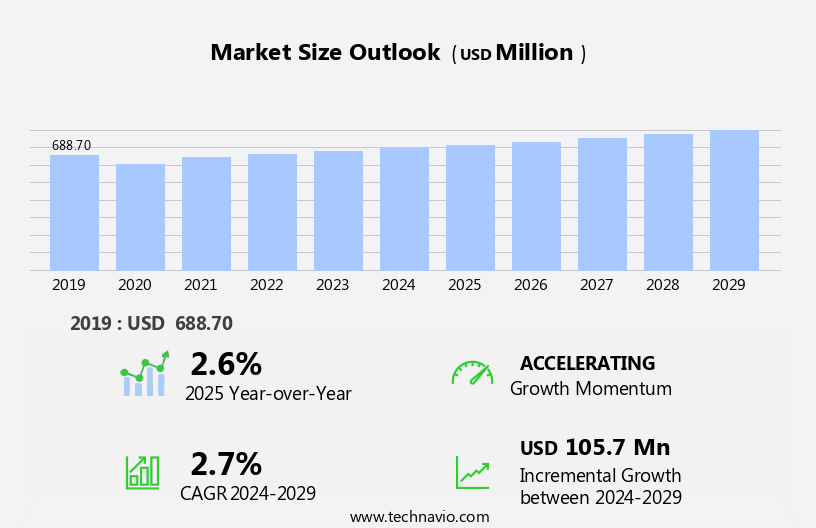

Industrial Gear Oil Market Size 2025-2029

The industrial gear oil market size is forecast to increase by USD 105.7 million at a CAGR of 2.7% between 2024 and 2029.

- The market is experiencing significant growth driven by the increasing automation of industrial processes and the expanding range of industry-specific gear oil products. Automation in various industries, including manufacturing, power generation, and transportation, is leading to a higher demand for reliable and efficient gear oils to ensure smooth operations. Furthermore, the development of specialized gear oils catering to specific industry needs is fueling market expansion. However, the market is not without challenges. The volatility in raw material prices, particularly for base oils and additives, poses a significant threat to market growth. Producers must navigate these price fluctuations to maintain profitability and competitiveness. Predictive maintenance and condition monitoring through oil analysis help prevent unexpected downtime, ensuring a consistent production schedule.

- Companies seeking to capitalize on market opportunities should focus on innovation, product differentiation, and cost management to stay ahead of the competition. Additionally, strategic partnerships and collaborations can help mitigate the impact of raw material price volatility and expand market reach. Overall, the market presents a compelling opportunity for growth, with automation trends and industry-specific product development driving demand. However, companies must navigate raw material price volatility to remain competitive and profitable.

What will be the Size of the Industrial Gear Oil Market during the forecast period?

- The market in the United States is experiencing significant activity and growth, driven by various factors. These include the increasing demand for tooth surface protection to ensure gear durability and improve equipment efficiency. Industry standards and regulations mandate regular oil changes and maintenance schedules, leading to a focus on low-temperature pumpability and high-temperature stability. Lubrication engineering advances, such as energy efficiency, contaminant control, and responsible sourcing, are also key factors. Additionally, trends toward oil management systems, fatigue resistance, and temperature performance are shaping the market. Other emerging trends include the adoption of predictive analytics for lubrication intervals, digital twin technology for remote diagnostics, and the use of low-emission lubricants and bio-based additives for sustainability.

- The market is further influenced by the importance of regulatory compliance, cost-benefit analysis, and power loss reduction. Gear efficiency, gear wear, sensor technologies, and remote diagnostics are also critical considerations. Overall, the market is evolving to meet the demands of industry for advanced gear oil formulations that enhance equipment performance and reduce operating costs.

How is this Industrial Gear Oil Industry segmented?

