Memory Ics Market Size 2026-2030

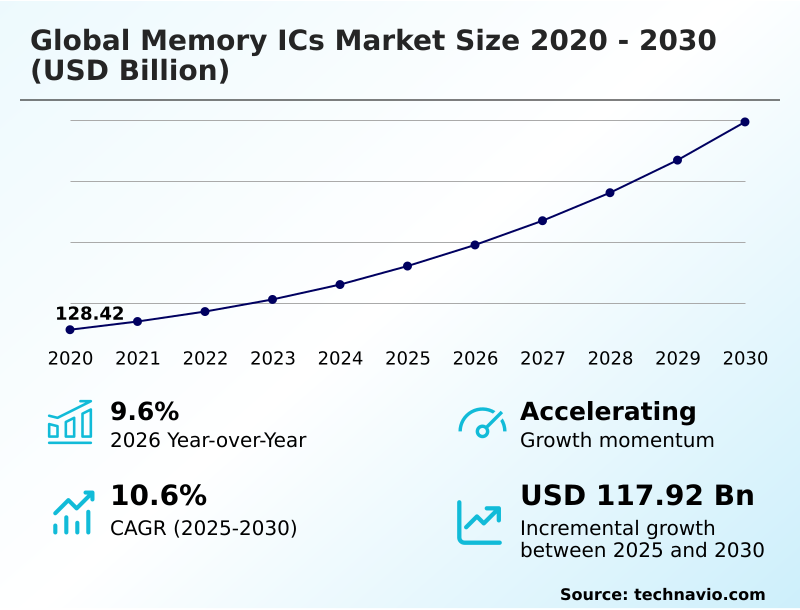

The memory ics market size is valued to increase by USD 117.92 billion, at a CAGR of 10.6% from 2025 to 2030. Proliferation of high-performance computing and AI will drive the memory ics market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 59.6% growth during the forecast period.

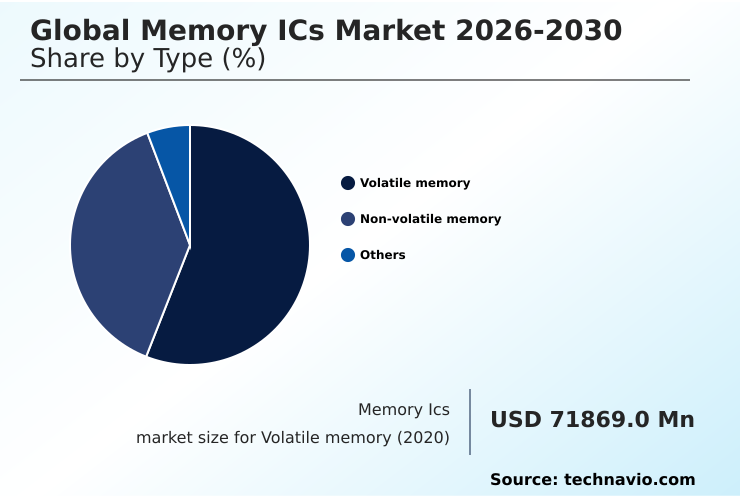

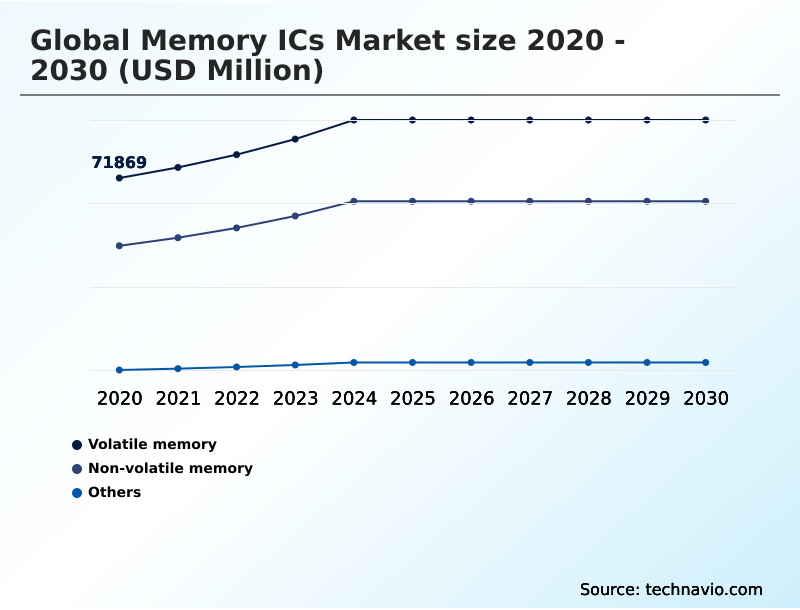

- By Type - Volatile memory segment was valued at USD 91.34 billion in 2024

- By End-user - Consumer electronics segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 170.00 billion

