Metallurgical Coal Market Size 2026-2030

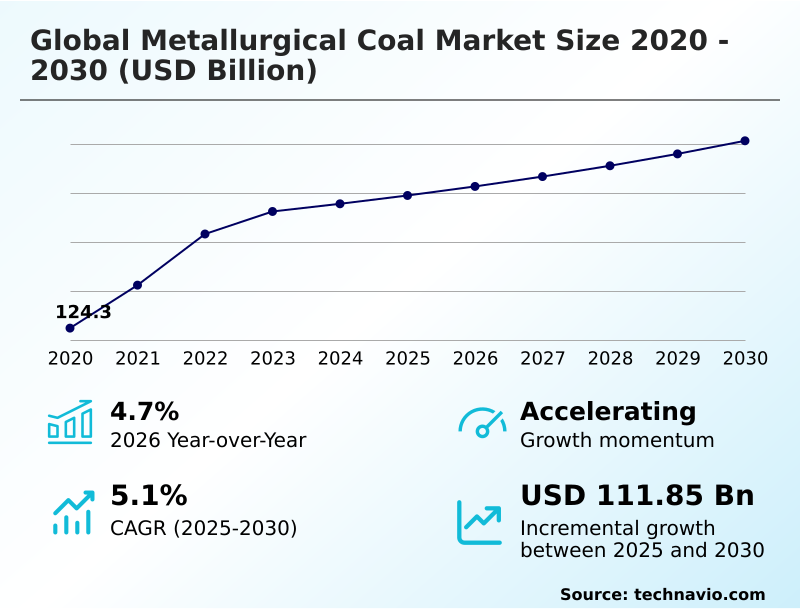

The metallurgical coal market size is valued to increase by USD 111.85 billion, at a CAGR of 5.1% from 2025 to 2030. Increasing demand for steel in various industries will drive the metallurgical coal market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 60.3% growth during the forecast period.

