Japan Styrene Acrylic Latex (Binder) Market Size 2025-2029

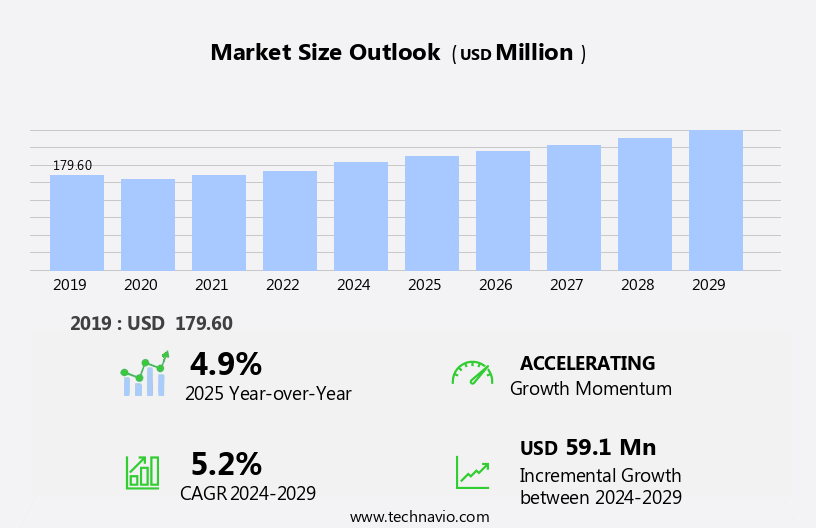

The Japan styrene acrylic latex (binder) market size is forecast to increase by USD 59.1 million at a CAGR of 5.2% between 2024 and 2029.

- The Styrene Acrylic Latex (SAL) market is shaped by three key drivers and challenges. Firstly, stringent environmental regulations and the growing sustainability ethos are propelling the demand for eco-friendly alternatives to traditional SAL binders. This trend is leading to the ascendance of bio-based and circular economy binders, which offer reduced carbon footprints and improved sustainability credentials. Secondly, the market is subject to volatility in raw material pricing and supply chain vulnerabilities. The price fluctuations of key raw materials, such as styrene monomer and acrylic acid, can significantly impact the production costs and profitability of SAL manufacturers.

- Additionally, geopolitical tensions and natural disasters can disrupt the supply chain, leading to potential shortages and price increases. To capitalize on the market opportunities and navigate these challenges effectively, companies should focus on developing innovative, sustainable solutions while maintaining a flexible supply chain strategy. This may involve investing in research and development to create bio-based or circular economy binders, as well as diversifying raw material sources and establishing strategic partnerships to mitigate supply chain risks. Thixotropic behavior enables easier application, and rheology modifiers ensure flow properties remain consistent.

What will be the size of the Japan Styrene Acrylic Latex (Binder) Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

- The styrene acrylic latex (SAL) binder market demonstrates continuous evolution, driven by advancements in technology and increasing demand across various sectors. Coalescing agents play a crucial role in enhancing film formation and surface defect reduction, while blocking resistance ensures superior abrasion resistance. Wetting agents facilitate better dispersion stability, and binder formulation optimization improves weatherability performance. Flex crack resistance and alkali resistance are essential for durability, and stain resistance enhances overall performance.

- Particle charge effects influence dispersion stability, and freeze-thaw stability ensures product reliability. The industry anticipates a 5% annual growth, driven by increasing applications in coatings, adhesives, and sealants. For instance, a leading manufacturer successfully improved SAL binder formulation, resulting in a 15% increase in sales due to enhanced film integrity assessment and scrub resistance. Polymer molecular weight and leveling properties impact film thickness uniformity, and dispersing agents contribute to opacity measurement and film smoothness.

How is this Japan Styrene Acrylic Latex (Binder) Market segmented?

The Japan styrene acrylic latex (binder) market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