- Market Future Opportunities: USD 117.92 billion

- CAGR from 2025 to 2030 : 10.6%

Market Summary

- The memory ICs market is undergoing a critical transformation, driven by the insatiable data demands of artificial intelligence and cloud computing. The necessity for high bandwidth memory (HBM) and faster dynamic random access memory (DRAM) is reshaping data center architectures and influencing enterprise capital expenditure.

- In a typical business scenario, a financial services firm can leverage memory-centric infrastructure to reduce latency in high-frequency trading algorithms, gaining a competitive edge. However, the industry grapples with the immense costs and technical complexities of scaling manufacturing processes, such as the move to extreme ultraviolet lithography.

- Geopolitical factors also introduce significant supply chain risks, compelling a strategic re-evaluation of global fabrication footprints. Simultaneously, the automotive sector's shift toward autonomous systems creates a new, high-growth vertical that demands automotive-grade memory components with exceptional reliability and endurance.

- The ongoing trend of disaggregating memory using protocols like Compute Express Link (CXL) further signals a shift toward more flexible and efficient hardware utilization, balancing performance with total cost of ownership.

What will be the Size of the Memory Ics Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Memory Ics Market Segmented?

The memory ics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Volatile memory

- Non-volatile memory

- Others

- End-user

- Consumer electronics

- IT and telecommunication

- Automotive

- Healthcare

- Others

- Application

- Smartphone and tablets

- Data centers and servers

- Automotive electronics

- Industrial electronics

- Others

- Geography

- APAC

- China

- Japan

- South Korea

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- APAC

By Type Insights

The volatile memory segment is estimated to witness significant growth during the forecast period.

Volatile memory, which requires continuous power to retain data, is a primary pillar of the memory ICs market.

This segment, featuring dynamic random access memory (DRAM) and high bandwidth memory (HBM), is essential for high-performance computing (HPC) and artificial intelligence frameworks where low-latency performance is critical.

The industry-wide transition to Double Data Rate 5 (DDR5) standards reflects a commitment to enhancing both bandwidth and power efficiency, with the new architecture delivering up to a 50% increase in data transfer rates over its predecessor.

The adoption of advanced packaging techniques and system-on-chip (SoC) integration supports the escalating computational workloads in hyperscale data centers. This evolution addresses the memory bandwidth bottleneck, ensuring that processing power and data accessibility remain synchronized in modern computing environments.

The Volatile memory segment was valued at USD 91.34 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 59.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Memory Ics Market Demand is Rising in APAC Request Free Sample

The geographic landscape of the memory ICs market is dominated by the APAC region, which accounts for nearly 60% of the market's incremental growth and serves as the primary hub for semiconductor fabrication facilities.

This concentration is driven by massive investments in wafer fabrication processes and advanced packaging techniques. North America remains a critical design and consumption hub, home to major hyperscale data centers and designers of high-end encryption-ready memory for enterprise applications.

In Europe, the focus is on automotive grade memory and embedded memory solutions for the Industrial Internet of Things (IIoT), supported by government initiatives to bolster local production.

The technical pursuit of storage density enhancement continues globally, with new architectures enabling a 15% improvement in data retention and endurance, a key factor for software-defined storage deployments in mission-critical systems.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic planning within the global memory ICs market 2026-2030 now requires a deep understanding of evolving technological benchmarks and use-case-specific demands. Decision-makers are constantly evaluating ddr5 vs ddr4 performance benchmarks to justify infrastructure upgrades, while mobile device manufacturers focus on lpddr5x power consumption advantages to extend battery life.

- For server architects, the key question is how to leverage cxl for memory expansion modules to build more flexible systems. The feasibility of these advancements hinges on resolving 3d nand vertical scaling challenges and optimizing hbm for ai training workloads. Furthermore, ensuring compliance with automotive grade memory reliability standards is non-negotiable for vehicle systems.

