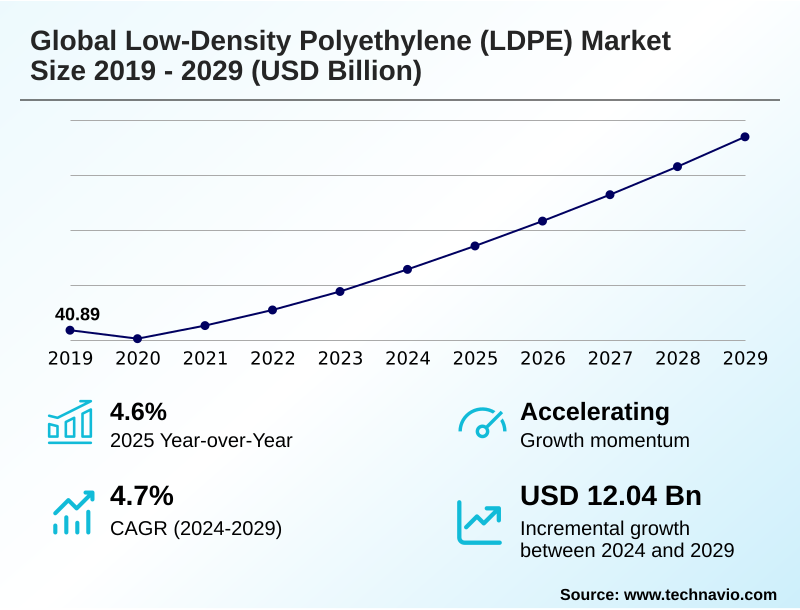

Low-density Polyethylene (LDPE) Market Size 2025-2029

The low-density polyethylene (ldpe) market size is valued to increase by USD 12.04 billion, at a CAGR of 4.7% from 2024 to 2029. Robust demand from expanding flexible packaging sector will drive the low-density polyethylene (ldpe) market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 50.4% growth during the forecast period.

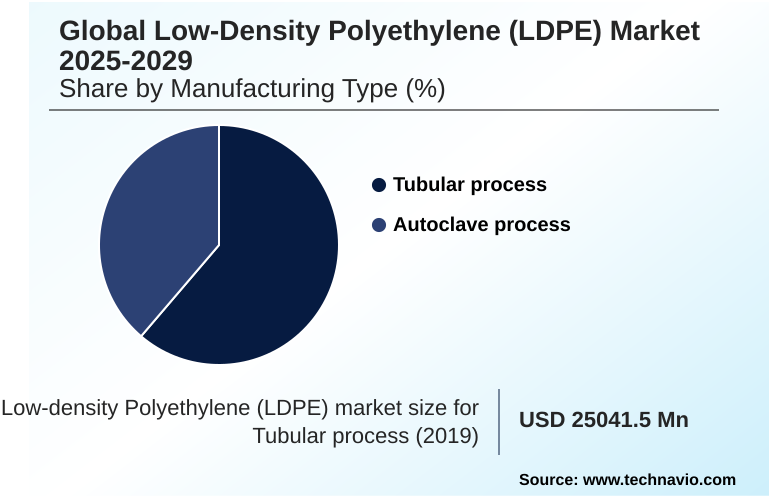

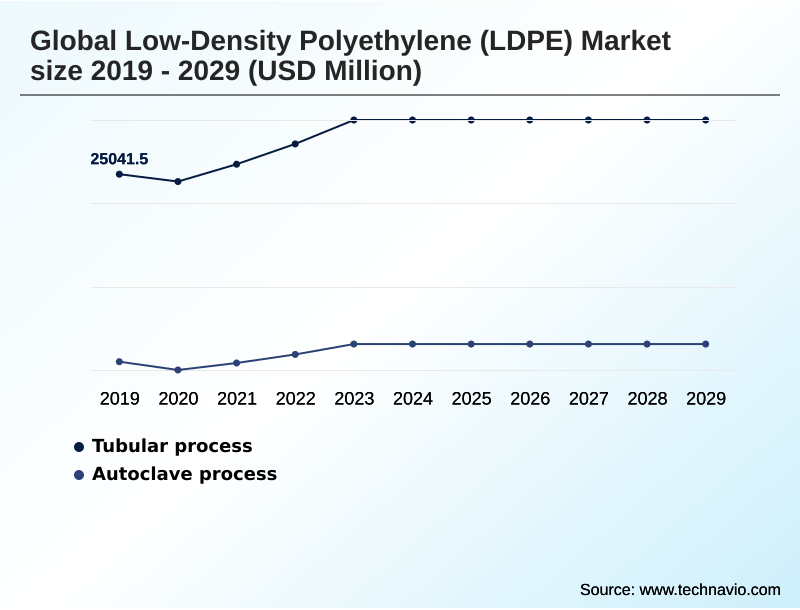

- By Manufacturing Type - Tubular process segment was valued at USD 27.70 billion in 2023

