Meat Packaging Market Size and Growth Forecast 2026-2030

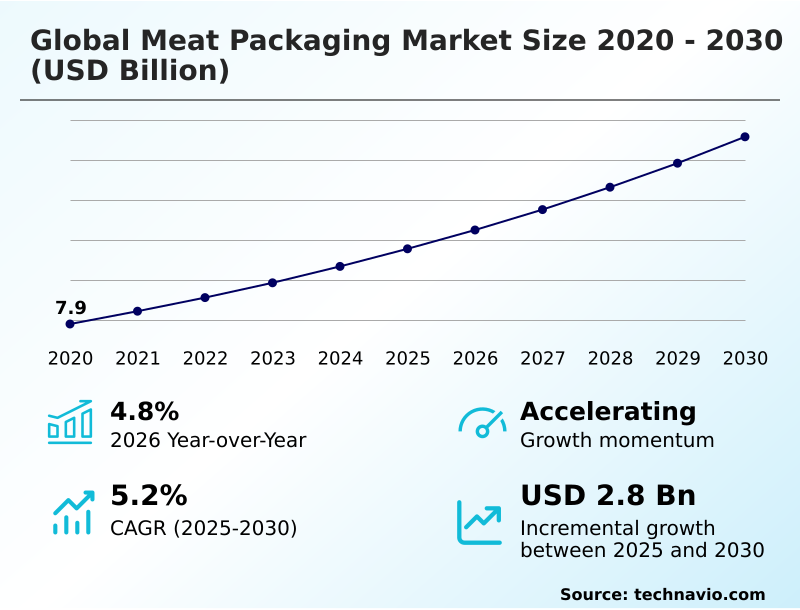

The Meat Packaging Market size was valued at USD 9.78 billion in 2025 growing at a CAGR of 5.2% during the forecast period 2026-2030.