- The selection of an nvme ssd for data centers depends on balancing performance with enterprise ssd endurance ratings. In parallel, the growth of the IoT is fueled by edge computing low power memory and non-volatile memory for iot devices. The industry's ability to innovate is tied to mastering euv lithography in dram production and exploring mram as a sram replacement.

- For storage solutions, qlc nand adoption in consumer ssds is a key cost-reduction strategy. The demand for volatile memory in high-performance computing is balanced by the need for embedded flash for microcontrollers. Data retention in automotive electronics and reducing latency with cxl memory are critical for safety and performance.

- Finally, the use of stacked dram for graphics cards and the development of phase change memory for storage-class memory are redefining performance expectations, forcing businesses to analyze twice as many supply chain variables for strategic sourcing.

What are the key market drivers leading to the rise in the adoption of Memory Ics Industry?

- The proliferation of high-performance computing and artificial intelligence is the key driver propelling market growth.

- Market growth is primarily propelled by the data-intensive requirements of next-generation applications.

- The proliferation of AI and high-performance computing (HPC) has created an insatiable demand for high bandwidth memory (HBM), with AI training workloads requiring memory capacities that are over 5 times larger than traditional server configurations.

- In the automotive sector, the rise of software-defined vehicles equipped with advanced driver-assistance systems (ADAS) is a major driver; these systems can generate over 1 terabyte of data per hour, necessitating robust volatile memory and solid state storage.

- The expansion of 5G and the Industrial Internet of Things (IIoT) further fuels demand for low power double data rate (LPDDR) memory in edge computing environments, enabling localized data processing and real-time analytics for improved operational efficiency.

What are the market trends shaping the Memory Ics Industry?

- The strategic migration toward DDR5 and LPDDR5X architectures is a significant upcoming market trend, driven by the escalating demands of global computing ecosystems.

- Key market trends are centered on architectural innovations that address escalating data demands. The adoption of Compute Express Link (CXL) is pivotal, enabling disaggregated memory architectures that can improve hardware utilization in data centers by over 30%. This shift facilitates memory pooling, significantly enhancing the efficiency of heterogeneous computing environments.

- Concurrently, the relentless scaling of 3D NAND flash memory, now surpassing 300 layers, drives storage density enhancement. This vertical integration allows manufacturers to increase capacity for enterprise-grade solid-state drives and consumer devices. The transition to DDR5 memory is also critical, doubling the effective bandwidth compared to previous generations, which directly benefits next-generation sequencing and other data-intensive applications.

- These advancements are supported by hybrid bonding technology and the exploration of novel materials like Ferroelectric RAM (FeRAM).

What challenges does the Memory Ics Industry face during its growth?

- Geopolitical volatility and macroeconomic uncertainty constitute a key challenge affecting the industry's growth trajectory.

- The memory ICs market confronts significant headwinds from both geopolitical and technical fronts. Geopolitical supply chain risk, stemming from regional manufacturing concentration, creates volatility and forces costly diversification strategies.

- The capital expenditure intensity required for a new semiconductor fabrication facility has increased by over 200% in the last decade, with extreme ultraviolet lithography (EUV) systems representing a substantial portion of this cost. At the technical level, engineers face challenges with process node shrinkage, including quantum tunneling effects that impact data integrity.

- Resource-intensive fabrication, which consumes millions of gallons of water daily, is also under scrutiny, with water usage at leading fabs increasing by 15% year-over-year. Overcoming these hurdles while maintaining high-yield manufacturing and achieving circular economy principles remains a primary strategic focus.

Exclusive Technavio Analysis on Customer Landscape

The memory ics market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the memory ics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Memory Ics Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, memory ics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Analog Devices Inc. - Specialized non-volatile memory solutions are engineered for high-reliability industrial and aerospace applications, focusing on data integrity in demanding operational environments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Analog Devices Inc.

- Changxin Technology Group Co. Ltd

- Fujitsu Ltd.

- GigaDevice Semiconductor Inc

- Infineon Technologies AG

- Integrated Silicon Solution Inc

- Kioxia Corp.

- Macronix International Co Ltd

- Microchip Technology Inc.

- Micron Technology Inc.

- ON Semiconductor Corp.

- Renesas Electronics Corp.

- ROHM Co. Ltd.

- Samsung Electronics Co. Ltd.

- Silicon Motion Technology Corp.

- SK hynix Co. Ltd.

- Solidigm

- STMicroelectronics NV

- Winbond Electronics Corp.

