintenance, including cleaning, alignment, splicing, and lubrication, is essential to prolong belt life and minimize downtime. Compliance with safety standards and process control requirements is also crucial. Tensioner installation, calibration, and replacement are critical aspects of belt maintenance. Belt tensioners are integral to the efficient operation of conveyor systems in industries like packaging machinery, industrial automation, and heavy-duty applications. Precision tensioning ensures consistent belt performance and reduces the risk of belt-related failures. Tensioner brackets and housings support proper belt alignment and tracking. Belt tension management is a continuous process that involves regular inspection and adjustment.

Automatic tensioners and control systems facilitate this process, ensuring consistent belt tension and reducing the need for manual intervention. Belt thickness and belt wear are essential factors in tension management, as they influence belt performance and lifespan. The market for these tensioners is influenced by the price volatility of raw materials such as metals, plastics, and rubber used in their production.

The Material handling industry segment was valued at USD 292.50 million in 2019 and showed a gradual increase during the forecast period.

The Industrial Belt Tensioners Market is evolving with advanced vibration analysis techniques, ensuring optimal performance and durability. Improved belt slip detection systems help prevent inefficiencies and downtime in industrial operations. The integration of digital twins enables real-time monitoring and predictive maintenance, enhancing equipment reliability. High abrasion resistance materials in belt tensioners contribute to longer lifespan and reduced maintenance costs. Innovations focused on reduced vibration enhance operational efficiency while minimizing wear and tear on machinery.

Regional Analysis

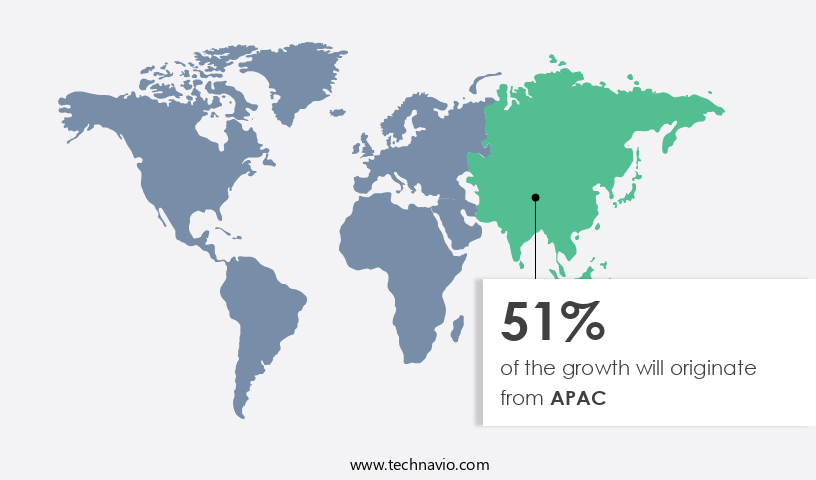

APAC is estimated to contribute 51% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

In APAC, the industrial sector is experiencing significant advancements, with countries like India and China spearheading creative initiatives such as "Make in India" and "Made in China" to bolster their domestic manufacturing industries. China is poised to lead Asian nations in industrial growth, particularly in sectors like industrial machinery, mining, agriculture, and construction. Notably, Australia and China are witnessing a rise in the mining and minerals industry, leading to increased machinery adoption. Consequently, the regional market for industrial belt tensioners is projected to expand at an impressive rate. Material handling applications, which include conveyor systems and packaging machinery, are primary consumers of belt tensioning devices.

Belt tension optimization ensures energy efficiency, reduces downtime, and enhances productivity. Various types of belts, such as flat, round, polyurethane, steel, rubber, and timing belts, necessitate different tensioning methods. Hydraulic, pneumatic, mechanical, and motorized tensioners cater to these requirements. Belt maintenance practices, including belt cleaning, tension measurement, alignment, and lubrication, are crucial for belt longevity and optimal performance. Safety standards and compliance requirements mandate regular belt inspection and tensioner calibration. Precision tensioning and automatic tensioners are increasingly popular for heavy-duty applications. Belt tension management systems employ sensors and control systems to provide real-time feedback, enabling belt wear monitoring and proactive maintenance.