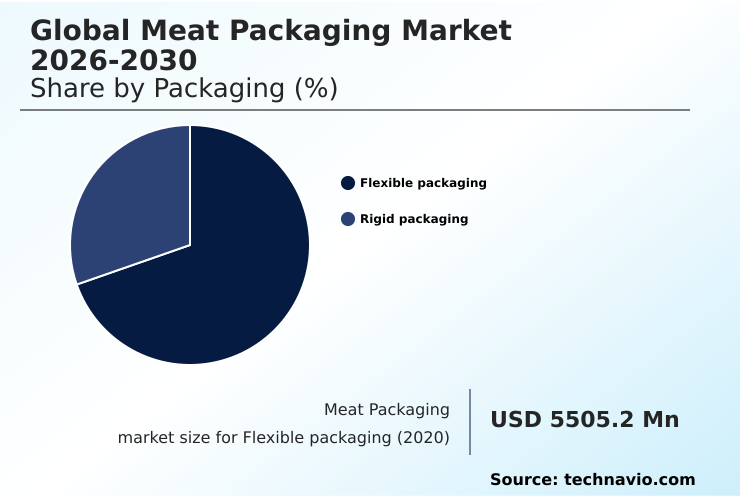

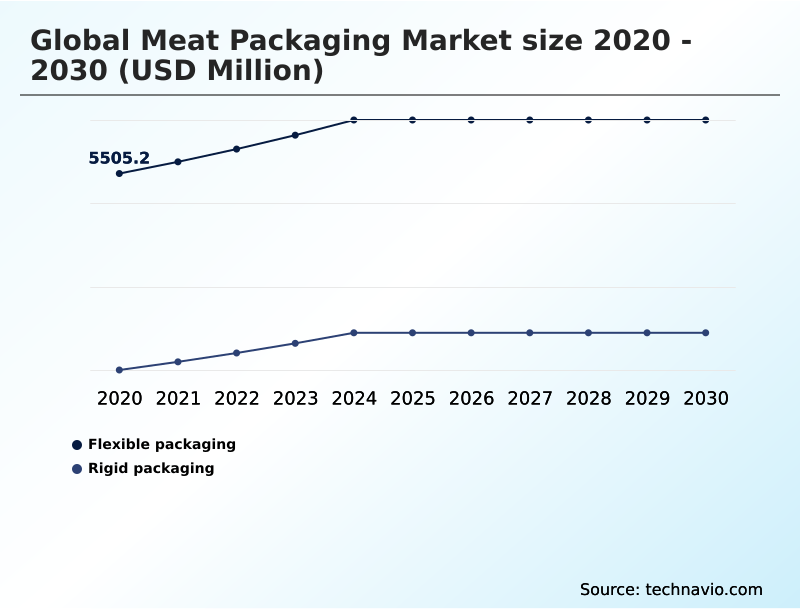

APAC accounts for 37.1% of incremental growth during the forecast period. The Flexible packaging segment by Packaging was valued at USD 6.35 billion in 2024, while the Pork segment holds the largest revenue share by Type.

The market is projected to grow by USD 4.68 billion from 2020 to 2030, with USD 2.80 billion of the growth expected during the forecast period of 2025 to 2030.

Get Key Insights on Market Forecast (PDF) Request Free Sample

Meat Packaging Market Overview

The meat packaging market is characterized by a consistent year-over-year growth of 4.8%, with a significant portion of this expansion, approximately 37.1%, originating from the APAC region. This growth is fueled by the rising consumer demand for convenient, safe, and nutritionally preserved protein products. Key industry developments include the adoption of sustainable meat packaging solutions like mono-material trays and the increasing use of advanced high-barrier films to extend shelf life. For instance, a mid-scale poultry processor implementing a new line of thermoforming machinery for vacuum skin packaging can reduce in-store spoilage by over 15%, directly improving retail margins. The industry also contends with challenges such as volatile raw material costs for high-density polyethylene and the need to comply with stringent food contact regulations like the EU's Regulation (EC) No 1935/2004. The integration of intelligent systems and tamper-evident features is becoming standard as processors and retailers prioritize supply chain transparency and food safety in both beef packaging and seafood packaging.

Drivers, Trends, and Challenges in the Meat Packaging Market

Strategic decisions in the meat packaging market are increasingly nuanced, depending on the specific product application. The global meat packaging market 2026-2030 for high-value items, such as premium beef cuts, relies on vacuum skin packaging to enhance retail appeal and justify higher price points.

In contrast, the global meat packaging market 2026-2030 for bulk freezing prioritizes durability and barrier properties to prevent freezer burn, often using heavy-duty flexible films. For processors, achieving ISO 22000 certification for food safety management systems necessitates different packaging line configurations.

For example, a facility might dedicate a high-speed line with thermoforming machinery to the global meat packaging market 2026-2030 for case-ready meat, which requires consistent tray sealing and labeling.

Simultaneously, a separate line may handle the global meat packaging market 2026-2030 for chilled and frozen meat, focusing on modified atmosphere packaging to manage microbial growth and color retention in poultry, which holds a larger market share than seafood. The global meat packaging market 2026-2030 for processed meats demands yet another approach, often utilizing antimicrobial packaging to ensure shelf stability.

Primary Growth Driver: A key driver for the market is the rising consumer awareness of the high nutritional value of meat products, which influences purchasing decisions.

Market growth is fundamentally driven by the expansion of retail-ready meat packaging and the strengthening of cold chain infrastructure, particularly in emerging economies.

The adoption of case-ready formats allows large retailers to centralize processing, improve hygiene, and reduce in-store labor costs. This shift is creating significant demand for standardized rigid trays and high-barrier lidding films.

In APAC, which is projected to contribute 37.1% of the market's incremental growth, investments in refrigerated transport and storage are enabling packaged meat to reach new urban and semi-urban consumers.

This infrastructure expansion supports the use of advanced solutions like modified atmosphere packaging and necessitates tamper-evident features to ensure product integrity across longer and more complex supply chains.

Emerging Market Trend: The increasing demand for advanced plastic films is a primary trend in meat packaging. This is driven by the need for enhanced product protection and extended shelf life.

