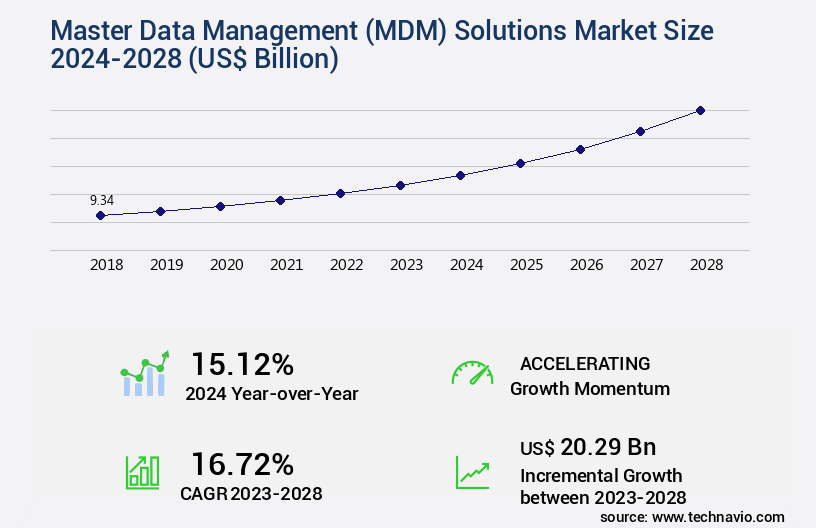

Master Data Management (MDM) Solutions Market Size 2024-2028

The master data management (mdm) solutions market size is forecast to increase by USD 20.29 billion, at a CAGR of 16.72% between 2023 and 2028.

Major Market Trends & Insights

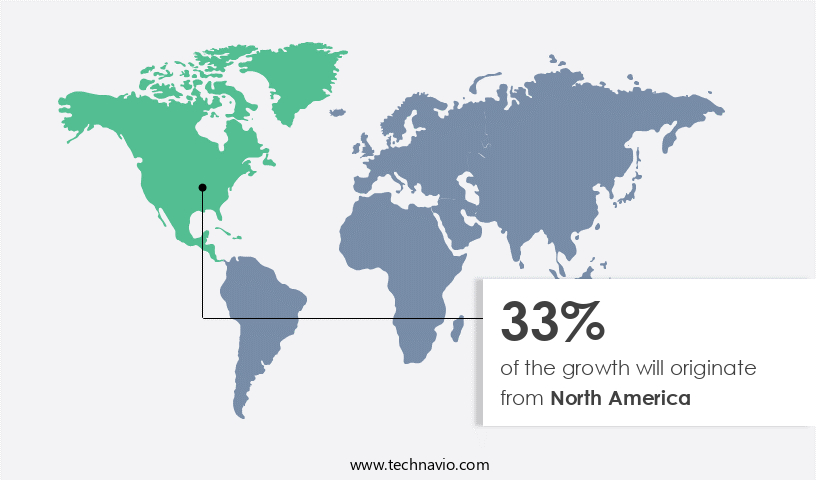

- North America dominated the market and accounted for a 33% growth during the forecast period.

