Industrial Digital Twin For Heavy Industries Market Size 2026-2030

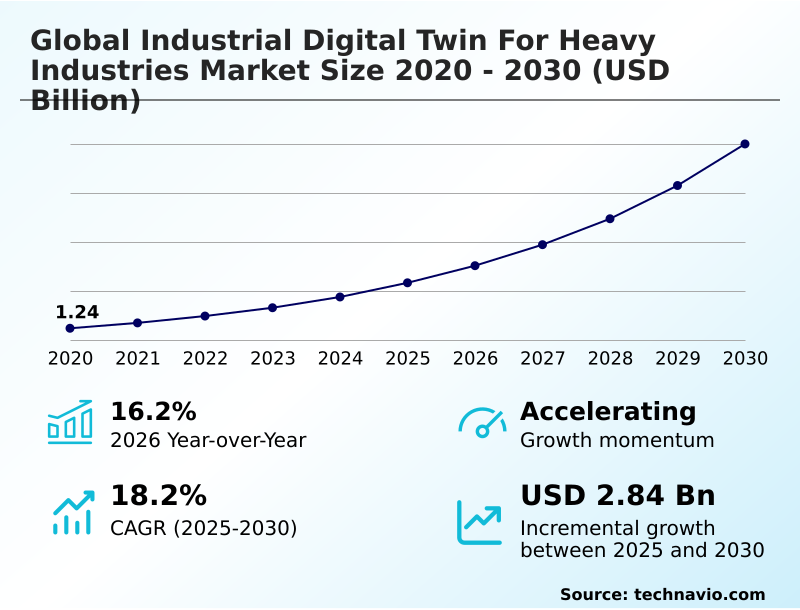

The industrial digital twin for heavy industries market size is valued to increase by USD 2.84 billion, at a CAGR of 18.2% from 2025 to 2030. Optimization of asset lifecycle and predictive maintenance will drive the industrial digital twin for heavy industries market.

Major Market Trends & Insights

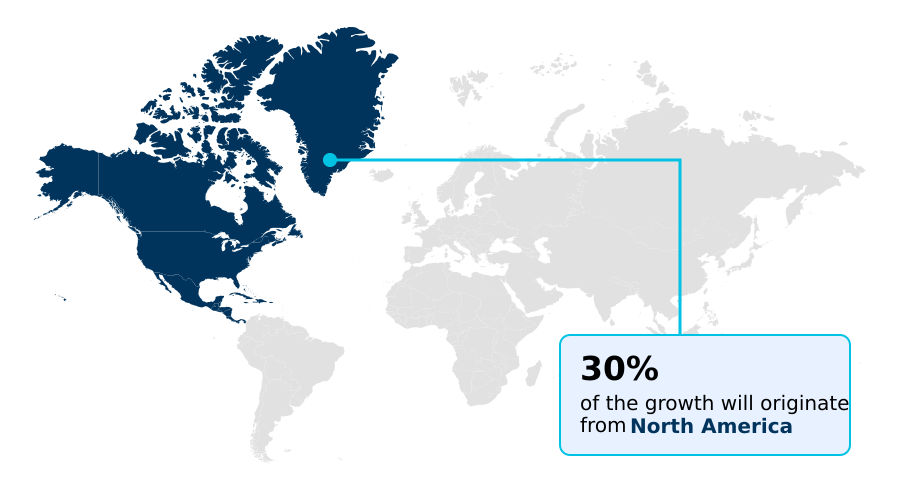

- North America dominated the market and accounted for a 29.8% growth during the forecast period.