- Yangtze RST Co., Ltd

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Memory ics market

- In September 2024, Samsung Electronics Co. Ltd. announced a strategic partnership with a leading automotive Tier-1 supplier to develop next-generation LPDDR5X memory solutions for autonomous driving platforms, aiming to enhance real-time data processing capabilities.

- In November 2024, Micron Technology Inc. launched its new portfolio of enterprise-grade SSDs featuring 300+ layer 3D NAND technology, specifically targeting the performance and endurance requirements of hyperscale data center workloads.

- In February 2025, SK hynix Co. Ltd. confirmed a multi-billion dollar investment to construct a new HBM4 production line, directly addressing the escalating demand for high-bandwidth memory from AI accelerator manufacturers.

- In April 2025, Kioxia Corp. demonstrated a breakthrough in its BiCS FLASH technology, achieving a significant increase in bit density for QLC NAND that enhances storage capacity for consumer devices without increasing physical footprint.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Memory Ics Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 317 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 10.6% |

| Market growth 2026-2030 | USD 117921.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 9.6% |

| Key countries | China, Japan, South Korea, India, Australia, Indonesia, US, Canada, Mexico, Germany, France, UK, Italy, The Netherlands, Spain, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The memory ICs market is fundamentally defined by the continuous innovation in core technologies such as dynamic random access memory (dram) and non-volatile memory (nvm), which are foundational to all digital systems. The industry's trajectory is increasingly dictated by the requirements of high-performance computing (hpc) and artificial intelligence, driving the adoption of high bandwidth memory (hbm) and stacked dram architecture.

- Boardroom decisions on infrastructure investment are now directly influenced by the potential of compute express link (cxl) to create disaggregated memory architectures, which can reduce total data center operational costs by over 20%. This shift necessitates advancements in 3d nand flash memory, with quad-level cell (qlc) and triple-level cell (tlc) technologies pushing storage density limits.

- The development of automotive grade memory is critical for software-defined vehicles, while enterprise-grade solid-state drives are essential for hyperscale data centers. Manufacturing these complex devices relies on a capital-intensive wafer fabrication process, including extreme ultraviolet lithography (euv) and advanced packaging techniques within a semiconductor fabrication facility.

- As silicon-based manufacturing approaches physical limits, the industry explores alternatives like magnetoresistive random access memory (mram) and phase-change memory (pcm) to ensure future progress.

What are the Key Data Covered in this Memory Ics Market Research and Growth Report?

-

What is the expected growth of the Memory Ics Market between 2026 and 2030?

-

USD 117.92 billion, at a CAGR of 10.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Volatile memory, Non-volatile memory, and Others), End-user (Consumer electronics, IT and telecommunication, Automotive, Healthcare, and Others), Application (Smartphone and tablets, Data centers and servers, Automotive electronics, Industrial electronics, and Others) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Proliferation of high-performance computing and AI, Geopolitical volatility and macroeconomic uncertainty

-

-

Who are the major players in the Memory Ics Market?

-

Analog Devices Inc., Changxin Technology Group Co. Ltd, Fujitsu Ltd., GigaDevice Semiconductor Inc, Infineon Technologies AG, Integrated Silicon Solution Inc, Kioxia Corp., Macronix International Co Ltd, Microchip Technology Inc., Micron Technology Inc., ON Semiconductor Corp., Renesas Electronics Corp., ROHM Co. Ltd., Samsung Electronics Co. Ltd., Silicon Motion Technology Corp., SK hynix Co. Ltd., Solidigm, STMicroelectronics NV, Winbond Electronics Corp. and Yangtze RST Co., Ltd

-

Market Research Insights

- The memory ICs market is shaped by intense capital expenditure intensity and the constant need to overcome process node shrinkage challenges. Advanced driver-assistance systems (ADAS) in the automotive sector now generate data volumes that have increased memory requirements by over 300% compared to previous vehicle generations.

- Concurrently, the adoption of disaggregated architectures in data centers is improving total cost of ownership (TCO) by increasing resource utilization by up to 40%. Geopolitical supply chain risk remains a key concern, influencing strategic decisions around localized production. Innovations in power management integrated circuits (PMICs) are also critical, contributing to enhanced system efficiency.

- The industry's focus on high-yield manufacturing is essential to manage costs amid escalating complexity, while over-the-air (OTA) updates for software-defined vehicles create new demands for durable and secure non-volatile memory.

We can help! Our analysts can customize this memory ics market research report to meet your requirements.

RIA -

RIA -