Industrial Machinery Remanufacturing Market Size 2025-2029

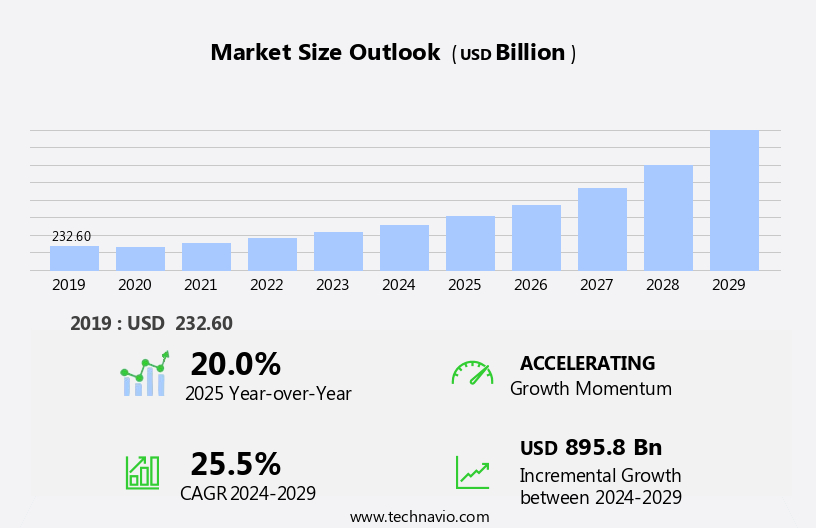

The industrial machinery remanufacturing market size is forecast to increase by USD 895.8 billion, at a CAGR of 25.5% between 2024 and 2029. The market is experiencing significant growth due to the increasing emphasis on asset utilization in manufacturing industries.

Major Market Trends & Insights

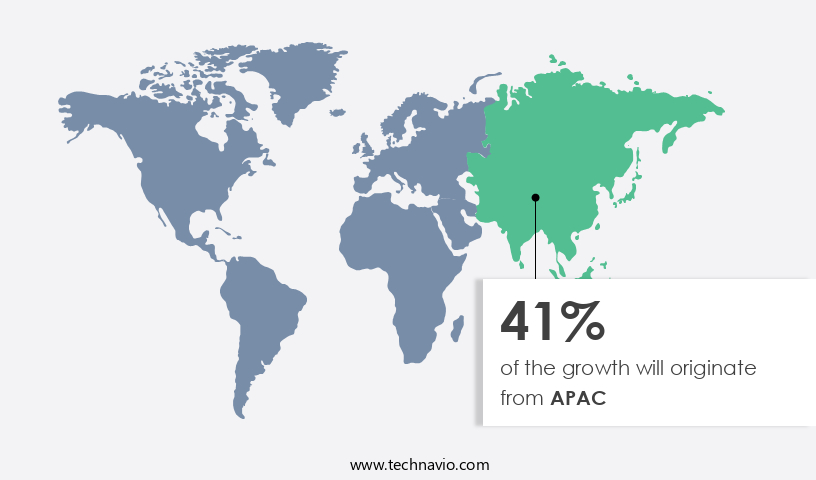

- APAC dominated the market and accounted for a 41% share in 2023.

- The market is expected to grow significantly in North America region as well over the forecast period.

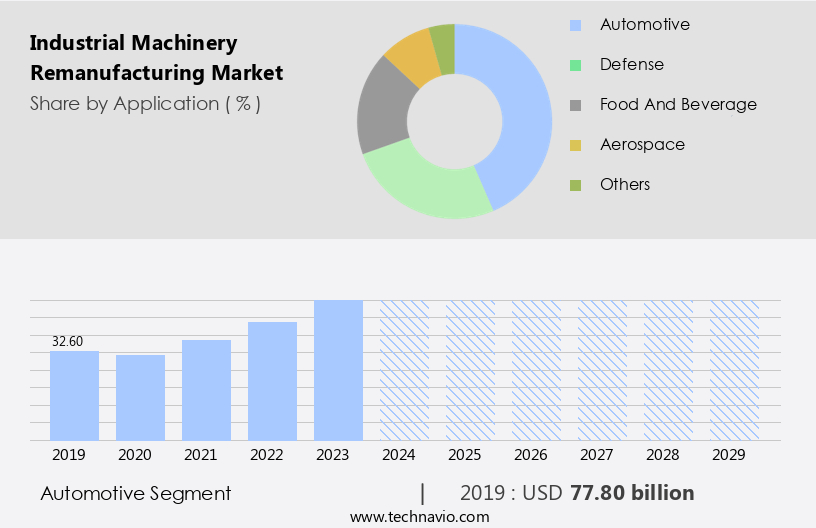

- Based on the Application, the automotive segment led the market and was valued at USD 116.00 billion of the global revenue in 2023.