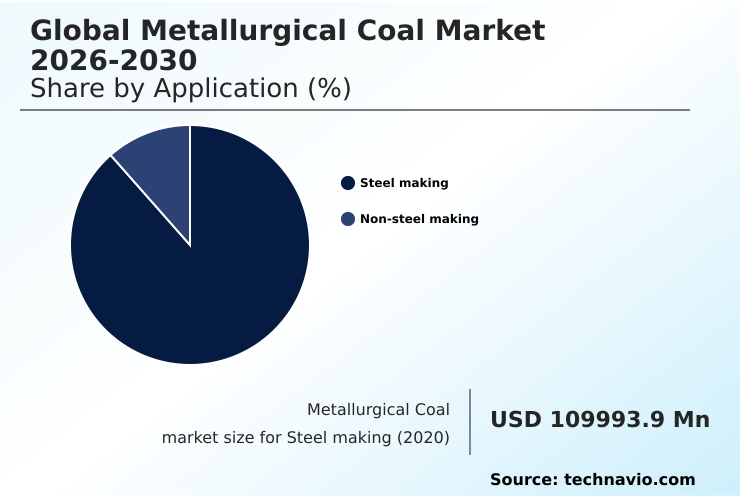

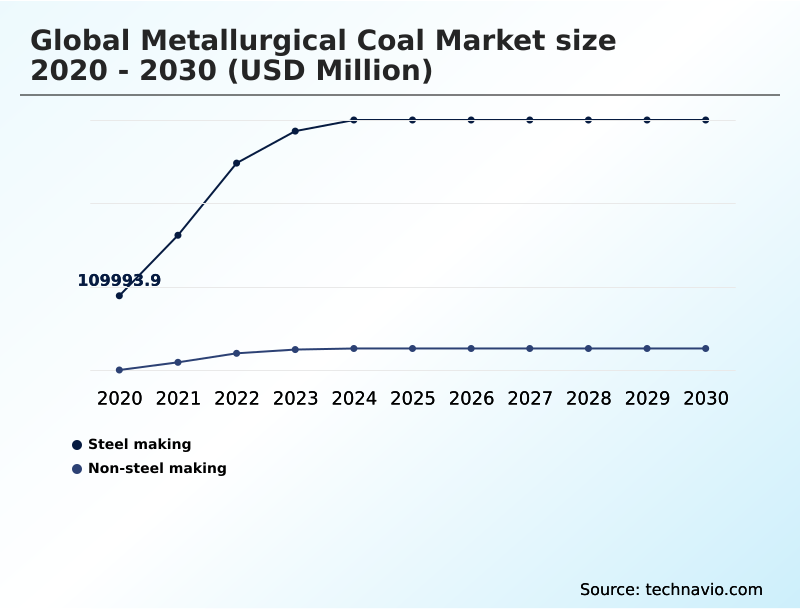

- By Application - Steel making segment was valued at USD 336.57 billion in 2024

- By Type - Hard coking coals segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 383.17 billion

- Market Future Opportunities: USD 111.85 billion

- CAGR from 2025 to 2030 : 5.1%

Market Summary

- The metallurgical coal market is a fundamental pillar of the global industrial economy, providing the essential carbon reductant agent for primary steelmaking. This specialized resource, predominantly hard coking coal and semi-soft coking coal, is converted into metallurgical coke through coal carbonization. This coke is indispensable in the blast furnace for iron ore reduction and pig iron production.

- Market dynamics are shaped by the relentless demand from infrastructure and manufacturing sectors, juxtaposed with the decarbonization challenge pushing for green steel pathway innovations. A key business scenario involves steel producers optimizing their coal blending strategies, combining different grades like low volatile coal and high volatile coal to manage costs while meeting stringent quality standards for coke strength after reaction.

- This balancing act between securing high-grade met coal and managing the carbon footprint from a carbon-intensive industry defines the sector's operational landscape. The efficient management of the coking byproduct stream further enhances economic viability, illustrating the industry's move towards greater resource use efficiency.

What will be the Size of the Metallurgical Coal Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Metallurgical Coal Market Segmented?

The metallurgical coal industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Steel making

- Non-steel making

- Type

- Hard coking coals

- Semi-soft coking coals

- Pulverized coal injection

- End-user

- Iron and steel industry

- Foundry industry

- Chemical and pharmaceutical

- Others

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- APAC

By Application Insights

The steel making segment is estimated to witness significant growth during the forecast period.

The steelmaking segment is the cornerstone of the metallurgical coal market, representing the primary demand driver for high-quality carbon resources.

This application is defined by the consumption of coking coal in the primary steelmaking process, where it is converted into metallurgical coke within specialized ovens.

This coke is essential for the blast furnace, acting as a reductant for pig iron production and providing structural support. Steel mill procurement focuses on securing high-quality metallurgical coal, particularly prime hard coking coal, to ensure an efficient metallurgical process.

The specifications for this steelmaking feedstock are stringent, as the quality of infrastructure and manufactured goods depends on it, with some facilities reporting a 15% improvement in furnace efficiency through optimized coal blending.

The Steel making segment was valued at USD 336.57 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