Key trends are reshaping the technical landscape, driven by consumer demand for both convenience and sustainability. The adoption of skin packaging is accelerating, as it offers superior product visibility and extended shelf life, particularly for high-value beef and seafood products. This method often involves advanced thermoforming machinery to create a second-skin effect.

Concurrently, there is a strong push toward sustainable meat packaging, with a focus on mono-material trays made from recycled PET and bio-based alternatives. Leading processors in regions like Europe, which accounts for nearly 20% of the market, are increasingly using compostable films for organic product lines to meet stringent environmental targets and consumer expectations.

This dual focus on premium presentation and environmental responsibility is a defining characteristic of current market evolution.

Key Industry Challenge: Constantly changing consumer preferences present a significant challenge, hampering stable growth in the market.

The market faces significant headwinds from the volatility of raw material prices and the complexities of regulatory compliance. The cost of polymers like high-density polyethylene is tied to unpredictable global energy markets, creating margin pressure for manufacturers of plastic films and rigid trays. This uncertainty complicates long-term planning and investment in innovation.

Furthermore, adhering to stringent regulations, such as the EU's Single-Use Plastics Directive, adds another layer of complexity. Processors must navigate evolving rules regarding post-consumer recycled content and materials approved for the food contact environment. This requires continuous investment in research and development to create packaging that is both compliant and cost-effective, balancing safety with sustainability mandates.

Explore Full Market Dynamics Analysis Request Free Sample

Meat Packaging Market Segmentation

The meat packaging industry research report provides comprehensive data including region-wise segment analysis, with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

Packaging Segment Analysis

The flexible packaging segment is estimated to witness significant growth during the forecast period.

The flexible packaging segment, which commands a majority share of the meat packaging market, is driven by the urgent need for extended shelf life and reduced transportation costs.

This segment heavily relies on multilayer films and vacuum skin packaging that conform to product shapes, reducing oxidative spoilage. In practice, a high-volume processing plant specializing in pork packaging utilizes specialized bone-guard films to prevent punctures, ensuring seal integrity.

This flexibility is essential for accommodating the diverse shapes of fresh poultry and beef in case-ready formats.

The adoption of oven-ready flexible pouches further highlights the move toward consumer convenience, integrating the packaging into the meal preparation process itself, a key factor in its continued market dominance over rigid formats.

The Flexible packaging segment was valued at USD 6.35 billion in 2024 and showed a gradual increase during the forecast period.

Meat Packaging Market by Region: APAC Leads with 37.1% Growth Share

APAC is estimated to contribute 37.1% to the growth of the global market during the forecast period.

The geographic landscape is led by APAC, which accounts for 37.1% of the market's incremental growth, driven by rising protein consumption and the modernization of retail infrastructure.

North America follows, contributing 28.79% to the expansion, with a mature market focused on innovation in case-ready formats and sustainable meat packaging.

In Europe, which represents a smaller but highly regulated segment, compliance with standards such as Regulation (EC) No 1935/2004 on food contact materials is paramount. This has accelerated the adoption of mono-material trays and high-barrier films.

The expansion of cold chain packaging infrastructure is a critical factor globally, enabling the safe distribution of products like pork packaging and seafood packaging to new urban centers and supporting the growth of online grocery channels.