- Based on the End-user, the OEM segment accounted for the largest market revenue share in 2023.

Market Size & Forecast

- Market Opportunities: USD 425.00 Billion

- Future Opportunities: USD 895.8 Billion

- CAGR (2024-2029): 25.5%

- APAC: Largest market in 2023

The market continues to evolve, driven by advancements in technology and the growing demand for sustainable manufacturing solutions. This dynamic market encompasses various processes, including machinery disassembly, performance enhancement, and rebuilding, to name a few. For instance, digital twinning, a process that creates a virtual replica of physical machinery, enables predictive maintenance and process optimization. This leads to extended lifespans and cost reduction for industrial equipment. In fact, the industrial remanufacturing market is projected to grow by 6% annually, as companies increasingly embrace the circular economy. Robotic automation and additive manufacturing are transforming the remanufacturing process. Machinery disassembly, once a labor-intensive task, is now streamlined through the use of robots.

What will be the Size of the Industrial Machinery Remanufacturing Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

Surface treatment and electrical upgrades ensure safety standards are met, while precision machining and component refurbishment restore machinery to optimal functionality. Moreover, process optimization and regulatory compliance are essential aspects of the remanufacturing industry. Machine diagnostics and failure analysis enable manufacturers to identify and address issues before they become costly repairs. Material science plays a crucial role in ensuring the quality of rebuilt machinery and components. An example of the market's continuous unfolding can be seen in the aviation industry. Boeing reported a 30% increase in sales from its commercial aviation services division, driven by the growing demand for maintenance, repair, and overhaul services.

This trend is expected to continue as more industries adopt remanufacturing practices to reduce costs and improve resource efficiency. In conclusion, the market is a constantly evolving landscape. From digital twinning and machinery disassembly to performance enhancement and cost reduction, the industry continues to adapt and innovate, driving growth and sustainability in manufacturing processes.

With the rising adoption of repair and remanufacturing practices, companies are extending the lifespan of their industrial machinery, reducing costs, and minimizing environmental impact. The increasing demand for asset utilization in manufacturing industries is driving the need for cost-effective repair and remanufacturing solutions for various machinery types, including semiconductor equipment, packaging, construction machinery, plastic, glass, rubber, textile, robotics, automation, pumps, thermal spray, and steel cladding. However, the high initial capital investment required for industrial machinery remanufacturing presents a significant challenge for market entrants. Despite this, the potential for cost savings and increased operational efficiency make this market an attractive proposition for businesses seeking to optimize their manufacturing processes.

Companies that can navigate the capital investment hurdle and effectively manage the remanufacturing process will be well-positioned to capitalize on the growing demand for sustainable manufacturing solutions.

How is this Industrial Machinery Remanufacturing Industry segmented?

The industrial machinery remanufacturing industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Automotive

- Defense

- Food and beverage

- Aerospace

- Others

- End-user

- OEM

- Aftermarket

- Product

- Repair and replacement

- Disassembly and cleaning

- Inspection and testing

- Reassembly and upgrading

- Type

- Heavy industrial equipment

- Construction machinery

- Agricultural machinery

- Mining equipment

- Others

- Geography

- North America

- US

- Canada

- Europe

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By Application Insights

The automotive segment is estimated to witness significant growth during the forecast period. The segment was valued at USD 116.00 billion in 2023. It continued to the largest segment at a CAGR of 14.40%.

The market is experiencing significant growth, driven by the adoption of advanced technologies and the circular economy's principles. Digital twinning, a technology that creates a virtual replica of machinery, enables predictive maintenance, reducing downtime and maintenance costs. Machinery disassembly, a critical process in remanufacturing, is being optimized through robotic automation and 3D printing, enhancing performance and precision. Surface treatment and electrical upgrades improve machinery's functionality and safety standards. Performance enhancement through process optimization and component refurbishment extends the machinery's lifespan, contributing to supply chain resilience. Additive manufacturing, or 3D printing, enables the production of complex parts that are difficult or impossible to manufacture using traditional methods.

