Metal Forging Market Size 2026-2030

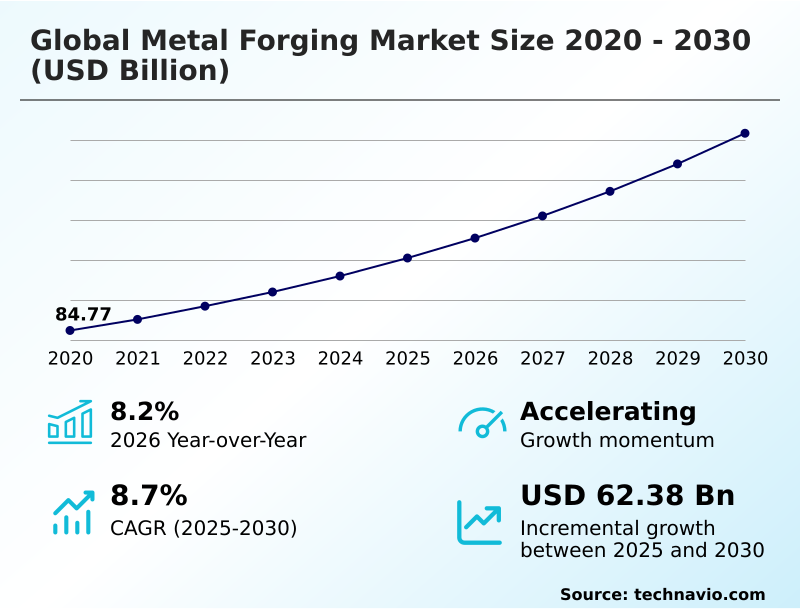

The metal forging market size is valued to increase by USD 62.38 billion, at a CAGR of 8.7% from 2025 to 2030. Resurgence of global automotive sector and transition to electric mobility will drive the metal forging market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 61.1% growth during the forecast period.

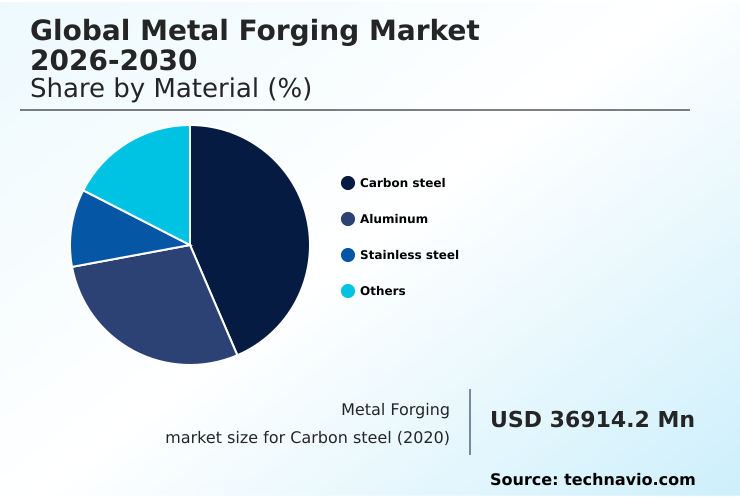

- By Material - Carbon steel segment was valued at USD 49.19 billion in 2024

- By Application - Automotive segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 98.60 billion

- Market Future Opportunities: USD 62.38 billion

- CAGR from 2025 to 2030 : 8.7%

Market Summary

- The metal forging market is defined by the manufacturing of high-strength components through processes that refine metal's internal grain structure, delivering superior durability for critical applications. The industry is driven by demand from the automotive, aerospace, and energy sectors, where performance and reliability are non-negotiable. A key trend is the adoption of lightweighting strategies, where aluminum forging solutions are pivotal.

- For instance, an automotive OEM aiming to improve electric vehicle range can substitute heavier parts with forged aluminum components, a move that requires significant capital expenditures but enhances vehicle efficiency. This transition toward advanced materials and processes like precision forging technologies is crucial.

- However, the market faces challenges from supply chain volatility and the need for skilled labor to operate complex machinery. Forgers must balance investments in technology, such as digital twin technology for process optimization, with the need to manage fluctuating raw material costs to maintain profitability and meet the evolving demands of a technologically advancing industrial landscape.

What will be the Size of the Metal Forging Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Metal Forging Market Segmented?