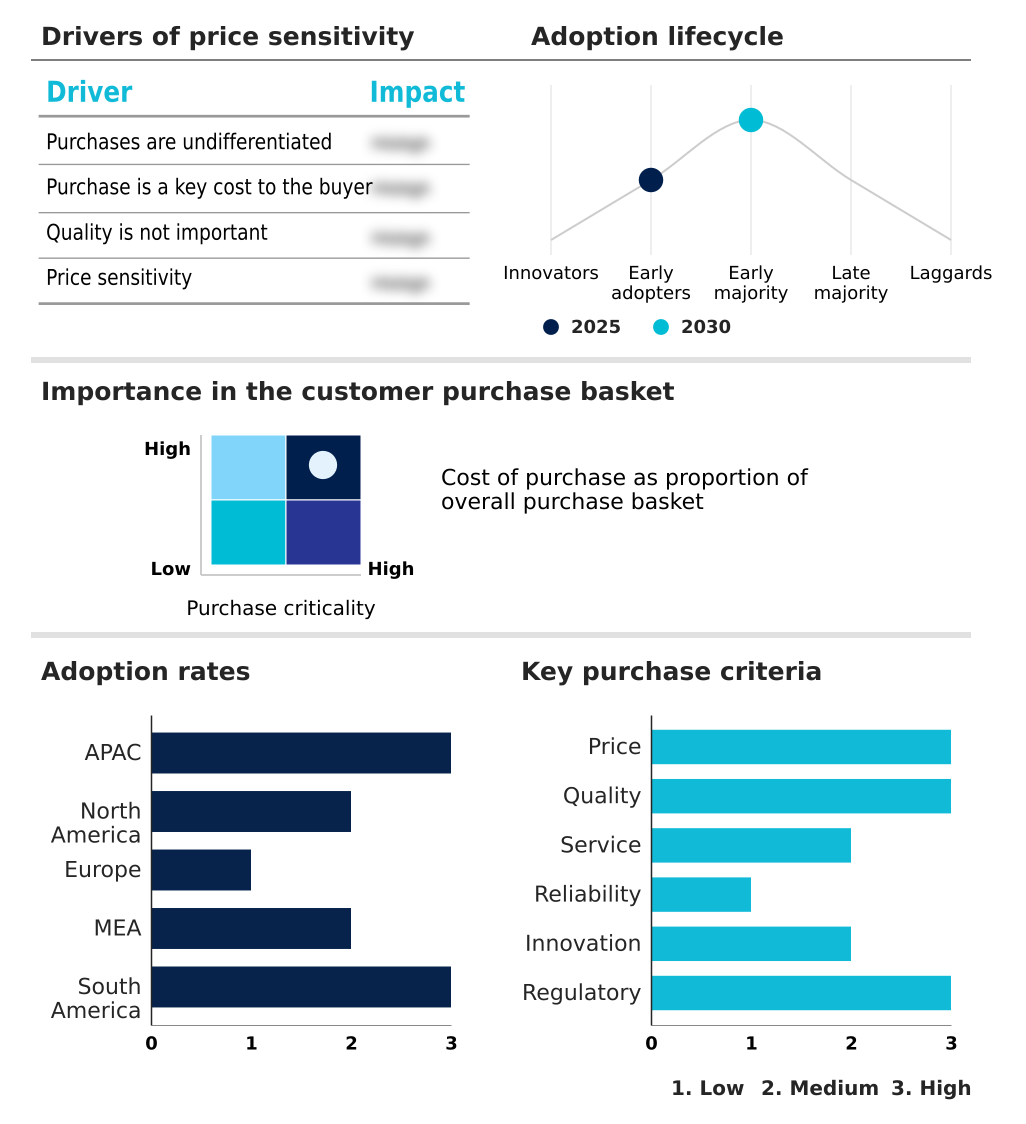

APAC is estimated to contribute 60.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Metallurgical Coal Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the metallurgical coal market is dominated by APAC, which accounts for over 60% of the incremental growth. This is driven by massive steel production in countries like China and India to support infrastructure development.

North America, particularly the US and Canada, serves as a key supplier of high-quality hard coking coal, leveraging its advanced deep mining and surface mining operations.

Europe remains a significant consumer but is heavily import-dependent and faces intense decarbonization pressure, leading to a focus on coke rate reduction and R&D into steelmaking alternatives.

In South America, Colombia is a notable exporter of metallurgical coke from its many beehive coke oven operations.

The global flow of this steelmaking feedstock relies on a complex network of seaborne supply chain logistics, connecting resource-rich regions with major industrial centers and highlighting the interconnectedness of global primary steelmaking.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Navigating the global metallurgical coal market 2026-2030 requires a deep understanding of several interconnected factors. The impact of price volatility on metallurgical coal remains a primary concern for steelmakers, where unhedged procurement can lead to margin erosion that is twice as severe as in more stable commodity markets.