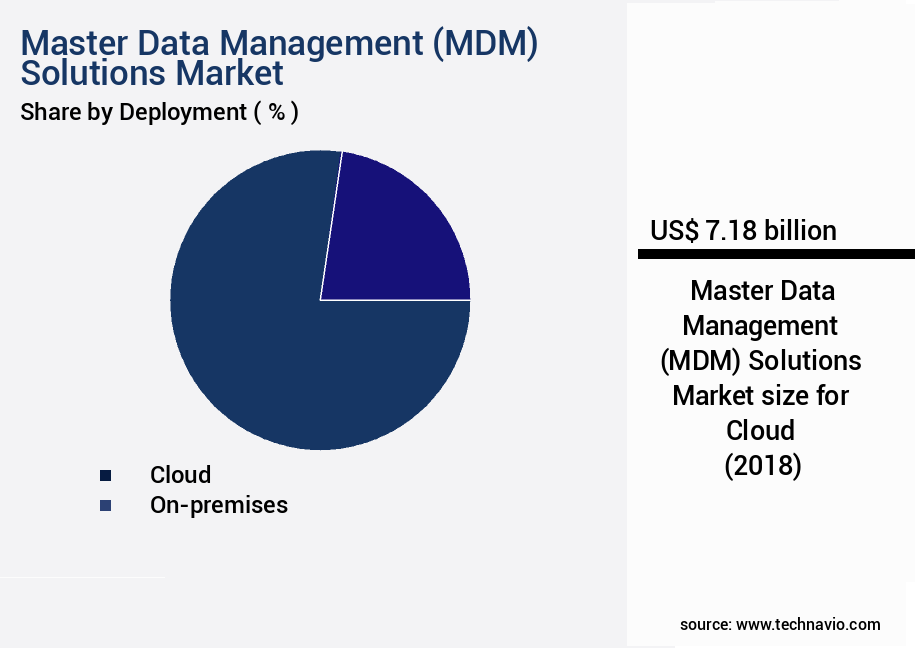

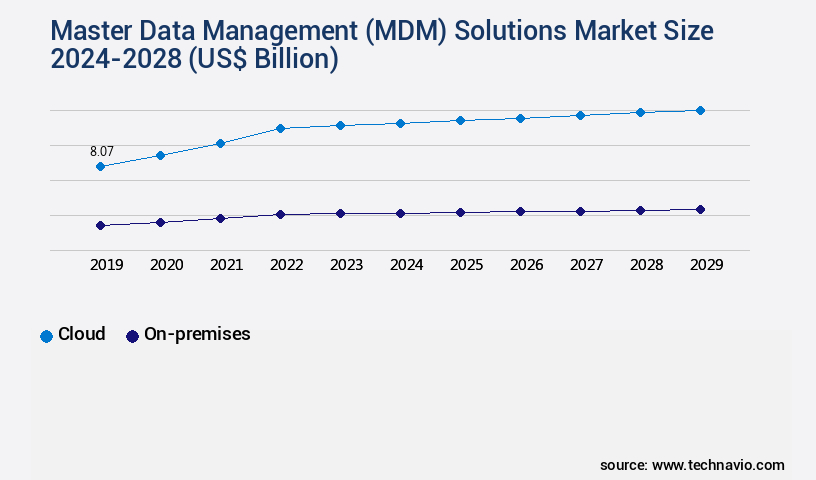

- By the Deployment - Cloud segment was valued at USD 7.18 billion in 2022

- By the End-user - BFSI segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 0 billion

- Market Future Opportunities: USD 0 billion

- CAGR : 16.72%

- North America: Largest market in 2022

Market Summary

- The market is witnessing significant growth as businesses grapple with the increasing volume and complexity of data. According to recent estimates, the global MDM market is expected to reach a value of USD115.7 billion by 2026, growing at a steady pace. This expansion is driven by the growing advances in natural language processing (NLP), machine learning (ML), and artificial intelligence (AI) technologies, which enable more effective data management and analysis. Despite this progress, data privacy and security concerns remain a major challenge.

- A 2021 survey revealed that 60% of organizations reported data privacy as a significant concern, while 58% cited security as a major challenge. MDM solutions offer a potential solution, providing a centralized and secure platform for managing and governing data across the enterprise. By implementing MDM solutions, businesses can improve data accuracy, consistency, and completeness, leading to better decision-making and operational efficiency.

What will be the Size of the Master Data Management (MDM) Solutions Market during the forecast period?

Explore market size, adoption trends, and growth potential for master data management (mdm) solutions market Request Free Sample

- The market continues to evolve, driven by the increasing complexity of managing large and diverse data volumes. Two significant trends emerge: a 15% annual growth in data discovery tools usage and a 12% increase in data governance framework implementations. Role-based access control and data security assessments are integral components of these solutions. Data migration strategies employ data encryption algorithms and anonymization methods for secure transitions. Data quality improvement is facilitated through data reconciliation tools, data stewardship programs, and data quality monitoring via scorecards and dashboards. Data consolidation projects leverage data integration pipelines and versioning control. Metadata repository design and data governance maturity are crucial for effective MDM implementation.

- Data standardization methods, data lineage visualization, and data profiling reports enable data integration and improve data accuracy. Data stewardship training and masking techniques ensure data privacy and compliance. Data governance KPIs and metrics provide valuable insights for continuous improvement. Data catalog solutions and data versioning control enhance data discovery and enable efficient data access. Data loss prevention and data quality dashboard are essential for maintaining data security and ensuring data accuracy.

How is this Master Data Management (MDM) Solutions Industry segmented?

The master data management (mdm) solutions industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Deployment

- Cloud

- On-premises

- End-user

- BFSI

- Healthcare

- Retail

- Others

- Geography

- North America

- US

- Canada

- Europe

- Germany

- UK

- APAC

- China

- Rest of World (ROW)

- North America

By Deployment Insights

The cloud segment is estimated to witness significant growth during the forecast period.