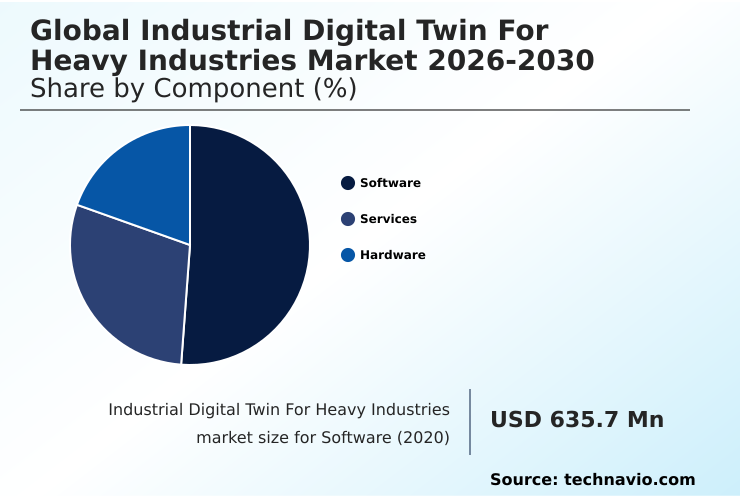

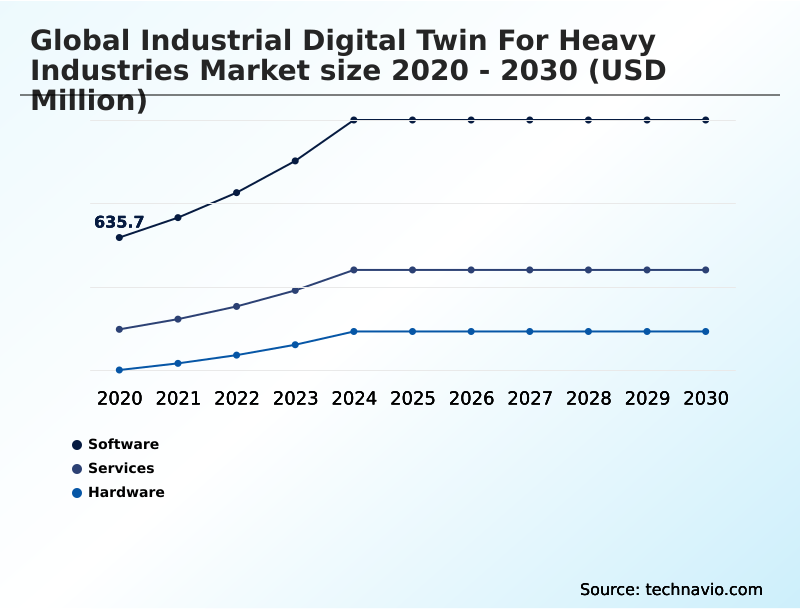

- By Component - Software segment was valued at USD 984.2 million in 2024

- By Deployment - Cloud segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 3.77 billion

- Market Future Opportunities: USD 2.84 billion

- CAGR from 2025 to 2030 : 18.2%

Market Summary

- The industrial digital twin for heavy industries market is defined by the convergence of advanced simulation, real-time data analytics, and the industrial internet of things (iiot). This technology enables the creation of a high-fidelity virtual replica of physical assets and processes, facilitating asset lifecycle optimization and a shift toward predictive maintenance models.

- Key drivers include the need for enhanced operational efficiency and sustainability, with physics-based simulation allowing for heavy machinery simulation and virtual testing that minimizes physical prototyping. For instance, a heavy equipment manufacturer can simulate wear and tear under various operational scenarios to refine designs using generative design algorithms before production, improving durability and reducing material waste.

- digital thread integration connects disparate data from plm and erp systems, providing a holistic view of operations. However, the market faces challenges related to data interoperability standards and the high cost of retrofitting legacy equipment with high-precision sensors.

- The integration of machine learning algorithms is also pivotal, enabling predictive and prescriptive analytics that transform factory floor data collection from a monitoring activity into a strategic asset for manufacturing process optimization and informed decision-making across the enterprise.

What will be the Size of the Industrial Digital Twin For Heavy Industries Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Industrial Digital Twin For Heavy Industries Market Segmented?

The industrial digital twin for heavy industries industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Software

- Services

- Hardware

- Deployment

- Cloud

- On-premises

- Hybrid

- Sector

- Downstream

- Upstream

- Midstream

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

By Component Insights

The software segment is estimated to witness significant growth during the forecast period.