The industrial gear oil industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

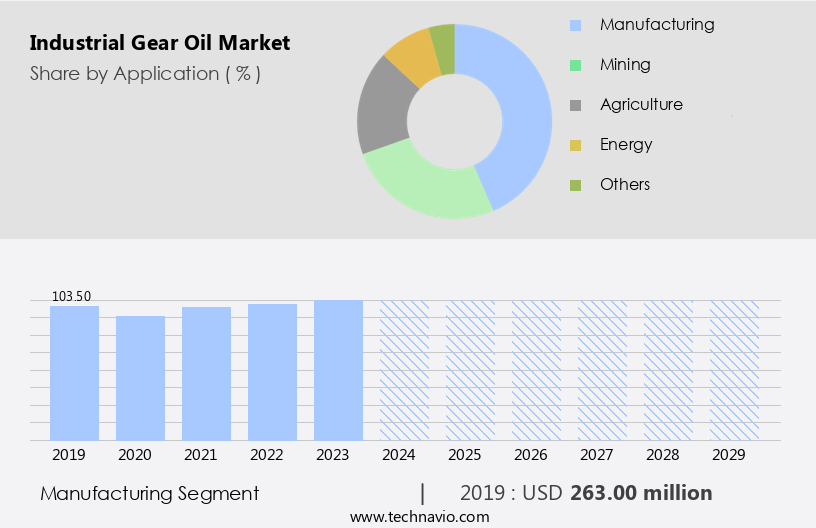

- Application

- Manufacturing

- Mining

- Agriculture

- Energy

- Others

- Product

- Mineral

- Synthetic

- Semi-synthetic

- Bio-based

- Variant

- ISO VG 320

- ISO VG 220

- ISO VG 460

- Others

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- India

- Japan

- Europe

- France

- Germany

- UK

- South America

- Brazil

- Middle East and Africa

- North America

By Application Insights

The manufacturing segment is estimated to witness significant growth during the forecast period. Gear oil plays a crucial role in manufacturing by lubricating the gears in machinery such as lathes, drill presses, and milling machines. This oil's ability to draw heat away from the gears reduces friction between them, preventing the gears from overheating and extending their lifespan. Industrial gear oil is specifically designed for heavy-duty enclosed gear drives with splash and circulation systems, as well as for plain bearings, sliding surfaces, and chain drives that experience significant shock loads. The temperature limit for the application of industrial gear oil is 100 degrees Celsius. Machinery efficiency is a top priority in the manufacturing sector, and the use of industrial gear oil contributes to this goal.

Hydraulic systems, marine gears, and industrial gearboxes all benefit from the oxidation resistance and load-carrying capacity of industrial gear oil. Furthermore, the adoption of sustainable lubricants derived from renewable resources aligns with the industry's focus on energy conservation and environmental friendliness. Supply chain management and customer service are essential aspects of any business, and the use of industrial gear oil can impact both. Additionally, the use of biodegradable oils and synthetic gear oil contributes to a circular economy by reducing waste and improving lubrication performance.

The manufacturing sector's complex machinery requires effective lubrication management. Life cycle analysis and lubrication optimization are critical components of this process. Gear lubrication, viscosity index, and thermal stability are essential factors in ensuring machinery runs efficiently and effectively. Corrosion protection and wear prevention are also vital considerations, particularly in aerospace applications, mining equipment, and heavy-duty equipment. Data analytics and performance testing are essential tools for assessing the effectiveness of industrial gear oil. These methods provide valuable insights into the oil's condition and performance, enabling proactive maintenance and optimization. Remote monitoring and field trials offer additional benefits by allowing for real-time monitoring and adjustments to optimize lubrication and improve machinery efficiency.

Industrial gear oil plays a vital role in the manufacturing sector by lubricating gears, reducing friction, and extending the lifespan of machinery. Its use contributes to machinery efficiency, sustainability, and predictive maintenance. The industry's focus on supply chain management, customer service, and performance optimization drives the adoption of advanced lubrication technologies and sustainable lubricants.

Get a glance at the market report of share of various segments Request Free Sample

The Manufacturing segment was valued at USD 263.00 million in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