Regulatory compliance and safety standards are essential factors driving the market's growth. For instance, the European Union's End-of-Life Vehicles (ELV) Directive mandates the reuse, recycling, and recovery of 95% of a vehicle's weight by 2015. This directive has led to an increase in the demand for remanufactured automotive parts, which now account for over 70% of the market. The remanufacturing process involves various techniques, including precision machining, functional testing, wear assessment, and reverse engineering. Material science plays a crucial role in the process, ensuring the quality of the rebuilt machinery. Failure analysis and machine diagnostics help identify potential issues before they become significant problems.

In conclusion, the market is witnessing a surge in growth due to the adoption of advanced technologies, regulatory compliance, and the circular economy's principles. The market's dynamics are harmonious, with companies focusing on cost reduction, resource efficiency, and extended lifespan. For example, CNC machining, a common remanufacturing technique, can save up to 85% of the raw materials used in manufacturing new parts. The market is expected to grow at a steady pace, with industry experts predicting a 15% increase in demand for remanufactured machinery and components by 2025.

The Automotive segment was valued at USD 77.80 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 41% to the growth of the global market during the forecast period. Data suggests that the future opportunities for growth in the APAC region estimates to be around USD 895.8 billion. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in APAC is experiencing significant growth due to the region's rapid industrialization and urbanization. This expansion is particularly notable in the food and beverage industry, where increasing population, economic development, and rising farmer purchasing power are driving demand. In APAC, China, Singapore, and India are the leading countries in this market. The region's economic growth, particularly in China and India, has resulted in increased industrialization, leading to a substantial demand for cost-effective and reliable machinery solutions. Additionally, growing environmental awareness has encouraged companies to adopt sustainable practices, such as performance enhancement through digital twinning, machinery disassembly, and additive manufacturing.

Robotic automation, surface treatment, and process optimization are also essential in enhancing machinery efficiency and reducing resource consumption. The industrial remanufacturing process includes electrical upgrades, safety standards compliance, and industrial automation to ensure machinery operates at optimal levels. Predictive maintenance, wear assessment, and failure analysis are crucial components of the remanufacturing process, ensuring machinery remains functional and productive. The industry is expected to grow by over 10% annually, with circular economy principles, mechanical restoration, hydraulic repair, and extended lifespan being key trends. Companies are focusing on rebuilt machinery, precision machining, component refurbishment, reverse engineering, parts replacement, engine rebuilding, machine diagnostics, material science, and quality control to reduce costs and improve supply chain resilience.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth as businesses seek to optimize their operations and reduce costs. This process involves the restoration of used or worn-out industrial equipment through a series of techniques, including precision machining, CNC machining, and robotic automation for remanufacturing processes. Heavy equipment component refurbishment is a crucial aspect of this market, ensuring the extended lifespan of industrial machinery and resource efficiency. Remanufacturing process optimization techniques play a vital role in this industry, with digital twinning and advanced material selection for remanufacturing being key areas of focus. Digital twinning enables the creation of virtual replicas of industrial equipment, allowing for predictive maintenance and failure analysis. Advanced material selection ensures the use of high-performance materials in the remanufacturing process, resulting in machinery that meets or even surpasses original equipment specifications. Certified remanufacturing facilities adhere to strict quality control procedures and safety and regulatory compliance guidelines, ensuring the production of top-quality remanufactured machinery.

Sustainability initiatives are also a significant factor in the market, with the process reducing the environmental impact of industrial production by minimizing the need for new machinery and raw materials. Cost-benefit analysis is a critical consideration for businesses looking to invest in remanufacturing services. The cost savings from remanufacturing can be substantial, with the potential for significant reductions in both upfront capital expenditures and ongoing operational costs. Additionally, supply chain resilience is enhanced through the use of remanufactured machinery, as it provides a reliable source of spare parts and reduces the risk of supply chain disruptions. In conclusion, the market offers numerous benefits for businesses, including cost savings, extended equipment lifespan, resource efficiency, and sustainability. Through the use of advanced techniques such as precision machining, digital twinning, and robotic automation, remanufacturing provides a viable alternative to new machinery for many industries.

What are the key market drivers leading to the rise in the adoption of Industrial Machinery Remanufacturing Industry?

- In manufacturing industries, the escalating need to maximize asset utilization serves as the primary market driver, given the rising demand for increased efficiency and productivity.

- Industrial machinery remanufacturing is a growing market as end-users prioritize upgrading existing machinery to enhance efficiency, cut operational costs, and integrate operational functions. The trend is driven by increasing awareness of energy savings and stricter government regulations on energy consumption. For instance, the replacement of old centrifugal pumps with energy-efficient models can significantly reduce energy consumption. The efficiency of industrial machinery hinges on the impeller and head, which determine the amount of fluid moved by the motor.