The software segment is the core of the market, providing the architecture for creating a high-fidelity virtual replica of physical assets. This involves physics-based simulation for industrial equipment virtual testing and heavy machinery simulation.

Through real-time data synchronization from factory floor data collection, these platforms enable advanced predictive and prescriptive analytics and robust asset performance management (apm).

The integration of generative design algorithms drives manufacturing process optimization and informs predictive maintenance models across the entire asset lifecycle optimization.

The industrial internet of things (iiot) underpins this ecosystem, with some platforms demonstrating over 20% improvement in fault detection accuracy, shifting maintenance from scheduled intervals to condition-based interventions.

The Software segment was valued at USD 984.2 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 29.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Industrial Digital Twin For Heavy Industries Market Demand is Rising in North America Request Free Sample

Regional adoption patterns vary, with APAC demonstrating the most rapid expansion, outpacing North America by nearly two percentage points. In regions with significant natural resource sectors, the focus is on raw material extraction simulation and midstream asset management.

Technologies enabling subsea wellhead monitoring and the analysis of geological surveys and high-frequency vibration data are critical. These specialized applications support heavy equipment remanufacturing and facilitate remote expert assistance, driving the creation of autonomous industrial environments.

A key goal is achieving a holistic industrial ecosystem view with cross-platform interoperability, supported by digital product passports for blast furnace optimization and sustainability tracking. Enhanced virtual reality training simulations are also being deployed to improve safety.

Market Dynamics

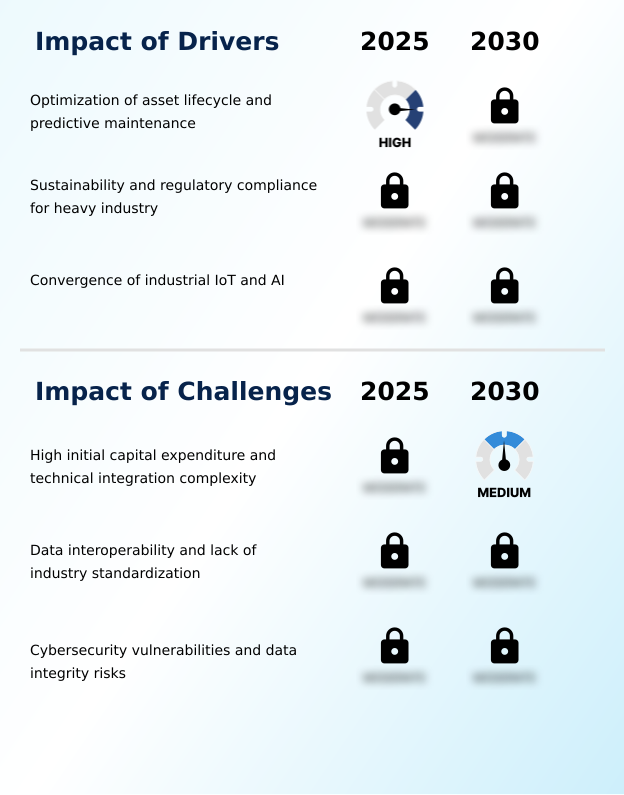

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic implementation of digital twin technology is becoming a competitive differentiator in heavy industries. Digital twin for predictive maintenance in mining is a prime example, where real-time asset health monitoring significantly reduces costly equipment failures. Similarly, manufacturers are using virtual commissioning to reduce factory downtime, validating production line changes in a virtual space before physical implementation.

- The role of generative ai in industrial design and simulation is expanding, enabling engineers to rapidly iterate and optimize complex components. However, addressing cybersecurity risks in ot and it convergence remains a critical priority for maintaining operational integrity. The industrial metaverse for remote collaboration and training is another key area, allowing global teams to interact with virtual assets.