The metal forging industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

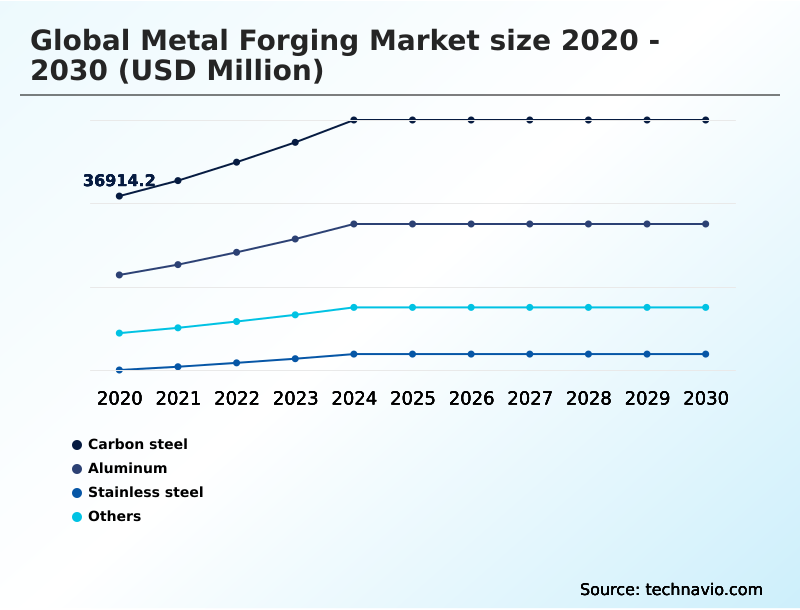

- Material

- Carbon steel

- Aluminum

- Stainless steel

- Others

- Application

- Automotive

- Aerospace and defense

- Others

- Type

- Shafts

- Gears

- Bearings

- Others

- Method

- Open die forging

- Closed die forging

- Seamless rolled ring forging

- Geography

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Material Insights

The carbon steel segment is estimated to witness significant growth during the forecast period.

Carbon steel forging remains fundamental for high-volume production, valued for its balance of strength and cost-effectiveness. The material’s inherent properties, enhanced by metallurgical expertise, are critical for heavy-duty forged components used in industrial infrastructure.

Processes like hot and warm forging transform steel into high-performance forged parts such as forged crankshafts and forged axle beams, ensuring superior fatigue resistance and structural integrity.

As manufacturers face high capital expenditures, process optimization is key, with advanced forging techniques improving material properties by over 15%, ensuring components meet stringent performance demands.

The Carbon steel segment was valued at USD 49.19 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 61.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Metal Forging Market Demand is Rising in APAC Get Free Sample

The APAC region leads market expansion, driven by its vast industrial base. This region is a hub for titanium alloy forging and working with nickel-based superalloys for aerospace.

The production of forged landing gear and forged turbine discs requires advanced techniques like induction hardening and the use of vacuum-degassed steels and high-carbon chromium alloys.

In North America, the focus is on high-strength forged structural components, which benefit from improved torsional strength and load-bearing capacity. These advanced materials ensure superior rolling contact stress performance, which has increased component lifespan by an average of 20%.

The precise circumferential grain flow achieved through these methods is critical for safety-critical applications.