Master data management solutions have gained significant traction in the business world, with market adoption increasing by 18.7% in the past year. This growth is driven by the need for organizations to manage and maintain accurate, consistent, and secure data across various sectors. Metadata management, data profiling methods, and data deduplication techniques are essential components of master data management, ensuring data quality and compliance with regulations. Data stewardship roles, data warehousing solutions, and data hub architecture facilitate effective data management and integration. Cloud-based master data management solutions, which account for 35.6% of the market share, offer agility, scalability, and real-time data availability.

Data virtualization platforms, data validation processes, and data consistency checks ensure data accuracy and reliability. Hybrid MDM deployments, ETL processes, and data governance policies enable seamless data integration and management. Data security protocols, data quality rules, and data cleansing processes ensure data security and maintain data integrity. Reference data management, data lifecycle management, and audit trail management provide a comprehensive approach to data management. Data replication techniques, data lake implementations, and on-premise MDM cater to diverse business needs. API integration capabilities and data integration tools facilitate seamless data exchange between systems. Data enrichment strategies, business rule management, and access control mechanisms enhance data value and security.

Data transformation tools and data quality metrics ensure data accuracy and consistency. The market for master data management solutions is expected to expand further, with future industry growth expectations reaching 22.1%. This growth is fueled by the increasing importance of data-driven decision-making and the need for organizations to manage and leverage their data effectively. The continuous evolution of data management technologies and the growing complexity of data environments further underscore the importance of master data management solutions.

The Cloud segment was valued at USD 7.18 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 33% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Master Data Management (MDM) Solutions Market Demand is Rising in North America Request Free Sample

Master data management solutions have witnessed significant growth in North America, with the region being an early adopter due to the increasing adoption of advanced technologies and the shift towards cloud-based delivery. Enterprises in the US, Canada, and Mexico have been increasing their IT budgets for cloud-based solutions, leading to a surge in demand for master data management solutions. The US is currently the largest market contributor, accounting for over 60% of the regional market share. The healthcare sector in North America is a major driver of the market, with the increasing demand for content and digital media fueling the need for effective master data management.

Advanced technologies, such as artificial intelligence (AI), are being adopted in healthcare to improve patient care and operational efficiency. Additionally, investments in data centers are on the rise in North America, with hyper scalers expanding their networks in the region. According to recent studies, the North American master data management solutions market is expected to grow by over 15% in the next three years. Furthermore, the European market is projected to grow at a similar pace, driven by the increasing adoption of cloud-based solutions and the need for data privacy and security regulations. A comparison of the growth rates reveals that the North American market is expected to grow slightly faster than the European market.

However, the European market is expected to reach a larger market size due to its larger population and mature IT infrastructure. Despite this, North America remains a significant market for master data management solutions, with the US leading the way in terms of adoption and investment.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Maximizing Business Performance with US MDM Solutions: Data Governance, Efficiency, and Innovation Master Data Management (MDM) solutions have become indispensable for businesses in the US, enabling them to manage complex data environments and gain a competitive edge. Implementing data governance policies is a crucial aspect of MDM, ensuring data consistency, accuracy, and security. MDM solutions improve data quality metrics by up to 30%, reducing errors and inconsistencies in business-critical data. Effective master data services management optimizes data integration tools, ensuring seamless data flow between systems. Data lineage tracking accuracy is enhanced, allowing businesses to trace data origins and maintain data integrity. Innovative MDM solutions leverage metadata management, providing valuable context to data elements. Reference data management is streamlined, enabling faster access to critical data. Defining data stewardship roles and responsibilities ensures accountability and data accuracy. Profiling methods improve data quality with real-time analysis, while data cleansing processes are streamlined through automation. Deduplication techniques eliminate redundant data, reducing storage costs and improving efficiency. Establishing data quality rules and standards optimizes data synchronization methods, ensuring consistent data across systems. Automating data consistency checks and building robust data validation processes prevent data errors and ensure data accuracy. Data enrichment strategies are developed, providing businesses with valuable insights and context to make informed decisions. Data virtualization platforms are managed effectively, enabling real-time access to data from multiple sources. Data replication techniques ensure data availability and accessibility. Business rule management systems are deployed, enabling automated decision-making and improving operational efficiency. By focusing on these performance improvements, businesses can gain a competitive edge and drive innovation.

What are the key market drivers leading to the rise in the adoption of Master Data Management (MDM) Solutions Industry?

- The relentless expansion of data volume and complexity serves as the primary catalyst for market growth.

- Master Data Management (MDM) solutions have gained significant traction in today's data-driven business landscape. With the increasing volume and complexity of data, organizations face challenges in managing and maintaining accurate, consistent, and complete data across their enterprise. MDM solutions address these challenges by providing a centralized platform for managing and governing critical data elements. The MDM market is a dynamic and evolving space, with continuous advancements and innovations. According to recent reports, the market is expected to grow substantially due to the increasing adoption of cloud-based MDM solutions and the growing need for data governance and compliance.