- The benefits of 5g for real-time digital twins are substantial, providing the low latency needed for precise control loops. The extension of the digital thread for sustainability and circular economy is now essential for ESG reporting, supported by digital product passports that track embodied carbon.

- Overcoming interoperability challenges in multi-vendor digital twin ecosystems is vital for creating a unified operational view. Enterprises are focusing on optimizing asset lifecycle with digital twin technology, leveraging edge computing applications for heavy manufacturing twins to process data locally. The decision between cloud vs on-premise digital twin deployment models often depends on security and latency needs.

- These systems are also crucial for improving supply chain visibility with digital twins and demonstrating the role of digital twins in achieving esg goals, which now influences investment decisions more than ever. Digital twin applications in aerospace manufacturing continue to set industry benchmarks.

- Overall, the market is focused on real-time monitoring of heavy industrial assets, leveraging physics-based simulation for structural integrity testing, and exploring natural language interfaces for digital twin interaction to democratize data access. How digital twins enhance worker safety training in virtual environments is also a major focus, demonstrating benefits that extend beyond pure operational efficiency.

What are the key market drivers leading to the rise in the adoption of Industrial Digital Twin For Heavy Industries Industry?

- The need to optimize asset lifecycles and implement predictive maintenance models is a primary driver for market growth in heavy industries.

- Market expansion is driven by the need for low-latency data transmission, supported by 5g-enabled digital platforms that enable real-time asset monitoring. The installation of high-precision sensors is fundamental, yet achieving data integrity and governance requires overcoming legacy system integration challenges.

- A major driver is the integration of product lifecycle management (plm) and enterprise resource planning (erp) systems to create a unified data model. This enhances industrial control systems security and supports initiatives like circular economy tracking.

- Adherence to data interoperability standards is crucial, as it allows for precise energy consumption modeling and helps reduce operational risks by up to 25% through better system-wide visibility.

What are the market trends shaping the Industrial Digital Twin For Heavy Industries Industry?

- The integration of generative AI and natural language interfaces is emerging as a significant trend. This transforms digital twins from passive monitors into active advisory systems.

- A key trend is the convergence of operational technology (ot) and information technology (it), enabled by edge computing hardware for remote operational intelligence. This facilitates digital thread integration across the value chain, improving supply chain visibility enhancement.

- The rise of industrial metaverse environments and immersive collaborative design using augmented reality headsets allows for virtual commissioning, which can reduce project validation times by up to 30%. This trend also supports sustainable manufacturing solutions through better carbon footprint reporting, with some systems achieving regulatory compliance automation for over 95% of reporting requirements.

- These advancements are redefining how manufacturers design, build, and operate heavy industrial assets.

What challenges does the Industrial Digital Twin For Heavy Industries Industry face during its growth?

- High initial capital expenditure and the technical complexity of integrating with legacy systems present a key challenge to market adoption.

- Significant challenges persist, primarily from the use of proprietary communication protocols that hinder the creation of unified open-source data lakes. The effective use of machine learning algorithms and natural language processing is constrained without standardized data. Industrial automation systems and real-time robotic coordination depend on closed-loop feedback systems and synchronous operational environments, which are difficult to achieve across disparate platforms.

- While virtual prototyping for heavy industry and structural integrity analysis show promise, their accuracy is limited by inconsistent data inputs. Improving resource utilization analysis requires better sensor integration, including specialized tools like downhole sensors, to move past the current fragmented data landscape, where integration failures can increase project costs by 15%.