- By Application - Packaging segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 17.58 billion

- Market Future Opportunities: USD 12.04 billion

- CAGR from 2024 to 2029 : 4.7%

Market Summary

- The low-density polyethylene (LDPE) market remains integral to the global economy, anchored by its versatile applications across multiple industries. As a key thermoplastic polymer within the polyolefin family, its unique molecular structure, achieved through high-pressure polymerization, imparts essential properties like flexibility, moisture resistance, and chemical inertness.

- These attributes sustain its dominance in film and sheet manufacturing for the packaging sector and in specialized applications such as wire and cable insulation.

- The industry is currently navigating a significant transformation driven by the principles of a circular economy, which is compelling innovation in advanced recycling technologies like the pyrolysis process and the development of bio-based LDPE from renewable sources. However, the market also contends with challenges from substitute materials like LLDPE and PET, alongside volatile feedstock prices.

- For instance, a packaging converter faces a critical business decision when new extended producer responsibility (EPR) mandates require incorporating 20% recycled content. This forces a strategic pivot in procurement to secure high-quality recycled material, impacting operational planning and supply chain logistics to maintain compliance and meet client demands.

What will be the Size of the Low-density Polyethylene (LDPE) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Low-density Polyethylene (LDPE) Market Segmented?

The low-density polyethylene (ldpe) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Manufacturing type

- Tubular process

- Autoclave process

- Application

- Packaging

- Agriculture

- Construction

- Electrical and electronics

- Others

- Grade type

- Film grade

- Injection molding grade

- Extrusion coating grade

- Blow molding grade

- Distribution channel

- Direct sales

- Indirect sales

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- Turkey

- UAE

- Rest of World (ROW)

- APAC

By Manufacturing Type Insights

The tubular process segment is estimated to witness significant growth during the forecast period.

The tubular process remains the dominant manufacturing method, characterized by the use of a long tubular reactor for high-pressure polymerization. This technology is highly efficient for large-scale production, establishing favorable economies of scale for commodity grades within the polyolefin family.

The resulting polymer's molecular structure provides superior mechanical properties, including excellent toughness and tear resistance, making it ideal for film and sheet manufacturing. These films are critical for general-purpose packaging, heavy-duty industrial sacks, and agricultural applications requiring robust performance.

Leveraging this process, manufacturers can achieve production efficiency gains of over 15% compared to less streamlined methods. The consistent output supports sectors reliant on dependable material for applications ranging from food preservation technology to damp-proof membranes in construction.

The Tubular process segment was valued at USD 27.70 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 50.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Low-density Polyethylene (LDPE) Market Demand is Rising in APAC Get Free Sample

The geographic landscape is characterized by varied growth dynamics, with APAC leading due to expanding industrial and consumer bases that drive demand for flexible packaging solutions. This region accounts for over 50% of the market's incremental growth.

In contrast, North America and Europe are mature markets focused on sustainability and high-performance applications like wire and cable insulation.

Regulatory frameworks are a key differentiator; in Europe, adherence to extended producer responsibility (EPR) schemes has compelled firms to innovate, with some achieving a 30% recycled content rate to align with regional targets.

The competitive advantage in North America stems from access to cost-effective ethane feedstock, supporting its status as a major production hub.

This regional diversification in demand, production, and regulation defines global trade flows and investment strategies for materials like polypropylene (PP).

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decisions in the low-density polyethylene (LDPE) market often begin with a fundamental choice between the tubular vs autoclave process LDPE, as each yields distinct properties tailored for different end uses. The primary application remains LDPE for flexible food packaging, where performance must now align with sustainable LDPE and circular economy models.

- This has spurred the development of bio-based LDPE from renewable feedstocks, although this path is complicated by recycling challenges for LDPE films, particularly the challenges of recycling multi-layer LDPE packaging. In specialized sectors, high-performance LDPE for wire insulation and LDPE film grade for agricultural use continue to show stable demand.

- Concurrently, LDPE geomembranes for landfill liners are critical for environmental compliance. The ongoing debate over LDPE vs LLDPE in stretch film applications highlights the intense material competition. Market-wide, the impact of feedstock volatility on LDPE prices and the effect of EPR schemes on LDPE market dynamics are major concerns for producers.

- From a technology standpoint, advances in metallocene catalysts for LDPE are enabling innovations in down-gauging LDPE films, crucial for the e-commerce protective packaging sector. Digitalization in LDPE production optimization is helping to mitigate cost pressures.