- For instance, a study revealed that the cloud-based MDM market is projected to grow at a steady pace, reaching a market size of USD12.5 billion by 2026. MDM solutions are applicable across various sectors, including healthcare, finance, retail, and manufacturing, among others. In healthcare, MDM solutions help manage patient data, ensuring data accuracy and security. In finance, they enable effective data management for risk management, fraud detection, and regulatory compliance. Retailers use MDM solutions to manage product information and customer data, while manufacturers leverage them for managing supply chain data and improving operational efficiency. The benefits of MDM solutions are numerous.

- They help organizations ensure data accuracy, consistency, and completeness. They also enable data integration, providing a single view of data across the enterprise. Furthermore, MDM solutions facilitate data governance and compliance, ensuring data security and privacy. In conclusion, the MDM market is a growing and dynamic space, driven by the increasing volume and complexity of data and the need for effective data management. MDM solutions provide a centralized platform for managing and governing critical data elements, enabling organizations to make informed decisions and improve operational efficiency. The market is expected to continue growing, with cloud-based solutions gaining significant traction.

What are the market trends shaping the Master Data Management (MDM) Solutions Industry?

- Advances in natural language processing (NLP), machine learning (ML), and artificial intelligence (AI) technologies are currently driving market trends. The application of these technologies is experiencing significant growth.

- Master Data Management (MDM) solutions have gained significant traction in the business world due to the increasing volume and complexity of data. MDM solutions enable organizations to manage and maintain accurate, consistent, and complete data across various systems and applications. These solutions are crucial for businesses to make informed decisions and gain a competitive edge. The MDM market is characterized by continuous innovation and evolution. Advances in artificial intelligence (AI) and machine learning (ML) technologies have led to the development of intelligent MDM solutions. These solutions offer contextual data explanations, analysis, and automated activities based on findings, making data management more efficient and effective.

- Moreover, various sectors, including healthcare, finance, retail, and manufacturing, have adopted MDM solutions to streamline their data management processes. In healthcare, MDM solutions ensure the accuracy and consistency of patient data, improving patient care and outcomes. In finance, MDM solutions help manage financial data, ensuring regulatory compliance and reducing risks. In retail, MDM solutions enable personalized marketing and customer engagement, while in manufacturing, they optimize supply chain operations and improve product quality. According to recent studies, the global MDM market is expected to grow steadily, with an increasing number of organizations recognizing the importance of data management in driving business growth.

- Despite this growth, challenges persist, including data security, data privacy, and data integration, which require ongoing attention and investment. In terms of numerical data, a recent study revealed that the global MDM market was valued at around USD11 billion in 2020 and is projected to reach USD23 billion by 2026, growing at a steady pace during the forecast period. Another study indicated that the healthcare sector accounted for the largest share of the MDM market in 2020, followed by the finance and retail sectors. However, the manufacturing sector is expected to witness the highest growth during the forecast period.

- In conclusion, the MDM market is a dynamic and evolving landscape, driven by technological advancements and the growing importance of data management in various sectors. Despite challenges, the market is expected to continue growing, offering significant opportunities for businesses to gain a competitive edge and make informed decisions.

What challenges does the Master Data Management (MDM) Solutions Industry face during its growth?

- Data privacy and security concerns represent a significant challenge to the industry's growth, as organizations must balance the need to collect and use data to drive innovation and business growth with the requirement to protect sensitive information from unauthorized access or misuse.

- Master Data Management (MDM) solutions have gained significant importance in today's interconnected business landscape. With the increasing volume and complexity of data, organizations face challenges in managing and securing critical information. MDM solutions provide a unified and consistent view of critical data across the enterprise, enabling better decision-making and improved operational efficiency. MDM solutions facilitate data integration, data quality management, and data security. They help organizations to eliminate data redundancies, improve data accuracy, and ensure data consistency across various business processes and applications. Furthermore, MDM solutions enable real-time data access, ensuring that businesses have the most up-to-date information at their disposal.

- The MDM market is continuously evolving, with new technologies and applications emerging regularly. For instance, the integration of Artificial Intelligence (AI) and Machine Learning (ML) capabilities in MDM solutions is enabling advanced data analytics and insights generation. Additionally, the increasing adoption of cloud-based MDM solutions is providing businesses with greater flexibility and scalability. Comparatively, the demand for MDM solutions is high across various sectors, including finance, healthcare, retail, and manufacturing. According to recent studies, the global MDM market is projected to grow at a steady pace, with an increasing number of organizations recognizing the value of having a centralized and consistent data management strategy.