Exclusive Technavio Analysis on Customer Landscape

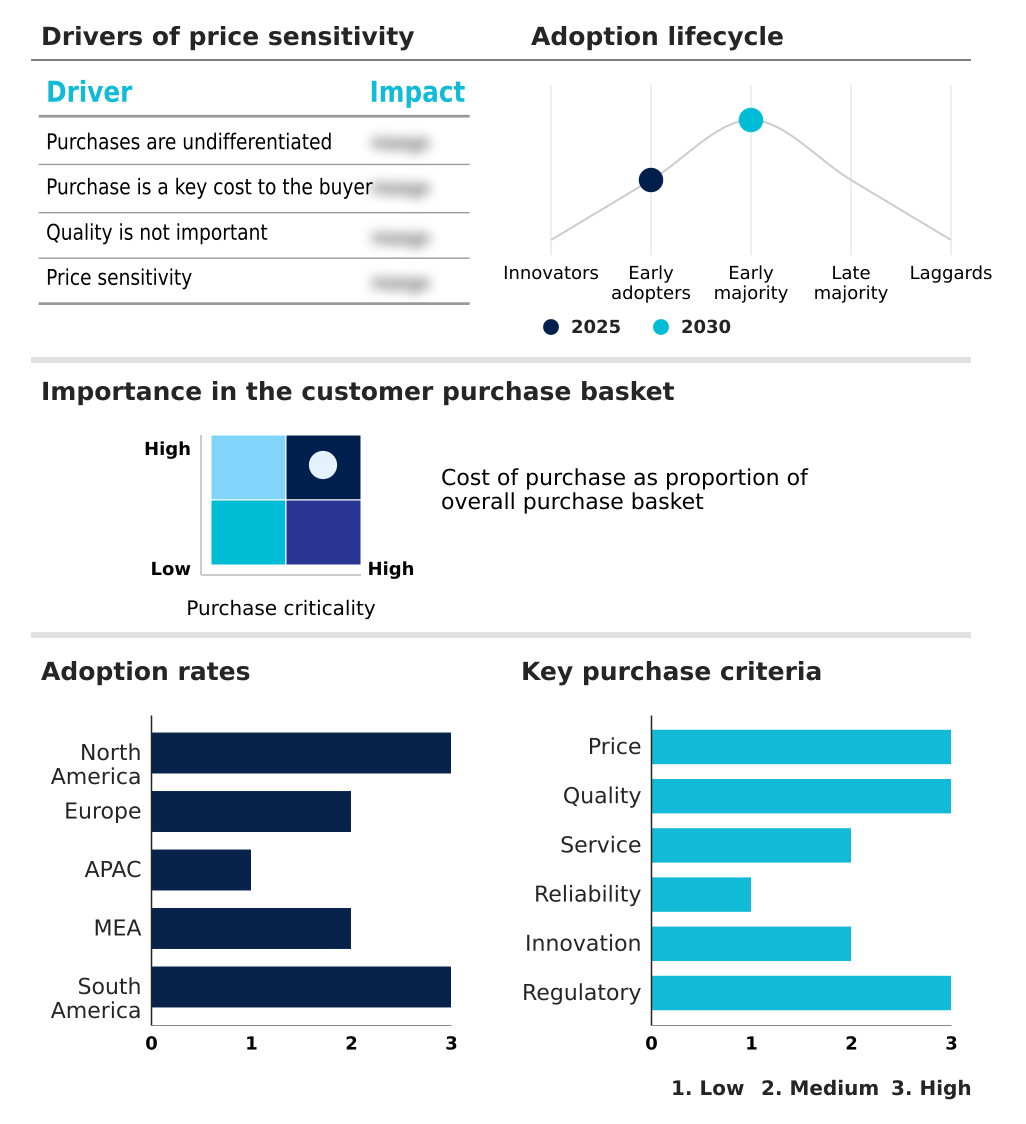

The industrial digital twin for heavy industries market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the industrial digital twin for heavy industries market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Industrial Digital Twin For Heavy Industries Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, industrial digital twin for heavy industries market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - Provides industrial digital twins via a proprietary platform, enabling real-time asset monitoring, predictive maintenance, and performance optimization for heavy equipment.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Altair Engineering Inc.

- Amazon.com Inc.

- ANSYS Inc.

- Bentley Systems Inc.

- Dassault Systemes SE

- Emerson Electric Co.

- General Electric Co.

- Hexagon AB

- Honeywell International Inc.

- IBM Corp.

- Microsoft Corp.

- Mitsubishi Electric Corp.

- Oracle Corp.

- PTC Inc.