Tensioner installation, replacement, and adjustment are essential for maintaining belt capacity and ensuring process control. Belt splicing and belt joining techniques ensure seamless belt transitions and minimize belt wear. Belt tensioners play a vital role in industrial automation, ensuring efficient and reliable belt operation. High-performance belts, designed for heavy loads and high speeds, necessitate robust tensioning systems. Tensioner bearings and housings facilitate smooth belt movement and protect against wear and tear. The market in APAC is expected to grow at an exponential rate due to the increasing adoption of machinery in the mining and manufacturing sectors.

The market caters to various belt types and applications, employing various tensioning methods and maintenance practices to ensure optimal belt performance and longevity. Precision tensioning, safety standards, and ease of use are key considerations for manufacturers when selecting belt tensioners, making this a dynamic and evolving market. China is projected to lead the region's industrial growth, particularly in sectors like industrial machinery, mining, agriculture, and construction.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Industrial Belt Tensioners market drivers leading to the rise in the adoption of Industry?

- A significant contributor to market growth is the escalating investment in industrial assets. The market is experiencing significant growth due to the increasing adoption of high performance belts in heavy duty applications. Industrial automation is a key trend in manufacturing, leading companies to invest in advanced machinery to minimize downtime and boost productivity. This growth is particularly noticeable in the Asia Pacific region, where governments are implementing initiatives to strengthen domestic manufacturing sectors. Industrial belt tensioners play a crucial role in maintaining the efficiency and longevity of conveyor systems and packaging machinery. Precision tensioning, belt inspection, and tensioner calibration are essential for ensuring optimal belt performance and minimizing belt wear.

- Automatic tensioners offer safety standards and ease of use, making them a popular choice for industrial applications. Belt joining and tensioner brackets are essential components of industrial belt drives. The thickness and material of the belts vary depending on the specific application, and tensioners must be able to accommodate these variations. As industrial processes become more complex and demanding, the need for reliable and efficient belt tensioning solutions continues to grow. The market is driven by the increasing demand for productivity and efficiency in manufacturing processes. The adoption of advanced machinery and automation, particularly in the Asia Pacific region, is fueling this growth.

What are the Industrial Belt Tensioners market trends shaping the Industry?

- Customized belt tensioners are currently gaining popularity in the market for their ability to be tailored to specific industrial applications. The development of these advanced tensioners represents a significant trend in the industry. Industrial belt tensioners play a crucial role in optimizing the performance of flat belts in capital-intensive industries. These tensioners ensure proper belt load and alignment, preventing belt slippage and enhancing energy efficiency. Manufacturers are responding to end-users' demands for advanced belt drive systems by expanding their product portfolios through strategic acquisitions.

- The focus on material handling applications and conveyor belts highlights the importance of belt tension optimization. Industrial belt tensioners contribute significantly to the modernization of machinery in various industries, making them an indispensable component of contemporary drive systems. By collaborating with end-users, these companies can better understand their requirements and customize belt tensioning devices, including those for polyurethane belts. Belt tension monitoring and measurement are essential for maintaining belt tension and ensuring the drive system's overall efficiency.

How does Industrial Belt Tensioners market face challenges during its growth?

- The volatility in the prices of raw materials used in manufacturing belt tensioners poses a significant challenge to the industry's growth trajectory. Industrial belt tensioners play a crucial role in maintaining optimal belt speed in manufacturing processes, which directly impacts productivity. Two common types of industrial belts are round belts and steel belts, each requiring specific tensioning methods. Hydraulic tensioners and mechanical tensioners are commonly used for belt tensioning. Belt maintenance is essential to ensure continuous operation and prevent downtime. Proper belt tension management is critical for belt longevity and efficiency. Belt cleaning is another essential aspect of belt maintenance, as debris buildup can negatively affect belt performance. Belt tension feedback systems, such as tensioner sensors, provide real-time data on belt tension levels.

- This information is vital for preventive maintenance and timely replacement of worn-out belts. Belt material, whether rubber or steel, influences the choice of tensioning method and the required belt width. Raw material price volatility can significantly impact the market. Increases in raw material prices can lead to higher production costs for manufacturers, potentially affecting demand and profit margins. Ensuring a stable supply of raw materials at reasonable prices is essential for maintaining production schedules and delivery times. The market faces challenges due to raw material price volatility. Proper belt tension management, belt maintenance, and the use of advanced technologies like belt cleaning and tension feedback systems are essential for maintaining productivity and efficiency.