Customer Landscape Analysis for the Meat Packaging Market

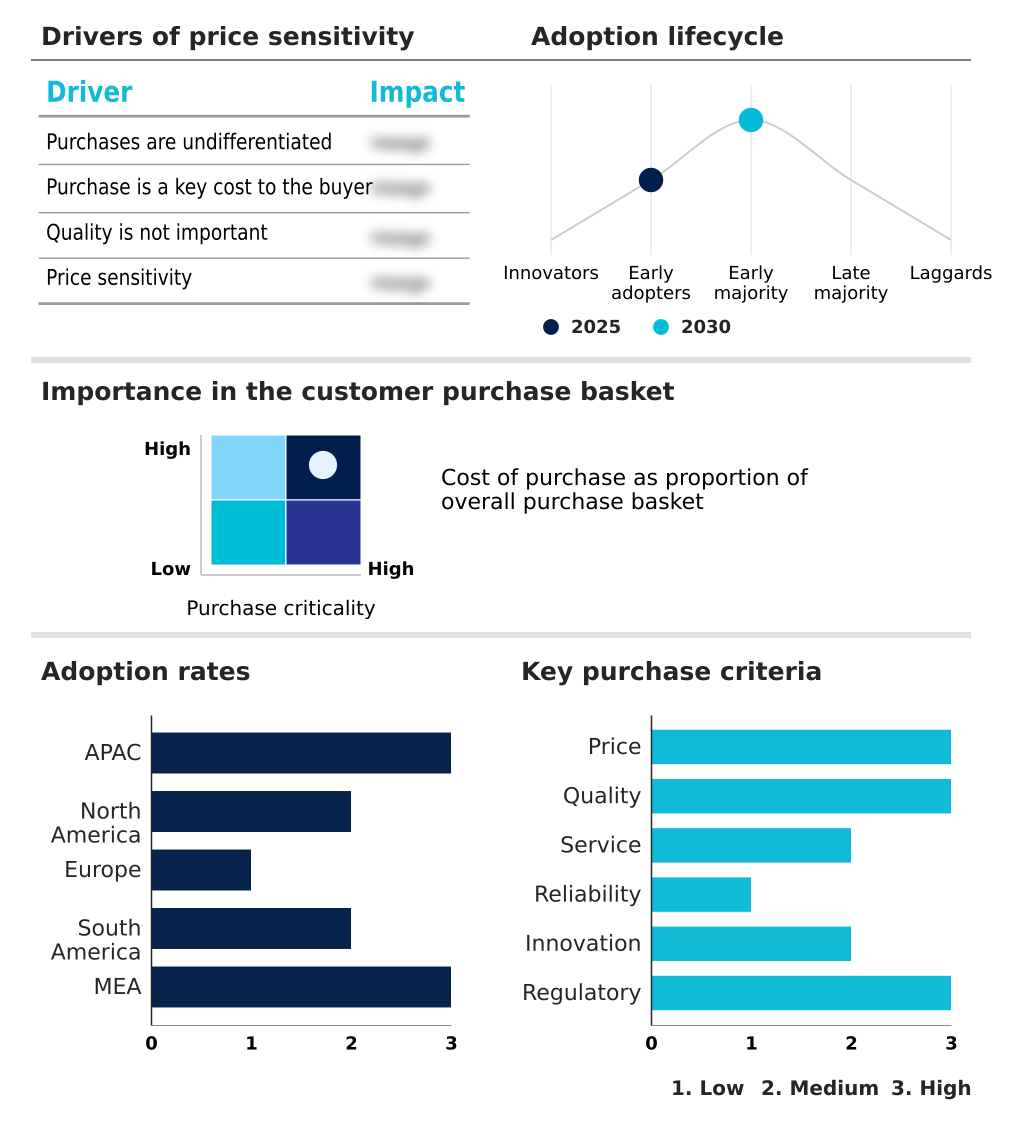

The meat packaging market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the meat packaging market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Competitive Landscape of the Meat Packaging Market

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the meat packaging market industry.

Amcor Plc - Key offerings include advanced flexible films, rigid containers, and high-barrier solutions designed to extend shelf life and ensure food safety for protein products.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amcor Plc

- Amerplast Ltd.

- AP Moller Maersk AS

- Berry Global Inc.

- Bollore SE

- Cascades Inc.

- Constantia Flexibles GmbH

- Coveris Management GmbH

- Crown Holdings Inc.

- EasyPak LLC

- Foster International Packaging

- GRUPO ULMA S. COOP

- Omori Machinery Co. Ltd.

- Pactiv Evergreen Inc.

- Sealed Air Corp.

- Smurfit Kappa Group

- Sonoco Products Co.

- Uniflex

- Viscofan SA

- Winpak Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments in the Meat Packaging Market

- In March 2025, Walmart announced the full implementation of its centralized case-ready meat facilities across its North American operations, a strategic move that significantly increased the demand for pre-packaged rigid trays and high-barrier films.