- Robert Bosch GmbH

- Rockwell Automation Inc.

- SAP SE

- Schneider Electric SE

- Siemens AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Industrial digital twin for heavy industries market

- In May 2025, Emerson Electric integrated generative artificial intelligence agents into its DeltaV automation system to assist engineers in interpreting complex digital twin simulations of chemical processing plants.

- In August 2025, SAP introduced a specialized digital thread synchronization tool for the heavy equipment manufacturing sector, enabling automated tracking of the carbon footprint of individual components.

- In October 2025, Bentley Systems launched an immersive three-dimensional visualization extension for its iTwin platform, allowing stakeholders to conduct remote design reviews of industrial facilities using augmented reality headsets.

- In February 2025, Schneider Electric collaborated with a global telecommunications leader to launch a dedicated 5G-enabled digital twin platform for heavy industrial applications, focusing on seamless sensor integration.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Industrial Digital Twin For Heavy Industries Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 310 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 18.2% |

| Market growth 2026-2030 | USD 2839.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 16.2% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Qatar, Nigeria, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The industrial digital twin market for heavy industries is maturing from a conceptual framework to a core operational tool, built on high-fidelity virtual replica technology and physics-based simulation. The integration of the industrial internet of things (iiot) with edge computing hardware is foundational, enabling real-time data synchronization and remote expert assistance in creating autonomous industrial environments.

- A key boardroom-level consideration is how digital thread integration supports ESG compliance through circular economy tracking and digital product passports. Tools like generative design algorithms and machine learning algorithms are automating asset lifecycle optimization and creating sophisticated predictive maintenance models. This technology facilitates virtual commissioning and blast furnace optimization, with some deployments achieving a 30% reduction in commissioning time.

- The ecosystem relies on high-precision sensors and emerging 5g-enabled digital platforms, alongside augmented reality headsets for industrial metaverse environments. Success hinges on integrating data from plm and erp systems, navigating cybersecurity vulnerabilities in converged ot and it landscapes, and establishing robust data interoperability standards for subsea wellhead monitoring and other critical applications.

What are the Key Data Covered in this Industrial Digital Twin For Heavy Industries Market Research and Growth Report?

-

What is the expected growth of the Industrial Digital Twin For Heavy Industries Market between 2026 and 2030?

-

USD 2.84 billion, at a CAGR of 18.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Software, Services, and Hardware), Deployment (Cloud, On-premises, and Hybrid), Sector (Downstream, Upstream, and Midstream) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Optimization of asset lifecycle and predictive maintenance, High initial capital expenditure and technical integration complexity

-

-

Who are the major players in the Industrial Digital Twin For Heavy Industries Market?

-

ABB Ltd., Altair Engineering Inc., Amazon.com Inc., ANSYS Inc., Bentley Systems Inc., Dassault Systemes SE, Emerson Electric Co., General Electric Co., Hexagon AB, Honeywell International Inc., IBM Corp., Microsoft Corp., Mitsubishi Electric Corp., Oracle Corp., PTC Inc., Robert Bosch GmbH, Rockwell Automation Inc., SAP SE, Schneider Electric SE and Siemens AG

-

Market Research Insights

- Market dynamics are shaped by the pursuit of remote operational intelligence and superior asset performance management (apm). The shift toward predictive and prescriptive analytics is central, with implementations showing up to a 40% reduction in unplanned downtime compared to traditional maintenance schedules.

- Sustainable manufacturing solutions, driven by regulations, are another key factor, as energy consumption modeling helps firms meet carbon footprint reporting goals. Effective manufacturing process optimization through heavy machinery simulation can improve production throughput by over 15%. This creates a strong business case for adoption despite challenges in legacy system integration.

- The ability to achieve enhanced supply chain visibility enhancement provides a significant competitive advantage, connecting factory floor data collection with enterprise-level strategic planning for a more resilient operational framework.

We can help! Our analysts can customize this industrial digital twin for heavy industries market research report to meet your requirements.

RIA -

RIA -