- This volatility is exacerbated by the ESG investment impact on the coal sector, which restricts capital for new mine development and resource extraction optimization, potentially creating future supply bottlenecks. Concurrently, stringent regulations for carbon pollution in steelmaking are forcing operators to invest in byproduct recovery and gas capture technologies to mitigate their carbon footprint.

- In response, many are exploring advanced technologies in metallurgical coal mining, including automation and digital mine twin platforms, to boost efficiency. The role of metallurgical coal in smart city infrastructure continues to be significant, as high-strength steel is essential for modern construction.

- Finally, byproduct valuation in the coking process, where coal tar and benzene are sold, provides a crucial secondary revenue stream that supports the economic viability of the entire carbon-intensive industry.

What are the key market drivers leading to the rise in the adoption of Metallurgical Coal Industry?

- Increasing demand for steel across various industries, including construction, automotive, and manufacturing, serves as a key driver for the metallurgical coal market.

- Market growth is fundamentally driven by the global demand for primary steelmaking, which relies on metallurgical coke as a key carbon reductant agent.

- Urbanization and infrastructure projects require vast amounts of steel, sustaining demand for iron ore reduction in the blast furnace.

- The economic viability of this process is enhanced by the high value of byproducts like coal tar and ammonia, which are essential to the chemical industry, promoting resource use efficiency.

- Innovations such as pulverized coal injection and sophisticated coal blending techniques allow steelmakers to reduce the coke rate and manage costs.

- These methods have improved blast furnace efficiency by over 10% in modern mills, ensuring that even as the industry faces decarbonization pressure, the demand for high-grade met coal remains robust.

What are the market trends shaping the Metallurgical Coal Industry?

- The increasing number of smart city projects worldwide is an emerging market trend, stimulating demand for specialized steel products and bolstering the metallurgical coal market.

- Key trends are reshaping the market, driven by technological adoption and sustainability goals. The use of advanced digital mine twin platforms allows for precise coal seam geology mapping, improving resource extraction optimization by up to 15%. This is complemented by the rollout of mining automation systems, which enhance safety and productivity in both deep mining and surface mining operations.

- In processing, modernized coal washing plants are achieving lower ash content and lower sulphur content, producing a higher-quality steelmaking feedstock. Concurrently, the push toward a circular economy principle is elevating the importance of the coking byproduct stream, with improved recovery of valuable chemicals. These advancements collectively support a more efficient metallurgical process and a degree of carbon footprint management.

What challenges does the Metallurgical Coal Industry face during its growth?

- The significant volatility in the prices of metallurgical coal presents a key challenge to the industry, impacting financial planning and investment stability for both miners and steel producers.

- The market faces significant challenges, primarily from raw material pricing volatility and increasing environmental regulation. The financial sector's shift toward stringent ESG investment criteria has led to widespread investment divestment from the coal sector, making it difficult to fund new mineable reserves and increasing capital costs by over 25% for some projects.

- This capital scarcity threatens the long-term seaborne supply chain. Furthermore, as a historically carbon-intensive industry, the sector is under immense pressure to decarbonize. The advent of green steel pathway technologies, though not yet at scale, represents a long-term existential threat.

- In the interim, operators must navigate complex environmental compliance rules while managing the operational realities of a capital-intensive business, making supply chain resilience a critical focus.

Exclusive Technavio Analysis on Customer Landscape

The metallurgical coal market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the metallurgical coal market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Metallurgical Coal Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, metallurgical coal market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alpha Metallurgical Resources - Key offerings include diverse grades of metallurgical coal, which are tailored and blended to meet the specific requirements of international and domestic steel producers.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alpha Metallurgical Resources

- Anglo American plc

- Alliance Resource Partners LP

- Bharat Coking Coal Ltd.

- BHP Group Ltd.

- Core Natural Resources

- Coronado Global Resources Inc.