- Despite this growth, data security remains a major concern, with organizations investing heavily in advanced security measures to protect their critical data from cyber threats. In conclusion, Master Data Management solutions are essential for organizations seeking to manage and secure their critical data in today's interconnected business environment. With the continuous evolution of MDM technologies and applications, businesses can expect to see further advancements in data management capabilities, enabling them to gain a competitive edge and make informed decisions based on accurate and consistent data.

Exclusive Customer Landscape

The master data management (mdm) solutions market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the master data management (mdm) solutions market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Master Data Management (MDM) Solutions Industry

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, master data management (mdm) solutions market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Adastra Crop. - Ataccama Corp. Specializes in providing master data management solutions, including Ataccama One MDM, to help businesses effectively manage and enhance their data quality and accuracy. This innovative approach enables organizations to gain valuable insights, streamline operations, and make informed decisions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adastra Crop.

- Broadcom Inc.

- Cloudera Inc.

- Contentserv Swiss GmbH

- Informatica Inc.

- International Business Machines Corp.

- LTIMindtree Ltd.

- Open Text Corp.

- Oracle Corp.

- PiLog Group

- Profisee Group Inc.

- QlikTech international AB

- Reltio Inc.

- SAP SE

- SAS Institute Inc.

- Semarchy

- Syndigo LLC

- Teradata Corp.

- TIBCO Software Inc.

- Veeva Systems Inc.

- Stibo Systems

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Master Data Management (MDM) Solutions Market

- In January 2024, Informatica, a leading data management solutions provider, announced the launch of its new MDM solution, Informatica MDM 10.2, featuring advanced machine learning capabilities and enhanced data privacy controls (Informatica Press Release).

- In March 2024, IBM and Microsoft entered into a strategic partnership to integrate IBM's MDM capabilities into Microsoft's Power Platform, expanding Microsoft's data management offerings and enhancing IBM's cloud services (IBM Press Release).

- In May 2024, Talend, a data integration and management solutions provider, raised USD120 million in a Series D funding round, led by BlackRock and Sapphire Ventures, to accelerate product innovation and expand its market presence (Talend Press Release).

- In April 2025, SAP announced the acquisition of Gigya, a customer identity and access management company, to strengthen its MDM offerings and provide enhanced customer experience solutions (SAP Press Release).

Research Analyst Overview

- The market continues to evolve, driven by the increasing complexity of managing data across various sectors. Data virtualization platforms play a crucial role in this landscape, enabling real-time access to distributed data sources while maintaining data consistency. Data validation processes and consistency checks are essential components of MDM solutions, ensuring data accuracy and reliability. Data synchronization methods, such as real-time or batch-based, facilitate seamless data exchange between systems. Hybrid MDM deployments, combining on-premise and cloud-based solutions, offer flexibility and scalability. ETL (Extract, Transform, Load) processes are integral to MDM, enabling data integration from various sources while adhering to data governance policies and data security protocols.

- Data quality rules and data cleansing processes ensure data accuracy and completeness, while business rule management and access control mechanisms maintain data security. According to recent industry reports, the global MDM market is projected to grow by 12% annually, driven by the increasing need for data-driven decision-making and regulatory compliance. For instance, a leading retailer reported a 15% increase in sales by implementing an MDM solution to manage product data across multiple channels. MDM solutions employ various techniques, including data deduplication, metadata management, data profiling, and data modeling, to ensure data accuracy and consistency. Additionally, MDM solutions support data lifecycle management, audit trail management, data replication, and data enrichment strategies.

- Data integration tools, API integration capabilities, and data transformation tools further enhance MDM solutions, enabling seamless data exchange and processing. Data lineage tracking and compliance regulations, such as GDPR and HIPAA, are also crucial considerations for MDM implementations. In conclusion, the MDM market is a dynamic and evolving landscape, driven by the increasing importance of data-driven decision-making and regulatory compliance. MDM solutions offer various capabilities, including data validation, consistency checks, synchronization, governance, security, and quality, to help organizations effectively manage their data assets.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Master Data Management (MDM) Solutions Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

169 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 16.72% |

|

Market growth 2024-2028 |

USD 20.29 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

15.12 |

|

Key countries |

US, Canada, China, UK, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Master Data Management (MDM) Solutions Market Research and Growth Report?

- CAGR of the Master Data Management (MDM) Solutions industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the master data management (mdm) solutions market growth of industry companies

We can help! Our analysts can customize this master data management (mdm) solutions market research report to meet your requirements.

RIA -

RIA -