- For instance, in blow molding LDPE for squeeze bottle applications, integrating advanced recycled content can increase production cycle times by up to 5%, a critical trade-off that supply chain managers must balance against sustainability mandates. Other key areas include injection molding grade LDPE for closures and understanding LDPE properties for medical device packaging.

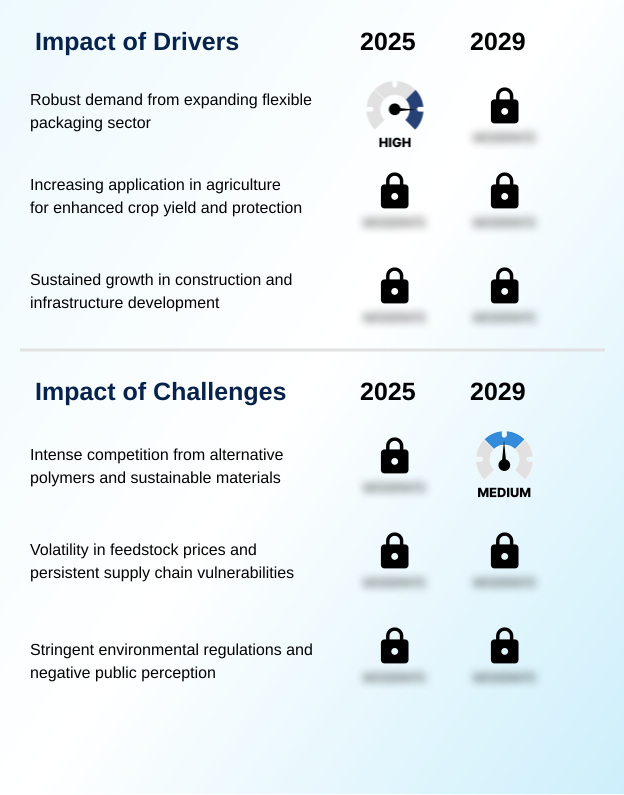

What are the key market drivers leading to the rise in the adoption of Low-density Polyethylene (LDPE) Industry?

- Robust demand from the expanding flexible packaging sector, fueled by shifts in consumer behavior and retail logistics, serves as a primary market driver.

- Sustained demand is anchored by the material's indispensable role in flexible packaging solutions, a sector continually fueled by e-commerce growth and consumer preference for convenience.

- Key properties such as moisture resistance and chemical inertness make it a preferred choice for film and sheet manufacturing.

- Another significant driver is the agricultural sector's growing reliance on plasticulture techniques, where greenhouse films, mulch films, and silage films are essential for enhancing crop yields.

- The use of mulch films, for example, can increase yields by over 20% in certain arid regions by improving water conservation.

- Additionally, infrastructure development projects create consistent demand for products like geomembranes for containment systems, which have demonstrated a 99.9% effectiveness rate in preventing soil contamination, underscoring the material's functional importance.

What are the market trends shaping the Low-density Polyethylene (LDPE) Industry?

- The accelerated shift toward a circular economy and the development of sustainable LDPE represents a transformative market trend. This is driven by regulatory pressures and evolving corporate sustainability goals.

- The market's evolution is increasingly dictated by a pivot to a circular economy, fostering innovation in both material science and processing. Key trends include the scaling of advanced recycling technologies, where the pyrolysis process converts waste back into feedstock, and the expansion of bio-based LDPE derived from sources like sugarcane-derived ethanol.

- Adopting recyclable mono-material polyethylene designs can increase packaging recyclability scores by up to 40% under certain eco-modulation fee systems. Furthermore, the use of metallocene catalysts in polymerization is enabling the production of high-performance films that are 15% thinner without sacrificing critical properties.

- This focus on sustainability and efficiency is also driving the adoption of smart factory concepts and digital twins to optimize production, particularly for high-value applications like aseptic cartons and sterile packaging.

What challenges does the Low-density Polyethylene (LDPE) Industry face during its growth?

- Intense competition from alternative polymers and a growing portfolio of sustainable materials presents a significant challenge to market growth.

- The market faces considerable headwinds from material substitution and a stringent regulatory climate. Intense competition arises from linear low-density polyethylene (LLDPE), which often provides superior puncture resistance, and from the growing adoption of bio-plastics and compostable materials.

- The financial impact of volatile feedstock prices for naphtha feedstock and ethane feedstock remains a persistent threat, with production costs fluctuating by over 25% in a single quarter. Moreover, overarching legislative frameworks, including the proposed Global Plastics Treaty and existing Extended Producer Responsibility (EPR) schemes, create significant compliance hurdles.