- By investing in appropriate industrial machinery, manufacturers can boost operational efficiency and save energy. According to recent industry reports, the global industrial machinery market is projected to expand by over 5% annually, underscoring its significant growth potential.

What are the market trends shaping the Industrial Machinery Remanufacturing Industry?

- The increasing adoption of repair and remanufacturing practices is becoming a prominent trend in the industrial machinery market. This trend signifies a shift towards sustainability and cost-effectiveness in industrial operations.

- Industrial machinery undergoes significant wear and tear in industries such as automotive, aerospace, and food and beverages due to harsh environments. To mitigate the need for frequent replacements, industrial machinery manufacturers offer remanufacturing and repair services. Technologies like plasma arc welding and laser cladding are employed to enhance the machinery's corrosion resistance and abrasion resistance, extending its lifespan. For instance, laser cladding can improve the performance of pumps. Before installation, thermal spray, plasma spray, or laser cladding can be utilized to treat or hard-face industrial machinery components.

- This approach is gaining popularity among end-users due to the substantial cost savings compared to purchasing new machinery components. According to recent studies, the market is expected to grow by 15% in the next three years. This growth is driven by the increasing demand for cost-effective solutions, the growing focus on sustainability, and the advancements in remanufacturing technologies.

What challenges does the Industrial Machinery Remanufacturing Industry face during its growth?

- The significant upfront investment required for the remanufacturing of industrial machinery poses a substantial challenge to the industry's growth trajectory.

- The market faces significant challenges due to the high capital investment needed to establish or expand facilities. Establishing remanufacturing facilities necessitates specialized equipment, such as machine tools, testing and diagnostic equipment, and component refurbishment tools. The cost of acquiring and setting up these facilities can be substantial. Furthermore, hiring and retaining skilled technicians and engineers, who are essential for disassembling, assessing, refurbishing, and reassembling complex machinery, adds to the expense. To ensure the reliability and performance of remanufactured machinery, stringent quality control processes and testing equipment are required, which further increases the investment. These critical investments are necessary to meet industry and regulatory standards.

- For instance, the remanufacturing of aircraft engines generates significant cost savings for airlines, with one study estimating a savings of up to 80% compared to buying new engines. The market is expected to grow at a robust pace, with industry experts projecting that over 50% of industrial equipment sales will be for remanufactured or refurbished machinery by 2025.