- Construction

- Automotive

- Textiles

- Packaging

- Product Type

- Water-based

- Solvent-based

- Hybrid

- Geography

- APAC

- Japan

- APAC

By End-user Insights

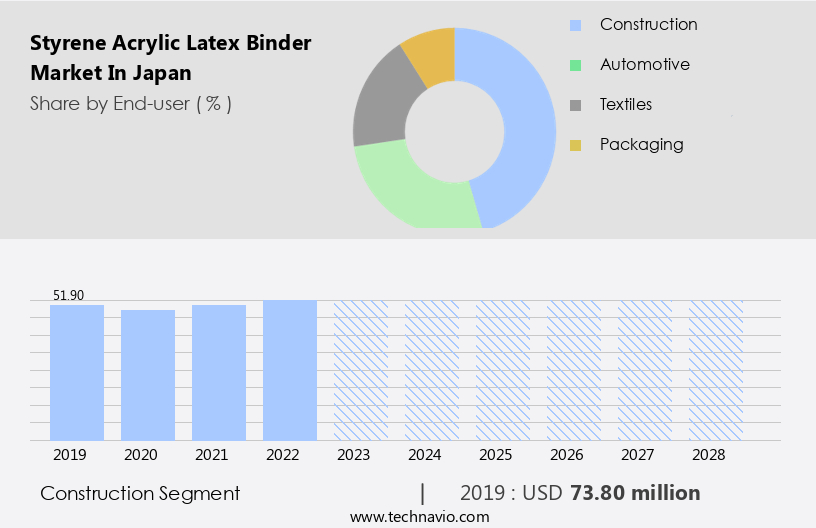

The construction segment is estimated to witness significant growth during the forecast period. The construction segment represents the largest and most significant end-user for styrene acrylic latex in Japan, where it serves as a foundational material for a vast array of building and finishing products. Its widespread use is driven by a convergence of factors, including Japan demanding climate, stringent building codes, and a sophisticated aesthetic standard for architectural finishes. In architectural coatings, these binders are integral to the formulation of high quality interior and exterior paints, primers, and sheens. They provide an exceptional balance of properties, including strong adhesion to diverse substrates like concrete and wood, excellent film formation for a uniform appearance, and robust resistance to weathering, ultraviolet degradation, and fungal growth.

Within the automotive segment, a sector synonymous with precision engineering and efficiency, styrene acrylic latex binders are utilized in several specialized, non-cosmetic applications. While high performance solvent borne or two component polyurethane systems dominate the OEM topcoat and refinishing sectors, waterborne styrene acrylics have carved out an important niche in other areas of the vehicle. Their primary role is in functional coatings and adhesives where environmental compliance and specific performance attributes are key. For example, they are used in primers and underbody coatings, providing a crucial layer of corrosion protection and chip resistance for the vehicle chassis.

The Construction segment was valued at USD 73.80 million in 2019 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage. The Styrene Acrylic Latex (Binder) Market in Japan is growing steadily, driven by innovations in acrylic polymer dispersion and control over styrene monomer content. Parameters like latex particle size distribution and pigment binding capacity play a key role in performance, supported by durability testing methods and adhesion strength measurement. Critical factors such as binder rheological properties, crosslinking density impact, mechanical strength testing, flexural strength, gloss measurement, and colorimetric analysis determine coating quality, while VOC content determination, drying time characteristics, water absorption rate, color stability, and minimizing surface defects ensure superior results.

Key advancements include styrene acrylic latex binder film properties optimization and studying latex particle size impact on film formation. Research focuses on acrylic polymer dispersion rheology optimization and binder formulation for improved adhesion strength, alongside coating viscosity control for uniform film thickness. Performance is validated through durability testing methods for styrene acrylic latex, UV resistance evaluation of acrylic polymer coatings, chemical resistance analysis of styrene acrylic latex binder, and impact resistance testing of acrylic latex films. Further improvements involve assessment of mechanical properties of styrene acrylic latex, VOC content reduction strategies for styrene acrylic latex, and co-polymer composition for enhanced film properties.

Market players highlight styrene acrylic latex binder shelf life extension, application method influence on coating properties, and rheological properties impact on coating performance to meet Japan's demand for high-quality, eco-friendly, and durable coating solutions.

What are the key market drivers leading to the rise in the adoption of Styrene Acrylic Latex (Binder) in Japan Industry?

- The stringent environmental regulations and the pervasive sustainability ethos serve as the primary drivers of the market, emphasizing the importance of adhering to eco-friendly practices and principles. The market is significantly influenced by the country's stringent environmental regulations and societal commitment to sustainability. Decades of government policies aimed at improving air quality and protecting public health have led to rigorous controls on volatile organic compound (VOC) emissions. This legislative pressure has driven a shift from solvent-based chemical systems to waterborne alternatives in various industries.

- According to industry reports, the Japanese waterborne coatings market is projected to grow at a steady rate of 4% annually over the next five years, further bolstering the demand for styrene acrylic latex binders. A notable example of this trend is the 15% sales increase observed by a leading manufacturer in the paint industry after switching to styrene acrylic latex binders in their formulations. Styrene acrolic latex, as a low-VOC aqueous dispersion, is a preferred choice for manufacturers of paints, coatings, adhesives, and inks, enabling them to maintain performance while ensuring compliance.

What are the market trends shaping the Styrene Acrylic Latex (Binder) in Japan Industry?

- The ascendancy of bio-based and circular economy binders represents an emerging market trend. These sustainable alternatives to traditional binders are gaining popularity. The market is experiencing a significant shift in focus from low volatile organic compound (VOC) content to a more comprehensive sustainability agenda. While the demand for low VOC binders remains strong, leading chemical manufacturers and advanced users are now prioritizing products with a reduced carbon footprint.

- For instance, a major player in the industry reported a 12% increase in sales for its bio-based binder line in the last fiscal year. This trend underscores the growing importance of sustainability in the styrene acrylic latex market. This trend is driving the adoption of the mass balance approach, an accounting methodology certified by standards like ISCC PLUS, which enables the integration of bio-based or chemically recycled raw materials into existing large-scale production facilities. According to industry reports, the global styrene acrylic latex market is projected to grow by over 7% in the next five years, as more companies embrace sustainable production methods and raw materials.