- In regions with strict single-use plastics prohibition, demand for certain LDPE products has declined by as much as 30%, forcing producers to innovate toward more sustainable or exempt applications.

Exclusive Technavio Analysis on Customer Landscape

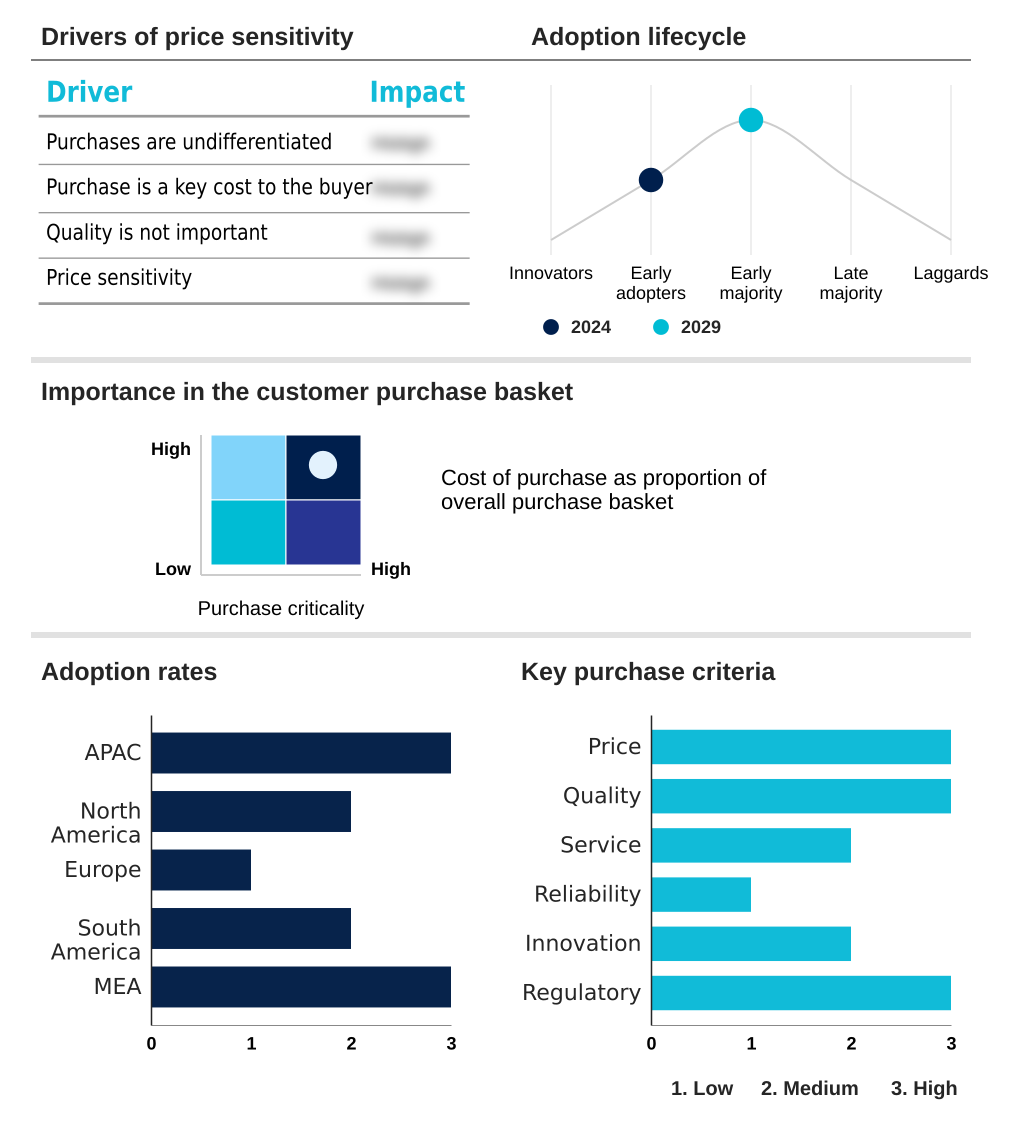

The low-density polyethylene (ldpe) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the low-density polyethylene (ldpe) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Low-density Polyethylene (LDPE) Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, low-density polyethylene (ldpe) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Borealis AG - Proprietary technology underpins specialty LDPE grades for advanced packaging and wire & cable, targeting high-performance sectors.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Borealis AG

- Borouge PLC

- Braskem SA

- Chevron Phillips Chemical Co.

- Dow Chemical Co.

- Exxon Mobil Corp.

- Formosa Plastics Corp.