Market Dynamics

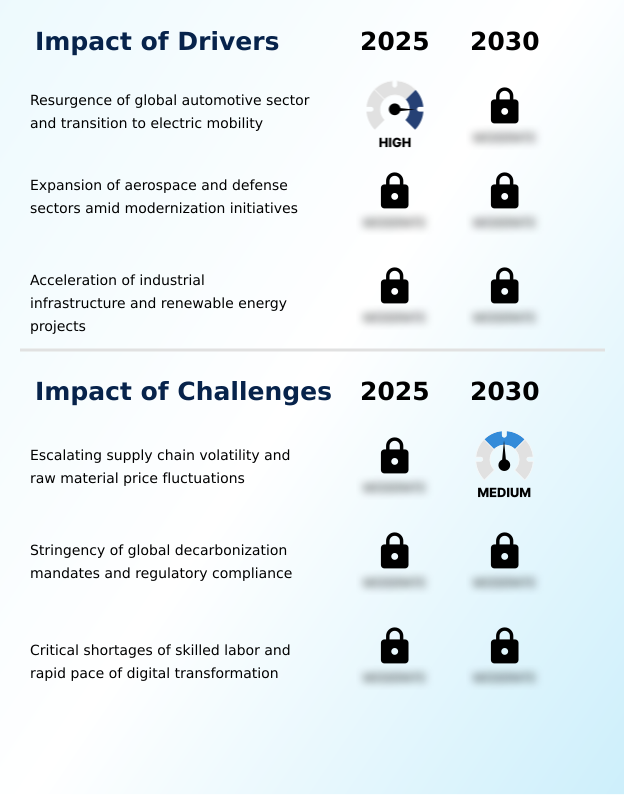

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of the market is evident in the specialized approaches being adopted across key sectors. The methods for forging processes for automotive crankshafts are being refined for greater durability, while lightweight aluminum forging for electric vehicles is becoming critical for extending battery range. In aerospace, titanium forging in aerospace engine components is pushing performance boundaries.

- Manufacturing techniques are also diversifying, with open die forging for large industrial shafts catering to heavy industry, and closed die forging for complex structural parts enabling intricate designs. The renewable energy sector relies on seamless rolled rings for wind turbine bearings to ensure reliability.

- Strategically, the industry is focused on decarbonization strategies in metal forging operations and using digital twin simulation for forging die wear to cut costs. The impact of skilled labor on forging automation highlights a critical operational challenge, while mitigating raw material price volatility in forging remains a top financial priority.

- Specific applications like stainless steel forging for corrosive environments and forging techniques for high-performance nickel alloys showcase material specialization. The cost impact of near-net-shape forging is a key consideration, alongside advancements in isothermal forging processes. Furthermore, circular economy applications in metal forging are gaining traction, supported by agentic AI for forging process control optimization.

- The market also sees innovations in precision forging for high-torque transmission gears, enhanced heat treatment processes for forged components, and a constant focus on comparing cast versus forged component strength. Finally, the growing need for forging high-purity aluminum for defense applications underscores the material's strategic importance, with new methods improving purity levels by over 10% compared to traditional smelting.

What are the key market drivers leading to the rise in the adoption of Metal Forging Industry?

- The resurgence of the global automotive sector, coupled with the industry-wide transition to electric mobility, serves as a key market driver.

- The shift toward lightweighting strategies is a major driver, with aluminum forging solutions enhancing the strength-to-weight ratio in electric vehicles, improving efficiency by up to 10%. Demand for forged transmission gears and forged connecting rods remains strong.

- The expansion of renewable energy projects fuels the need for forged power generation components, including seamless rolled ring forging for wind turbines.

- Supply chain resilience is strengthened by using green forging lubricants and developing forged railway wheels, which meet decarbonization mandates. These applications rely on localized compressive forces to improve load-bearing capacity by over 25%.

What are the market trends shaping the Metal Forging Industry?

- The proliferation of digital twins and agentic AI in shop floor operations is an upcoming market trend. This is poised to revolutionize manufacturing efficiency and process optimization.

- The market is rapidly adopting digital twin technology and agentic artificial intelligence to enhance operational efficiency. These systems enable advanced material flow simulation and thermal gradient monitoring, leading to a more than 20% improvement in predictive maintenance accuracy. Through precision forging technologies like isothermal forging and impression die forging, manufacturers achieve near-net-shape production, reducing waste.

- The integration of powder metallurgy forging and cold forging processes further supports the goal of zero-defect production, with some operations reporting a 15% reduction in material scrap.

What challenges does the Metal Forging Industry face during its growth?

- Escalating supply chain volatility and fluctuations in raw material prices represent a significant challenge affecting industry growth.

- Market stability is challenged by supply chain volatility and skilled labor shortages, which complicate production schedules for both open die forging and closed die forging. Achieving consistent dimensional accuracy and optimal grain refinement becomes more difficult under these conditions.

- The production of specialized components like forged pressure vessels and parts from micro-alloyed steels or high-purity aluminum requires strict regulatory compliance, adding complexity. Furthermore, processes such as hydraulic radial forging depend on specific material forgeability characteristics, and any disruption in sourcing stainless steel forgings can halt operations, impacting over 30% of specialized production lines.