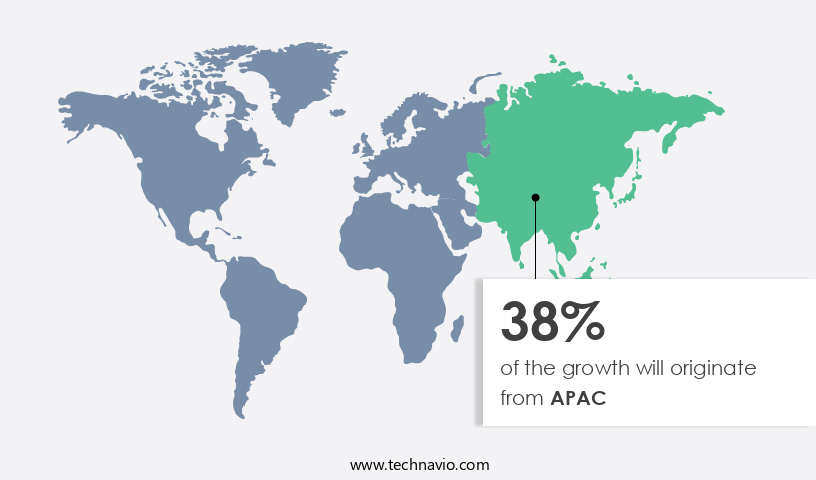

APAC is estimated to contribute 38% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

In North America, the US contributes significantly to the regional market's revenue growth. Previously, major US companies outsourced their manufacturing to Asia Pacific (APAC) due to lower labor costs. However, rising labor wages in APAC have compelled these companies to relocate their manufacturing plants to countries like Brazil and Mexico. This trend has resulted in an increased demand for industrial gear oil in the region. The expansion of industries such as automotive, construction, mining, and oil and gas is driving the market's growth in North America. The automotive sector's increasing demand for automobiles, coupled with the construction industry's wave in activities, is a significant factor.

Additionally, the mining industry's expansion and the rise in offshore and oil drilling activities are contributing to the market's growth. Industrial gear oil plays a crucial role in various industries, including hydraulic systems, power transmission, and machinery efficiency. Its properties, such as oxidation resistance, viscosity index, and load-carrying capacity, make it an essential component in these applications. Furthermore, the use of renewable resources in industrial gear oil production aligns with the circular economy and sustainability trends. Advancements in technology have led to the development of synthetic gear oils, sustainable lubricants, and bio-based lubricants. These innovations offer extended oil life, improved thermal stability, and enhanced wear prevention.

Additionally, predictive maintenance, condition monitoring, and oil analysis are essential practices that ensure machinery efficiency and longevity. The market is witnessing significant advancements in areas such as lubrication management, lubricant performance standards, and distribution networks. These developments enable efficient supply chain management, reduce maintenance costs, and ensure the availability of high-performance gear oils. The market in North America is experiencing strong growth due to the expanding industries, technological advancements, and the shift towards sustainable practices. The market's evolution is driven by factors such as increasing demand for automobiles, rising construction activities, expanding mining industry, and the rise of renewable resources in lubricant production.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Industrial Gear Oil Industry?

- Increase in plant automation is the key driver of the market. Industrial gear oils play a crucial role in the smooth operation of automated manufacturing systems, which are increasingly prevalent due to the global demand for superior quality products and population growth. With the continuous operation of these systems comes a higher risk of failure, leading to an increased need for 24/7 automated monitoring systems. According to research, the investment in global process automation is projected to grow at a rate of 7% by the end of 2025.

- This growth encompasses advancements in technology, hardware, software, services, and communication protocols used for automation. The increasing automation trend is expected to drive the demand for industrial gear oils, ensuring the seamless functioning of manufacturing processes around the clock.

What are the market trends shaping the Industrial Gear Oil Industry?

- An increasing number of industry-specific products is the upcoming market trend. The market is witnessing significant growth due to the increasing production of industry-specific gear oils. Two primary types of players operate in this market: those providing generic products and those manufacturing industry-specific solutions. In times, there has been a noteworthy focus among companies to cater to the unique requirements of various industries. For instance, Royal Dutch Shell and Exxon Mobil Corporation are major players in the market, offering comprehensive lubricant solutions tailored to specific industries through their respective branches.

- Exxon Mobil's Mobil Serv Engineering Services provides a complete range of plant studies and lubricant solutions. This strategic approach allows these companies to meet the evolving needs of their customers and maintain a competitive edge.

What challenges does the Industrial Gear Oil Industry face during its growth?