- INEOS Group Holdings S.A.

- LG Chem Ltd.

- Lotte Chemical Corp.

- LyondellBasell Industries NV

- Mitsui Chemicals Inc.

- NOVA Chemicals Corp.

- Qatar Petrochemical Company (QAPCO) Q.P.J.S.C

- Reliance Industries Ltd.

- Saudi Basic Industries

- Tasnee

- TotalEnergies SE

- Westlake Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Low-density polyethylene (ldpe) market

- In September, 2024, LyondellBasell Industries NV announces a strategic partnership with a leading chemical recycling firm to offtake pyrolysis oil for its circular polymer production line, enhancing its sustainable feedstock portfolio.

- In November, 2024, Dow Chemical Co. launches a new series of recyclable mono-material polyethylene resins designed for high-barrier food packaging, enabling downgauging by up to 15% without compromising performance.

- In January, 2025, The Alliance to End Plastic Waste, in collaboration with SABIC, initiates a large-scale project in Southeast Asia to establish collection and sorting infrastructure for flexible plastic films, addressing a critical gap in the circular economy.

- In April, 2025, Borouge PLC confirms the successful commissioning of its new world-scale tubular process LDPE plant, adding significant capacity to serve the growing demand for packaging and agricultural films in Asian markets.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Low-density Polyethylene (LDPE) Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 324 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.7% |

| Market growth 2025-2029 | USD 12044.3 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 4.6% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, Brazil, Argentina, Colombia, Saudi Arabia, Turkey, UAE, South Africa and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The low-density polyethylene (LDPE) market is defined by its dual role as a high-volume thermoplastic polymer and a platform for specialized material innovation.

- As a member of the polyolefin family, this material is produced from monomer ethylene via high-pressure polymerization in either a tubular reactor or an autoclave reactor, resulting in a distinct molecular structure used in film and sheet manufacturing, extrusion coating, and wire and cable insulation. The paramount boardroom-level issue is the industry-wide transition toward a circular economy.

- This strategic shift necessitates significant investment in both mechanical recycling and advanced recycling infrastructure, including pyrolysis process facilities, to produce recycled content and meet stringent Extended Producer Responsibility (EPR) mandates. Companies leveraging digital twins and machine learning algorithms in production have demonstrated a quantifiable reduction in off-spec material by over 10%, directly enhancing profitability.

- This drive for efficiency is critical, as the market contends with competition from materials like LLDPE, PP, PET, PLA, and PHA, alongside the persistent volatility of feedstock prices for both naphtha feedstock and ethane feedstock, while developing solutions like bio-based LDPE from sugarcane-derived ethanol.

What are the Key Data Covered in this Low-density Polyethylene (LDPE) Market Research and Growth Report?

-

What is the expected growth of the Low-density Polyethylene (LDPE) Market between 2025 and 2029?

-

USD 12.04 billion, at a CAGR of 4.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Manufacturing Type (Tubular process, Autoclave process), Application (Packaging, Agriculture, Construction, Electrical and electronics, Others), Grade Type (Film grade, Injection molding grade, Extrusion coating grade, Blow molding grade), Distribution Channel (Direct sales, Indirect sales) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Robust demand from expanding flexible packaging sector, Intense competition from alternative polymers and sustainable materials

-

-

Who are the major players in the Low-density Polyethylene (LDPE) Market?

-

Borealis AG, Borouge PLC, Braskem SA, Chevron Phillips Chemical Co., Dow Chemical Co., Exxon Mobil Corp., Formosa Plastics Corp., INEOS Group Holdings S.A., LG Chem Ltd., Lotte Chemical Corp., LyondellBasell Industries NV, Mitsui Chemicals Inc., NOVA Chemicals Corp., Qatar Petrochemical Company (QAPCO) Q.P.J.S.C, Reliance Industries Ltd., Saudi Basic Industries, Tasnee, TotalEnergies SE and Westlake Corp.

-

Market Research Insights

- Market dynamics are shaped by a persistent need for high-performance materials in diverse applications, from flexible packaging solutions to sterile packaging in healthcare. The adoption of advanced agricultural methods creates steady demand for greenhouse films and mulch films.

- In response to efficiency pressures, manufacturers are integrating smart factory concepts; the use of IoT sensors in production has enabled some operators to reduce energy consumption by over 10%. Concurrently, the push for sustainability drives innovation in recyclable mono-material polyethylene, with new designs improving recycling stream purity by over 25% compared to complex multi-layer structures.

- These shifts reflect an industry balancing performance requirements with circular economy goals.

We can help! Our analysts can customize this low-density polyethylene (ldpe) market research report to meet your requirements.

RIA -

RIA -