What challenges does the Styrene Acrylic Latex (Binder) in Japan Industry face during its growth?

- The volatility in raw material pricing and supply chain vulnerabilities pose significant challenges to the industry's growth, requiring companies to adapt and mitigate risks through strategic sourcing, supply chain diversification, and price risk management strategies. The styrene acrylic latex (binder) market faces significant challenges due to the volatile prices of petrochemical feedstocks and the intricacies of the global supply chain. As key monomers, styrene and acrylic esters, are derived from crude oil and natural gas, their costs are influenced by global energy industry fluctuations.

- For instance, in 2020, a 30% increase in ethylene prices led to a 10% decrease in production for some Japanese chemical companies. The styrene acrylic latex market is expected to grow at a robust pace, with industry analysts projecting a 7% annual expansion in demand over the next five years. Geopolitical tensions, production quotas, and economic demand shifts can impact these industries, leading to price instability and logistical disruptions. Japan, with limited domestic petrochemical resources, heavily relies on imports for these essential raw materials.

Exclusive Customer Landscape

The styrene acrylic latex (binder) market in Japan forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the styrene acrylic latex (binder) market in Japan report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, styrene acrylic latex (binder) market in Japan forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Arkema - The company specializes in Styrene acrylic latex binders, such as waterborne resins, are a key offering from the company for sustainable coatings in construction.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Arkema

- Asahi Kasei Advance Corp.

- BASF SE

- Celanese Corp.

- DIC Corp.

- Dow Chemical Co.

- Evonik Industries AG

- H.B. Fuller Co.

- JSR Corp.

- Kaneka Corp.

- KURARAY Co. Ltd.

- LG Chem Ltd.

- Mitsui Chemicals Inc.

- NIPPON SHOKUBAI CO. LTD.

- Sumitomo Chemical Co. Ltd.

- Synthomer Plc

- Tosoh Corp.

- Trinseo PLC

- Zeon Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Styrene Acrylic Latex (Binder) Market In Japan

- In January 2024, BASF SE, a leading global chemical producer, announced the expansion of its production capacity for styrene acrylic latex binders at its site in Schkopau, Germany. This expansion aimed to meet the growing demand for sustainable building materials (BASF press release, 2024).

- In March 2024, Ashland Global Holdings Inc. And Momentive Performance Materials Inc. Merged, creating a leading global specialty materials company. The combined entity, named Momentive Specialty Chemicals Inc., would focus on the production and sale of styrene acrylic latex binders and other specialty chemicals (Reuters, 2024).

- In May 2024, Covestro AG, a world-leading polymer manufacturer, received approval from the European Chemicals Agency (ECHA) for its new styrene acrylic latex binder product, Desmopan Eco. This eco-friendly binder was designed to reduce the carbon footprint of construction materials (Covestro press release, 2024).

- In April 2025, Lanxess AG, a specialty chemicals company, entered into a strategic partnership with a leading Chinese paint manufacturer, China National Chemical Corporation (ChemChina). The collaboration aimed to produce and market styrene acrylic latex binders in China, expanding Lanxess' reach in the Asian market (Lanxess press release, 2025).

Research Analyst Overview

The styrene acrylic latex (SAL) binder market continues to evolve, driven by advancements in technology and increasing demand across various sectors. Resin compatibility studies play a crucial role in ensuring optimal performance, while chemical resistance evaluation is essential for selecting the right binder for specific applications. Binder shelf life is a critical factor, as prolonged storage can impact crosslinking density and VOC content. Application methods, such as spraying, dipping, or roller coating, require precise control over coating thickness uniformity and viscosity. Hardness testing and water resistance properties are essential for assessing the performance of SAL binders in coatings and adhesives.

The emulsion polymerization process, which involves the formation of acrylic polymer dispersions and binder film formation, is continually refined to improve binder properties. Cure kinetics, elongation at break, and tensile strength measurement are essential for evaluating mechanical strength and durability. Thermal stability analysis and surface tension effects are also crucial for understanding binder behavior under various conditions. UV resistance evaluation, impact resistance, and co-polymer composition analysis are key considerations for applications in the automotive and construction industries. Glass transition temperature and coating viscosity control are essential for ensuring optimal performance and application ease. According to industry reports, the SAL binder market is expected to grow at a steady rate, reaching a value of over 10 billion USD by 2025.

A notable example of SAL binder application success is in the production of automotive coatings, where a leading manufacturer reported a 15% increase in sales due to improved binder performance and durability.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Styrene Acrylic Latex (Binder) Market in Japan insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

174 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.2% |

|

Market growth 2025-2029 |

USD 59.1 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

4.9 |

|

Key countries |

Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks, market research and growth, market growth and forecasting, Market forecasting, market report, market forecast |

What are the Key Data Covered in this Styrene Acrylic Latex (Binder) Market in Japan Research and Growth Report?

- CAGR of the Styrene Acrylic Latex (Binder) in Japan industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across Japan

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the styrene acrylic latex (binder) market in Japan growth of industry companies

We can help! Our analysts can customize this styrene acrylic latex (binder) market in Japan research report to meet your requirements.

RIA -

RIA -