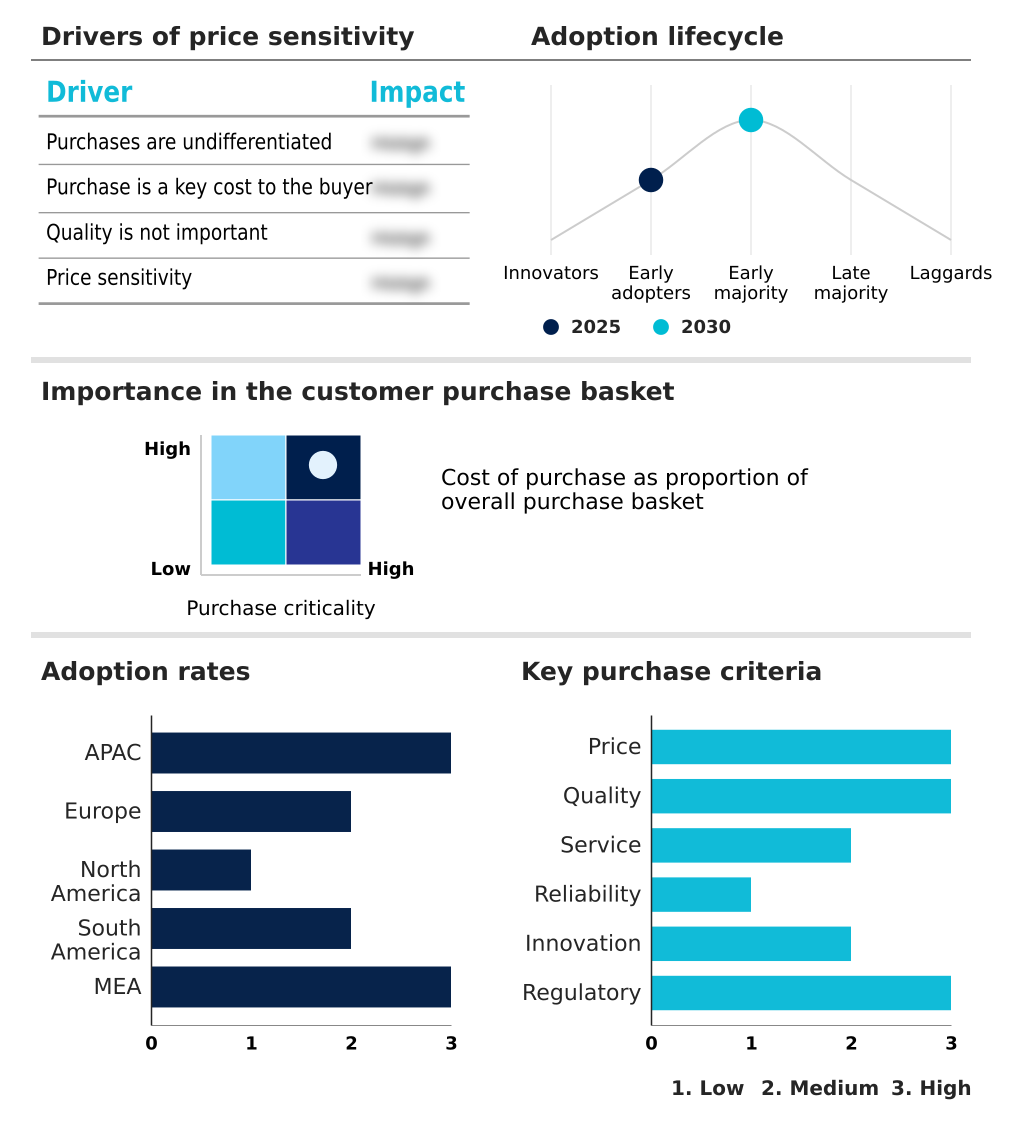

Exclusive Technavio Analysis on Customer Landscape

The metal forging market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the metal forging market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Metal Forging Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, metal forging market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aichi Steel Corp. - Delivering metal forging solutions like forged rings, flanges, and pressure vessel components for demanding applications in the aerospace and oil and gas industries.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aichi Steel Corp.

- Alicon Castalloy Ltd.

- All Metals and Forge Group

- Allegheny Technologies Inc.

- Aluminum Precision Products

- Arconic Corp.

- Asahi Forge Corp.

- Bharat Forge Ltd.

- Bluewater Thermal Solutions

- Bruck GmbH

- Consolidated Industries Inc.

- Farinia SA

- Fountaintown Forge Inc.

- Larsen and Toubro Ltd.

- Mitsubishi Steel Mfg. Co. Ltd.

- Pacific Forge Inc.

- Patriot Forge Co.