Exclusive Customer Landscape

The industrial belt tensioners market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the industrial belt tensioners market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, industrial belt tensioners market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AB SKF - The company specializes in providing advanced industrial belt tensioning solutions. Our offerings encompass automatic belt tensioner units and the SKF belt tension system.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AB SKF

- Applied Industrial Technologies Inc.

- Bando Chemical Industries Ltd.

- Brewer Machine and Gear Co.

- Continental AG

- Dayco IP Holdings LLC

- Gates Industrial Corp. Plc

- Hangzhou Chinabase Machinery Co. Ltd.

- Hutchinson SA

- Litens Automotive

- Michelin Group

- Murtfeldt Kunststoffe GmbH and Co. KG

- Regal Rexnord Corp.

- Schaeffler AG

- The Timken Co.

- TotalEnergies SE

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Industrial Belt Tensioners Market

- In February 2023, Trelleborg AB, a leading industrial solutions provider, announced the launch of its new line of industrial belt tensioners, the T-TEN Series, designed for heavy-duty applications in the mining and quarrying sectors (Trelleborg AB Press Release, 2023). This expansion broadens the company's product portfolio and strengthens its presence in the market.

- In July 2024, Continental AG and Schaeffler AG, two major automotive and industrial suppliers, entered into a strategic partnership to develop and produce belt drives for electric vehicles (Continental AG Press Release, 2024). This collaboration is expected to result in advanced belt tensioning systems, contributing to the growth of the market in the electric vehicle sector.

- In November 2024, ContiTech AG, a subsidiary of Continental AG, acquired the industrial belt tensioner business of a leading European competitor, expanding its market share and product offerings in the European market (ContiTech AG Press Release, 2024). This acquisition is expected to generate significant synergies and economies of scale for ContiTech AG.

- In March 2025, the European Union passed new regulations on emissions standards for industrial processes, which include the use of energy-efficient belt tensioning systems (European Parliament and Council of the European Union, 2025). This regulatory development is expected to drive demand for advanced industrial belt tensioners in Europe, as companies seek to comply with the new regulations and reduce their carbon footprint.

Research Analyst Overview

The market is characterized by its continuous evolution, driven by the dynamic interplay of various factors. Belt load, a significant influencer, is a constant concern for manufacturers seeking to optimize their drive systems and enhance energy efficiency. Belt tensioning devices, including hydraulic, pneumatic, and mechanical varieties, are essential components in this regard, enabling precise belt tensioning and monitoring. Belt slippage, a common issue in material handling applications, is addressed through advanced belt tension optimization techniques. These methods, in turn, contribute to increased productivity and reduced downtime. Polyurethane belts, with their superior strength and durability, are increasingly adopted in heavy-duty applications, necessitating the development of specialized tensioners and installation techniques.

Belt alignment, tension measurement, and belt cleaning are critical aspects of belt maintenance, ensuring the longevity and performance of conveyor belts and other industrial applications. Compliance with safety standards and process control requirements is another driving force, leading to the development of automatic tensioners, tensioner control systems, and belt tension feedback mechanisms. Belt capacity, belt speed, belt width, and belt thickness are essential factors influencing belt selection and tensioning requirements. As industries continue to automate and demand higher performance from their machinery, the market for industrial belt tensioners will remain a vibrant and dynamic arena.

The Industrial Belt Tensioners Market is evolving with advancements in pneumatic tensioners and efficient tensioner adjustment technologies, ensuring smooth operation across industries. Optimized belt tracking enhances the lifespan of rubber belts, reducing wear and tear in conveyor belt systems. Reliable belt lubrication helps maintain performance, while durable tensioner springs and tensioner housings improve stability and longevity. Proper belt tension measurement is critical for preventing failures in high-speed drive system operations. Regular tensioner replacement ensures consistent efficiency, minimizing downtime in industrial processes.

Dive into Technavio's strong research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Industrial Belt Tensioners Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

226 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.4% |

|

Market growth 2025-2029 |

USD 167.6 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

3.2 |

|

Key countries |

US, China, Japan, India, South Korea, Germany, UK, Australia, Canada, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Industrial Belt Tensioners Market Research and Growth Report?

- CAGR of the Industrial Belt Tensioners industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the industrial belt tensioners market growth of industry companies

We can help! Our analysts can customize this industrial belt tensioners market research report to meet your requirements.

RIA -

RIA -