- EVRAZ Plc

- Glencore Plc

- Idemitsu Kosan Co. Ltd.

- Marubeni Corp.

- Mitsubishi Corp.

- Nippon Steel Corp.

- Peabody Energy Corp.

- POSCO Co. Ltd.

- Ramaco Resources Inc.

- Sojitz Corp.

- Warrior Met Coal Inc.

- Whitehaven Coal Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Metallurgical coal market

- In October 2025, Anglo American announced progress on the divestment of its steelmaking coal portfolio to align its long-term strategy toward metals required for the energy transition.

- In July 2025, Cleveland Cliffs highlighted an increase in its domestic steel production capacity to meet surging demand from the automotive industry for high-strength steel components.

- In June 2025, BHP published a report detailing the successful rollout of an autonomous haulage fleet at its major metallurgical coal mines, improving operational productivity and safety.

- In May 2025, ArcelorMittal stated it was accelerating efforts to meet new European carbon reduction targets by modifying existing coking facilities to integrate cleaner processing units.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Metallurgical Coal Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 300 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.1% |

| Market growth 2026-2030 | USD 111850.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.7% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The metallurgical coal market remains integral to the global industrial framework due to its role in pig iron production and as a primary steelmaking feedstock. The conversion of coking coal into metallurgical coke via coal carbonization in a coke oven is a foundational process that currently has no scalable, cost-effective alternative for virgin steel production.

- Key quality metrics such as low ash content, low sulphur content, coke strength after reaction (CSR), and coke reactivity index (CRI) dictate the suitability of different coal grades, including prime hard coking coal and blends of high and low volatile coal.

- While the industry grapples with its identity as a carbon-intensive industry, producers are innovating with byproduct recovery of chemicals like coal tar and benzene, and technologies like pulverized coal injection to improve efficiency. For instance, optimizing coal blending has been shown to reduce coke consumption by up to 10% in some blast furnace operations.

- Boardroom decisions are now centered on balancing the operational need for this critical carbon reductant agent with mounting ESG investment criteria and the long-term pursuit of sustainable mining practices.

What are the Key Data Covered in this Metallurgical Coal Market Research and Growth Report?

-

What is the expected growth of the Metallurgical Coal Market between 2026 and 2030?

-

USD 111.85 billion, at a CAGR of 5.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Steel making, and Non-steel making), Type (Hard coking coals, Semi-soft coking coals, and Pulverized coal injection), End-user (Iron and steel industry, Foundry industry, Chemical and pharmaceutical, and Others) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for steel in various industries, Volatility in prices of metallurgical coal

-

-

Who are the major players in the Metallurgical Coal Market?

-

Alpha Metallurgical Resources, Anglo American plc, Alliance Resource Partners LP, Bharat Coking Coal Ltd., BHP Group Ltd., Core Natural Resources, Coronado Global Resources Inc., EVRAZ Plc, Glencore Plc, Idemitsu Kosan Co. Ltd., Marubeni Corp., Mitsubishi Corp., Nippon Steel Corp., Peabody Energy Corp., POSCO Co. Ltd., Ramaco Resources Inc., Sojitz Corp., Warrior Met Coal Inc. and Whitehaven Coal Ltd.

-

Market Research Insights

- Market dynamics are increasingly shaped by the push for sustainable mining and a resilient seaborne supply chain. The adoption of mining automation systems has led to a 20% increase in operational efficiency at select sites, while the use of a digital mine twin for resource extraction optimization has reduced geological uncertainty by 15%.

- Steel mill procurement strategies are also evolving; while high-quality metallurgical coal remains essential for the metallurgical process, there is growing pressure from ESG investment criteria. This has spurred interest in green steel pathway technologies and greater coke oven gas utilization.

- Raw material pricing volatility and environmental regulation complexities require companies to focus on supply chain resilience and carbon footprint management to navigate the industry's ongoing transformation.

We can help! Our analysts can customize this metallurgical coal market research report to meet your requirements.

RIA -

RIA -