- Volatility in raw material prices is a key challenge affecting the industry's growth. Industrial gear oils are predominantly manufactured using raw materials derived from paraffin-based mineral oils, synthetic polyalkylene glycols, synthetic esters, and synthetic polyalphaolefins, primarily sourced from the oil and gas industry. The oil and gas sector serves as a significant contributor to the market due to its role as a primary supplier of raw materials. The volatility of crude oil prices significantly influences the cost of these raw materials and, consequently, the price of industrial gear oils. In the past few years, the unpredictable fluctuations in oil prices have compelled oil and gas industry players to adopt cost-saving strategies, such as workforce reduction and rig idling.

- As of December 2023, the price of Brent crude oil stood at USD 78 per barrel. This price instability underscores the importance of monitoring and managing raw material costs for market participants in the industrial gear oil sector.

Exclusive Customer Landscape

The industrial gear oil market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the industrial gear oil market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, industrial gear oil market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ADVANCED LUBRICATION SPECIALTIES - The company offers industrial gear oil such as Advantage AMP Gear Oils, and Advantage EP Gear Oils.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ADVANCED LUBRICATION SPECIALTIES

- AMALIE OIL CO.

- Apar Industries Ltd.

- BASF SE

- BP Plc

- Chevron Corp.

- China Petrochemical Corp.

- Croda International Plc

- Exxon Mobil Corp.

- FUCHS SE

- Gandhar Oil Refinery India Ltd.

- Hinduja Group Ltd.

- Petroleos de Venezuela SA

- Petromin Corp.

- PJSC LUKOIL

- Shell plc

- TotalEnergies SE

- Valvoline Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Industrial gear oils play a vital role in the efficient operation of various machinery and equipment across numerous industries. These specialized lubricants are designed to provide superior performance in high-load, high-stress applications, ensuring the longevity and productivity of hydraulic systems, construction machinery, marine gears, wind turbines, and other industrial gearboxes. The market for industrial gear oils is driven by several key factors. One significant trend is the increasing demand for extended oil life, which is achieved through advanced formulations that offer enhanced oxidation resistance and thermal stability. This not only reduces the frequency of oil changes but also lowers maintenance costs and downtime.

Another critical aspect of the market is the focus on product certifications and quality assurance. As industries strive for improved machinery efficiency and sustainability, there is a growing emphasis on performance testing and data analytics to ensure lubricant compatibility and optimize lubrication management. Moreover, the shift towards renewable resources and sustainable lubricants is gaining momentum. Bio-based lubricants and synthetic gear oils derived from renewable sources are increasingly being adopted to reduce the environmental impact of industrial operations. This trend is particularly prevalent in industries such as mining, aerospace, and automotive, where the use of heavy-duty equipment and large industrial gearboxes necessitates the use of high-performance lubricants.

Furthermore, predictive maintenance and condition monitoring are becoming essential components of effective lubrication management. Remote monitoring and oil analysis enable early detection of potential issues, allowing for timely maintenance and reducing the risk of unexpected downtime. In the realm of power transmission, there is a growing focus on lubrication optimization and energy conservation. Mineral gear oil and synthetic gear oil formulations with improved viscosity index and load-carrying capacity are being developed to enhance machinery efficiency and reduce energy consumption. The circular economy is also influencing the market, with a growing emphasis on life cycle analysis and the reuse and recycling of lubricants.

This not only helps to reduce waste and minimize the environmental impact of industrial operations but also lowers costs by extending the useful life of lubricants. The market is characterized by continuous innovation and a focus on enhancing machinery efficiency, reducing downtime, and minimizing environmental impact. The adoption of advanced technologies such as predictive maintenance, condition monitoring, and data analytics is driving the development of high-performance lubricants, while the shift towards renewable resources and sustainable lubricants is gaining momentum. The market is expected to remain dynamic, with ongoing research and development efforts aimed at improving lubricant performance, reducing costs, and minimizing environmental impact.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

242 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 2.7% |

|

Market growth 2025-2029 |

USD 105.7 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

2.6 |

|

Key countries |

US, China, Canada, Mexico, Brazil, India, Germany, Japan, France, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Industrial Gear Oil Market Research and Growth Report?

- CAGR of the Industrial Gear Oil industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the industrial gear oil market growth and forecasting

We can help! Our analysts can customize this industrial gear oil market research report to meet your requirements.

RIA -

RIA -