- In May 2025, Multivac showcased its latest thermoforming machinery at an industrial fair in Milan, Italy, specifically designed to handle high-speed skin packaging for organic beef cuts, illustrating how technology enhances the premium feel and shelf life of meat products.

- In July 2025, Sealed Air introduced a new generation of ultra-thin, high-barrier films that enabled a twenty percent reduction in plastic usage while maintaining shelf-life extension for fresh poultry, highlighting a commitment to material efficiency.

- In September 2025, Berry Global produced its first large-scale batch of rigid meat trays containing sixty percent post-consumer recycled content for a leading UK-based meat processor, marking a milestone in integrating recycled materials into demanding food-contact applications.

Research Analyst Overview: Meat Packaging Market

An analyst view reveals that the meat packaging market is undergoing a structural shift where sustainability is no longer a peripheral concern but a central factor in boardroom decisions regarding capital expenditure and brand strategy.

While the market is experiencing steady expansion, compliance with forthcoming regulations like the EU's Packaging and Packaging Waste Regulation (PPWR) requires proactive investment in new materials and processes. This has elevated the importance of mono-material trays and advanced flexible films that support a circular economy.

A key decision point for processors is balancing the high performance of multilayer films for beef packaging and poultry packaging with the recyclability of mono-material alternatives. The adoption of advanced technologies like thermoforming machinery for vacuum skin packaging and oxygen scavenger films is crucial for maintaining product quality.

This transition is not merely about compliance but about securing long-term market position and meeting the evolving criteria of major retailers, especially in regions like North America, which accounts for nearly 29% of market growth.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Meat Packaging Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 301 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.2% |

| Market growth 2026-2030 | USD 2804.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.8% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Meat Packaging Market: Key Questions Answered in This Report

-

What is the expected growth of the Meat Packaging Market between 2026 and 2030?

-

The Meat Packaging Market is expected to grow by USD 2.80 billion during 2026-2030, registering a CAGR of 5.2%. Year-over-year growth in 2026 is estimated at 4.8%%. This acceleration is shaped by rising awareness of high nutritional value of meat products, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Packaging (Flexible packaging, and Rigid packaging), Type (Pork, Poultry, Beef, Goat meat or mutton, and Seafood), End-user (Supermarkets and hypermarkets, Online grocery, and Meat processors) and Geography (APAC, North America, Europe, South America, Middle East and Africa). Among these, the Flexible packaging segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers APAC, North America, Europe, South America and Middle East and Africa. APAC is estimated to contribute 37.1% to market growth during the forecast period. Country-level analysis includes China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is rising awareness of high nutritional value of meat products, which is accelerating investment and industry demand. The main challenge is constant changing of consumer preferences hampering market growth, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Meat Packaging Market?

-

Key vendors include Amcor Plc, Amerplast Ltd., AP Moller Maersk AS, Berry Global Inc., Bollore SE, Cascades Inc., Constantia Flexibles GmbH, Coveris Management GmbH, Crown Holdings Inc., EasyPak LLC, Foster International Packaging, GRUPO ULMA S. COOP, Omori Machinery Co. Ltd., Pactiv Evergreen Inc., Sealed Air Corp., Smurfit Kappa Group, Sonoco Products Co., Uniflex, Viscofan SA and Winpak Ltd.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Meat Packaging Market Research Insights

Market dynamics are shaped by a definitive shift toward flexible packaging formats, which hold a substantially larger share than rigid alternatives. This preference is driven by demands for material efficiency and consumer convenience, exemplified by the development of oven-ready flexible pouches.

A key operational reality is the rigorous compliance with standards like the US Food Safety Modernization Act (FSMA), which dictates protocols for the food contact environment and necessitates the use of tamper-evident features. Processors are increasingly adopting intelligent systems with smart labels to provide digital passports for their products, enhancing traceability.

The integration of moisture absorbent pads and bone-guard films in poultry and pork packaging demonstrates the technical specificity required to meet both regulatory and consumer expectations, moving beyond basic containment to active product preservation.

We can help! Our analysts can customize this meat packaging market research report to meet your requirements.

RIA -

RIA -