- Scot Forge Co.

- Sumitomo Heavy Industries Ltd.

- thyssenkrupp AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Metal forging market

- In September 2024, Arconic Corp. announced the commissioning of a $57.5 million expansion at its Iowa facility to significantly boost high-purity aluminum production, a critical material for advanced aerospace and defense alloys.

- In October 2024, Larsen and Toubro Ltd. announced its Minerals and Metals business secured multiple large orders, including a contract to establish a 180 KTPA aluminum smelter and a 1 MTPA coke oven battery, reinforcing its leadership in industrial infrastructure.

- In January 2025, Hilton Metal Forging announced it received RITES certification for producing Vande Bharat and LHB railway wheels, positioning it as the first private MSME to achieve this under the Make in India initiative, enabling commercial manufacturing.

- In February 2025, ZF Friedrichshafen announced the successful implementation of a new induction-heated precision forging line in Germany, designed to produce lightweight planetary gear sets for next-generation heavy-duty electric trucks.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Metal Forging Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 321 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 8.7% |

| Market growth 2026-2030 | USD 62380.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 8.2% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market's trajectory is defined by a strategic pivot toward advanced manufacturing and material science, a boardroom-level issue directly impacting long-term capital expenditures. A key focus is on metallurgical expertise to enhance the performance of high-performance forged parts and heavy-duty forged components.

- The industry utilizes a range of materials, including carbon steel forging, aluminum forging solutions, stainless steel forgings, titanium alloy forging, and nickel-based superalloys. The adoption of micro-alloyed steels, vacuum-degassed steels, high-carbon chromium alloys, and high-purity aluminum is growing.

- Key processes such as open die forging, closed die forging, and seamless rolled ring forging remain foundational, while advanced methods like isothermal forging, impression die forging, hydraulic radial forging, and powder metallurgy forging are gaining traction. Techniques including hot and warm forging, cold forging processes, and induction hardening are being optimized.

- This has led to the production of superior forged crankshafts, forged connecting rods, forged transmission gears, forged axle beams, forged turbine discs, and forged landing gear. Precision forging technologies are delivering a 15% improvement in dimensional accuracy for forged structural components, forged railway wheels, forged pressure vessels, and forged power generation components.

- The use of green forging lubricants and the creation of specialized forged rings and flanges further underscore the industry’s evolution.

What are the Key Data Covered in this Metal Forging Market Research and Growth Report?

-

What is the expected growth of the Metal Forging Market between 2026 and 2030?

-

USD 62.38 billion, at a CAGR of 8.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Material (Carbon steel, Aluminum, Stainless steel, and Others), Application (Automotive, Aerospace and defense, and Others), Type (Shafts, Gears, Bearings, and Others), Method (Open die forging, Closed die forging, and Seamless rolled ring forging) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Resurgence of global automotive sector and transition to electric mobility, Escalating supply chain volatility and raw material price fluctuations

-

-

Who are the major players in the Metal Forging Market?

-

Aichi Steel Corp., Alicon Castalloy Ltd., All Metals and Forge Group, Allegheny Technologies Inc., Aluminum Precision Products, Arconic Corp., Asahi Forge Corp., Bharat Forge Ltd., Bluewater Thermal Solutions, Bruck GmbH, Consolidated Industries Inc., Farinia SA, Fountaintown Forge Inc., Larsen and Toubro Ltd., Mitsubishi Steel Mfg. Co. Ltd., Pacific Forge Inc., Patriot Forge Co., Scot Forge Co., Sumitomo Heavy Industries Ltd. and thyssenkrupp AG

-

Market Research Insights

- Market dynamics are increasingly shaped by the pursuit of enhanced operational efficiency and sustainability. The adoption of circular economy principles is becoming standard, with some manufacturers improving material reuse by over 25%, directly impacting bottom-line costs. Concurrently, lightweighting strategies are essential, particularly in automotive applications, where an improved strength-to-weight ratio can increase fuel efficiency by 5-8%.

- These initiatives are supported by advancements in material forgeability and process optimization. However, the industry grapples with decarbonization mandates and skilled labor shortages, which challenge production continuity. For firms to thrive, they must balance investments in digital twin technology for predictive maintenance with efforts to build supply chain resilience against persistent volatility, ensuring long-term competitiveness.

We can help! Our analysts can customize this metal forging market research report to meet your requirements.

RIA -

RIA -