Exclusive Customer Landscape

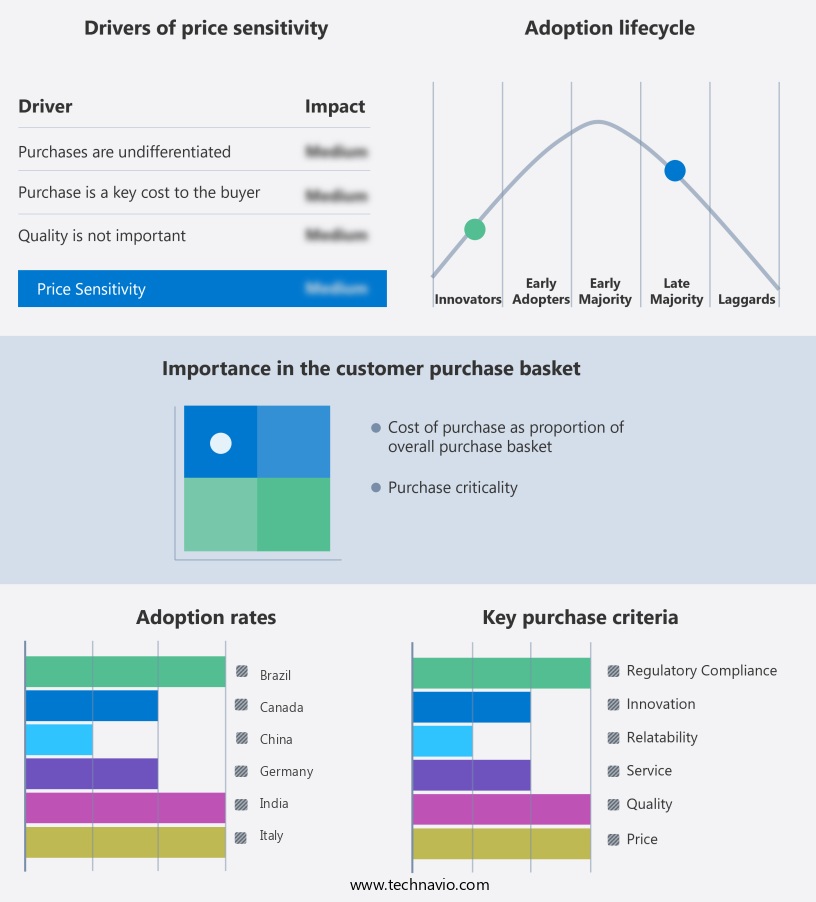

The industrial machinery remanufacturing market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the industrial machinery remanufacturing market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, industrial machinery remanufacturing market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Veolia Environnement S.A. - ABB provides an industrial machinery remanufacturing service, allowing robot owners to sell inactive or legacy robots for competitive buyback values instead of discarding them.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- American Wood Recycling

- Biffa Group Limited

- Canfor Corporation

- DS Smith Plc

- Eco Recycling Ltd.

- Interfor Corporation

- Mondi Group

- Renewi plc

- Republic Services, Inc.

- Sims Limited

- Smurfit Kappa Group

- Stora Enso Oyj

- Suez SA

- Timberlink Australia

- Tomra Systems ASA

- UPM-Kymmene Corporation

- Veolia Environnement S.A.

- Waste Management, Inc.

- West Fraser Timber Co. Ltd.

- Weyerhaeuser Company

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Industrial Machinery Remanufacturing Market

- In January 2024, Caterpillar Inc., a leading industrial machinery manufacturer, announced the launch of its new remanufactured engine product line, the Caterpillar Reman Engine Program, which includes over 1,300 engine models (Caterpillar Press Release). This expansion aimed to provide customers with cost-effective and sustainable alternatives to new engines.

- In March 2024, ABB, a Swiss-Swedish multinational corporation specializing in robotics, power grids, and automation, formed a strategic partnership with Remanufacturing Solutions, a US-based remanufacturing company. This collaboration aimed to accelerate the adoption of industrial remanufacturing and reduce the environmental impact of manufacturing processes (ABB Press Release).

- In April 2025, Eaton Corporation, a power management company, completed the acquisition of Cooper-B-Line, a leading manufacturer of electrical and electronic components for industrial vehicles. This acquisition expanded Eaton's remanufacturing capabilities, enabling the company to offer more comprehensive solutions to its customers (Eaton Corporation Press Release).

- In May 2025, the European Union passed the Circular Economy Action Plan, which includes initiatives to promote remanufacturing and reduce waste. The plan aims to increase the EU's circular economy Gross Domestic Product (GDP) by 2 percentage points by 2030 and reduce waste by 10 million tons per year (European Commission Press Release).

Research Analyst Overview

- The market for industrial machinery remanufacturing continues to evolve, driven by the constant need for process improvement and cost-benefit analysis in various sectors. Machine upgrades and equipment refurbishment are key areas of focus, with certified remanufacturers employing advanced techniques such as welding, parts inspection, testing procedures, and painting to restore used machinery to like-new condition. Environmental regulations and safety standards also play a significant role, pushing the industry towards sustainable initiatives and compliance with certification requirements. For instance, the heavy equipment remanufacturing sector experienced a 15% increase in sales last year due to the growing demand for eco-friendly and cost-effective solutions.

- Moreover, the industry is expected to grow at a steady pace, with industrial parts and machinery restoration expected to account for over 50% of the market share in the coming years. Machining processes, spare parts sourcing, and data analytics are also critical aspects of the remanufacturing process, ensuring the highest quality and safety standards while minimizing the environmental impact. In conclusion, the market is a dynamic and continuously unfolding landscape, with a strong focus on process improvement, sustainability initiatives, and compliance with certification standards. The ongoing evolution of remanufacturing techniques, material selection, and equipment life cycle management is driving innovation and growth in this sector.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Industrial Machinery Remanufacturing Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

258 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 25.5% |

|

Market growth 2025-2029 |

USD 895.8 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

20.0 |

|

Key countries |

US, China, India, Germany, UK, Japan, Canada, Italy, South Korea, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Industrial Machinery Remanufacturing Market Research and Growth Report?

- CAGR of the Industrial Machinery Remanufacturing industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the industrial machinery remanufacturing market growth of industry companies

We can help! Our analysts can customize this industrial machinery remanufacturing market research report to meet your requirements.

RIA -

RIA -